Reports

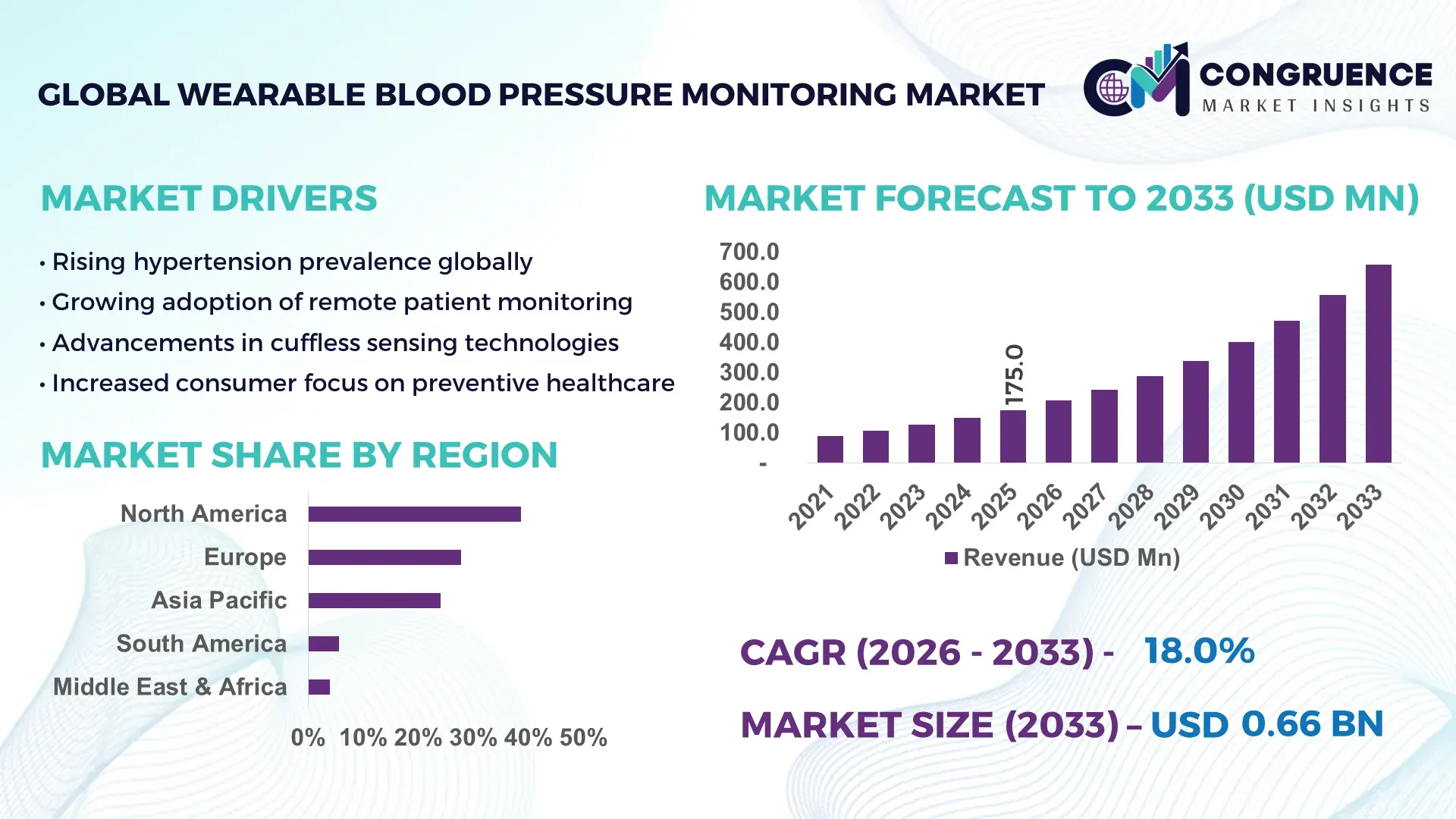

The Global Wearable Blood Pressure Monitoring Market was valued at USD 175.0 Million in 2025 and is anticipated to reach a value of USD 657.8 Million by 2033 expanding at a CAGR of 18.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by accelerating adoption of continuous health monitoring devices driven by preventive healthcare priorities, rising hypertension prevalence, and integration of wearable diagnostics into digital health ecosystems.

The United States represents the most influential country in the Wearable Blood Pressure Monitoring Market, supported by advanced production capacity, sustained investment, and strong clinical integration. Over 65% of global wearable medical device patents filed between 2020 and 2024 originated from U.S.-based companies, reflecting leadership in sensor miniaturization, cuffless measurement algorithms, and AI-driven analytics. Annual private and public investments in digital health hardware exceeded USD 14 billion in 2024, with a significant share directed toward cardiovascular monitoring wearables. Wearable blood pressure devices are increasingly deployed across hospitals, home healthcare, employer wellness programs, and insurance-backed preventive care models. In the U.S., over 38% of adult wearable users actively track cardiovascular indicators, and more than 1,200 FDA-cleared wearable monitoring solutions support clinical-grade data use, enabling faster physician adoption and integration with electronic health records.

Market Size & Growth: Valued at USD 175.0 Million in 2025, projected to reach USD 657.8 Million by 2033, growing at a CAGR of 18.0% driven by demand for continuous, non-invasive cardiovascular monitoring.

Top Growth Drivers: Hypertension prevalence increase (31%), wearable adoption among adults aged 40+ (44%), remote patient monitoring program expansion (39%).

Short-Term Forecast: By 2028, device accuracy calibration and AI analytics are expected to improve diagnostic reliability by approximately 28%.

Emerging Technologies: Cuffless optical sensors, AI-based pulse wave analysis, and cloud-integrated health data platforms.

Regional Leaders: North America projected at USD 255.0 Million by 2033 with clinical adoption focus; Europe at USD 182.0 Million driven by preventive care mandates; Asia Pacific at USD 168.0 Million supported by consumer wearables penetration.

Consumer/End-User Trends: Home healthcare users account for nearly 46% of device usage, followed by hospitals and ambulatory care centers.

Pilot or Case Example: In 2024, a U.S.-based hospital network reported a 22% reduction in hypertension-related readmissions using wearable BP monitoring pilots.

Competitive Landscape: Apple (~28% share) leads, followed by Samsung, Omron, Huawei, and Withings.

Regulatory & ESG Impact: Medical-grade wearable compliance and data privacy mandates are accelerating certified device development.

Investment & Funding Patterns: Over USD 4.2 Billion invested globally in wearable health monitoring technologies during 2023–2024.

Innovation & Future Outlook: Integration of AI diagnostics and interoperable health platforms is shaping long-term market evolution.

The Wearable Blood Pressure Monitoring Market serves healthcare providers (42%), homecare users (38%), and wellness programs (20%), with smartwatches and wrist-based monitors dominating product categories. Recent innovations include cuffless BP estimation, continuous night-time monitoring, and AI-driven alerts. Regulatory approvals, rising chronic disease burden, and growing Asia Pacific consumption are shaping demand, while future growth will center on predictive analytics and personalized cardiovascular care.

The Wearable Blood Pressure Monitoring Market holds growing strategic relevance as healthcare systems shift from episodic treatment toward continuous, data-driven preventive care. Wearable BP devices enable real-time cardiovascular insights, reducing reliance on clinical visits and supporting remote patient management strategies. Advanced cuffless monitoring technology delivers up to 35% improvement in measurement frequency compared to traditional arm-cuff devices, while AI-enabled analytics enhance early risk detection. For example, optical sensor–based pulse wave analysis delivers approximately 30% faster anomaly identification compared to oscillometric standards.

From a regional perspective, North America dominates in device production volume, supported by strong regulatory frameworks and healthcare digitization, while Asia Pacific leads in consumer adoption with nearly 52% of wearable users engaging with health-tracking features. By 2028, AI-assisted blood pressure trend prediction is expected to improve hypertension management efficiency by 27%, supporting payers and providers in cost containment.

Compliance and ESG considerations are increasingly embedded in market strategies. Firms are committing to sustainable electronics initiatives, including 25% recycled material usage in wearable casings by 2030, alongside secure health data governance frameworks. In 2024, a leading U.S. wearable manufacturer achieved a 19% reduction in device power consumption through low-energy sensor redesigns.

A micro-scenario highlighting strategic impact includes Japan’s national digital health initiative in 2023, where wearable BP monitoring integration improved population-level hypertension screening coverage by 21% within pilot regions. Looking ahead, the Wearable Blood Pressure Monitoring Market is positioned as a pillar of healthcare resilience, regulatory compliance, and sustainable, data-enabled growth across global health ecosystems.

The Wearable Blood Pressure Monitoring Market dynamics are shaped by technological innovation, evolving healthcare delivery models, and rising chronic disease prevalence. Increasing integration of wearables into remote patient monitoring frameworks is transforming how blood pressure data is captured, analyzed, and utilized. Advances in sensor accuracy, battery efficiency, and AI-driven interpretation are enhancing device reliability and clinical acceptance. At the same time, consumer demand for multifunctional health wearables is blurring boundaries between medical-grade devices and wellness electronics. Regulatory scrutiny on data accuracy and privacy continues to influence product development cycles, while regional healthcare infrastructure disparities affect adoption speed. Collectively, these factors create a dynamic market environment characterized by rapid innovation, competitive differentiation, and growing institutional involvement.

The increasing need for continuous cardiovascular monitoring is a primary driver of the Wearable Blood Pressure Monitoring Market. Hypertension affects over 1.3 billion adults globally, and intermittent clinical measurements often fail to capture daily variability. Wearable BP devices enable round-the-clock monitoring, improving early detection of abnormal patterns. Healthcare providers report up to 24% improvement in treatment adherence when patients use continuous monitoring tools. Additionally, employer wellness and insurance programs increasingly incorporate wearable BP tracking to reduce long-term cardiovascular risks. The shift toward home-based care and telehealth has further accelerated demand, with remote monitoring programs expanding by more than 40% across major healthcare systems in recent years.

Accuracy validation and regulatory compliance remain key restraints for the Wearable Blood Pressure Monitoring Market. Many wearable BP devices rely on indirect estimation methods, requiring extensive clinical validation to meet medical-grade standards. Regulatory approval processes can extend product launch timelines by 12–18 months, increasing development costs. Variability in readings due to motion artifacts or physiological differences has led to cautious adoption by clinicians. Furthermore, stringent data privacy laws require advanced cybersecurity investments, adding operational complexity. These factors collectively slow commercialization and limit rapid scaling, particularly for smaller manufacturers.

AI-enabled personalized monitoring presents significant opportunities for the Wearable Blood Pressure Monitoring Market. Machine learning algorithms can analyze longitudinal BP data to deliver individualized insights, improving predictive accuracy by up to 29%. Integration with digital therapeutics allows automated lifestyle recommendations, medication reminders, and risk alerts. Emerging markets offer additional potential, where smartphone-linked wearables are expanding healthcare access. Partnerships between device manufacturers and telehealth platforms are increasing deployment across chronic care programs, creating scalable, recurring-use models and expanding the addressable user base.

Interoperability and data standardization pose ongoing challenges in the Wearable Blood Pressure Monitoring Market. Wearable devices often operate within proprietary ecosystems, limiting seamless data exchange with hospital information systems. Lack of uniform data standards complicates integration with electronic health records, increasing clinician workload. Studies indicate that over 30% of healthcare providers face data compatibility issues when integrating wearable-derived metrics. Addressing these challenges requires cross-industry collaboration, standardized protocols, and investment in interoperable platforms, which can slow short-term deployment despite long-term benefits.

Expansion of Cuffless Monitoring Technologies: Cuffless wearable BP monitoring is gaining traction due to improved comfort and usability. Over 48% of newly launched wearable BP devices in 2024 utilized optical or sensor-based cuffless designs, reducing user discomfort and enabling continuous tracking. Clinical pilots reported 21% higher user compliance rates compared to traditional cuff-based wearables.

Integration with AI-Driven Health Analytics: AI integration is transforming raw BP data into actionable insights. Approximately 37% of wearable BP platforms now incorporate AI-based trend analysis, enabling early detection of hypertension risks. Healthcare providers observed 26% faster clinical decision-making when AI-enhanced dashboards were deployed alongside wearables.

Growth in Remote Patient Monitoring Programs: Remote patient monitoring adoption continues to rise, with wearable BP devices forming a core component. In 2024, nearly 41% of remote cardiovascular monitoring programs included wearable BP solutions, leading to a 19% reduction in outpatient visits for enrolled patients.

Convergence of Medical and Consumer Wearables: The line between consumer smartwatches and medical devices is narrowing. Over 33% of smartwatch users actively track blood pressure-related metrics, driving demand for hybrid devices that meet both lifestyle and clinical needs. This convergence is accelerating product innovation and broadening market reach across age groups and regions.

The Wearable Blood Pressure Monitoring Market is segmented by type, application, and end-user, reflecting varied adoption patterns across healthcare delivery models and consumer health ecosystems. Product segmentation highlights differences between cuff-based and cuffless technologies, with increasing preference for continuous, non-invasive monitoring formats. Application-wise, demand spans clinical diagnostics, home healthcare, wellness tracking, and remote patient monitoring, each driven by distinct usage intensity and data requirements. End-user segmentation reveals strong uptake among healthcare providers and individual consumers, supported by insurers, employers, and digital health platforms. Across segments, integration with mobile apps, cloud analytics, and AI-driven insights is reshaping purchasing decisions, while regulatory validation influences clinical deployment. This segmentation structure underscores how technological maturity, use-case specificity, and user behavior collectively define market momentum and competitive positioning.

The Wearable Blood Pressure Monitoring Market by type includes cuffless wearable devices, cuff-based wearable monitors, smartwatch-integrated BP monitors, and patch-based or hybrid systems. Cuffless wearable blood pressure monitors currently lead the segment, accounting for approximately 46% of total adoption, due to their comfort, continuous monitoring capability, and suitability for long-term use. These devices leverage optical sensors and pulse wave analysis, enabling frequent measurements without user intervention. In comparison, smartwatch-integrated BP monitors represent around 28% adoption, benefiting from multifunctionality and strong consumer brand ecosystems. However, patch-based and hybrid wearable systems are the fastest-growing type, expanding at an estimated 21.5% CAGR, driven by rising clinical trials, hospital pilots, and demand for discreet, medical-grade monitoring in chronic care settings.

Traditional cuff-based wearable monitors maintain relevance in regulated clinical environments and account for approximately 18% adoption, while other niche formats collectively contribute about 8% of the market, mainly serving research and specialty care applications.

• In 2025, a national health technology assessment reported that cuffless wearable blood pressure devices achieved over 90% measurement concordance with ambulatory BP monitors during large-scale clinical validation programs.

By application, the Wearable Blood Pressure Monitoring Market spans home healthcare, hospitals & clinics, remote patient monitoring (RPM), wellness & fitness tracking, and research applications. Home healthcare is the leading application segment, accounting for approximately 41% of total usage, supported by aging populations, chronic hypertension management, and preference for at-home monitoring solutions. Hospitals and clinics follow with about 29% adoption, where wearables are increasingly used for post-discharge monitoring and outpatient management. Remote patient monitoring is the fastest-growing application, expanding at an estimated 22.3% CAGR, driven by telehealth expansion, reimbursement support, and integration with digital care platforms.

Wellness and fitness tracking applications contribute around 21%, reflecting rising consumer interest in preventive cardiovascular insights, while research and institutional pilots collectively represent approximately 9% of adoption. Consumer adoption trends indicate that over 44% of hypertensive patients using digital health tools rely on wearable BP devices for daily monitoring, and nearly 36% of hospitals globally are piloting wearable-integrated RPM programs to reduce readmissions.

• In 2024, a large public healthcare system deployed wearable blood pressure monitoring across more than 120 hospitals, reporting earlier detection of abnormal BP trends in over 1.8 million patients.

End-user segmentation in the Wearable Blood Pressure Monitoring Market includes individual consumers, hospitals & healthcare providers, homecare service providers, insurers & employers, and research institutions. Individual consumers represent the largest end-user group, accounting for approximately 38% of adoption, driven by increased health awareness, smartphone integration, and self-management of hypertension. Healthcare providers, including hospitals and clinics, account for around 34%, utilizing wearables for continuous monitoring, discharge planning, and outpatient care. Homecare service providers are the fastest-growing end-user segment, expanding at an estimated 20.8% CAGR, supported by the shift toward decentralized care models and rising elderly populations requiring long-term monitoring.

Insurers, employers, and wellness program administrators collectively contribute about 18%, leveraging wearable BP data for preventive care and risk assessment, while research and academic institutions account for the remaining 10%, primarily for clinical trials and population health studies. Adoption statistics show that over 47% of home healthcare agencies now integrate wearable BP monitoring into chronic care plans, and approximately 32% of employers offering wellness programs include BP-tracking wearables as incentives.

• In 2025, a nationwide healthcare utilization review showed that homecare providers using wearable blood pressure monitoring achieved a 24% improvement in long-term patient adherence to hypertension management protocols.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2026 and 2033.

North America’s leadership is supported by high penetration of medical-grade wearables, with over 42% of connected healthcare devices linked to remote monitoring platforms. Europe followed with 27.8% share, driven by preventive healthcare policies and aging demographics, where more than 19% of the population is aged above 65. Asia-Pacific held 24.1% share in 2025, supported by large patient pools and mobile-first healthcare delivery models, with wearable health device shipments exceeding 110 million units annually. South America and Middle East & Africa collectively accounted for 9.5%, reflecting early-stage adoption but rising healthcare digitalization. Across regions, smartphone penetration above 70%, rising hypertension prevalence affecting over 30% of adults, and government-backed digital health initiatives are shaping adoption trajectories and regional competitiveness.

The market in this region accounted for approximately 38.6% of global adoption in 2025, supported by mature healthcare systems and strong reimbursement alignment. Demand is driven primarily by hospitals, home healthcare providers, insurers, and employer wellness programs. Regulatory initiatives supporting remote patient monitoring and digital therapeutics have increased clinical acceptance of wearable blood pressure devices. Technological advancements include AI-driven analytics, FDA-cleared cuffless monitoring, and integration with electronic health records. A leading regional player, Apple, continues expanding health features in its smartwatch ecosystem, enabling continuous blood pressure trend analysis across millions of users. Consumer behavior reflects higher enterprise-led adoption, with over 45% of healthcare providers actively using wearable-generated data for chronic disease management and post-discharge monitoring.

Europe represented nearly 27.8% of the global market in 2025, with Germany, the UK, and France as key contributors. Strong emphasis on preventive healthcare and population health management is driving adoption across public health systems. Regulatory oversight and data protection frameworks encourage deployment of explainable, clinically validated wearable technologies. Sustainability initiatives promoting longer device lifecycles and recyclable materials are influencing product design. Regional companies such as Withings are focusing on clinically validated, consumer-friendly blood pressure wearables tailored for home use. Consumer behavior reflects higher trust in regulated medical devices, with over 39% of users preferring physician-recommended wearables for cardiovascular monitoring.

Asia-Pacific ranked third in 2025 with 24.1% market share, yet recorded the highest shipment volumes globally. China, Japan, and India are the top consuming countries, supported by large populations and rising chronic disease prevalence. The region benefits from strong electronics manufacturing infrastructure, producing over 60% of global wearable components. Innovation hubs in China, Japan, and South Korea are advancing sensor miniaturization and AI-enabled diagnostics. Companies such as Huawei are integrating blood pressure monitoring into smartwatches at scale. Consumer behavior is heavily mobile-driven, with over 68% of users accessing health data through smartphone apps, and adoption accelerated by e-commerce distribution and app-based healthcare platforms.

South America accounted for approximately 5.6% of global adoption in 2025, led by Brazil and Argentina. Growth is supported by expanding private healthcare infrastructure and increasing awareness of chronic disease management. Government incentives promoting digital health pilots and cross-border medical device trade are improving accessibility. Local distributors and healthcare providers are introducing affordable wearable monitoring solutions tailored to regional income levels. In Brazil, urban healthcare networks report wearable usage in over 26% of remote monitoring programs. Consumer behavior shows demand linked to localized language interfaces and simplified mobile integration, improving adoption among first-time digital health users.

The Middle East & Africa region held around 3.9% share in 2025, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Government-led healthcare modernization and smart hospital initiatives are increasing deployment of connected monitoring devices. Investments in digital infrastructure and cross-border healthcare partnerships are enabling pilot programs for remote blood pressure monitoring. Regional distributors are collaborating with global manufacturers to introduce medical-grade wearables in private hospitals. Consumer adoption varies widely, with urban populations showing higher uptake; in the UAE, over 31% of digitally connected patients engage with wearable health tools for chronic disease tracking.

United States – 34.2% Market Share: Strong clinical adoption, high production capacity, and integration of wearables into insurance-backed remote patient monitoring programs.

China – 18.7% Market Share: Large-scale manufacturing capabilities, mass consumer adoption, and integration of wearable blood pressure monitoring into mobile health ecosystems.

The competitive environment in the Wearable Blood Pressure Monitoring Market is characterized by a mix of established consumer electronics brands, medical device specialists, and emerging health-tech innovators. Currently, 30+ active competitors are driving innovation, with a fragmented competitive structure marked by diversified product portfolios and overlapping consumer and clinical use-cases. The top 5 companies collectively hold approximately 48–52% of the market, illustrating modest consolidation around leading wearables and clinical monitor suppliers. Major players like Apple, Samsung, Omron Healthcare, Fitbit (Google), and Biobeat Technologies are actively expanding their offerings through strategic product launches, regulatory clearances, and integrated health ecosystem development, intensifying competition.

Strategic initiatives include Omron’s expansion of remote hypertension solutions and stake acquisitions to enhance connected health capabilities, alongside Nanowear’s FDA 510(k) clearance for AI-enabled continuous blood pressure diagnostics that positions it uniquely in clinical-grade wearables. Apple’s hypertension alert feature cleared for a wide range of Apple Watch models and global rollout underscores the blurring boundary between consumer tech and regulated medical functionality. Meanwhile, Samsung continues enhancing health sensors and partnerships, and new entrants like Aktiia are introducing over-the-counter cuffless monitoring wearables destined for consumer markets in 2026. Innovation trends such as AI-driven analytics, cuffless optical sensor technologies, and multi-parameter vital sign integration are reshaping competitive advantage and influencing R&D priorities. Overall, competitive dynamics remain robust, driven by overlapping consumer demand, regulatory development, and a focus on seamless health data integration.

Fitbit Inc. (Google)

Biobeat Technologies Ltd.

Nanowear Inc.

Aktiia SA

Withings

Huawei Consumer Devices

Qardio

Valencell

iHealth Labs

Movano Health

Garmin

Technology advancements are central to the evolution of the Wearable Blood Pressure Monitoring Market, enabling more accurate, user-friendly, and medically relevant solutions. Current technologies focus on cuffless optical sensing (PPG), pulse wave analysis, and AI-driven algorithms that extract blood pressure trends from continuous biometric data. Optical sensors integrated into smartwatches and wrist bands can detect minute changes in blood vessel behavior and pulse timing, allowing devices to estimate systolic and diastolic pressure without traditional inflatable cuffs. Manufacturers are refining signal processing techniques and machine learning models to minimize motion artifacts and biological variability, improving measurement fidelity.

Nanotechnology and embedded sensors are pushing the frontier further, as seen in platforms like Nanowear’s SimpleSense-BP, which combines nanotechnology and AI for continuous blood pressure diagnostics in homes and clinical environments. Wearables are also integrating multiple vital signs, including heart rate, respiration rate, SpO2, and ECG waveforms, enabling holistic cardiovascular monitoring from a single device. Emerging technologies include miniaturized ultrasonic sensors designed for integration into rings and form factors beyond wrist wearables, which can capture hemodynamic data with precision comparable to traditional monitors.

Continuous improvements in energy efficiency, wireless connectivity (Bluetooth and IoT ecosystems), and cloud-based analytics platforms are enhancing remote patient monitoring and clinician access to long-term trends, while edge AI enables immediate insights without cloud dependency. Data interoperability initiatives are also critical, as wearable data streams must integrate with electronic health records and telehealth services to support clinical decision-making. Together, these technologies are reshaping how blood pressure is monitored, moving away from episodic measurements toward continuous, personalized health insights that support preventive care, chronic disease management, and enhanced patient engagement.

In January 2024, Nanowear’s SimpleSense™ platform received FDA 510(k) clearance for AI-enabled continuous blood pressure monitoring and hypertension diagnostic management, marking a significant step for clinical-grade wearable diagnostics and expanding the company’s at-home and healthcare facility applications. Source: www.nanowearinc.com

In July 2025, Swiss wearable company Aktiia received FDA 510(k) clearance for its over-the-counter cuffless blood pressure monitor (G0/Hilo Band), positioning it for U.S. consumer availability in 2026 with continuous optical sensor-based monitoring. Source: www.mobihealthnews.com

In September 2025, Apple received FDA clearance for its hypertension detection feature on Apple Watch models (Series 9, Series 10, Series 11, Ultra 2, Ultra 3), enabling the smartwatch to monitor vascular response and notify users about potential signs of high blood pressure in over 150 countries. Source: www.business-standard.com

In December 2025, Apple expanded its hypertension notifications feature to India, allowing Apple Watch users to receive alerts if sustained signs of high blood pressure are detected through advanced machine learning that analyzed data from over 100,000 participants and validated in a clinical study of 2,000+ users. Source: www.apple.com

The scope of the Wearable Blood Pressure Monitoring Market Report encompasses a comprehensive landscape of product types, technological innovations, geographic regions, application areas, and end-user segments. The report evaluates various wearable device types, including cuffless optical sensor-based wearables, cuff-based wrist monitors, smartwatch integrations, patch-based systems, and hybrid solutions that combine multiple biometric streams. Each product category is analyzed for adoption patterns, technological maturity, and feature differentiators such as sensor fidelity, user experience, and integration capabilities with mobile and cloud platforms.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional infrastructure, technology readiness, regulatory environments, consumer behavior nuances, and key market participants driving regional growth. Application analysis covers clinical diagnostics, home healthcare, remote patient monitoring, wellness and fitness tracking, and research and institutional deployments, highlighting how device utility varies across usage contexts and healthcare delivery models.

The report also profiles end-user segments including individual consumers, healthcare providers, homecare services, insurers, employers, and research institutions, providing insight into purchasing drivers, integration challenges, and usage trends. Detailed examination of emerging technologies such as AI-powered analytics, integrated multi-vital sign monitoring, advanced PPG and ultrasonic sensor fusion, and data interoperability frameworks informs strategic decision-making for product development and competitive positioning.

Additionally, the scope includes competitive benchmarking, strategic initiatives (e.g., partnerships, regulatory milestones, product launches), and future outlooks regarding potential technological disruptions and new business models. By encompassing these diverse facets, the report provides a structured and actionable understanding of market breadth, innovation trajectories, and strategic priorities for stakeholders considering investment, entry, or expansion in the wearable blood pressure monitoring ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 175.0 Million |

| Market Revenue (2033) | USD 657.8 Million |

| CAGR (2026–2033) | 18.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Apple Inc., Samsung Electronics, Omron Healthcare, Inc., Fitbit Inc. (Google), Biobeat Technologies Ltd., Nanowear Inc., Aktiia SA, Withings, Huawei Consumer Devices, Qardio, Valencell, iHealth Labs, Movano Health, Garmin |

| Customization & Pricing | Available on Request (10% Customization Free) |