Reports

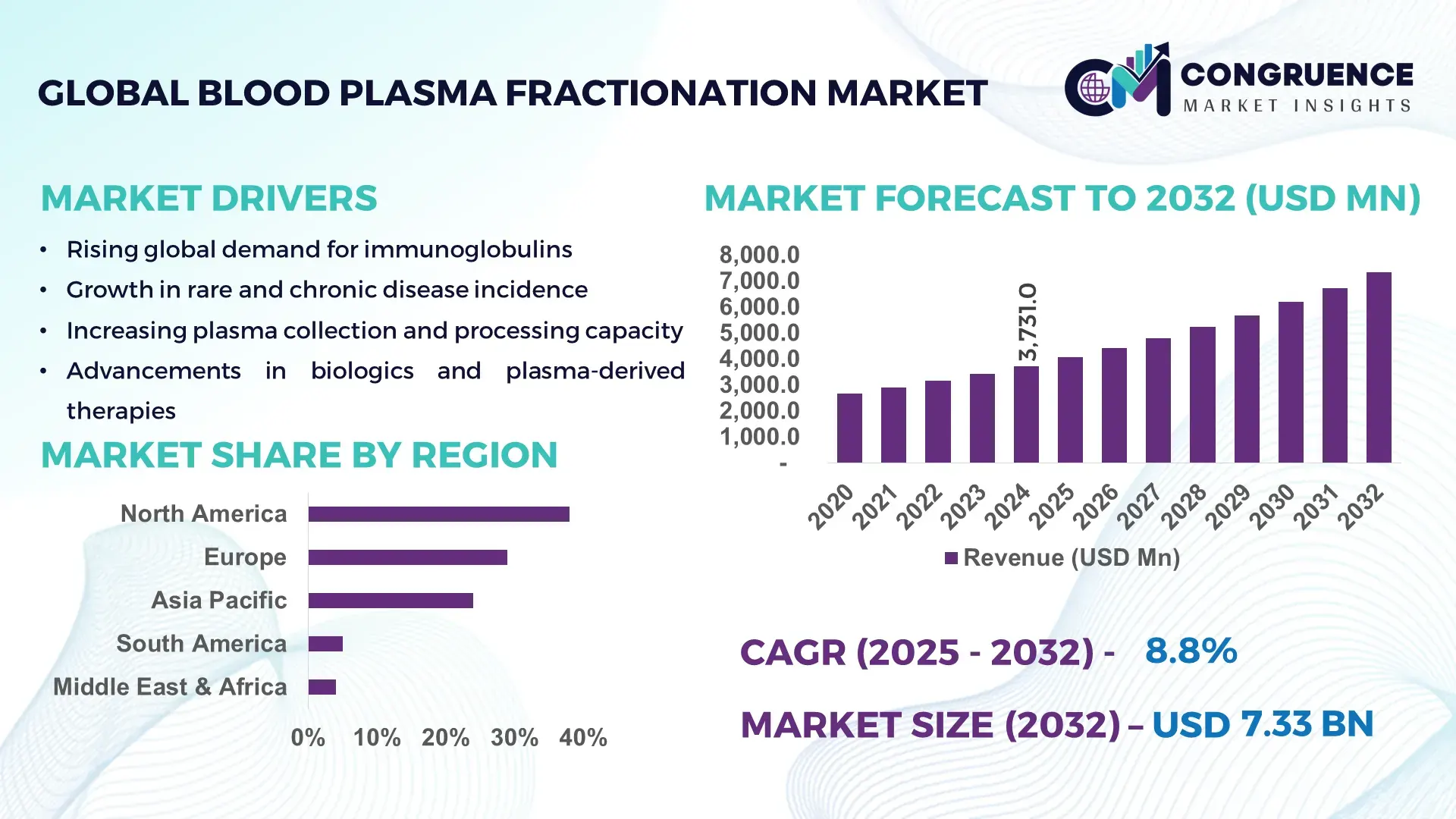

The Global Blood Plasma Fractionation Market was valued at USD 3,731.0 Million in 2024 and is anticipated to reach a value of USD 7,325.8 Million by 2032, expanding at a CAGR of 8.8% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is supported by rising therapeutic demand for immunoglobulins and continuous expansion in plasma collection and processing capacity.

