Reports

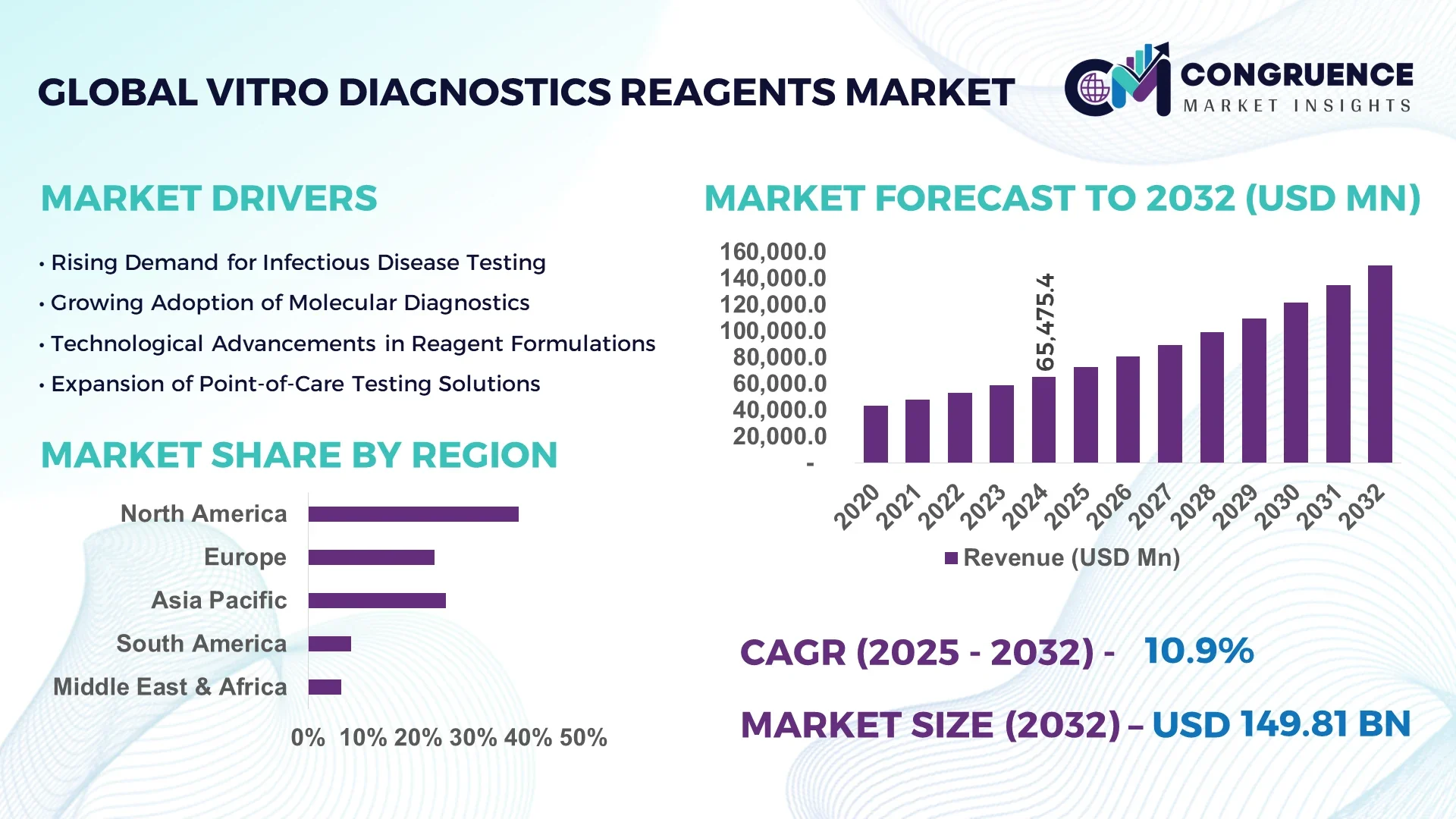

The Global Vitro Diagnostics Reagents Market was valued at USD 65,475.36 Million in 2024 and is anticipated to reach a value of USD 149,806.36 Million by 2032 expanding at a CAGR of 10.9% between 2025 and 2032.

The United States plays a significant role in shaping the global Vitro Diagnostics Reagents market due to its substantial production capacity, high-level investments in biotechnology research, and integration of reagents across advanced diagnostic laboratories, especially for oncology, infectious diseases, and genetic testing. The country also leads in the adoption of automation technologies in reagent development and utilization.

The Vitro Diagnostics Reagents market is undergoing a dynamic transformation, driven by rapid technological advancements and growing clinical demand for precise diagnostic tools. Immunoassay reagents, molecular diagnostics reagents, and hematology reagents are among the top-performing segments, particularly in high-throughput clinical laboratories and research institutions. Advances in microfluidics, lab-on-chip technologies, and reagent stabilization techniques are improving shelf life and accuracy of results. Regulatory frameworks across regions, especially in Europe and North America, are increasingly supporting personalized diagnostics and companion testing, influencing reagent innovation. Additionally, Asia-Pacific is witnessing a surge in consumption due to expanding healthcare infrastructure and growing awareness around early disease detection. Environmental sustainability is also emerging as a crucial consideration, with manufacturers developing eco-friendly and low-waste reagent solutions. Looking ahead, demand will be propelled by automation in diagnostics, precision medicine, and rising chronic disease prevalence globally.

Artificial Intelligence is playing a transformative role in reshaping the Vitro Diagnostics Reagents Market by enhancing both the development and deployment of diagnostic reagents. AI-driven tools now assist in reagent formulation by predicting molecular interactions, reducing trial-and-error cycles, and accelerating product innovation. These technologies are cutting down R&D timelines and improving the overall efficiency of product development cycles. In clinical diagnostics, AI is streamlining workflows by enabling smarter reagent usage, leading to faster and more accurate test outcomes.

AI-powered systems also optimize reagent inventory management in laboratories through predictive analytics, which lowers wastage and ensures uninterrupted diagnostic operations. Furthermore, machine learning algorithms are increasingly used in conjunction with reagents to analyze test results in real time, providing actionable insights and minimizing diagnostic errors. In oncology and genetic testing, AI enhances the interpretation of complex assays, making reagent-based diagnostics more precise and personalized.

Additionally, automated platforms integrated with AI are improving quality control in reagent manufacturing, ensuring batch-to-batch consistency. With the rise in demand for point-of-care testing and home diagnostics, AI-supported reagent kits are becoming more intuitive and user-friendly, making diagnostics accessible to a wider population. These advancements collectively underscore how the Vitro Diagnostics Reagents Market is being optimized and scaled using intelligent technologies that elevate accuracy, reduce costs, and enhance operational resilience.

“In 2024, a leading diagnostics company introduced an AI-powered reagent quality control system that reduced production defects by 37% and shortened validation cycles by 28%, setting a new benchmark for reagent manufacturing precision in the Vitro Diagnostics Reagents Market.”

The rise in global infectious diseases and chronic health conditions such as diabetes, cancer, and cardiovascular disorders is directly influencing the demand within the Vitro Diagnostics Reagents Market. Reagents used in immunodiagnostics, molecular assays, and microbiological testing have become integral to clinical diagnostics, especially in the aftermath of COVID-19, which accelerated the adoption of high-performance reagents across laboratories. For example, the growing reliance on real-time PCR tests has led to significant demand for nucleic acid reagents. Additionally, government health initiatives promoting early disease screening in both developed and developing countries are encouraging investments in advanced reagent formulations. As disease burden continues to escalate, the role of diagnostic reagents in effective clinical decision-making is becoming increasingly critical.

The Vitro Diagnostics Reagents Market is significantly affected by complex and stringent regulatory requirements that slow down product approvals and market entry. Regulatory bodies such as the FDA and the European Medicines Agency impose rigorous clinical validation and quality assurance processes that can extend development timelines. These hurdles are particularly challenging for small and mid-sized manufacturers aiming to bring innovative reagent solutions to market. Compliance with region-specific protocols, including Good Manufacturing Practices (GMP) and In Vitro Diagnostic Regulation (IVDR), requires substantial investment in documentation, audits, and product revalidation. These delays in regulatory approval processes not only hinder product launch strategies but also limit the market availability of new and advanced reagents, thereby affecting innovation cycles.

The increasing demand for point-of-care (POC) diagnostic solutions presents a strong growth opportunity for the Vitro Diagnostics Reagents Market. With a rising preference for decentralized healthcare models and remote patient monitoring, POC testing is gaining popularity in primary care settings and rural healthcare systems. This trend is driving the need for ready-to-use, highly sensitive, and stable reagents that can deliver accurate results in non-laboratory conditions. Technological integration, such as smartphone connectivity and AI-enabled data interpretation, is enhancing the application of reagents in compact devices. The global health ecosystem’s shift toward patient-centric care and early diagnostics creates favorable conditions for reagent manufacturers to innovate and capitalize on fast-growing POC diagnostic solutions across emerging and developed markets.

One of the critical challenges in the Vitro Diagnostics Reagents Market is the rising cost of production, largely driven by raw material price volatility and increasing labor and infrastructure expenses. High-purity biological components and complex chemical agents used in reagent formulation require stringent handling and manufacturing controls, contributing to elevated operational costs. Additionally, disruptions in global supply chains and fluctuations in the availability of key materials like enzymes, antibodies, and nucleotides further strain manufacturers. These cost pressures often lead to reduced profit margins, especially in price-sensitive markets. Maintaining consistent reagent quality while navigating economic uncertainties and unpredictable logistics remains a formidable task for producers across the diagnostics industry.

• Growing Preference for Personalized Diagnostic Reagents: Demand for tailored reagents designed to support precision medicine is rising significantly. Customized reagents are increasingly used in oncology and pharmacogenomics to improve the accuracy of patient-specific diagnostic outcomes. Hospitals and diagnostic laboratories are incorporating specialized reagent kits aligned with genomic profiles. In 2024, over 38% of high-throughput labs in the U.S. reportedly transitioned to customized reagent platforms, indicating a strong shift toward personalized diagnostics.

• Surge in Use of Automated Liquid Handling Systems: Laboratories worldwide are investing in automated liquid handling technologies to enhance throughput and reduce human error. This automation trend is directly impacting the consumption of reagents, especially in clinical chemistry and immunoassay applications. In Europe and Japan, more than 60% of newly installed diagnostic instruments in 2024 were compatible with auto-loading reagent systems, demonstrating a significant transition toward fully integrated platforms.

• Increased Development of Eco-Friendly and Stabilized Reagents: Manufacturers are increasingly focusing on developing reagents with longer shelf lives and minimal environmental impact. Reagents that can withstand varying temperature conditions and maintain efficacy over time are becoming popular in remote and resource-limited settings. In 2024, over 25% of newly launched reagents incorporated biodegradable packaging or stabilization-enhancing components, supporting the market’s sustainability goals.

• Rapid Expansion of Molecular Diagnostic Reagent Portfolios: Molecular diagnostics remains one of the fastest-evolving segments in the Vitro Diagnostics Reagents Market. The demand for nucleic acid-based reagents for real-time PCR, sequencing, and genotyping assays has expanded due to increasing applications in infectious disease testing, oncology, and inherited disorder screening. In 2024 alone, global approvals of molecular reagent products increased by over 40%, highlighting the pace of innovation in this category.

The Vitro Diagnostics Reagents Market is segmented into three key categories: by type, by application, and by end-user. Each segment reflects specific usage patterns, technological integration, and regional preferences. Reagent types include clinical chemistry, immunoassays, molecular diagnostics, hematology, and microbiology reagents, with varying adoption based on laboratory infrastructure and diagnostic requirements. Application-wise, the reagents serve infectious disease testing, oncology, cardiology, autoimmune diseases, and blood screening, among others. From an end-user perspective, hospitals, diagnostic laboratories, academic research centers, and point-of-care settings are the primary stakeholders. Notably, hospitals and clinical labs account for the highest usage due to volume and test diversity, while decentralized testing environments are gaining momentum due to increasing demand for rapid diagnostics and patient-centric care models.

Among the different types of Vitro Diagnostics Reagents, immunoassay reagents hold the leading position due to their widespread use in disease screening, hormone detection, and infectious disease diagnostics. Their adaptability in automated analyzers and suitability for both qualitative and quantitative analysis make them indispensable in clinical laboratories. Molecular diagnostic reagents are the fastest-growing type, largely driven by the surge in demand for high-sensitivity tests for viral infections, genetic diseases, and oncology applications. Advancements in real-time PCR and sequencing-based diagnostics have accelerated the adoption of these reagents globally. Clinical chemistry reagents continue to support routine metabolic testing and are essential in large-scale screening. Hematology and microbiology reagents maintain a stable yet niche presence, primarily in specialized diagnostic workflows. These reagents are essential for complete blood counts and pathogen identification, contributing to comprehensive diagnostic portfolios across healthcare facilities.

Infectious disease testing remains the dominant application area for Vitro Diagnostics Reagents, propelled by the ongoing global surveillance of emerging pathogens and antibiotic resistance. The persistent demand for rapid, reliable, and sensitive diagnostic tools sustains high consumption of reagents in this segment. Oncology is emerging as the fastest-growing application due to increasing cases of cancer and the expansion of companion diagnostics that require highly specific reagents for mutation and biomarker detection. Cardiology applications continue to grow steadily, especially in regions with aging populations and high prevalence of cardiovascular conditions. Autoimmune disease diagnostics and blood screening also represent significant application areas. While their volumes are comparatively lower, they contribute to the market by supporting specialized and preventive diagnostic practices. The need for early and precise disease identification ensures sustained reagent demand across all application categories.

Hospitals constitute the largest end-user group in the Vitro Diagnostics Reagents Market due to their broad range of diagnostic services, patient volume, and investment in advanced laboratory technologies. These institutions typically use reagents across multiple departments, including pathology, microbiology, and biochemistry, resulting in high daily consumption. Diagnostic laboratories represent the fastest-growing end-user segment, particularly due to outsourcing trends and increased establishment of private and independent labs. Their focus on operational efficiency and test accuracy drives continuous procurement of high-quality reagents. Academic and research institutions contribute to reagent demand through ongoing clinical studies and biomarker research, although their consumption volumes are comparatively smaller. Point-of-care settings, including clinics and mobile units, are gradually expanding their role, particularly in underserved areas and during public health emergencies, as they require ready-to-use, stable, and quick-reacting reagent kits to deliver immediate results.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.7% between 2025 and 2032.

The dominance of North America is driven by its well-established diagnostic infrastructure, high adoption of technologically advanced reagents, and continuous investments in precision medicine and molecular diagnostics. Meanwhile, Asia-Pacific’s surge is supported by rapidly expanding healthcare systems, growing awareness of early disease detection, and increasing local reagent production capacities across China, India, and Southeast Asia. The Vitro Diagnostics Reagents Market is also benefitting from regulatory harmonization efforts, increased government funding for diagnostics, and the rising trend of decentralized testing across regions. Global shifts toward automation, AI integration, and personalized healthcare are further transforming reagent demand and distribution strategies. Regional diversification in manufacturing hubs, supported by digital transformation initiatives, is also impacting market dynamics and supply chain efficiencies.

High Demand for Clinical Reagents Driving Precision Testing Evolution

North America held a commanding 38.2% share of the global Vitro Diagnostics Reagents Market in 2024, driven by significant demand across clinical laboratories and hospitals. The region’s growth is largely influenced by the strong presence of life sciences and biotechnology industries, particularly in the U.S., which leads in immunoassays and molecular diagnostics reagent development. Recent regulatory reforms by the FDA have expedited approval pathways for diagnostic reagents, encouraging innovation. Additionally, the integration of AI in diagnostics and the adoption of automated platforms in clinical labs are enhancing reagent accuracy and processing speeds. Government funding for infectious disease surveillance and cancer screening programs is further propelling reagent demand across public and private sectors.

Advanced Laboratory Networks Accelerate Diagnostic Reagent Adoption

Europe captured 29.6% of the global Vitro Diagnostics Reagents Market in 2024, with leading contributions from Germany, France, and the UK. These countries have well-established diagnostic lab networks and ongoing initiatives promoting early disease detection. The European Medicines Agency (EMA) and newly implemented IVDR regulations are playing a pivotal role in ensuring reagent quality and safety. Additionally, sustainability is a strong regional focus, with growing adoption of eco-friendly reagent packaging and low-waste manufacturing processes. Digital transformation, including AI integration and real-time data analytics in diagnostics, is enabling precision diagnostics at scale, particularly in centralized labs and university hospitals across Western Europe.

Rapid Healthcare Expansion Fuels Next-Gen Reagent Innovation

Asia-Pacific emerged as the fastest-growing region in the Vitro Diagnostics Reagents Market in 2024, driven by substantial volume growth across China, India, and Japan. These countries are expanding diagnostic infrastructure through public-private partnerships, boosting demand for reagents in infectious disease and chronic illness diagnostics. China's robust biotech manufacturing capabilities and India’s rapidly expanding hospital network are fueling reagent adoption across both urban and semi-urban regions. Japan remains a hub for high-end diagnostic innovation, especially in oncology. Regional innovation clusters, particularly in Shenzhen, Hyderabad, and Tokyo, are enhancing reagent development with integrated AI, automation, and cloud-based diagnostics systems.

Public Health Campaigns and Lab Modernization Drive Reagent Demand

South America accounted for 6.1% of the global Vitro Diagnostics Reagents Market in 2024, with Brazil and Argentina leading the regional landscape. Brazil’s large-scale public health programs, including blood screening and infectious disease control, have spurred consistent reagent demand. Argentina’s emphasis on diagnostic modernization and lab automation is also contributing to reagent usage. Investments in healthcare infrastructure, particularly in urban hospitals and regional laboratories, are expanding the use of immunoassays and clinical chemistry reagents. Government subsidies and favorable trade regulations for medical imports further support market expansion in key countries across the region.

Modernized Labs and Policy Support Stimulate Reagent Growth

The Middle East & Africa held a 4.2% share of the global Vitro Diagnostics Reagents Market in 2024, with strong activity in the UAE, Saudi Arabia, and South Africa. Demand is driven by growing healthcare investments, particularly in molecular and serological diagnostics aligned with national health objectives. The UAE has emerged as a regional diagnostic hub with cutting-edge lab facilities using automated and AI-integrated reagent systems. In South Africa, reagent demand is being fueled by public health testing initiatives and donor-funded programs targeting communicable diseases. Regulatory bodies in these regions are aligning with international standards to improve reagent quality, while trade agreements are easing access to high-performance diagnostics products.

United States – 31.4% market share:

Dominates the Vitro Diagnostics Reagents Market due to high production capacity, advanced clinical laboratories, and consistent innovation in molecular and immunodiagnostics.

China – 18.7% market share:

Strong manufacturing base, growing demand for diagnostics in public health, and rapid adoption of automation in reagent production drive market leadership.

The Vitro Diagnostics Reagents market is characterized by a moderately consolidated competitive landscape, with over 45 globally active players competing through a mix of technological innovation, regional expansion, and product diversification. Leading companies maintain strong portfolios across multiple reagent categories, including immunoassays, molecular diagnostics, and clinical chemistry. These players are continually expanding their global footprint through strategic partnerships with hospitals, diagnostic labs, and academic institutions.

Recent years have seen a notable increase in product launches featuring improved reagent stability, automation compatibility, and AI-integrated diagnostic functionality. Market leaders are heavily investing in R&D to develop next-generation reagents that support faster turnaround times and increased diagnostic precision. Several companies have entered joint ventures to co-develop reagents tailored for regional needs, especially in Asia-Pacific and Latin America. Mergers and acquisitions are also shaping the market, with larger companies acquiring niche reagent developers to gain access to specialized testing solutions and proprietary technologies. Intellectual property strategies and regulatory compliance remain central to competitive differentiation, especially in highly regulated markets such as North America and Europe. Meanwhile, emerging players are leveraging digital platforms and flexible manufacturing models to gain ground in underserved regions. As innovation and quality remain pivotal, competition in the Vitro Diagnostics Reagents market continues to intensify.

Abbott Laboratories

Thermo Fisher Scientific Inc.

Danaher Corporation

bioMérieux SA

F. Hoffmann-La Roche Ltd

Bio-Rad Laboratories, Inc.

DiaSorin S.p.A.

Sysmex Corporation

Ortho Clinical Diagnostics

Agilent Technologies, Inc.

QuidelOrtho Corporation

Hologic, Inc.

The Vitro Diagnostics Reagents Market is being significantly reshaped by advancements in automation, artificial intelligence, molecular technologies, and sustainable formulation approaches. One of the most influential shifts has been the integration of AI-powered algorithms within reagent-based platforms, enhancing diagnostic precision and workflow automation. These systems optimize reagent usage, reduce error rates, and provide data-driven insights in real-time. Advanced liquid handling robotics have further improved reagent application efficiency, particularly in high-throughput laboratories and centralized diagnostic centers. Molecular diagnostics continues to evolve rapidly, with real-time PCR, digital PCR, and next-generation sequencing (NGS) leading innovation. Reagents used in these applications are becoming more sensitive, with improved stability and storage flexibility. The development of multiplex reagents capable of detecting multiple targets in a single test is also gaining momentum, reducing both time and cost per diagnosis.

Sustainable technologies are playing an increasing role, with manufacturers focusing on eco-friendly packaging and biodegradable reagent components. Stabilization techniques, such as lyophilization and enhanced buffering agents, are extending shelf-life and improving transportability, particularly for use in decentralized settings or low-resource environments. Cloud-connected diagnostics and Internet of Medical Things (IoMT) solutions are also being integrated with reagent systems to facilitate remote monitoring, automated reordering, and real-time data analytics, offering labs unprecedented control over their diagnostic ecosystems.

• In March 2024, Roche launched its new Elecsys HCV Duo immunoassay reagent, enabling simultaneous detection of hepatitis C virus antigens and antibodies. The dual-marker approach aims to shorten diagnostic windows and improve early detection in clinical settings.

• In December 2023, Thermo Fisher Scientific unveiled a fully automated reagent platform designed for next-generation sequencing sample preparation, reducing hands-on time by 45% while enhancing throughput in oncology and genetic testing applications.

• In August 2024, Sysmex Corporation introduced a new line of hematology reagents with integrated RFID technology for real-time monitoring of reagent usage, enabling improved inventory control and reducing waste across high-volume laboratories.

• In October 2023, Abbott launched its Alinity m Resp-4-Plex reagents in Europe, a molecular diagnostic reagent panel capable of simultaneously identifying SARS-CoV-2, influenza A/B, and RSV with high sensitivity and specificity in a single test cycle.

The Vitro Diagnostics Reagents Market Report offers a comprehensive examination of the industry, covering critical aspects across product types, applications, end-users, and regional dynamics. The report analyzes key reagent categories including immunoassay reagents, molecular diagnostics reagents, clinical chemistry reagents, hematology reagents, and microbiology reagents, evaluating their utilization trends, innovations, and emerging use cases across clinical and research settings. Applications analyzed within the report span infectious disease testing, oncology, cardiology, autoimmune disorders, and blood screening, highlighting diagnostic preferences across developed and emerging healthcare systems. The end-user segment includes hospitals, diagnostic laboratories, academic research institutions, and point-of-care settings, with distinct insights into reagent consumption behaviors and adoption drivers.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering detailed region-wise analysis based on healthcare infrastructure, technological readiness, and regulatory landscapes. The study also provides insight into emerging technologies such as AI-enhanced reagents, sustainable manufacturing practices, and automation-compatible formulations. Furthermore, the report highlights evolving trends such as the shift toward personalized medicine, decentralized testing, and digital diagnostics, identifying opportunities for market expansion and investment. This strategic perspective makes the report valuable for manufacturers, investors, healthcare providers, and regulatory planners shaping the future of in vitro diagnostics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 65,475.36 Million |

|

Market Revenue in 2032 |

USD 149,806.36 Million |

|

CAGR (2025 - 2032) |

10.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Abbott Laboratories, Thermo Fisher Scientific Inc., Danaher Corporation, bioMérieux SA, F. Hoffmann-La Roche Ltd, Bio-Rad Laboratories, Inc., DiaSorin S.p.A., Sysmex Corporation, Ortho Clinical Diagnostics, Agilent Technologies, Inc., QuidelOrtho Corporation, Hologic, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |