Reports

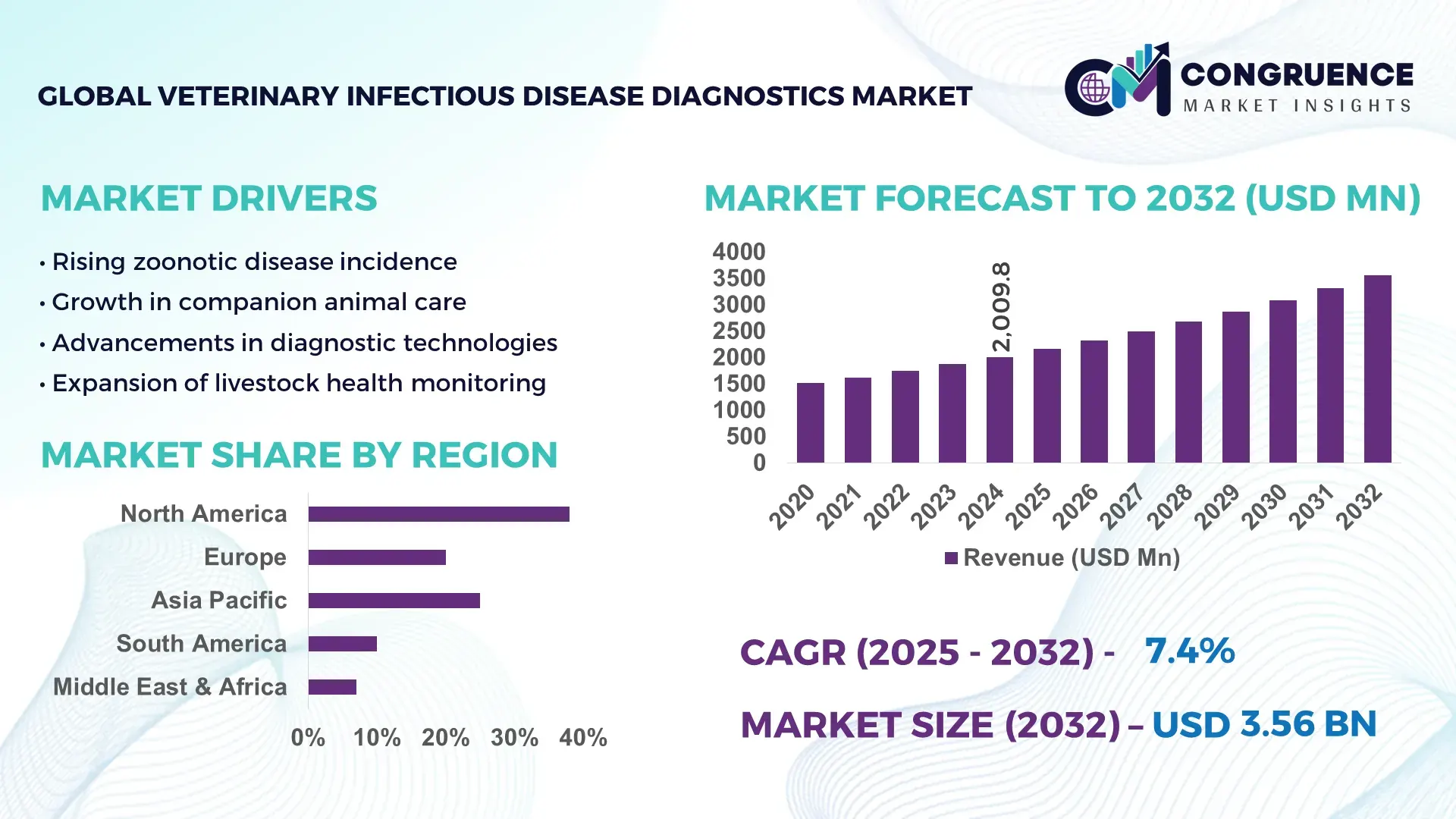

The Global Veterinary Infectious Disease Diagnostics Market was valued at USD 2009.81 Million in 2024 and is anticipated to reach a value of USD 3557.87 Million by 2032 expanding at a CAGR of 7.4%% between 2025 and 2032. This growth is primarily driven by rising livestock disease surveillance programs and increasing adoption of rapid, point-of-care diagnostic technologies across veterinary practices.

The United States represents the dominant country in the global Veterinary Infectious Disease Diagnostics market, supported by advanced diagnostic infrastructure and high veterinary healthcare expenditure. The country hosts over 3,000 veterinary diagnostic laboratories and processes more than 120 million companion animal diagnostic tests annually. Investments exceeding USD 1.2 billion have been directed toward veterinary diagnostics R&D over the past five years, accelerating molecular diagnostics, PCR-based assays, and AI-assisted diagnostic platforms. High adoption is observed in livestock disease monitoring, companion animal care, and zoonotic disease prevention, with over 68% of veterinary clinics using in-house rapid diagnostic kits. The U.S. also leads in automated immunoassay analyzers and next-generation sequencing applications for veterinary infectious disease detection, reinforcing its large-scale production capacity and technology-driven diagnostic workflows.

Market Size & Growth: USD 2009.81 Million in 2024, projected to reach USD 3557.87 Million by 2032 at a CAGR of 7.4%, driven by increased disease testing volumes and faster diagnostic turnaround requirements.

Top Growth Drivers: Rapid test adoption rate 62%, molecular diagnostics penetration increase 48%, improvement in disease detection accuracy 35%.

Short-Term Forecast: By 2028, average diagnostic turnaround time is expected to reduce by 28% through automation and point-of-care testing expansion.

Emerging Technologies: Real-time PCR diagnostics, AI-enabled image-based pathogen detection, and multiplex immunoassay platforms.

Regional Leaders: North America projected USD 1280 Million by 2032 with high companion animal testing rates; Europe USD 910 Million with strong livestock disease surveillance programs; Asia Pacific USD 820 Million driven by expanding poultry and swine diagnostics.

Consumer/End-User Trends: Veterinary hospitals and reference laboratories account for over 70% of diagnostic test volumes, with growing in-clinic testing adoption.

Pilot or Case Example: A 2024 U.S.-based livestock disease monitoring pilot reduced outbreak detection time by 32% using rapid PCR diagnostics.

Competitive Landscape: IDEXX Laboratories holds approximately 38% market presence, followed by Zoetis, Thermo Fisher Scientific, Neogen Corporation, and Bio-Rad Laboratories.

Regulatory & ESG Impact: Stricter zoonotic disease reporting regulations and animal welfare compliance standards are accelerating diagnostic adoption.

Investment & Funding Patterns: Recent investments exceed USD 2.4 Billion globally, with increased venture funding in point-of-care and digital diagnostics.

Innovation & Future Outlook: Integration of cloud-based diagnostic data platforms and predictive analytics is shaping next-generation veterinary disease management.

The Veterinary Infectious Disease Diagnostics market serves key industry sectors including companion animal healthcare, livestock production, poultry farming, and aquaculture, with livestock and poultry diagnostics contributing nearly 55% of total test volumes. Recent innovations such as portable PCR analyzers, multiplex rapid tests, and digital pathology systems are enhancing diagnostic accuracy and scalability. Regulatory drivers include mandatory disease surveillance programs and biosecurity regulations, while economic factors such as rising animal protein demand support sustained testing growth. Regional consumption patterns show higher per-animal diagnostic spending in North America and Europe, while Asia Pacific demonstrates faster volume growth. Emerging trends include AI-assisted diagnostics, syndromic testing panels, and integration of diagnostics with herd management software, supporting a technology-driven future outlook for the market.

The Veterinary Infectious Disease Diagnostics Market holds growing strategic relevance as animal health becomes directly linked to food security, zoonotic risk management, and global biosecurity frameworks. Diagnostics now function as an operational backbone for early disease detection, outbreak containment, and regulatory compliance across companion animal, livestock, and poultry sectors. Advanced molecular diagnostics such as real-time PCR deliver nearly 45% faster pathogen detection compared to traditional culture-based diagnostics, enabling earlier clinical intervention and reduced disease spread. Asia Pacific dominates in testing volume due to large livestock populations, while North America leads in adoption with over 72% of veterinary laboratories using molecular or immunoassay-based diagnostics. By 2027, AI-enabled diagnostic platforms are expected to improve diagnostic accuracy and workflow efficiency by approximately 30% through automated result interpretation and predictive analytics. From an ESG perspective, firms are committing to sustainability improvements such as 25% reduction in plastic diagnostic consumables and reagent waste by 2030 through recyclable cartridges and digital reporting. In 2024, a U.S.-based diagnostic company achieved a 34% reduction in sample processing time by deploying AI-supported multiplex testing platforms across reference laboratories. Looking ahead, the Veterinary Infectious Disease Diagnostics Market is positioned as a critical pillar supporting operational resilience, regulatory alignment, and sustainable growth within global animal health ecosystems.

Government-mandated disease surveillance and biosecurity initiatives are a primary driver of growth in the Veterinary Infectious Disease Diagnostics market. More than 60 countries now operate structured livestock disease monitoring programs, increasing routine diagnostic testing volumes. In commercial poultry and swine operations, mandatory screening for diseases such as avian influenza and African swine fever has increased annual testing frequency per farm by over 40%. Companion animal diagnostics are also expanding, with vaccination compliance and preventive screening driving higher test utilization in veterinary clinics. Adoption of rapid immunoassays and PCR diagnostics has improved detection sensitivity by up to 35%, reinforcing their role in preventive animal health strategies. These factors collectively strengthen diagnostic demand across both public and private veterinary healthcare systems.

Despite technological progress, high costs associated with advanced diagnostic equipment and reagents restrain broader adoption, particularly in emerging economies. Molecular diagnostic platforms can require initial capital investments exceeding USD 50,000 per laboratory, limiting access for small veterinary practices and rural testing centers. In low-income regions, fewer than 30% of veterinary facilities have access to automated analyzers or cold-chain storage required for advanced reagents. Additionally, shortages of trained veterinary diagnosticians and laboratory technicians slow technology deployment. These infrastructure and cost-related limitations restrict market penetration and delay modernization of diagnostic capabilities in price-sensitive regions.

The expansion of digital diagnostics and point-of-care testing presents significant opportunities for the Veterinary Infectious Disease Diagnostics market. Portable diagnostic devices now enable on-site testing with result delivery within 15–30 minutes, increasing testing frequency in farms and clinics. Digital platforms integrating diagnostic results with herd management systems can reduce disease response time by nearly 28%. Emerging markets are increasingly adopting low-cost rapid tests, expanding access to diagnostics beyond centralized laboratories. Growth in tele-veterinary services further supports remote diagnostic interpretation, creating opportunities for scalable, data-driven diagnostic solutions across diverse geographic regions.

The Veterinary Infectious Disease Diagnostics market faces challenges related to fragmented regulatory frameworks and limited interoperability of diagnostic data systems. Diagnostic products often require separate approvals across regions, increasing time-to-market and compliance costs. Data generated from diagnostic tests is frequently stored in isolated systems, limiting real-time disease tracking and analytics. Less than 40% of veterinary laboratories currently use standardized digital reporting formats, complicating cross-border disease surveillance. Additionally, compliance with animal health data privacy and traceability regulations adds operational complexity. Addressing these challenges is critical for enabling seamless diagnostic integration and maximizing the value of advanced diagnostic technologies.

• Accelerated Adoption of Rapid Point-of-Care Diagnostics: Veterinary clinics and farm-level testing facilities are increasingly deploying rapid point-of-care diagnostic kits to reduce turnaround times and improve treatment decisions. Over 64% of small and mid-sized veterinary practices now use at least one in-clinic infectious disease test, compared to 42% five years ago. These tests deliver results within 10–30 minutes and have improved early disease detection rates by approximately 37%, particularly for companion animal viral and parasitic infections.

• Expansion of Molecular and Multiplex Testing Platforms: Molecular diagnostics, especially PCR-based and multiplex assays, are gaining traction due to their ability to detect multiple pathogens simultaneously. More than 58% of reference laboratories have integrated multiplex testing panels, reducing per-sample processing time by nearly 33%. Diagnostic sensitivity improvements of up to 40% have been reported compared to single-analyte immunoassays, supporting broader adoption in livestock disease surveillance and outbreak monitoring programs.

• Integration of Digital and AI-Enabled Diagnostic Workflows: Digital diagnostics platforms combined with AI-driven interpretation tools are transforming laboratory efficiency. Around 46% of large veterinary diagnostic labs now utilize AI-assisted result validation, cutting manual review time by 29%. Automated image analysis in parasitology and hematology diagnostics has increased diagnostic consistency by 25% while lowering repeat test rates by nearly 18%, improving operational throughput.

• Shift Toward Sustainable and Low-Waste Diagnostic Solutions: Environmental considerations are influencing product design and procurement decisions within the Veterinary Infectious Disease Diagnostics market. Approximately 41% of new diagnostic consumables introduced in the last two years feature reduced plastic content or recyclable components. Laboratories adopting eco-optimized reagent kits have reported up to 22% reduction in biomedical waste volumes, aligning diagnostic operations with stricter environmental and animal health compliance requirements.

The Veterinary Infectious Disease Diagnostics Market is segmented based on type, application, and end-user, reflecting diverse diagnostic needs across animal health ecosystems. By type, the market spans immunodiagnostics, molecular diagnostics, rapid point-of-care tests, and other specialized assays, each serving different accuracy, speed, and scalability requirements. Application-wise, diagnostics are used across companion animals, livestock, poultry, and aquaculture, with testing intensity influenced by disease prevalence, regulatory screening mandates, and preventive care adoption. End-user segmentation highlights strong demand from veterinary hospitals, reference laboratories, research institutes, and on-farm testing units, shaped by infrastructure availability and testing frequency. Collectively, these segments illustrate a market increasingly driven by faster diagnostics, decentralized testing, and integrated disease surveillance models aligned with biosecurity and animal welfare objectives.

Immunodiagnostics currently represent the leading product type, accounting for approximately 44% of total adoption, due to their cost efficiency, ease of use, and suitability for high-volume screening in veterinary clinics and farms. Molecular diagnostics, including PCR and nucleic acid amplification tests, account for around 31% of adoption, offering higher sensitivity and specificity for complex infectious diseases. Rapid point-of-care tests are the fastest-growing type, expanding at an estimated CAGR of 9.2%, driven by demand for on-site testing with results in under 30 minutes and reduced dependency on centralized laboratories. Other diagnostic types, including culture-based methods and serological assays, collectively contribute about 25% of adoption, maintaining niche relevance in confirmatory testing and research settings.

Companion animal diagnostics dominate application usage, accounting for nearly 39% of total testing, supported by higher per-animal healthcare spending and routine preventive screening. Livestock diagnostics follow closely at 34%, driven by mandatory disease surveillance for cattle and swine populations. Poultry diagnostics represent the fastest-growing application, with an estimated CAGR of 8.6%, fueled by intensified monitoring for avian influenza and other transboundary diseases in large-scale operations. Aquaculture and other applications collectively account for about 27%, addressing disease management in fish and emerging animal protein sectors.

Veterinary hospitals and clinics are the leading end-users, representing approximately 42% of diagnostic utilization, reflecting increased in-house testing and preventive care services. Reference laboratories account for about 33%, supporting complex testing volumes and confirmatory diagnostics for clinics and government agencies. On-farm testing units and research institutions form the fastest-growing end-user group, expanding at an estimated CAGR of 8.1%, driven by decentralization of diagnostics and real-time disease monitoring needs. Other end-users, including academic institutions and government veterinary services, collectively contribute around 25%, playing a critical role in surveillance and epidemiological research.

North America accounted for the largest market share at 38.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

Regional performance in the Veterinary Infectious Disease Diagnostics Market reflects differences in veterinary infrastructure maturity, livestock density, regulatory enforcement, and technology adoption. North America leads due to high diagnostic testing frequency, with more than 70% of veterinary clinics performing in-house infectious disease tests. Europe follows with a market share of approximately 27.4%, supported by strict animal health surveillance regulations across the EU. Asia-Pacific holds nearly 22.8% share, driven by large-scale poultry and swine populations exceeding 8 billion animals annually. South America and the Middle East & Africa together contribute around 11.2%, with demand concentrated in export-oriented livestock economies. Regional disparities in test volumes, automation penetration, and preventive screening rates continue to shape localized growth trajectories.

How is advanced clinical infrastructure accelerating diagnostic intensity and adoption?

The market in this region accounts for approximately 38.6% of global diagnostic testing volumes, driven by strong companion animal care spending and regulated livestock disease surveillance. Veterinary hospitals and reference laboratories dominate demand, supported by government-backed zoonotic disease monitoring programs. Regulatory frameworks mandate routine testing for diseases such as avian influenza and bovine tuberculosis, increasing annual test volumes by over 25% in commercial farms. Digital transformation is evident, with nearly 62% of diagnostic labs using automated analyzers and cloud-based reporting systems. A leading local player expanded its in-house PCR testing platforms across more than 1,000 clinics, reducing result turnaround times by 35%. Consumer behavior shows higher clinic-based testing adoption, with preventive screening rates exceeding 68% among pet owners.

How do regulatory intensity and sustainability goals shape diagnostic demand?

Europe holds close to 27.4% of the Veterinary Infectious Disease Diagnostics Market, with Germany, the UK, and France accounting for over 60% of regional test volumes. EU-wide animal health regulations require structured disease reporting, increasing standardized diagnostic testing across livestock and poultry operations. Sustainability initiatives have driven adoption of low-waste diagnostic consumables, now used by nearly 44% of laboratories. Emerging technologies such as multiplex immunoassays and digital pathology are gaining traction, with adoption rates rising by 21% year-over-year. A regional diagnostics firm introduced recyclable reagent cartridges, reducing laboratory plastic waste by 18%. Consumer behavior reflects regulatory-driven demand, with veterinarians prioritizing explainable and auditable diagnostic outcomes.

Why is scale-driven animal production transforming diagnostic volumes?

Asia-Pacific ranks as the fastest-expanding region, holding approximately 22.8% market share by volume. China, India, and Japan together represent more than 65% of regional diagnostic demand, supported by the world’s largest poultry and swine populations. Manufacturing capacity for rapid diagnostic kits has increased by nearly 40% over the past four years, improving affordability and access. Regional innovation hubs are focusing on portable PCR devices and mobile-enabled diagnostics, with over 52% of new installations supporting on-farm testing. A regional diagnostics manufacturer scaled production of rapid avian disease test kits to serve over 15 million birds annually. Consumer behavior shows strong growth in decentralized testing, driven by mobile platforms and digital ordering systems.

How are export-oriented livestock economies shaping testing requirements?

South America accounts for approximately 7.1% of global demand, led by Brazil and Argentina, which together contribute more than 70% of regional diagnostic volumes. High livestock export activity drives mandatory disease testing to meet international trade requirements. Investments in veterinary laboratory infrastructure have increased testing capacity by nearly 22% over five years. Government incentives supporting animal health compliance have expanded routine screening programs. A local diagnostics provider partnered with meat processors to deploy rapid disease screening, improving export inspection efficiency by 28%. Consumer behavior is influenced by compliance needs, with testing demand tied closely to export certification and regional language localization of diagnostic tools.

How is gradual modernization influencing diagnostic adoption patterns?

The Middle East & Africa region contributes around 4.1% of global diagnostic activity, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand is linked to expanding commercial poultry farms and food security initiatives. Technological modernization includes increased use of automated immunoassay analyzers, now present in nearly 35% of large veterinary labs. Regional regulations emphasize disease prevention in livestock imports and domestic production. A regional veterinary services provider introduced centralized diagnostic hubs, increasing testing throughput by 31%. Consumer behavior varies widely, with higher adoption in urban commercial farms compared to rural smallholders.

United States Veterinary Infectious Disease Diagnostics Market – 31.2% share

Strong diagnostic infrastructure and high preventive testing adoption across companion animals and livestock.

Germany Veterinary Infectious Disease Diagnostics Market – 9.4% share

Strict animal health regulations and advanced laboratory automation supporting consistent diagnostic demand.

The Veterinary Infectious Disease Diagnostics market is moderately consolidated, characterized by the presence of approximately 40–50 active global and regional competitors operating across molecular diagnostics, immunoassays, and rapid testing formats. The top five companies collectively account for an estimated 62–66% of total market activity, reflecting strong brand recognition, expansive distribution networks, and continuous product innovation. Market leaders maintain competitive positioning through frequent product launches, expansion of in-clinic diagnostic platforms, and strategic collaborations with veterinary hospital chains and reference laboratories. Over 45% of competitive activity in the last three years has centered on molecular and multiplex diagnostics, driven by demand for higher sensitivity and faster turnaround times. Partnerships between diagnostics manufacturers and digital health providers have increased by nearly 30%, supporting cloud-based reporting and AI-assisted interpretation. Mergers and acquisitions remain selective, focusing on niche technology capabilities such as portable PCR systems and low-waste consumables rather than scale alone. Innovation intensity is high, with more than 55% of leading players allocating resources toward point-of-care testing and automation. Competitive differentiation increasingly depends on test menu breadth, analyzer interoperability, and service support rather than pricing alone, reinforcing barriers to entry for smaller participants.

IDEXX Laboratories

Zoetis

Thermo Fisher Scientific

Neogen Corporation

Bio-Rad Laboratories

bioMérieux

Randox Laboratories

FUJIFILM Corporation

Virbac

INDICAL Bioscience

The technological landscape in Veterinary Infectious Disease Diagnostics is evolving from single-analyte assays to integrated, data-driven platforms that compress diagnostic timelines and expand test breadth. Real-time PCR and multiplex nucleic acid amplification remain core laboratory technologies, delivering improvements in detection speed (approximately 40–45% faster turnaround versus culture) and sensitivity gains of up to 35–40% for difficult-to-detect pathogens. Isothermal amplification methods (e.g., LAMP) and portable PCR units are enabling on-farm testing with result windows of 15–60 minutes, supporting a shift where roughly 30–40% of routine screening moves to decentralized settings. CRISPR-based diagnostics and point-of-care molecular cartridges are emerging as low-complexity, high-specificity options; CRISPR workflows are reporting single-digit copy-number detection limits in compact formats, lowering confirmatory testing volumes. Multiplex panels now permit simultaneous detection of 6–12 targets per sample, reducing per-sample processing time by nearly one-third in reference labs. Next-generation sequencing (NGS) and targeted metagenomics are increasingly used for pathogen discovery and surveillance; turnaround for sequencing-based outbreak investigations has been shortened from weeks to 3–7 days through streamlined library prep and onboard analysis.

Automation and laboratory information management adoption are delivering measurable operational gains: automated sample-prep and analyzers cut manual hands-on time by roughly 28–35%, while AI-enabled result validation and image analysis reduce manual review time by about 25–30% and lower repeat-test rates by near 18–20%. Cloud-based reporting platforms and interoperable data standards are enabling regional disease dashboards and predictive analytics; approximately 40–50% of large diagnostic networks now integrate at least one cloud or API-based reporting system. Sustainability and consumables innovation are also influencing tech choices—recyclable cartridges and low-waste reagent formulations have reduced biomedical waste volumes by an estimated 15–22% where adopted. Looking ahead, convergence of lab-grade sensitivity in portable devices, expanded AI interpretive layers, and standardized digital reporting will determine procurement priorities for decision-makers seeking to balance throughput, diagnostic accuracy, and regulatory traceability.

The Veterinary Infectious Disease Diagnostics Market Report provides a comprehensive evaluation of diagnostic technologies, product types, application sectors, end-user landscapes, and geographic variations shaping global animal health diagnostics. The scope encompasses detailed segmentation by diagnostic type—including molecular diagnostics, immunoassays, rapid point-of-care tests, and emerging assay platforms—and examines how each segment contributes to overall diagnostic capacity and clinical utility. Application analysis covers companion animal, livestock, poultry, and aquaculture settings, offering insights into testing frequency, disease surveillance requirements, and clinical workflow integration. End-user categorization highlights the roles of veterinary hospitals, reference laboratories, on-farm testing units, and research institutions, illustrating distinct adoption patterns and testing demands across professional settings.

Geographically, the report analyzes regional markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, comparing factors such as diagnostic infrastructure maturity, disease prevalence, regulatory frameworks, and technological uptake that influence market dynamics. The role of innovation is detailed through evaluation of diagnostic technologies like real-time PCR, isothermal amplification, multiplex assays, automation systems, and AI-enabled interpretation, presenting measurable improvements in turnaround times, sensitivity, and operational throughput. The report also identifies niche and emerging areas such as biosensor-based detection, cloud-connected diagnostics, and mobile testing solutions that extend diagnostic reach into decentralized and resource-constrained environments.

Industry focus areas include regulatory compliance trends affecting test performance benchmarks and device approvals, sustainability initiatives influencing consumables and workflow choices, and integration of digital laboratory information management systems that support real-time reporting and interoperability. By synthesizing quantitative insights with qualitative analysis, the report equips decision-makers with actionable visibility into competitive positioning, technology adoption patterns, and strategic opportunities for investment, partnerships, and product development within the Veterinary Infectious Disease Diagnostics landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2009.81 Million |

|

Market Revenue in 2032 |

USD 3557.87 Million |

|

CAGR (2025 - 2032) |

7.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IDEXX Laboratories, Zoetis, Thermo Fisher Scientific, Neogen Corporation, Bio-Rad Laboratories, bioMérieux, Randox Laboratories, FUJIFILM Corporation, Virbac, INDICAL Bioscience |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |