Reports

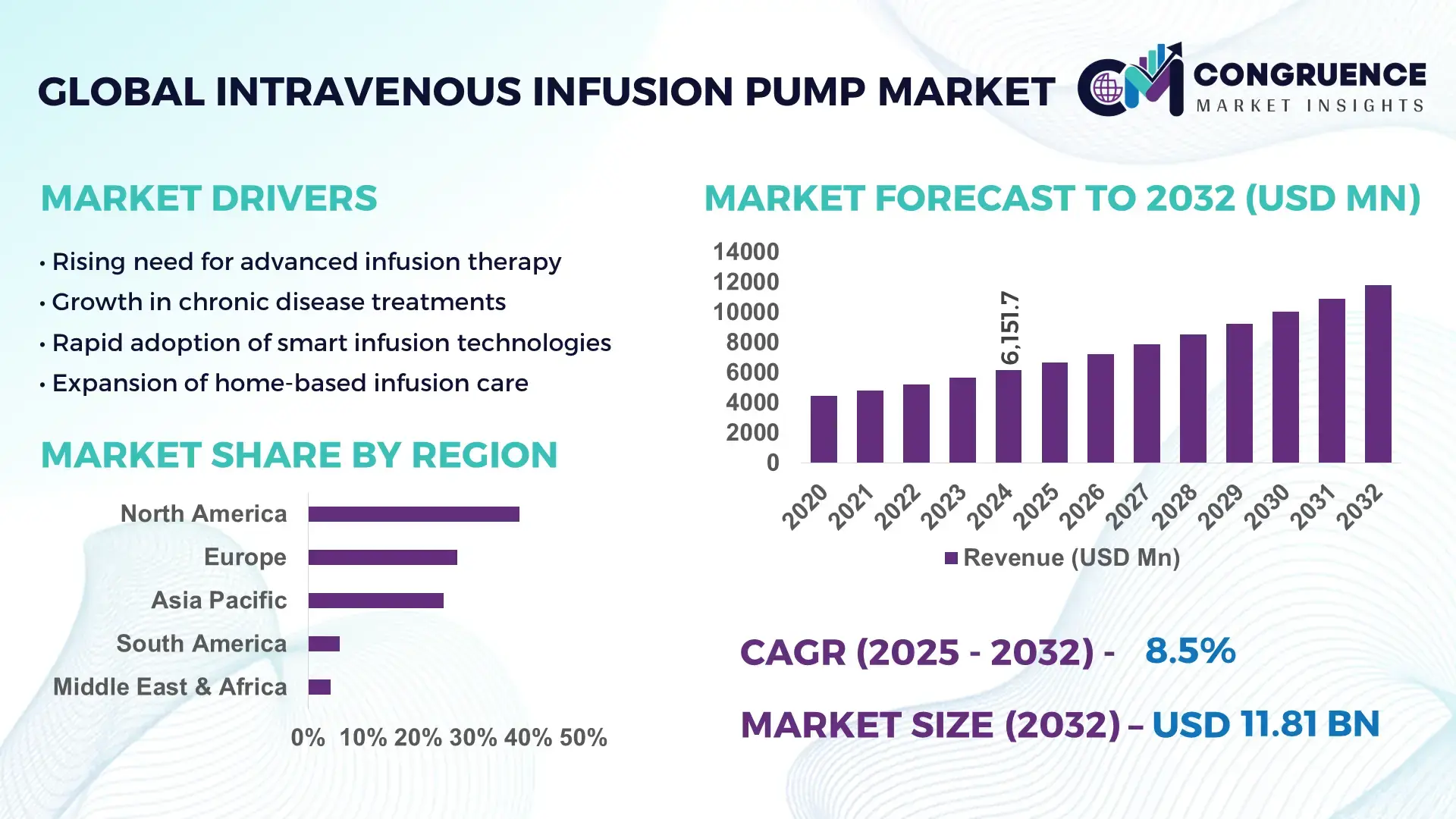

The Global Intravenous Infusion Pump Market was valued at USD 6,151.7 Million in 2024 and is anticipated to reach USD 11,815.0 Million by 2032, expanding at a CAGR of 8.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by accelerating upgrades to smart, digitally connected infusion systems that enhance medication safety and clinical workflow efficiency.

The United States remains the dominant country in the Intravenous Infusion Pump Market, backed by extensive manufacturing capacity, advanced clinical technology ecosystems, and strong investment in high-reliability medication-delivery systems. The country maintains a large installed base with more than 80% adoption of smart infusion systems in acute-care hospitals, supplemented by expanding interoperability pilots across large health systems. U.S. manufacturers operate substantial production facilities for volumetric, syringe, PCA, and ambulatory pumps, while national R&D investments continue to support innovations in dose-error reduction software, wireless connectivity, and advanced alarm-management algorithms. High utilization in oncology, critical care, and chronic-disease infusion therapies, combined with widespread integration of drug libraries, strengthens domestic demand and elevates the country’s technological leadership.

Market Size & Growth: USD 6.15B in 2024, projected to reach USD 11.81B by 2032, at an 8.5% CAGR; growth driven by adoption of smart pumps with integrated safety and workflow features.

Top Growth Drivers: Smart-system adoption above 80%; interoperability initiatives improving workflow efficiency by 30%+; home- and ambulatory-infusion usage rising over 25%.

Short-Term Forecast: By 2028, infusion-accuracy KPIs are expected to improve by ~30% due to wider deployment of interoperable pump systems.

Emerging Technologies: AI-enabled infusion analytics, closed-loop medication delivery, and wireless fleet-management platforms.

Regional Leaders: North America projected to surpass USD 4.0B by 2032 (high upgrade cycles); Europe expected to reach USD 2.8B (regulatory-driven tech adoption); Asia Pacific around USD 2.5B (rapid hospital expansion).

Consumer/End-User Trends: Hospitals, oncology centers, and home-infusion providers increasingly prefer interoperable, high-accuracy pumps supported by real-time monitoring.

Pilot or Case Example: A recent hospital pilot demonstrated over 90% reduction in infusion-variance rates after implementing automated infusion-order programming.

Competitive Landscape: Market leader holds approx. 25% share; major competitors include Baxter, B. Braun, ICU Medical, Terumo, and Smiths Medical.

Regulatory & ESG Impact: Heightened safety, interoperability, and cybersecurity requirements, alongside device-recycling initiatives, influence procurement criteria.

Investment & Funding Patterns: Recent global investments in smart-infusion technologies exceed several hundred million USD, along with increasing financing for digital monitoring platforms.

Innovation & Future Outlook: AI-driven safety algorithms, cloud-connected pump ecosystems, and closed-loop dosing frameworks will define the next generation of infusion technologies.

The Intravenous Infusion Pump Market is reinforced by advanced applications across hospitals, specialty clinics, and home-care networks. Innovations in drug libraries, alarm optimization, and wireless monitoring enhance safety and operational efficiency, while regulatory pressures and digital-health integration accelerate modernization. Rising infusion volumes in oncology, critical care, and chronic therapies further support sustained market expansion.

The Intravenous Infusion Pump Market holds substantial strategic relevance, as infusion devices underpin core clinical workflows in acute care, oncology, emergency medicine, and chronic disease management. Modern health systems increasingly rely on advanced pump platforms to reduce medication-administration errors, standardize dosing protocols, and improve documentation accuracy. Smart pumps integrated with hospital EHR systems deliver measurable operational advantages: new-generation interoperability solutions provide up to 40% improvement in programming consistency compared to older standalone pumps. These performance gains support both safety initiatives and digital-transformation strategies across healthcare facilities.

Regional performance varies significantly. North America leads in installation volume, driven by rapid upgrade cycles and stringent safety mandates, while Asia Pacific leads in adoption growth, with fast-expanding hospitals and over 20% yearly increases in new-system procurement. Europe maintains high compliance with unified regulatory standards, accelerating adoption of advanced devices with integrated safety software.

Short-term projections highlight rapid digitalization. By 2028, AI-supported infusion-monitoring platforms are expected to improve clinical workflow efficiency by 25–35%, particularly in busy oncology and critical-care units. Digital-fleet management is projected to reduce device downtime by 10–15% over the same period, enabling hospitals to manage larger patient loads with optimized asset utilization.

ESG commitments also influence future procurement, with healthcare networks targeting measurable improvements in device sustainability, including double-digit increases in recyclable components and multi-year reductions in energy requirements for portable infusion equipment.

A notable micro-scenario illustrates measurable progress: In 2024, a multi-hospital network implemented automated order-to-pump programming across its oncology centers and reported a 90% reduction in infusion-variance events, demonstrating the tangible benefits of integrating advanced infusion systems into clinical workflows.

Looking ahead, the Intravenous Infusion Pump Market is positioned as a pillar of healthcare resilience, compliance, and sustainable growth. Its evolution will be defined by digital interoperability, AI-driven error prevention, and expanded infusion delivery beyond traditional hospital walls.

The Intravenous Infusion Pump Market continues to evolve through rapid technological upgrades, expanding clinical workloads, and modernized therapy environments. Growth is driven by rising volumes of complex infusions, the expansion of home and ambulatory care, and increasing emphasis on minimizing medication-administration errors. Hospitals are accelerating the transition from legacy pumps to smart, connected platforms with automated dose-error reduction systems, which streamline clinician workflows and reduce variability. At the same time, manufacturers are increasing production to address replacement cycles, while also investing in cloud connectivity, cybersecurity, and advanced alarm-management algorithms. Regulatory pressures, operational efficiency demands, and population-driven increases in chronic-disease infusions further shape market direction. The interplay of these factors establishes a high-value, technology-driven landscape suited for sustained long-term development.

Demand for smart and interoperable infusion pumps continues accelerating as healthcare facilities pursue measurable improvements in medication-administration safety and workflow optimization. Smart pump adoption exceeds 80% in major hospital systems, reflecting strong confidence in dose-error reduction software and high-precision infusion management. Interoperable systems further strengthen outcomes by automating infusion programming and synchronizing pump settings with physician orders, reducing manual entry steps by up to 50% in advanced deployments. Studies consistently show substantial declines in infusion-related deviations after implementing integrated drug libraries and automated order-transmission functions, with reductions in medication-setup time and significant improvements in dosing accuracy. As hospitals seek to standardize workflows across departments—ICU, oncology, pediatrics, and emergency care—interoperable pumps become essential assets, driving continuous procurement and upgrade cycles.

Despite clear clinical benefits, full pump-EHR interoperability requires substantial investment in IT infrastructure, integration testing, and workflow redesign. Many healthcare facilities face budget constraints or lack internal technical resources to support cross-department integration. Custom interfaces, multi-vendor environments, and continuous drug-library governance add significant cost and administrative burden. Training requirements also remain high, particularly when facilities operate mixed fleets of legacy and next-generation pumps. Delays in regulatory certification for new features, combined with cybersecurity mandates for connected devices, further extend deployment timelines. These operational and cost-related barriers can slow decision-making for hospitals and outpatient centers, limiting the pace of broader interoperability implementation.

The integration of AI analytics and cloud-based fleet management opens significant opportunities across hospitals, specialty clinics, and home-care networks. Predictive maintenance analytics can reduce pump downtime by 10–15%, enabling better utilization of existing assets. Remote drug-library updates eliminate manual workflows and decrease compliance gaps, while AI-driven pattern recognition identifies recurring programming errors, supporting targeted clinical training. Ambulatory and home-infusion sectors represent substantial expansion potential as patient transitions from inpatient to outpatient settings increase annually. Device-as-a-service financing models further broaden accessibility, allowing institutions to deploy advanced pumps without substantial upfront capital. These innovations collectively create a scalable, data-driven pathway for long-term market growth.

Compliance with evolving regulatory standards for device safety, software integrity, and cybersecurity significantly increases development and operational costs for manufacturers. Hospitals incur additional expenses through maintenance contracts, periodic recalibration, software updates, and device fleet replacement. Human-factor limitations—such as complex interfaces, multi-step programming, and inconsistent alarm behavior—can contribute to preventable use errors, necessitating continuous training and device redesign. Variations in clinical workflow across departments further complicate standardization efforts, making universal design optimization difficult. Collectively, these challenges slow purchasing cycles and require extensive coordination across clinical, IT, and biomedical engineering teams.

Smart Pump Interoperability Enhancing Safety: Hospitals adopting interoperability report measurable improvements in clinical accuracy, with infusion-variance reductions ranging from 15% to over 90% in controlled implementations. Automated order transmission eliminates several manual entry steps and reduces workflow bottlenecks, supporting safer and more predictable medication administration.

High Penetration of Smart Pumps in Advanced Care settings: Smart pump utilization surpasses 80% across large healthcare networks, driven by standardized infusion protocols in oncology, pediatric, and critical-care units. Facilities report double-digit improvements in workflow efficiency and faster programming cycles, strengthening demand for advanced safety and connectivity features.

Expansion of Home and Ambulatory Infusion Therapy: Demand for portable and ambulatory pumps is rising rapidly, with annual procurement growth above 20–25% in several high-demand regions. These systems support chronic treatment regimens and post-discharge care, increasing the need for user-friendly, long-battery-life devices with simplified programming interfaces.

AI and Cloud-Based Infusion Management: AI-assisted analytics and cloud fleet-management tools are gaining traction, providing 10–15% improvements in uptime and enhancing visibility into device performance. Predictive maintenance alerts, usage analytics, and centralized drug-library governance allow hospitals to optimize asset allocation and reduce preventable delays.

The Intravenous Infusion Pump Market is structured across three core dimensions—type, application, and end-user—each reflecting differing clinical demands, regulatory criteria, and technology adoption patterns. Type segmentation encompasses volumetric, syringe, ambulatory, insulin, elastomeric, PCA, and implantable pumps, with hospitals prioritizing high-capacity platforms while home-care channels favor portable systems. Application segmentation spans oncology, critical care, surgery, pediatrics, home infusion, and specialty therapies, all influenced by protocol-driven dosing requirements and the rising volume of chronic-disease management. End-user segmentation highlights hospitals, ambulatory infusion centers, home-care providers, specialty clinics, and long-term care facilities, each adopting devices based on workflow complexity, connectivity expectations, staffing models, and maintenance capacity. These segmentation patterns guide OEM product development and fleet-management strategies, shaping investments in safety features, interoperability, and miniaturized pump architectures.

Volumetric infusion pumps represent the leading type segment, accounting for 36.6% of total market usage in 2024. Their dominance is driven by broad application across ICUs, surgical wards, and long-duration therapies requiring precise high-volume delivery. Syringe pumps remain crucial for neonatology, anesthesia, and low-volume drug administration, while ambulatory pumps support the shift toward outpatient and home-based care. The fastest-growing type is the smart/connected infusion pump segment, expanding at approximately 13.3% CAGR, supported by interoperable software, dose-error reduction systems, and wireless fleet-management capabilities. Other pump types—including insulin/patch pumps, elastomeric disposable pumps, PCA pumps, and implantable pumps—collectively account for 63.4% of the remaining market mix and maintain strong relevance in chronic-care, oncology, and post-operative environments.

Oncology and chemotherapy constitute the largest application segment, accounting for ~30% of total infusion pump utilization due to the high frequency, structured protocols, and long-duration infusions associated with cancer treatment. Critical care and ICU applications follow, supported by continuous vasopressor, sedation, and nutrition delivery requirements. The fastest-growing application is ambulatory and home infusion, expanding at an estimated 6.9%–8% CAGR, driven by the decentralization of care, reduced hospitalization strategies, and workforce optimization in outpatient environments. Other major applications include anesthesia/surgical care, pediatrics/neonatology, and specialty biologic therapies; together these categories represent ~70% of the application share. Consumer adoption trends show strong momentum: in 2024, over 80% of large healthcare systems expanded smart-pump deployment across high-acuity units, while 20–25% year-over-year increases were reported in home-infusion pump adoption across multiple regions.

Hospitals remain the dominant end-user segment, accounting for 60–70% of all pump deployments, supported by high-acuity care demands, multi-department fleet usage, and extensive safety-protocol integration. These facilities prioritize smart volumetric and syringe pumps with strong interoperability and advanced drug-library governance. The fastest-growing end-user category is home-care and ambulatory infusion providers, expanding at mid-single to low-double-digit growth rates, fueled by long-term therapy programs, chronic-care expansion, and payer-driven outpatient treatment models. Specialty oncology centers, outpatient infusion clinics, and long-term care facilities collectively account for 30–40% of remaining utilization and rely heavily on portable, wearable, and disposable pump types. End-user adoption patterns reinforce this shift: in 2024, over 80% of hospital systems reported multidepartment integration of smart pumps, while outpatient infusion networks cited double-digit increases in demand for portable units to support decentralized care.

North America accounted for the largest market share at 38.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

North America’s leadership reflects high device penetration, strong clinical digitalization, and accelerated replacement cycles across hospitals. Europe followed with 27.1%, supported by stringent infusion-safety regulations and rapid adoption of interoperable pump platforms. Asia-Pacific reached 24.6%, driven by expanding hospital infrastructure and large therapy volumes in China, India, and Japan. South America represented 5.8%, with rising public–private investments in cancer and chronic-care infusion. Middle East & Africa captured 4.1%, with demand concentrated in advanced-care clusters in GCC states and South Africa. These regional variations underscore differing maturity levels, infrastructure capabilities, and investment patterns shaping infusion pump adoption.

North America maintained a significant market presence with 38.4% share in 2024, driven by high deployment across hospitals, ambulatory surgical centers, and oncology infusion networks. Demand is primarily influenced by critical-care, chronic-disease management, and precision-therapy requirements. Regulatory reforms promoting standardized drug libraries and interoperability continue to advance device modernization across major care settings. The region is witnessing rapid adoption of smart infusion platforms, wireless connectivity, and automated asset-tracking systems. A notable local player expanded its digital pump-fleet integration program across more than 800 clinical sites, improving medication-administration compliance and reducing manual workflow steps. Consumer behavior shows higher acceptance of connected medical devices, with healthcare and enterprise sectors consistently demonstrating early uptake of clinical automation technologies.

Europe held 27.1% market share in 2024, supported by strong demand in Germany, the UK, and France—countries with established medical-device manufacturing and advanced hospital digitalization. Regional regulatory frameworks emphasizing safety, alarm standardization, and infusion accuracy continue to shape procurement priorities. Sustainability and energy-efficiency directives also drive upgrades to modern pump platforms with improved lifecycle performance. European facilities are adopting emerging technologies such as integrated dose-error reduction systems, automated infusion-workflow management, and cloud-enabled analytics. A major regional manufacturer enhanced its production capacity for smart pumps to support growing infusion demand across EU healthcare networks. Consumer behavior trends show preference for transparent, explainable clinical technologies due to heightened regulatory oversight and patient-safety expectations.

Asia-Pacific ranked among the largest and fastest-expanding regions, capturing 24.6% market share in 2024. China, India, and Japan remain the top-consuming countries, accounting for more than 70% of the region’s total infusion pump volume. Rapid hospital construction, investment in oncology and critical-care services, and expansion of home-infusion programs propel broader device adoption. Manufacturing hubs across China and Southeast Asia are increasing production of volumetric and syringe pumps, supporting cost-effective supply to domestic and export markets. Regional innovation clusters continue advancing portable infusion technologies, closed-loop medication-delivery capabilities, and digital monitoring platforms. Consumer behavior trends reveal high engagement with mobile health interfaces and remote-care tools, accelerating demand for connected pumps and outpatient infusion flexibility.

South America accounted for 5.8% of global infusion pump utilization in 2024, led by Brazil and Argentina, which together represented more than 65% of regional demand. Growth is supported by improvements in oncology, intensive care, and surgical infrastructure in urban centers. Regulatory harmonization efforts and government-backed modernization programs are shaping procurement cycles for updated infusion systems. Healthcare providers increasingly deploy portable and durable pump designs suitable for diverse clinical environments. A prominent regional supplier expanded distribution networks for ambulatory pumps, improving access for chronic-disease patients. Consumer behavior shows rising comfort with digital interfaces and device-guided therapy workflows, particularly in metropolitan care settings with expanding telehealth adoption.

The Middle East & Africa region held 4.1% market share in 2024, supported by concentrated demand in the UAE, Saudi Arabia, and South Africa. Investments in high-acuity hospitals, oncology centers, and specialized treatment facilities continue to boost adoption of infusion technology. The region is undergoing rapid technological modernization, with increased integration of connected pumps, centralized drug libraries, and digitally governed infusion-management systems. Regulatory initiatives encouraging safety compliance and medical-device standardization are shaping procurement strategies. A recognized local healthcare group recently expanded its deployment of smart infusion platforms across multiple tertiary hospitals, enhancing therapy consistency and clinical workflow reliability. Consumer behavior trends indicate strong acceptance of advanced medical technologies in high-income urban clusters.

United States – 32.5% Market Share: Strong device penetration supported by extensive hospital networks, high treatment volumes, and accelerated adoption of connected infusion platforms.

China – 18.2% Market Share: Leadership reinforced by expanding production capacity, large-scale healthcare infrastructure development, and increasing demand for infusion-dependent therapies.

The competitive environment in the Intravenous Infusion Pump Market remains moderately consolidated yet dynamically evolving, with 10–15 major active companies and several smaller niche players vying for market share. The top 5 global companies collectively hold approximately 55–60% of the total market, while the remainder is spread across mid-tier and regional manufacturers. This overlap between established med-tech firms and emerging innovators creates a landscape of guarded competition and rapid innovation.

Key market participants continuously roll out strategic initiatives — new product launches, regulatory clearances, manufacturing expansions, and smart-pump/platform updates — to maintain relevance. For example, multiple firms introduced next-generation infusion pumps with improved connectivity and safety features in 2023–2024, signaling a shift toward “infusion-as-a-system” rather than standalone devices. Competitive pressure is further intensified by innovation trends such as smart-pump interoperability, IoT-enabled fleet management, closed-loop infusion control, and predictive maintenance offerings. These trends influence procurement decisions and push companies to invest heavily in R&D and regulatory compliance.

Because of varied end-use requirements (hospitals, home care, clinics, oncology centers), the market is neither fully consolidated nor fragmented; rather it sits in a balanced “consolidated-but-competitive” state, where top-tier players manage global supply and safety standards, and smaller firms attempt to differentiate through niche segments (ambulatory pumps, low-cost devices, emerging markets). Strategic initiatives such as multi-year hospital supply contracts, digital-health integration, and service-based business models (pump-as-a-service) strengthen leading firms’ positions while enabling growth for agile newcomers. Overall, competitive dynamics are shaped by a combination of product innovation, regulatory compliance, supply-chain resilience, and increasingly sophisticated customer requirements for safety, connectivity, and lifecycle support.

Fresenius Kabi AG

Terumo Corporation

Smiths Medical Group Ltd.

Medtronic plc

The current and emerging technology landscape for infusion pumps is marked by a rapid transition from legacy volumetric and syringe pumps toward connected, smart, and integrated infusion systems. Key technology trends include: IoT-enabled infusion devices with real-time monitoring and remote management; integrated drug-library software that helps enforce dosing protocols; connectivity with electronic health records (EHR) systems; and enhanced safety algorithms that flag potential infusion errors or deviations.

In many modern systems, pumps now feature unified platforms supporting both large-volume and syringe infusion modalities with a common user interface, reducing training burden and simplifying device management across hospital fleets. Innovations also extend to ambulatory and portable pumps optimized for home-care and outpatient infusion therapy — these devices emphasize compact design, battery efficiency, simplified programming, and remote monitoring capabilities, enabling decentralized care with medical-grade reliability.

Another major area of technological advancement is digital health integration: infusion pumps are increasingly part of broader hospital IT ecosystems, enabling fleet-level analytics, usage tracking, maintenance scheduling, and compliance reporting. These capabilities allow healthcare providers to optimize pump utilization, reduce downtime, and improve dosing accuracy. Predictive maintenance — where the system anticipates component wear or sensor drift — is being adopted to cut device-related interruptions, supporting high-availability care environments.

Finally, security and data integrity are receiving increased focus: with connected infusion pumps transmitting patient and therapy data over hospital networks, manufacturers are embedding secure communication protocols, encryption, and audit-trail capabilities to comply with regulatory and data-privacy requirements. For decision-makers and procurement planners, these technological evolutions mean that next-generation infusion systems are no longer standalone hardware, but part of integrated clinical-IT infrastructure — offering not only reliable fluid delivery, but also data transparency, operational efficiency, and safety governance.

On April 1, 2024, Baxter received U.S. FDA 510(k) clearance for the Novum IQ large-volume infusion pump and Dose IQ Safety Software, adding LVP capability to the Novum IQ platform with enterprise connectivity, auto-programming and over-the-air update features to support integrated LVP + syringe workflows. Source: www.baxter.com

On August 29, 2023, ICU Medical received U.S. FDA 510(k) clearance for the Plum Duo infusion pump and LifeShield infusion-safety software; the dual-channel Plum Duo (with precision cassette design) was positioned for U.S. availability in early 2024 to improve simultaneous-infusion workflows in critical care. Source: www.icumed.com

In 2024, Smiths Medical issued urgent software corrections for CADD-Solis and CADD-Solis VIP ambulatory infusion pumps; the FDA posted notifications (Class I level) and the correction action referenced approximately 9,284 units in commerce, requiring customers to update software/usage instructions to mitigate false upstream-occlusion alarms and other safety risks. Source: www.smiths.com

In August 2024, Fresenius Kabi received a Trailblazer Award from a major group-purchasing organization recognizing supply-chain innovation; the award highlighted investments in U.S. manufacturing and resiliency that support distribution of infusion medicines and technologies to a network representing roughly 4,350 hospitals and provider organizations. Source: www.fresenius-kabi.com

This report comprehensively covers the global Intravenous Infusion Pump Market across multiple dimensions, including product types (volumetric pumps, syringe pumps, ambulatory/portable pumps, insulin/patch pumps, elastomeric/disposable pumps, PCA pumps, implantable systems), applications (oncology, critical-care/ICU, surgery/anesthesia, pediatrics/neonatology, home infusion, specialty therapies), and end-user segments (hospitals and tertiary care centers, ambulatory infusion clinics, home-health providers, specialty oncology centers, long-term care facilities). Geographically, the report spans all major regions: North America, Europe, Asia-Pacific, South America, Middle East & Africa — offering region-wise market insights, growth patterns, and consumption trends.

Technological focus includes smart/connected infusion platforms, IoT and EHR integration, cloud-based fleet management, safety-software and drug-library governance, portable and ambulatory pump design, and predictive-maintenance analytics. The report also addresses manufacturing capacity, supply-chain resilience, regulatory and compliance influences, and shifting end-user preferences including outpatient and home-care infusion. Additionally, niche and emerging segments — such as implantable pumps, wearable infusion devices, and digital-health enhanced therapy management — are included to reflect future growth pathways and innovation potential. The scope ensures decision-makers and industry stakeholders gain a holistic view: from device-level technology and product segmentation to regional demand dynamics, end-user behavior, competitive positioning, and the evolving role of infusion technology in modern healthcare delivery.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 6,151.7 Million |

| Market Revenue (2032) | USD 11,815.0 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Baxter International Inc., B. Braun Melsungen AG, ICU Medical, Fresenius Kabi, Terumo Corporation, Smiths Medical, Medtronic plc |

| Customization & Pricing | Available on Request (10% Customization Free) |