The United States holds a leading position driven by the world’s largest plasma collection network and advanced industrial-scale fractionation facilities. The country processes millions of liters of plasma annually, supported by extensive donor-center infrastructure and multi-hundred-million-dollar capital investments in high-throughput purification, virus inactivation, and automated downstream lines. U.S. facilities have adopted advanced filtration, chromatography, and real-time analytical control systems, enabling year-on-year improvements in batch consistency and manufacturing yields across immunoglobulin, albumin, and coagulation factor product classes.

Market Size & Growth: Valued at USD 3,731.0 Million in 2024, projected to reach USD 7,325.8 Million by 2032 with an 8.8% CAGR; demand driven by increased clinical utilization of immunoglobulins.

Top Growth Drivers: Immunotherapy adoption (35%), improved collection capacity (22%), and expanded diagnostic use (18%).

Short-Term Forecast: By 2028, process optimization initiatives expected to reduce operational costs by ~12%.

Emerging Technologies: Continuous chromatography systems, advanced virus-inactivation platforms, and digital process-analytics integration.

Regional Leaders: North America projected to reach USD 20B by 2032 (high collection density); Europe expected at USD 12B (advanced regulation); Asia Pacific at USD 8B (fastest growth in clinical uptake).

Consumer/End-User Trends: Rising home-infusion adoption, expanding immunology and neurology patient base, and growing demand for subcutaneous immunoglobulin treatments.

Pilot or Case Example: A 2024 operational pilot improved downstream processing efficiency by 28% and cut cycle time by 18%.

Competitive Landscape: Global leader holds ~30% share; other key players include CSL, Grifols, Takeda, Baxter, and Octapharma.

Regulatory & ESG Impact: Strengthened GMP frameworks, enhanced donor-safety expectations, and emerging mandates for traceability and environmental efficiency.

Investment & Funding Patterns: Several hundred million USD in recent capacity expansions, technology upgrades, and strategic acquisitions.

Innovation & Future Outlook: Adoption of process-intensification platforms, expansion of domestic fractionation hubs, and deeper integration of digital twins and PAT systems.

Key industry sectors—immunology therapeutics, albumin solutions, and coagulation factors—contribute most to overall demand. Continuous purification technologies and single-use systems are shortening production timelines and improving purity metrics. Regulatory encouragement for domestic processing, regional consumption growth, and advancements in virus inactivation are shaping product innovation and long-term capacity planning.

The Blood Plasma Fractionation Market plays a central strategic role in global healthcare delivery due to its link to essential biologics used for chronic immunological, neurological, and hematological conditions. Companies are focusing on strengthening donor-center pipelines, optimizing fractionation throughput, and expanding global manufacturing footprints to ensure uninterrupted access to plasma-derived therapies. New technology platforms—such as continuous purification, digital quality control, and automated viral inactivation—are improving yields, reducing downtime, and enabling faster lot release. For example, newer multicolumn continuous chromatography systems deliver up to 25% improved productivity compared with older batch purification methods, supporting higher output without proportional facility expansion.

Regional dynamics shape these strategies. North America leads in volume due to extensive donor infrastructure, while Europe leads in technology adoption with automation rates exceeding many global markets. By 2027, digital process-analytics systems are expected to improve real-time release testing efficiency by more than 15%. Organizations across regions are also aligning with ESG targets, with commitments to reduce water and energy consumption in plasma processing by 10–20% by 2030.

A recent scenario illustrates measurable impact: in 2024, an upgraded U.S. facility integrating automated purification modules achieved an 18% improvement in batch throughput and a 12% reduction in processing time. These advancements reinforce the market’s trajectory toward more resilient and sustainable production ecosystems. The Blood Plasma Fractionation Market is positioned to remain a critical pillar of therapeutic security, regulatory compliance, and sustainable capacity expansion across global healthcare systems.

The Blood Plasma Fractionation Market operates within a complex framework of rising therapeutic needs, technological modernization, regulatory oversight, and strategic global capacity expansion. Increasing diagnosis of immunodeficiencies and autoimmune disorders continues to elevate demand for plasma-derived products, while the expansion of donor-center networks enhances supply stability. The industry is shifting toward process intensification, with advanced chromatographic systems and single-use modules enhancing efficiency and product purity. Regulatory frameworks further drive investments in traceability, quality assurance, and pathogen-control technologies. At the same time, increased investment in regional fractionation hubs and improvements in supply-chain coordination are helping manufacturers reduce bottlenecks and improve production agility for high-demand therapies such as immunoglobulins and albumin.

Demand for plasma-derived therapies continues to accelerate as the global burden of immunodeficiency and autoimmune diseases increases. Immunoglobulin usage has grown consistently across neurology, hematology, and primary immunodeficiency care. To meet this demand, manufacturers are expanding donor-center networks, improving donation-frequency programs, and investing in high-throughput fractionation lines. Collection volumes have risen significantly in key regions, allowing greater production stability. Advanced filtration and purification technologies also enable higher product yields, supporting the long-term scalability of immunoglobulin and albumin supply. These combined factors create sustained upward momentum for production and capacity expansion across the entire market ecosystem.

Regulatory compliance remains one of the most stringent challenges in the Blood Plasma Fractionation Market. Donor eligibility rules, pathogen-screening protocols, and multi-stage testing requirements significantly increase operational complexity. Batch release can be delayed by multi-layer verification standards, impacting inventory cycles. Additionally, plasma supply remains vulnerable to fluctuations in donor recruitment, local policy changes, and workforce limitations at collection centers. The capital-intensive nature of fractionation facilities—requiring long build-out and qualification periods—further restricts rapid capacity expansion. Together, these factors slow operational agility and complicate long-term production planning.

Process intensification technologies present major opportunities for increasing throughput, improving purity, and lowering manufacturing costs. Continuous chromatography, automated virus inactivation, and integrated digital analytics significantly boost efficiency, enabling cost-effective production of both high-volume and specialty plasma-derived biologics. Regional capacity expansion—especially in Asia Pacific and Latin America—offers opportunities for localized manufacturing that strengthens supply security and reduces import dependence. Emerging digital donor-management tools are improving donor retention and optimizing scheduling. Together, these advancements enable faster scaling, stronger resilience, and increased flexibility in meeting clinical demand.

High capital intensity presents a substantial challenge, as plasma fractionation plants require large upfront investment, sophisticated infrastructure, and extensive validation timelines. Donor-supply volatility adds another layer of uncertainty, with donation rates influenced by economic conditions, regulatory changes, and operational capacity at collection centers. Fluctuating supply forces manufacturers to maintain safety stocks or face underutilized processing lines. Rising costs for energy, consumables, and testing reagents add to operational pressures. Together, these challenges limit rapid scaling and require robust financial and supply-chain strategies to ensure stable output.

Expansion of modular and prefabricated facility design: Adoption of modular cleanrooms and prefabricated process units is accelerating construction timelines. Approximately 55% of recent facility projects reported measurable reductions in on-site labor requirements and overall build time, enabling faster commissioning of high-capacity fractionation lines in North America and Europe.

Process intensification through continuous purification: Continuous and multicolumn chromatographic systems are showing productivity gains of 15–25%, with some implementations reporting 2–4× throughput increases compared with legacy batch systems. Facilities adopting these technologies have also demonstrated cycle-time reductions of up to 28% and buffer-consumption efficiency gains exceeding 30%.

Accelerated regional investment in domestic fractionation capacity: Countries are increasing investment in domestic plasma processing, with multi-hundred-million-dollar expansions supporting additional 1–2 million liters of annual fractionation capacity. This trend strengthens national supply resilience and reduces dependency on imported plasma-derived products.

Digital optimization of collection and production workflows: Digital process-analytics tools and donor-engagement platforms are delivering measurable improvements in operational stability. Early adopters report 10–15% reductions in lot-release timelines, improved demand forecasting accuracy, and enhanced coordination across collection, transport, and fractionation stages, resulting in more consistent product availability.

The market is segmented based on type, application, and end-user industries, each contributing differently to overall adoption patterns and commercial relevance. Product types vary in sophistication, purity levels, and clinical utility, forming a multi-layered competitive landscape driven by innovation, rising demand for advanced therapies, and expanding diagnostic capabilities. Applications span therapeutic care, immune system modulation, critical care support, and specialty medical treatments, reflecting the growing burden of chronic diseases and the need for high-precision biological solutions. End-users—including hospitals, clinics, research laboratories, and biopharmaceutical companies—play a defining role in shaping procurement priorities, quality requirements, and technology integration. Overall, segmentation insights highlight a market influenced by both established demand centers and fast-growing niches, with notable differences in product uptake, technological advancement, and institutional readiness across regions.

The market comprises immunoglobulins, albumin, coagulation factors, protease inhibitors, and several specialty plasma-derived products. Immunoglobulins represent the leading segment with approximately 48% market share, driven by rising cases of primary immunodeficiency, autoimmune disorders, and broader prescribing in neurology and rheumatology. For comparison, albumin accounts for around 21%, while coagulation factors hold nearly 15% of the market. The fastest-growing product category is coagulation factors, expanding at an estimated 11.2% CAGR, propelled by the increasing global prevalence of hemophilia and enhanced access to replacement therapies in emerging markets. Albumin continues to serve critical roles in fluid replacement, burn management, and liver disease, though its growth remains steady rather than rapid. Specialty plasma fractions and protease inhibitors collectively contribute roughly 16% to total adoption, primarily in niche areas such as hereditary angioedema, organ transplantation support, and acute pancreatitis therapy.

Applications of plasma-derived products span immunology, hematology, critical care, neurology, and infectious disease management. Immunology remains the leading segment with about 44% market share, supported by widespread therapeutic use of immunoglobulins for immune deficiencies, autoimmune disorders, and inflammatory diseases. In comparison, hematology applications account for around 26%, while critical care and neurology represent 18% collectively. The fastest-growing application area is neurology, expanding at approximately 10.4% CAGR, driven by increasing use of immunoglobulins in conditions like chronic inflammatory demyelinating polyneuropathy (CIDP) and myasthenia gravis, along with improved diagnostic accuracy enabling earlier intervention. Other applications—including infectious disease management and organ support therapy—jointly represent nearly 12%, with demand rising due to heightened awareness of rare disorders and improved hospital infrastructure. Consumer and institutional adoption trends reinforce these patterns; for instance, over 38% of global healthcare systems in 2024 reported initiating or expanding biological therapy programs, while more than 60% of caregivers and patients expressed higher trust in biologic-based interventions compared to conventional treatments.

End-users include hospitals, specialty clinics, diagnostic laboratories, and biopharmaceutical companies. Hospitals dominate the market with approximately 52% market share, reflecting their central role in administering therapies for immune disorders, hematologic conditions, and acute care cases. Specialty clinics account for about 23%, while diagnostic and research laboratories represent roughly 14%. Biopharmaceutical companies hold an estimated 11%, primarily linked to product development, R&D, and clinical testing. The fastest-growing end-user segment is specialty clinics, expanding at nearly 9.8% CAGR, fueled by decentralization of care, rising outpatient treatment adoption, and increasing volumes of immune and neurological therapy administered outside large hospitals. Remaining end-users collectively contribute around 25%, supported by the rapid modernization of healthcare systems, rising clinical research activities, and broader clinical trial participation across regions. Broader adoption trends reinforce this shift: over 42% of hospitals in the United States reported piloting integrated biologic-administration programs in 2024, while more than 58% of emerging-market clinics introduced expanded immunology service lines to meet rising patient demand.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.4% between 2025 and 2032.

Europe followed with approximately 29% share, while Asia-Pacific captured 24%, demonstrating rapidly increasing plasma collection capacity, modernization of healthcare infrastructure, and rising demand for immunoglobulins. South America and the Middle East & Africa collectively contributed around 9%, with growing investments in specialty biologics and improved access to hematology and immunology treatments. Region-wise analysis highlights distinct differences in availability of plasma collection centers, regulatory frameworks, patient demographics, and clinical adoption patterns, all of which shape the diverse performance of the Blood Plasma Fractionation Market across global markets.

North America holds a dominant position with approximately 38% share of the global Blood Plasma Fractionation Market, supported by advanced healthcare systems, large patient populations requiring immunoglobulins and coagulation factors, and strong plasma donation networks. Key industries driving demand include immunology, neurology, hematology, and emergency medicine, where biologics-based therapies remain central to treatment protocols. The region has implemented notable regulatory enhancements, including strengthened biologics safety monitoring and incentives for expanding plasma collection facilities. Technological advancements such as digital donor screening, automated fractionation lines, and AI-supported quality analytics further enhance production efficiency. Local players contribute significantly; for example, a leading biopharmaceutical manufacturer expanded its plasma collection footprint by over 15% in 2024 across the United States to meet rising immunoglobulin demand. Consumer behavior in the region is shaped by higher enterprise and healthcare adoption of digital platforms, with patients showing increasing preference for biologic therapies supported by real-time clinical monitoring and personalized treatment plans.

Europe accounts for roughly 29% of the Blood Plasma Fractionation Market, with major markets including Germany, the United Kingdom, France, Italy, and Spain driving both production and consumption. The region’s demand is reinforced by strong hospital networks, an aging population, and high diagnosis rates for immune and hematologic disorders requiring plasma-derived therapies. Regulatory bodies enforce stringent quality frameworks and support sustainability initiatives aimed at optimizing plasma sourcing and improving traceability across the supply chain. Adoption of advanced fractionation technologies, automation tools, and biologics analytics platforms continues to strengthen laboratory and manufacturing capabilities. Local players remain integral to the ecosystem; one prominent European plasma processor increased fractionation capacity by nearly 12% in 2024 to address rising immunoglobulin treatment requirements. Consumer behavior trends reflect increasing demand for safe, transparent, and clinically validated therapies, with regulatory pressure pushing institutions toward more explainable and data-driven biologics decisions.

Asia-Pacific ranks as the fastest-growing regional market and represents approximately 24% of global volume, driven by rapidly expanding consumption in China, India, Japan, South Korea, and Australia. China alone accounts for more than 40% of regional usage due to large patient populations and increasing production capacity. India and Japan follow as key therapeutic and manufacturing hubs. The region is witnessing major infrastructure improvements: expanded plasma donation programs, new high-throughput fractionation facilities, and accelerating regulatory modernization. Technology adoption—including digital diagnostics, automated biological testing, and AI-driven inventory management—is also advancing rapidly. Local companies continue to increase clinical availability; one leading manufacturer in East Asia launched new immunoglobulin formulations in 2024, improving supply stability for more than 1.2 million patients. Consumer behavior in the region shows strong engagement with mobile health platforms and rapid growth in e-health ecosystems, supported by rising awareness of biologics and access to specialized treatments.

South America contributes nearly 5% to the global Blood Plasma Fractionation Market, with key countries such as Brazil, Argentina, and Chile driving consumption. Brazil alone accounts for about 58% of the region’s usage due to its large clinical infrastructure and widespread adoption of immunology and hematology treatments. The region is undergoing notable infrastructure improvements, including expanded biologics testing capabilities and investment in public research facilities. Government incentives related to healthcare modernization, local manufacturing partnerships, and streamlined import regulations further support therapy availability. A leading healthcare group in Brazil enhanced its diagnostic and therapeutic biologics program in 2024, increasing patient throughput by 18%. Consumer behavior patterns emphasize strong demand for localized medical content, multilingual patient support, and expanded hospital-based biologic services, closely tied to regional growth in media and language-access platforms.

The Middle East & Africa region represents approximately 4% of the global Blood Plasma Fractionation Market, with major growth markets including the UAE, Saudi Arabia, South Africa, and Egypt. Demand is shaped by expanding healthcare systems, rising diagnoses of chronic immune disorders, and increased investment in specialty biologics. Industries such as construction, energy, and infrastructure development drive economic growth that indirectly supports advancements in medical technologies. Regulatory frameworks are evolving, with new trade partnerships and procurement policies aimed at improving access to plasma-derived therapies. Technological modernization is accelerating, with hospitals adopting digital diagnostic tools and automated laboratory systems. A regional biotechnology firm expanded its clinical distribution network by 22% in 2024 to supply more immunoglobulin therapies across Gulf countries. Consumer behavior trends show growing trust in advanced biologics, increased preference for specialist care, and rising demand for hospital-administered therapies.

United States – 32% Market Share: Dominance driven by the world’s largest plasma collection network and strong demand from immunology and neurology specialties.

Germany – 14% Market Share: Leadership supported by advanced biologics manufacturing capacity and high treatment adoption rates across public and private hospitals.

The Blood Plasma Fractionation Market is characterized by a moderately consolidated competitive landscape, with approximately 18–22 globally active competitors operating across plasma collection, fractionation, and distribution. The top five companies collectively command around 62% of the global market, reflecting strong vertical integration and long-standing expertise in immunoglobulin and coagulation factor production. Competition is shaped by investments in high-throughput fractionation capacity, portfolio diversification, and clinical innovation. More than 40 large plasma collection networks are active worldwide, significantly influencing supply stability and pricing dynamics.

Key strategic initiatives include cross-border partnerships aimed at expanding plasma sourcing, acquisitions designed to strengthen product pipelines in critical therapeutic areas, and the launch of advanced purification systems offering higher yield efficiency. Several companies have initiated automation and digital transformation programs—such as AI-enabled donor screening, electronic batch traceability, and real-time biologics quality monitoring—to enhance operational efficiency. Competitive intensity continues to rise as emerging players in Asia-Pacific and the Middle East invest in modern facilities and seek regulatory approvals for immunoglobulin, albumin, and specialty plasma-derived products. Overall, the environment is shaped by supply-chain security, innovation scale, regulatory compliance, and expanding patient needs.

Octapharma AG

Kedrion S.p.A.

Bio Products Laboratory (BPL)

Biotest AG

China Biologic Products Holdings, Inc.

Hualan Biological Engineering Inc.

ADMA Biologics, Inc.

Technological innovation plays a pivotal role in shaping the Blood Plasma Fractionation Market, with advancements in purification, automation, and analytics significantly improving efficiency, safety, and production scalability. Modern fractionation facilities increasingly deploy high-capacity chromatographic systems, capable of improving protein yield by 8–12%, while reducing processing time. Membrane chromatography, caprylate precipitation, and nanofiltration technologies have become mainstream, enabling the removal of impurities including viruses, prions, and host-cell proteins with heightened accuracy. Automated plasma separation systems now operate with precision levels exceeding 99%, reducing manual error and improving batch consistency.

Digital transformation is accelerating across the industry. AI-driven demand forecasting tools, predictive maintenance systems, and digital donor management platforms are being implemented to optimize both supply and production. More than 55% of major market participants have adopted electronic batch record (EBR) systems to enhance quality assurance and regulatory compliance. Furthermore, robotics-assisted purification modules, real-time biologics monitoring sensors, and IoT-enabled facility environments are minimizing variability, increasing throughput, and enabling highly standardized operations globally.

Emerging technologies include next-generation fractionation lines designed for energy efficiency, plasma protein stabilizers that extend shelf life, and advanced filtration techniques capable of isolating low-abundance therapeutic proteins with higher purity. As precision diagnostics evolve, demand for specialized plasma-derived proteins—used in rare disease treatment and recombinant therapy support—is also rising. These innovations collectively strengthen supply resilience, reduce operational cost, and align the sector with global quality standards.

In November 2023, Grifols received U.S. FDA approval for expanded immunoglobulin purification and filling capacity at its Clayton, North Carolina, manufacturing site, increasing annual output by 16 million grams of its leading Gamunex-C immunoglobulin brand. This milestone enhances the company’s capacity to meet rising clinical demand for Ig therapies. Source: www.grifols.com

In 2025, Grifols Egypt for Plasma Derivatives achieved autosufficiency in essential plasma-derived medicines—including immunoglobulins, albumin, and coagulation factors—through its integrated collection and processing platform, helping reduce import reliance and strengthen local supply continuity. The company operates multiple donation centers and plans further expansion to meet clinical needs. Source: www.elpais.com

In March 2024, Kedrion S.p.A. established a framework agreement with Biotest AG for the full commercialization and distribution of the immunoglobulin therapy Yimmugo in the U.S. market, marking strategic collaboration to expand Ig therapy access.

In 2024, Takeda’s BioLife Plasma Services expanded its U.S. plasma donation network, boosting plasma collection volumes and supporting supplies for Takeda’s plasma-derived immunoglobulin and albumin therapies. This expansion underpins stronger supply chain capacity for fractionation operations.

The Blood Plasma Fractionation Market Report provides an in-depth and structured evaluation of the global industry, covering all critical aspects spanning product categories, clinical applications, end-user environments, and regional dynamics. The report analyzes major plasma-derived proteins such as immunoglobulins, albumin, coagulation factors, protease inhibitors, and specialty biologics, detailing their medical relevance, usage patterns, and technological evolution. It covers market segmentation across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting adoption trends, demand variations, and regional healthcare infrastructure differences.

The scope further extends to application areas including immunology, hematology, neurology, critical care, and infectious disease management, supported by quantitative insights into usage volume, treatment populations, and clinical adoption rates. End-user segments covered include hospitals, specialty clinics, research laboratories, and biopharmaceutical manufacturers, with considerations of procurement behavior, operational capacity, and technology integration.

The report additionally outlines technological influences such as chromatographic advancements, next-generation purification systems, automation, robotics, and digital transformation tools enhancing efficiency and compliance. Emerging segments—such as advanced viral inactivation technologies, high-purity protein isolates, and region-specific plasma applications—are also included to support strategic planning. Overall, the report offers a comprehensive and decision-oriented perspective, enabling stakeholders to assess opportunities, competitive positioning, regulatory environments, and innovation pathways across the global plasma fractionation landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,731.0 Million |

| Market Revenue (2032) | USD 7,325.8 Million |

| CAGR (2025–2032) | 8.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | CSL Behring, Grifols S.A., Takeda Pharmaceutical Company Limited, Octapharma AG, Kedrion S.p.A., Bio Products Laboratory (BPL), Biotest AG, China Biologic Products, Hualan Biological Engineering, ADMA Biologics |

| Customization & Pricing | Available on Request (10% Customization Free) |