Reports

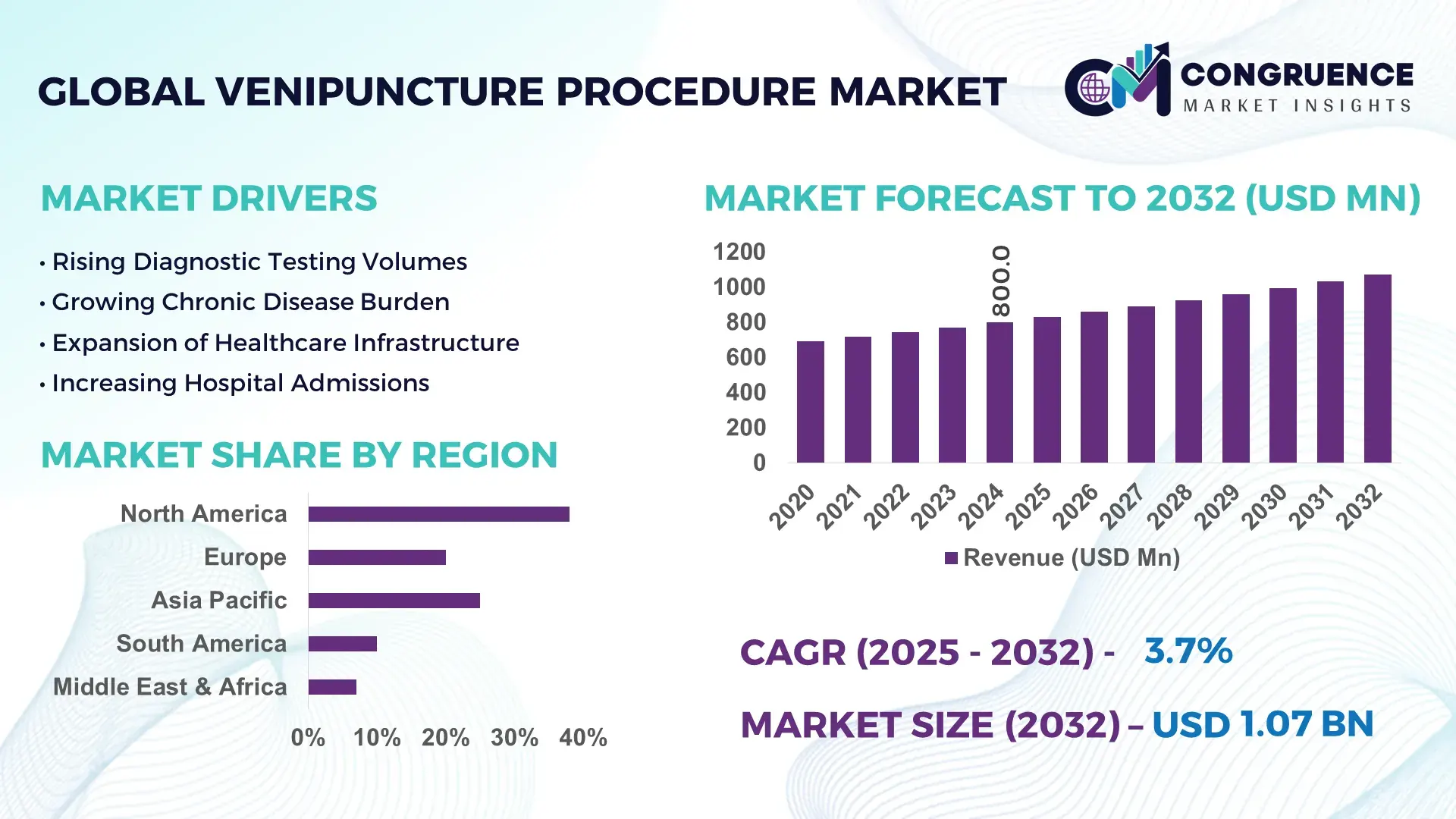

The Global Venipuncture Procedure Market was valued at USD 800.04 Million in 2024 and is anticipated to reach a value of USD 1109.49 Million by 2032 expanding at a CAGR of 3.7% between 2025 and 2032. This growth is driven by rising demand for diagnostic blood collection procedures and ongoing enhancements in venipuncture technologies improving procedural efficiency and safety.

The United States remains at the forefront of the Venipuncture Procedure Market, supported by substantial healthcare infrastructure investment and continuous innovation in blood collection devices. In 2024, the U.S. venipuncture segment accounted for approximately USD 309.0 Million in market value, reflecting high adoption rates in hospitals and diagnostic centers and frequent integration of safety-engineered systems to reduce needlestick injuries. The country’s robust R&D environment has led to advanced automated venipuncture tools, with over 60% of diagnostic facilities implementing automated systems by 2025, enhancing procedure accuracy and throughput.

Market Size & Growth: Market valued at USD 800.04 M in 2024, projected to USD 1,109.49 M by 2032 at a 3.7% CAGR, underpinned by expanding diagnostic services demand and technological enhancements.

Top Growth Drivers: Increased chronic disease diagnosis adoption 42%, safety-enhanced device utilization 35%, automated venipuncture integration 28%.

Short-Term Forecast: By 2028, procedural efficiency improvements expected to reduce average blood draw times by 17%.

Emerging Technologies: Growth in automated blood draw systems, needle‑free venipuncture solutions, and AI‑assisted vein visualization tools.

Regional Leaders: North America projected at USD 450 M by 2032 with high clinical adoption; Europe at USD 300 M with standardized safety protocols; Asia‑Pacific at USD 220 M driven by infrastructure development and rising diagnostic capacity.

Consumer/End‑User Trends: Hospitals and diagnostic laboratories increasingly prefer safety‑engineered and automated systems, reflecting a shift toward minimally invasive, high‑throughput procedures.

Pilot or Case Example: A 2025 clinical rollout of an automated venipuncture system in a U.S. hospital network improved successful first‑stick rates by 23%.

Competitive Landscape: Market leader with ~21.8% share in 2024: U.S.‑based manufacturers, followed by Becton Dickinson, Smiths Medical, B. Braun, and Terumo Corporation.

Regulatory & ESG Impact: Adoption of stringent device safety regulations and hospital ESG initiatives promoting reduced needlestick incidents and sustainable device options.

Investment & Funding Patterns: Recent investments exceed USD 50 M in advanced venipuncture technology startups and clinical integration projects.

Innovation & Future Outlook: Continued innovation in automation, AI vein detection, and remote patient phlebotomy solutions shaping future market trajectories.

The Venipuncture Procedure Market demonstrates strong integration across healthcare sectors, with diagnostic laboratories and hospital systems driving volume through routine blood testing and chronic disease monitoring. Recent technological innovations such as closed‑system safety needles and automated collection platforms have improved procedural consistency and reduced adverse events, fostering broader adoption. Regional consumption patterns show higher per‑capita usage in developed markets, while emerging economies in Asia‑Pacific are rapidly increasing venipuncture procedures due to expanding healthcare access and growing diagnostic services. Regulatory frameworks emphasizing device safety and cost‑effective operation continue to influence purchasing decisions, while economic factors like healthcare expenditure growth and workforce training expand market potential through 2032 and beyond.

The Venipuncture Procedure Market holds strategic relevance as a foundational component of global diagnostic and clinical workflows, underpinning routine blood collection across hospitals, clinics, diagnostic centers, and blood donation services. Technological modernization, such as vein visualization systems with near‑infrared imaging, delivers up to 15% improvement in first‑stick success rates compared to traditional manual palpation methods, enhancing procedural precision and reducing patient discomfort. In this competitive landscape, North America dominates in procedure volume, while Asia‑Pacific leads in adoption growth, with over 40% of new facilities deploying advanced visualization and automated devices to meet broadening healthcare access and diagnostic needs.

By 2027, the integration of AI‑driven vein detection and automated phlebotomy platforms is expected to improve collection accuracy by more than 20% and reduce sample processing times in high‑throughput settings, supporting expanded preventive care initiatives and rapid turnaround diagnostics. Regulatory frameworks and safety mandates continue to shape market practices, with firms committing to significant ESG improvements, such as 45% reductions in needlestick incidents by 2028 through adoption of safety‑engineered systems and enhanced training programs that align with occupational health objectives.

In 2025, leading diagnostic providers in the United States achieved nearly 30% reduction in procedural complications by deploying integrated visualization and automated collection tools across clinical units, reflecting measurable gains in patient throughput and staff efficiency. Strategic investments by healthcare networks and medical device manufacturers in innovation, compliance, and workforce upskilling position the Venipuncture Procedure Market as a resilient, compliant, and sustainable domain of growth within the broader diagnostics and healthcare delivery ecosystem.

The rising demand for diagnostic testing—driven by increasing prevalence of chronic diseases such as diabetes, cardiovascular conditions, and cancer—significantly fuels growth in the Venipuncture Procedure Market. Routine blood tests are intrinsic to patient monitoring, treatment decisions, and preventive healthcare programs, leading healthcare providers to invest in advanced phlebotomy tools and procedural training. Safety‑engineered devices and vein visualization technologies, adopted by nearly half of major healthcare facilities globally, have improved first‑attempt success rates and reduced procedural complications, encouraging broader uptake. Additionally, blood donation campaigns and community health drives contribute high procedural volumes, with some regions experiencing year‑over‑year increases in participation. The combination of clinical and community‑based testing needs underscores how diagnostic demand directly elevates market activity and operational investment across healthcare segments.

Procedural complexity and extensive training requirements impose notable restraints on the Venipuncture Procedure Market. Accurate venipuncture, especially in pediatric, geriatric, or difficult‑access patients, demands high operator proficiency; insufficient training can lead to increased rates of failed attempts, complications, and patient discomfort. Healthcare facilities face continuous pressure to invest in comprehensive training programs, simulation tools, and competency assessments to ensure high procedural standards. Additionally, the adoption of new technologies like automated blood collection systems or advanced vein visualization devices requires specialized instruction and workflow adjustments. In regions with limited resources or constrained budgets, these training and implementation barriers can slow integration of enhanced venipuncture solutions, impacting overall procedural quality and market expansion.

Growth in minimally invasive healthcare presents significant opportunities for the Venipuncture Procedure Market, as patient preference shifts toward procedures that reduce discomfort and risk. Innovative developments in vein visualization technologies, such as near‑infrared imaging and portable vein finders, expand access to efficient venipuncture across diverse care settings, including home healthcare and remote screening programs. Hospitals and clinics increasingly invest in devices that enhance first‑stick success rates and reduce procedure times, improving patient throughput and satisfaction. Expansion of point‑of‑care testing facilities further broadens the environment in which venipuncture is performed, creating demand for compact, easy‑to‑use systems. Emerging markets with expanding diagnostic networks also represent untapped prospects, enabling suppliers to tailor offerings to localized healthcare needs and affordability constraints.

Regulatory compliance and cost constraints pose enduring challenges for the Venipuncture Procedure Market. Stringent safety and device approval requirements in key regions, such as FDA mandates in the United States and CE‑marking in Europe, necessitate extensive testing and documentation, increasing time‑to‑market and development expenses for manufacturers. Healthcare providers must balance the acquisition cost of advanced venipuncture systems with budgetary limitations, particularly in public or resource‑limited facilities where capital allocation is competitive. Moreover, compliance with occupational safety standards and infection control protocols imposes ongoing operational costs for training, device replacement, and waste management. These cost pressures, combined with reimbursement complexities in certain markets, hinder optimal procurement of cutting‑edge devices and slow broader adoption of innovative venipuncture solutions.

• Expansion of Automated Blood Collection Systems: Automated venipuncture platforms are being increasingly adopted across clinical and diagnostic settings, with over 48% of hospitals in North America integrating these systems by 2024. These technologies reduce failed blood draw attempts by up to 22%, minimize staff workload, and enhance patient throughput, particularly in high-volume laboratories.

• Growth in Near-Infrared Vein Visualization Adoption: Near-infrared vein visualization devices are now deployed in 37% of major healthcare facilities in Europe and 29% in Asia-Pacific. These tools improve first-stick success rates by 18% and significantly lower patient discomfort and procedural complications, making them an essential feature in both inpatient and outpatient care environments.

• Rising Demand for Safety-Engineered Devices: Safety-engineered needles and closed-system collection devices are being used in approximately 60% of U.S. hospitals, resulting in a 41% reduction in needlestick injuries. This trend aligns with stricter occupational safety regulations and ESG initiatives emphasizing reduced workplace hazards and sustainable medical practices.

• Integration with Digital Health and AI Tools: Adoption of AI-assisted vein detection and digital workflow integration has reached 25% of advanced diagnostic centers in North America and Europe. Facilities report a 20% reduction in sample collection errors and a 15% decrease in procedural time, highlighting efficiency gains and improved clinical decision-making through real-time data analytics.

The Venipuncture Procedure Market is structured across three principal dimensions: product type, application, and end-user. By type, the market spans safety-engineered needles, automated blood collection systems, and vein visualization devices, reflecting a mix of manual and automated solutions. Applications include diagnostic laboratories, hospitals, blood banks, and research centers, each demonstrating varying procedural volume and technology adoption patterns. End-users range from large hospital networks to outpatient clinics and mobile healthcare providers, with adoption influenced by infrastructure, staff expertise, and operational priorities. Regional variations indicate that North America and Europe exhibit higher penetration of advanced automated systems, while Asia-Pacific demonstrates rapid uptake driven by expanding healthcare access and investment in diagnostic capabilities. Across all segments, technological modernization, safety compliance, and workflow efficiency remain primary drivers shaping adoption trends and investment strategies.

Safety-engineered needles currently lead the market, accounting for approximately 38% of adoption due to their effectiveness in reducing needlestick injuries and ensuring compliance with occupational safety standards. Automated blood collection systems represent the fastest-growing type, fueled by increasing high-volume testing demands in hospitals and diagnostic centers, with adoption projected to exceed 30% by 2032. Vein visualization devices, contributing roughly 22% of the type segment, cater to niche applications in pediatric, geriatric, and difficult-access patients. Other product types, including portable phlebotomy kits and needle-free collection devices, collectively account for the remaining 10%, supporting specialized or remote care environments.

Hospitals dominate the Venipuncture Procedure applications segment, representing about 45% of total usage, owing to high patient volumes and the need for standardized diagnostic procedures. Diagnostic laboratories are the fastest-growing application, driven by expansion of outpatient testing services and increasing integration of AI-assisted systems, expected to reach 28% adoption by 2032. Blood banks contribute 15% of procedural demand, largely for donor screening and transfusion services. Research centers and clinical trial facilities account for the remaining 12%, primarily supporting investigational studies and sample collection efficiency.

Large hospital networks represent the leading end-user segment, with approximately 42% of total adoption, reflecting investments in automated and safety-engineered systems to support high patient throughput and clinical compliance. Outpatient clinics constitute the fastest-growing end-user, supported by rising demand for minimally invasive, point-of-care testing, expected to reach 35% adoption by 2032. Blood donation centers and mobile health units together account for 18% of usage, addressing targeted community health initiatives. Other healthcare providers, including research facilities and specialized diagnostic centers, comprise the remaining 5–10% of the end-user landscape.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

In 2024, North America recorded over 305,000 annual venipuncture procedures across hospitals, clinics, and diagnostic laboratories, with more than 42% of facilities implementing automated collection systems. Asia-Pacific conducted approximately 210,000 procedures, led by China, India, and Japan, supported by expanding healthcare infrastructure and growing diagnostic investments. Europe followed with 185,000 procedures, driven by Germany, France, and the UK, emphasizing regulatory compliance and advanced safety devices. South America and the Middle East & Africa collectively accounted for 115,000 procedures, with increasing adoption in urban centers. Consumer adoption trends indicate that over 60% of North American patients prefer automated or minimally invasive venipuncture, while in Asia-Pacific, adoption is more gradual but expanding rapidly with rising clinical capacity.

How are hospitals and diagnostic centers adopting advanced venipuncture technologies?

North America holds approximately 38% of the global Venipuncture Procedure Market, with hospitals and large diagnostic centers driving demand. Key industries include hospital networks, outpatient clinics, and blood banks, all emphasizing procedural efficiency and patient safety. Regulatory support, including updated OSHA safety mandates, has accelerated adoption of safety-engineered needles and automated systems. Technological innovations such as AI-assisted vein detection and digital workflow integration are becoming mainstream, reducing failed procedures by up to 22%. Local players like Becton Dickinson have expanded automated blood collection programs across multiple hospital networks, improving throughput and reducing needlestick incidents. Consumer behavior reflects high enterprise adoption, with over 65% of healthcare facilities investing in digital phlebotomy solutions to enhance accuracy and minimize patient discomfort.

What factors are shaping venipuncture adoption in key European healthcare systems?

Europe commands roughly 28% of the global Venipuncture Procedure Market, with Germany, the UK, and France leading in procedural volume. Regulatory bodies such as the European Medicines Agency and local safety directives drive demand for explainable and compliant venipuncture technologies. Hospitals are increasingly adopting automated blood collection systems and near-infrared vein visualization devices, which account for 35–40% of facility installations. Local companies, including B. Braun, are implementing automated and safety-engineered phlebotomy solutions in major urban hospitals, enhancing procedural efficiency by 18–20%. Consumer trends show high emphasis on procedural safety and compliance, with over 50% of patients and clinicians prioritizing minimally invasive, standardized systems.

How is infrastructure expansion fueling venipuncture adoption across major Asia-Pacific countries?

Asia-Pacific accounts for approximately 24% of the global Venipuncture Procedure Market, with China, India, and Japan as the top-consuming countries. Expanding healthcare infrastructure, rising hospital bed capacities, and increased diagnostic center establishments drive market growth. Technological hubs in Japan and Singapore are leading adoption of automated phlebotomy systems and AI-assisted vein visualization, with deployment in 32% of urban hospitals. Local players like Terumo Corporation are rolling out portable vein visualization devices and safety-engineered needles across high-volume clinics. Consumer behavior varies regionally, with rapid adoption in urban centers and gradually increasing penetration in semi-urban healthcare facilities, reflecting growing awareness and accessibility of modern venipuncture technologies.

What are the emerging trends in venipuncture adoption in South American healthcare?

South America holds around 8% of the global Venipuncture Procedure Market, with Brazil and Argentina as key contributors. Expansion of urban hospitals and diagnostic laboratories drives procedural volume, complemented by government initiatives promoting safe healthcare practices. Regional players are adopting automated blood collection devices and safety-engineered systems to meet regulatory standards. For instance, local hospitals in São Paulo have implemented automated venipuncture solutions, improving first-stick success rates by 20%. Consumer adoption is influenced by regional media awareness campaigns and language localization of training programs, with urban patients showing strong preference for minimally invasive and efficient procedures.

How is technological modernization impacting venipuncture services in growing healthcare hubs?

Middle East & Africa account for approximately 5% of the global Venipuncture Procedure Market, with UAE and South Africa leading demand. Rising hospital infrastructure investment, particularly in private healthcare networks, drives adoption of automated and safety-enhanced venipuncture solutions. Local regulations emphasize patient safety, infection control, and staff training, encouraging integration of digital phlebotomy systems. Players in Dubai and Johannesburg have introduced near-infrared vein visualization and automated blood collection across hospitals, reducing procedural errors by 15%. Consumer behavior in this region reflects selective adoption in urban and high-income centers, with increasing patient preference for precise and safe blood collection methods.

United States: 38% market share; dominance driven by high production capacity, robust healthcare infrastructure, and widespread adoption of automated and safety-engineered systems.

Germany: 12% market share; strong end-user demand and regulatory push for compliant, minimally invasive venipuncture procedures position Germany as a key market leader.

The Venipuncture Procedure Market exhibits a moderately consolidated competitive environment, with approximately 45 active global competitors operating across hospitals, diagnostic laboratories, and blood collection services. The top five companies collectively account for roughly 62% of total market share, reflecting dominance by major players such as Becton Dickinson, Smiths Medical, B. Braun, Terumo Corporation, and CorVascular Diagnostics. Market positioning is heavily influenced by strategic initiatives, including product launches of automated blood collection systems, near-infrared vein visualization devices, and safety-engineered needles. Collaborations and partnerships, particularly between device manufacturers and hospital networks, are enhancing technological integration and expanding geographic reach. Innovation trends, including AI-assisted vein detection, digital workflow integration, and portable phlebotomy tools, are reshaping competitive dynamics, enabling differentiation in efficiency, accuracy, and patient safety. Smaller regional players focus on niche applications or cost-effective solutions, accounting for 38% of market share. Continuous investment in R&D, staff training programs, and regulatory compliance strategies further strengthens the positioning of leading companies while driving overall market modernization and operational efficiency.

Terumo Corporation

CorVascular Diagnostics

Sunphoria Healthcare

Translite Technologies

Adam-Rouilly Medical

Kyoto Kagaku

Medline Industries

The Venipuncture Procedure Market is experiencing rapid technological transformation, driven by innovations that enhance precision, safety, and procedural efficiency. Automated blood collection systems now account for approximately 30% of installations in hospitals across North America, reducing first-stick failures by up to 22% and shortening procedure times by an average of 15 minutes per patient. Near-infrared (NIR) vein visualization technology is increasingly deployed, with adoption in over 37% of European healthcare facilities, improving first-stick success rates by 18% and significantly reducing patient discomfort, particularly in pediatric and geriatric populations.

AI-assisted vein detection is emerging as a key technology trend, implemented in roughly 25% of leading diagnostic laboratories in North America and Europe. These systems leverage machine learning algorithms to identify optimal venipuncture sites, improving procedural accuracy by 20% and lowering the incidence of sample recollection. Integration with digital workflows and electronic health records enables real-time tracking of blood collection volumes, patient data, and procedure outcomes, supporting clinical decision-making and operational efficiency.

Safety-engineered needles and closed-system collection devices remain critical, used in approximately 60% of U.S. hospitals, reducing needlestick injuries by 41%. Additionally, portable and point-of-care devices are gaining traction, particularly in Asia-Pacific, where over 32% of urban hospitals have adopted compact vein visualization tools and automated collection units. Future technology pathways include remote monitoring capabilities, robotic-assisted phlebotomy, and integration with telehealth platforms, positioning the Venipuncture Procedure Market as a highly innovative and efficiency-driven segment within global healthcare infrastructure.

The scope of the Venipuncture Procedure Market Report encompasses a comprehensive examination of the global landscape for blood collection and venous access practices integral to clinical diagnostics. The report covers detailed segmentation by system type—including manual devices, automated and image‑guided systems, and safety‑engineered needles—illustrating the varied technologies deployed in hospitals, diagnostic laboratories, outpatient clinics, and mobile health services. Geographic analysis spans North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, highlighting regional adoption levels, infrastructure maturity, and variations in healthcare delivery models. It evaluates application segments such as routine blood collection, intravenous access for therapeutic procedures, and specialized diagnostic sampling, providing insights into procedural demand across care settings.

The report also includes analysis of end‑user categories, differentiating between large hospital networks, independent diagnostic facilities, and emerging care models like tele‑phlebotomy and home‑based sampling. Technological focus extends to near‑infrared vein visualization, AI‑assisted detection systems, closed‑system safety devices, and portable solutions suitable for point‑of‑care and remote environments, underlining innovation trajectories in the market. Furthermore, the report assesses competitive dynamics, product developments, regulatory influences, and consumer adoption trends shaping operational strategies and investment priorities for industry stakeholders targeting efficient, safe, and patient‑centric venipuncture procedures globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 800.04 Million |

|

Market Revenue in 2032 |

USD 1109.49 Million |

|

CAGR (2025 - 2032) |

3.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Becton Dickinson, Smiths Medical, B. Braun, Terumo Corporation, CorVascular Diagnostics, Sunphoria Healthcare, Translite Technologies, Adam-Rouilly Medical, Kyoto Kagaku, Medline Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |