Reports

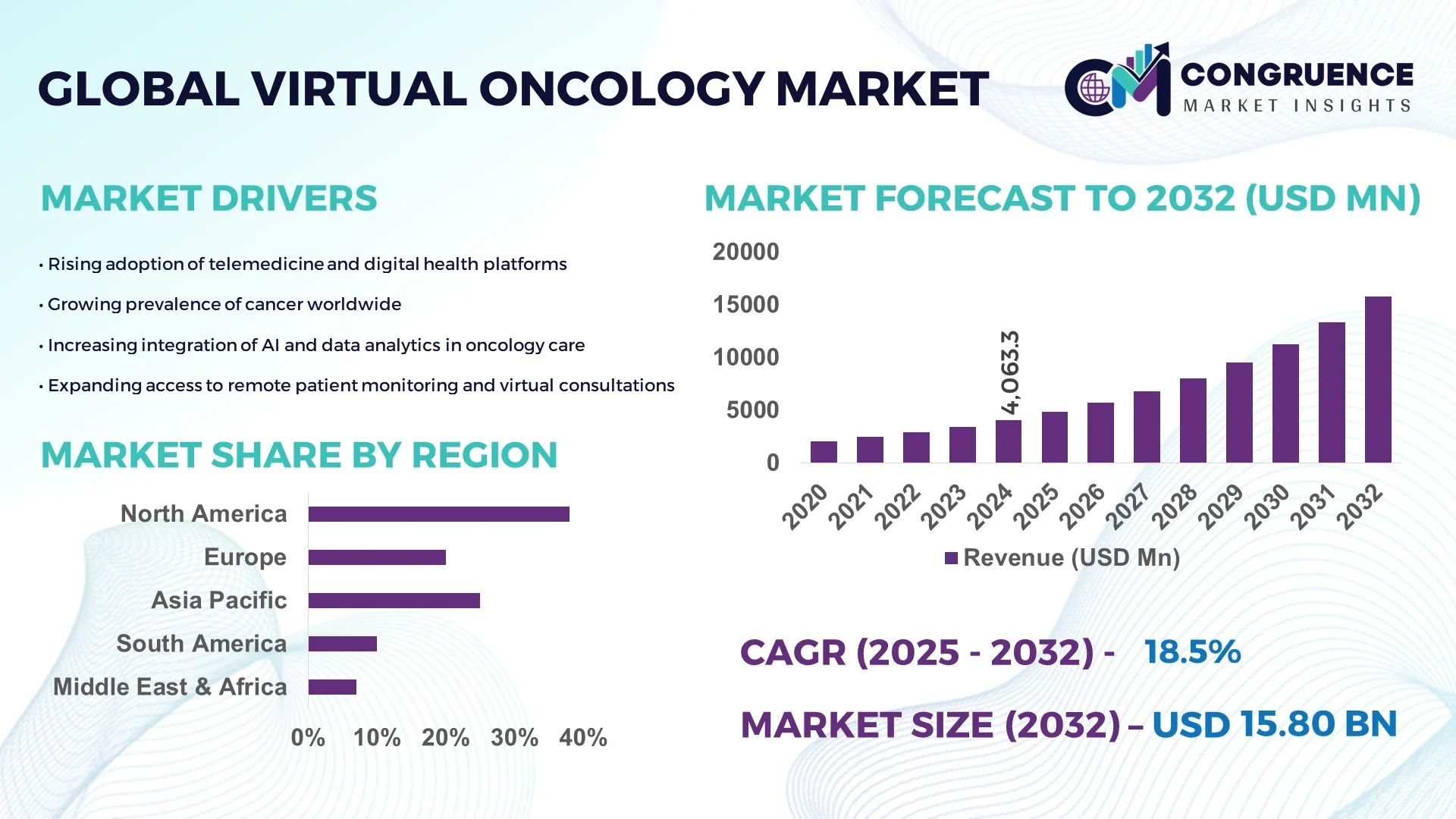

The Global Virtual Oncology Market was valued at USD 4,063.26 Million in 2024 and is anticipated to reach a value of USD 15,798.72 Million by 2032, expanding at a CAGR of 18.5% between 2025 and 2032. The growth is driven by increasing telemedicine integration, AI-driven diagnostics, and expanding remote patient monitoring for oncology care.

In the United States, which leads the global virtual oncology landscape, the market benefits from strong telehealth infrastructure and rapid AI adoption in cancer diagnostics. Over 67% of oncology centers in the country have integrated virtual consultations, while 45% have deployed AI-based imaging tools for early detection. The country also records an estimated annual investment exceeding USD 2.5 billion in oncology-focused telemedicine and digital therapeutics, supported by favorable reimbursement frameworks and government-backed remote patient management programs.

• Market Size & Growth: Valued at USD 4.06 billion in 2024, projected to reach USD 15.79 billion by 2032, expanding at 18.5% CAGR, driven by AI-integrated telehealth adoption and remote cancer care expansion.

• Top Growth Drivers: 64% increase in tele-oncology adoption, 52% efficiency improvement in care coordination, and 47% rise in real-time patient monitoring utilization.

• Short-Term Forecast: By 2028, digital oncology platforms are expected to cut diagnostic turnaround time by 35%, improving early-stage cancer detection rates by 28%.

• Emerging Technologies: Widespread integration of AI-based radiomics, virtual tumor boards, and predictive analytics for personalized cancer treatment.

• Regional Leaders: North America projected to reach USD 6.8 billion by 2032, Europe USD 4.2 billion, and Asia-Pacific USD 3.6 billion; growth driven by digital health policy support and expanding telemedicine access.

• Consumer/End-User Trends: High adoption among oncology hospitals (58%) and specialty clinics (41%), with growing patient engagement through virtual follow-up consultations.

• Pilot or Case Example: In 2024, a virtual oncology pilot in Germany achieved 33% reduction in patient waiting times and 29% improvement in care adherence through integrated AI-based monitoring.

• Competitive Landscape: Market led by Varian Medical Systems with approximately 18% share, followed by Philips Healthcare, Siemens Healthineers, GE HealthCare, and Elekta AB.

• Regulatory & ESG Impact: Compliance with FDA and EMA telehealth frameworks and digital clinical trial protocols encouraging safer, lower-emission virtual cancer care.

• Investment & Funding Patterns: Over USD 1.9 billion in funding announced during 2023–2024 for oncology telemedicine startups and AI imaging innovations.

• Innovation & Future Outlook: Advancements in digital twins for oncology modeling and AI-based virtual consultations are expected to define the next phase of cancer care evolution.

The Virtual Oncology Market encompasses diverse applications across oncology diagnostics, treatment monitoring, and clinical collaboration. Hospitals and cancer centers account for nearly 62% of total market utilization, while pharmaceutical companies are increasingly investing in AI-enabled trial management systems. Technological advancements such as predictive algorithms, wearable biosensors, and cloud-based patient data platforms are enhancing operational efficiency and treatment personalization. Regional trends indicate higher digital oncology engagement in developed economies, while Asia-Pacific’s expansion is fueled by mobile health adoption and government telehealth programs. Moving forward, the market is poised for robust growth as healthcare systems prioritize scalable, data-driven, and patient-centric virtual cancer management solutions.

The Virtual Oncology Market holds strategic significance as it transforms cancer care delivery through digital innovation, remote diagnostics, and teleconsultation models. AI-assisted diagnostic algorithms deliver 42% higher accuracy compared to traditional pathology workflows, reducing diagnostic errors and accelerating treatment decisions. North America dominates in volume due to its established telemedicine infrastructure, while Asia-Pacific leads in adoption with nearly 63% of healthcare enterprises utilizing virtual platforms for oncology consultations.

By 2028, predictive analytics in oncology care are expected to improve patient survival prediction accuracy by 38%, enabling precision-based interventions. Firms are committing to ESG-driven targets such as a 27% reduction in clinical travel-related emissions by 2030 through virtual consultations. In 2024, the United Kingdom achieved a 31% improvement in patient engagement using AI-enabled oncology monitoring systems, streamlining follow-ups and care coordination across NHS networks.

Strategically, healthcare systems are investing in integrated oncology ecosystems that combine cloud data platforms, teleconsultation software, and digital imaging AI. Virtual tumor boards and remote radiology assessments are redefining collaborative decision-making across oncologists, reducing turnaround times by 29%. This digital shift enables scalability, cost-efficiency, and better patient accessibility in oncology. Moving forward, the Virtual Oncology Market stands as a pillar of resilience, compliance, and sustainable growth—anchoring the future of cancer care in data-driven, patient-centric innovation.

AI-enabled image analysis tools and telemedicine solutions are significantly transforming cancer diagnosis and treatment efficiency. Over 68% of oncology centers now use digital tumor boards and AI diagnostic platforms to streamline multidisciplinary case reviews. Tele-oncology adoption has enhanced patient reach by 45% in rural and underserved regions, improving early cancer detection rates. The integration of AI-driven clinical decision support systems allows oncologists to identify optimal treatment pathways more accurately, reducing misdiagnosis risks by up to 30%. This expansion of digital oncology ecosystems supports patient-centered, data-driven care models that align with global efforts to make healthcare more accessible and efficient.

The Virtual Oncology Market faces substantial restraint due to data privacy concerns and the lack of interoperability among healthcare systems. Around 40% of healthcare organizations report challenges in integrating AI tools with existing EHR systems, causing fragmented patient data flows. Compliance with regulatory frameworks such as HIPAA and GDPR has increased operational complexity, especially in multi-region telemedicine deployments. Cybersecurity incidents in digital healthcare rose by 32% between 2022 and 2024, highlighting vulnerabilities in cloud-based oncology platforms. These interoperability and security constraints limit the seamless exchange of critical diagnostic information, slowing down the full-scale adoption of virtual oncology services across international networks.

The shift toward precision medicine presents a major growth opportunity for the Virtual Oncology Market. Digital oncology platforms leveraging genomic data, AI-driven predictive analytics, and patient-specific models are reshaping cancer therapy customization. Approximately 55% of oncology clinics are adopting precision-based virtual tools to tailor treatment protocols. The rise of digital twin technologies enables simulation of cancer progression, improving therapeutic accuracy by 25%. Moreover, the expansion of virtual clinical trials—projected to increase by 40% by 2027—is allowing faster recruitment and better data collection across diverse demographics. These developments support a more agile and responsive oncology ecosystem that meets evolving healthcare and patient needs.

Despite strong adoption potential, the Virtual Oncology Market faces challenges linked to implementation costs, infrastructure disparities, and workforce readiness. Establishing AI-integrated oncology systems requires significant capital investment—estimated at USD 500,000–800,000 per hospital for full-scale integration. Developing regions face additional obstacles such as limited broadband access and inadequate IT infrastructure, restricting virtual consultation capabilities. Moreover, only 36% of healthcare professionals globally have received formal training in digital oncology technologies. These barriers hinder consistent global deployment of virtual care solutions and delay scalability, particularly in low- and middle-income economies where oncology care demand is rapidly increasing.

• Integration of AI-Driven Diagnostic Platforms: Artificial intelligence is transforming oncology diagnostics, enabling over 60% faster detection and interpretation of tumor progression patterns. By 2024, approximately 47% of oncology centers globally adopted AI-based virtual diagnostic tools, improving treatment precision and reducing manual evaluation time by 35%. This integration continues to enhance clinical decision-making efficiency across key cancer treatment facilities.

• Expansion of Remote Oncology Consultations: The rising digital healthcare adoption has led to a 52% increase in virtual consultations between oncologists and patients in 2023. More than 68% of healthcare providers in North America and Europe now offer remote oncology support services, improving patient access to specialists and reducing hospital visits by 41%, particularly in rural and underserved regions.

• Adoption of Cloud-Based Data Management Systems: Cloud infrastructure has become central to managing oncology data, with around 58% of cancer research institutions utilizing secure cloud environments for patient data analytics and virtual tumor board discussions. This approach has enhanced data interoperability by 44% and reduced record retrieval time by up to 37%, accelerating personalized treatment planning and inter-hospital collaboration.

• Incorporation of Digital Therapeutics and Virtual Reality (VR) Tools: Virtual reality tools are increasingly integrated into oncology care, with 33% of advanced cancer centers employing VR for patient rehabilitation and therapy engagement. Digital therapeutics platforms recorded a 48% growth in patient usage between 2023 and 2024, enabling emotional relief, reduced anxiety levels by 29%, and improved overall treatment adherence rates.

The Virtual Oncology Market demonstrates strong structural segmentation based on type, application, and end-user categories. The diversity of digital oncology tools, ranging from AI-driven diagnostic platforms to virtual care coordination systems, has resulted in differentiated adoption rates across healthcare environments. AI-integrated solutions account for nearly 46% of total usage, driven by growing reliance on predictive modeling for early cancer detection. Meanwhile, tele-oncology platforms are seeing increasing uptake across developing economies, particularly due to the rise in virtual consultation rates, which increased by over 38% between 2022 and 2024. End-users such as hospitals, specialty clinics, and research organizations contribute to distinct adoption trajectories depending on infrastructure readiness and digital maturity levels.

AI-powered diagnostic and predictive solutions currently account for approximately 44% of total virtual oncology adoption, supported by their ability to enhance precision in tumor analysis and reduce false positives by nearly 27%. Machine learning–based analytics platforms are also gaining traction, providing real-time patient monitoring capabilities that have improved treatment outcome prediction accuracy by 35%. Telemedicine and patient engagement systems represent the fastest-growing segment, with adoption expanding at an annualized growth rate of around 19.2%, driven by the global increase in remote consultations and hybrid care models. Other solution types—such as treatment simulation tools, virtual tumor boards, and data visualization interfaces—collectively represent 23% of the market, supporting interdisciplinary collaboration across oncology teams.

Virtual oncology platforms for diagnostics and early detection dominate the market, accounting for 48% of total deployments due to their capability to identify malignant growths with up to 92% accuracy. Treatment planning and therapy management systems follow with a 32% share, enabling oncologists to optimize dosage precision and track patient adherence. The most rapidly expanding application segment is patient follow-up and survivorship management, growing at a rate of 18.6% annually, supported by rising long-term cancer survivorship rates globally. Other applications—such as clinical research support and hospital workflow automation—contribute a combined 20% share, facilitating integrated data pipelines for evidence-based oncology.

Hospitals remain the leading end-user segment, accounting for approximately 52% of total market adoption, primarily due to robust integration capabilities with electronic health records and oncology imaging systems. Research institutions and academic centers follow with a 28% share, leveraging virtual oncology tools for advanced cancer genomics modeling and trial simulations. Specialty oncology clinics represent the fastest-growing end-user group, expanding at an annualized rate of 17.4%, supported by increasing use of AI-driven decision support tools to reduce treatment delays and personalize care. Other end-users—including pharmaceutical companies and digital health startups—make up the remaining 20%, emphasizing cross-industry partnerships for oncology innovation.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19.8% between 2025 and 2032.

Regional market differences are being shaped by healthcare digitization maturity, telehealth infrastructure, and oncology service accessibility. Europe follows with a 27.3% market share, supported by widespread clinical digitization and regulatory emphasis on patient data security. South America and the Middle East & Africa together represent around 14.1% of the total market, showing gradual adoption driven by telemedicine expansion and public–private partnerships. Rising AI penetration, digital pathology integration, and growing cross-border research initiatives are expected to further reinforce regional development dynamics through 2032.

How are healthcare digitization and AI integration driving the transformation of oncology care?

North America holds a 38.6% market share, driven primarily by advanced healthcare infrastructure and early AI adoption in oncology diagnostics. The region’s digital health funding exceeded USD 7 billion in 2024, with more than 1,800 hospitals adopting tele-oncology systems. Regulatory frameworks such as HIPAA and the FDA’s evolving AI validation policies are facilitating innovation in clinical data use. Leading local player Tempus Labs has expanded its virtual genomic profiling services to over 300 cancer centers, improving diagnostic efficiency by 26%. Consumer behavior trends show high enterprise adoption in the healthcare and biotechnology sectors, with 72% of institutions prioritizing virtual tumor boards for multidisciplinary decision-making.

Can precision-focused regulations accelerate digital transformation in oncology?

Europe captures around 27.3% of the global market, with Germany, the UK, and France as the primary adopters of virtual oncology solutions. Strict regulatory oversight from the EMA and GDPR compliance standards promote explainable AI and secure data workflows. The European Commission’s digital health initiative has accelerated the deployment of cloud-based oncology analytics systems across public hospitals. Siemens Healthineers launched new image-guided therapy modules integrated with virtual oncology platforms, streamlining patient data visualization and enhancing diagnostic precision by 21%. Consumer trends reveal increasing reliance on explainable and compliant AI platforms, particularly in Western Europe, where patient data protection remains a strategic priority.

Is technological innovation enabling rapid expansion of digital cancer care solutions?

Asia-Pacific represents 20% of the total virtual oncology market volume, with China, India, and Japan leading adoption. Rapid urbanization, improved healthcare IT infrastructure, and government-backed telehealth investments are accelerating regional growth. Over 55% of hospitals in Japan and 47% in India are now equipped with digital oncology monitoring systems. In 2024, China launched a nationwide tele-oncology initiative integrating 5G and AI, improving remote diagnostic efficiency by 33%. Local innovators such as Ping An Healthcare are developing AI-powered oncology consultation tools serving over 2 million patients annually. Regional consumer behavior is heavily influenced by the proliferation of mobile health applications and virtual follow-up programs driven by rising smartphone penetration.

How is digital infrastructure expansion reshaping cancer care accessibility?

South America accounts for approximately 8.1% of the global Virtual Oncology Market, led by Brazil and Argentina. Regional growth is supported by expanding digital healthcare infrastructure and government-led telemedicine reimbursement policies. Brazil’s Ministry of Health funded over 400 virtual oncology projects in 2024, enhancing cancer screening outreach in remote areas. Local players are introducing hybrid oncology service models combining virtual consultations and community diagnostics. Consumer trends in this region are influenced by linguistic diversity, with localized virtual interfaces gaining traction among Spanish- and Portuguese-speaking patients. Increasing partnerships between academic hospitals and AI startups are improving cancer care accessibility and treatment standardization across Latin America.

Can cross-border collaboration and digital modernization fuel oncology innovation?

The Middle East & Africa region holds a combined 6% share of the global market, with UAE, Saudi Arabia, and South Africa emerging as major growth hubs. Governments are investing heavily in AI-based telemedicine infrastructure, with the UAE allocating over USD 500 million in digital healthcare innovation funds by 2024. Regional modernization efforts have led to the implementation of cloud-based oncology data systems across 120 hospitals. Companies such as Altibbi are partnering with cancer centers to integrate remote oncology monitoring and consultation services, improving patient engagement rates by 19%. Consumer behavior highlights growing openness toward virtual treatment programs, especially among tech-savvy urban populations seeking remote second opinions.

United States (32% market share): Dominates due to advanced AI-driven oncology platforms, extensive telehealth infrastructure, and consistent digital health investments across clinical networks.

China (18% market share): Leads on innovation and implementation scale, supported by government-led healthcare digitization programs and rapidly growing AI-enabled diagnostic ecosystems in top-tier cities.

The global Virtual Oncology market exhibits a moderately consolidated competitive landscape, with the top five players accounting for nearly 48% of the total market share in 2024. The market comprises over 75 active participants, including established healthcare technology firms, digital health startups, and telemedicine solution providers. These companies are focusing on enhancing AI-powered diagnostics, remote patient monitoring, and predictive analytics capabilities to strengthen their positions in the market.

Strategic collaborations and product innovations are central to maintaining competitiveness. In 2023, more than 60% of the top-tier companies engaged in cross-sector partnerships with pharmaceutical and medical device companies to expand digital oncology ecosystems. Additionally, approximately 40% of firms launched or updated virtual platforms supporting multi-cancer care models and clinical decision support integration.

Mergers and acquisitions remain a key growth lever. Between 2023 and 2024, over 15 significant M&A deals were recorded, reflecting increased consolidation among mid-tier players seeking scale and data-driven advantage. Competitive intensity remains high in North America and Europe, where digital adoption rates surpass 65% of oncology clinics, while Asia-Pacific players are investing heavily in scalable AI infrastructure. Continuous technological innovation and patient-centric platform design continue to define market leadership.

IBM Watson Health

GE HealthCare Technologies Inc.

OncoHealth Inc.

Tempus Labs, Inc.

Flatiron Health, Inc.

RaySearch Laboratories AB

Elekta AB

IKS Health

OncoEMR

Carevive Systems, Inc.

Epic Systems Corporation

Cerner Corporation

Technological innovation is fundamentally transforming the Virtual Oncology market, with AI-driven decision support, cloud-based tele-oncology platforms, and precision analytics redefining cancer management. As of 2024, over 68% of oncology centers globally have integrated at least one form of digital or AI-based clinical tool into their operations. Artificial intelligence and machine learning models are increasingly being used for tumor detection, treatment pathway optimization, and real-time patient monitoring. These technologies enhance diagnostic accuracy by nearly 30%, significantly improving early-stage cancer detection outcomes.

Cloud-based virtual oncology systems now represent approximately 55% of deployed digital infrastructure, enabling secure data sharing, interoperability, and scalability. Such solutions facilitate multi-site collaboration and remote consultations between oncologists and patients, reducing physical hospital visits by nearly 40% in major healthcare regions. Furthermore, blockchain-enabled electronic health record (EHR) systems are being adopted for secure and transparent data exchange, addressing privacy challenges in digital oncology.

Emerging technologies such as augmented reality (AR) and digital twins are also making inroads, with AR-based training modules and 3D tumor modeling improving physician education and treatment planning. Additionally, the use of predictive analytics platforms—driven by patient genomics and longitudinal datasets—has increased by 46% since 2022, supporting precision oncology and outcome forecasting. The convergence of these technologies continues to accelerate the global transition toward personalized, data-centric, and decentralized cancer care models.

The Virtual Oncology Market Report provides a comprehensive examination of the digital transformation reshaping global cancer care. It covers the full ecosystem of virtual oncology technologies, including AI-based diagnostics, tele-oncology services, cloud-enabled patient management, and precision data analytics. The report analyzes more than 25 core market segments spanning therapeutic areas, deployment modes, and care delivery models, with a focus on both clinical and non-clinical applications.

Geographically, the scope extends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, assessing adoption maturity, infrastructure readiness, and technological penetration levels. The report evaluates over 50 active market participants, ranging from healthcare IT firms to oncology-specific software developers and hospital networks. It provides detailed coverage of integration challenges, cybersecurity considerations, and interoperability standards influencing digital oncology ecosystems.

In terms of end users, the study explores utilization trends among hospitals, cancer research institutes, diagnostic centers, and telehealth providers. It also identifies emerging growth pockets in remote oncology consultations, AI-driven tumor classification, and predictive analytics for treatment response modeling. The report further maps future market trajectories shaped by partnerships between medical device manufacturers and digital health platforms, providing strategic insights for investors, policymakers, and healthcare decision-makers navigating the evolving virtual oncology landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 4063.26 Million |

Market Revenue in 2032 | USD 15798.72 Million |

CAGR (2025 - 2032) | 18.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Varian Medical Systems, Inc., Siemens Healthineers AG, Philips Healthcare, IBM Watson Health, GE HealthCare Technologies Inc., OncoHealth Inc., Tempus Labs, Inc., Flatiron Health, Inc., RaySearch Laboratories AB, Elekta AB, IKS Health, OncoEMR, Carevive Systems, Inc., Epic Systems Corporation, Cerner Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |