Reports

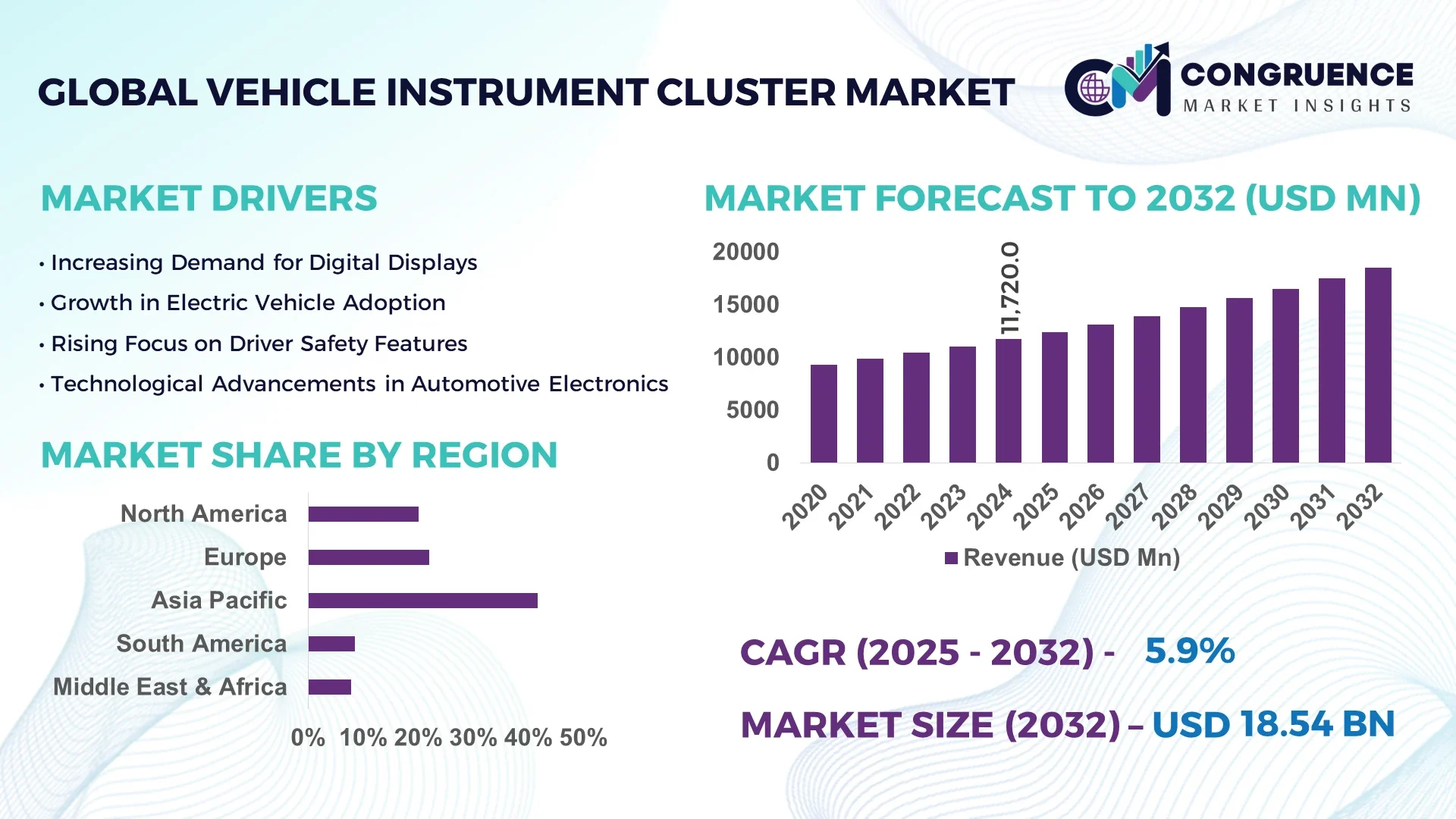

The Global Vehicle Instrument Cluster Market was valued at USD 11.72 Billion in 2024 and is anticipated to reach a value of USD 18.53 Billion by 2032, expanding at a CAGR of 5.9% between 2025 and 2032.

Asia-Pacific dominates the global vehicle instrument cluster market, driven by robust automotive manufacturing in countries like China, India, and Japan. China, in particular, leads due to its expansive vehicle production, increasing demand for advanced automotive features, and substantial investments in automotive technology. The region's focus on electric vehicles and smart mobility solutions further propels the demand for sophisticated instrument clusters.

Globally, the vehicle instrument cluster market is experiencing a significant transformation, with a shift from traditional analog displays to digital and hybrid clusters. This evolution is fueled by consumer demand for enhanced driver experiences, integration of advanced driver-assistance systems (ADAS), and the proliferation of electric vehicles. Manufacturers are investing in innovative technologies such as OLED displays, augmented reality (AR), and artificial intelligence (AI) to offer customizable, intuitive, and safer driving interfaces. Additionally, the rise of connected vehicles necessitates instrument clusters that can seamlessly integrate with infotainment systems, navigation, and real-time vehicle diagnostics, ensuring a holistic and interactive driving experience.

Artificial Intelligence (AI) is revolutionizing the vehicle instrument cluster market by introducing advanced features that enhance driver interaction, safety, and personalization. AI-powered clusters can adapt to individual driver preferences, learning behaviors to provide tailored information and alerts. For instance, AI algorithms can prioritize and display critical information based on driving conditions, reducing cognitive load and minimizing distractions.

Moreover, AI facilitates the integration of voice recognition systems, allowing drivers to interact with their vehicle's systems hands-free, thereby improving safety. These systems can control navigation, climate settings, and infotainment options through natural language processing, making the driving experience more intuitive.

In the realm of safety, AI enhances the functionality of ADAS by processing data from various sensors and cameras to provide real-time alerts and assistance. For example, AI can detect driver fatigue or inattention and prompt necessary warnings or corrective actions. Additionally, AI enables predictive maintenance by analyzing vehicle data to forecast potential issues before they become critical, thus reducing downtime and maintenance costs.

The integration of AI also supports the development of augmented reality (AR) displays within instrument clusters. These AR systems overlay critical information, such as navigation cues and hazard warnings, directly onto the driver's field of view, enhancing situational awareness without diverting attention from the road.

Furthermore, AI contributes to the evolution of connected vehicles by enabling seamless communication between the vehicle and external systems, such as traffic management centers and other vehicles. This connectivity allows for real-time updates and adaptive responses to changing driving conditions, thereby improving overall traffic flow and safety.

In summary, AI is a pivotal force in transforming vehicle instrument clusters into intelligent, adaptive, and interactive systems that significantly enhance the driving experience, safety, and vehicle maintenance.

“In late 2025, BMW has unveiled a groundbreaking new iDrive operating system featuring a striking heads-up display (HUD) that spans the entire windshield. This innovative system integrates a 3D display providing essential driving information, augmented reality for navigation, and driver assistance features. Traditional dashboard gauges have been replaced with a customizable digital version projected onto the windshield. The new system is a part of BMW's all-electric platform, debuting in an unannounced SUV. Additionally, it features a customizable infotainment screen, edge AI to learn user preferences, and a redesigned steering wheel with haptic feedback buttons. This advanced technology aims to enhance connectivity between driver, vehicle, and road, improving the overall driving experience.”

The growing consumer preference for vehicles equipped with advanced comfort and safety features is a significant driver of the car seats market. Manufacturers are responding by developing seats with integrated heating, cooling, massage functions, and ergonomic designs that reduce driver fatigue. Additionally, the incorporation of safety features such as side airbags and seatbelt reminders is becoming standard, driven by stringent safety regulations and consumer awareness. This trend is particularly prominent in the premium and luxury vehicle segments, where consumers are willing to invest in superior seating experiences.

The high cost associated with digital instrument clusters poses a significant restraint to market growth. Advanced display technologies, integrated circuits, and the need for high-resolution graphics increase production expenses. Moreover, the maintenance and potential repair costs of these sophisticated systems can be substantial, deterring adoption, especially in cost-sensitive markets. Additionally, the rising threat of cyber-attacks on digital devices in vehicles raises concerns about data security and system vulnerabilities, further impacting consumer confidence and market expansion.

Developing markets present unexplored growth prospects for the automotive instrument cluster industry, especially in Latin America, Africa, and Asia-Pacific. There is a lot of room for growth for instrument cluster producers as vehicle ownership rises and demand for premium and mid-range vehicles rises in nations like Mexico, Brazil, China, and India. Government programs encouraging the use of hybrid and electric cars in developing nations will increase the need for advanced clusters even more because EVs frequently need complex digital displays to track important metrics like battery life.

Instrument clusters are more susceptible to cybersecurity risks as a result of their increased connectivity and integration with other systems (such as mobile devices, cloud services, and autonomous driving technologies). These systems’ interconnectedness puts them at risk for hacking, data breaches, and illegal access, which might jeopardize user privacy and vehicle safety. One of the biggest challenges facing the automotive industry is ensuring strong cybersecurity protections for these systems, particularly as more connected and autonomous driving technologies are used. It is crucial to protect the data that passes.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping the demand dynamics in the Rebar Machines Market. Pre-bent and cut rebar elements are being prefabricated off-site using automated rebar machines, drastically reducing on-site labor requirements and speeding up project delivery timelines. The demand for high-precision machines capable of delivering consistent product quality is surging, especially in Europe and North America.

Integration of Advanced Display Technologies: The automotive instrument cluster market is witnessing a significant shift towards digitalization, with traditional analog gauges being replaced by digital and fully configurable displays. This transformation is driven by the growing demand for enhanced driver experiences, as consumers seek more interactive and visually appealing interfaces. A notable trend is the rise of head-up displays (HUDs) and OLED-based clusters, which provide better visibility and a futuristic look to vehicle dashboards.

Emphasis on User Experience and Customization: Modern consumers have high expectations for their vehicles, seeking features that enhance both functionality and aesthetics. The demand for enhanced user experience is driving manufacturers to develop instrument clusters that are not only informative but also visually appealing and customizable. Consumers expect their vehicle’s interface to be intuitive and easy to use, similar to their smartphones and other personal devices.

Focus on Sustainability and Eco-Friendly Practices: The instrument cluster industry is witnessing transformative trends driven by technological advancements, sustainability efforts, and evolving consumer demands. In the B2B landscape, automakers are collaborating with technology providers to develop customized clusters tailored to specific vehicle requirements. New materials, such as lightweight polymers and sustainable composites, are gaining traction to enhance efficiency and reduce environmental impact.

The global vehicle instrument cluster market is segmented based on type, application, and end-user, providing a detailed overview of market dynamics across different consumer and industrial categories. These segments help in identifying the growth opportunities and challenges specific to various product categories and usage patterns. The rising demand for advanced digital interfaces and increasing integration of intelligent systems in vehicles have contributed to segment-wise growth. As vehicle manufacturers diversify their product lines to cater to different consumer needs, understanding the leading and emerging segments becomes essential for strategic market positioning.

The vehicle instrument cluster market by type is segmented into analog, digital, and hybrid clusters. Among these, digital instrument clusters lead the market due to their advanced functionalities, modern aesthetics, and seamless integration with in-vehicle infotainment and ADAS systems. Digital clusters are gaining traction in premium and mid-range vehicles, offering drivers customizable displays, better visibility, and real-time updates. They also support complex data visualization, which enhances safety and user experience.

Hybrid instrument clusters are the fastest-growing segment, driven by their ability to provide a balance between traditional analog readability and digital customization. This type is especially popular in transitional vehicle models where OEMs aim to deliver modern features without overwhelming cost implications. Analog clusters, while declining in overall market share, still hold relevance in economy vehicles and cost-sensitive markets, where price competitiveness outweighs technological advancement. The growing penetration of electric and autonomous vehicles further fuels demand for sophisticated digital and hybrid instrument clusters.

Based on application, the market is segmented into speedometers, tachometers, fuel gauges, odometers, temperature gauges, and others. Speedometers account for the largest market share, as they are a critical component in all types of vehicles, regardless of category or price point. Their prominence is maintained by regulatory requirements and user necessity for speed monitoring.

Fuel gauges are another major segment, especially in traditional ICE vehicles, providing essential data for fuel management. However, with the rise of electric vehicles, fuel gauges are being replaced or augmented by battery level indicators, shifting the technology used within this segment.

The fastest-growing application is tachometers and temperature gauges, driven by their increased relevance in performance vehicles and vehicles with complex powertrains. Tachometers assist drivers in optimizing gear shifts and engine performance, while temperature gauges help monitor engine and battery temperatures, a crucial metric in EVs. As vehicles become more connected and intelligent, real-time diagnostic and performance data displays will see further integration into the cluster system, boosting growth across these applications.

The end-user segmentation of the vehicle instrument cluster market includes passenger cars, commercial vehicles, and electric vehicles (EVs). Passenger cars dominate the market due to their massive production volume and higher rate of digital feature adoption. Mid and high-end passenger vehicles increasingly come equipped with advanced digital or hybrid clusters to meet customer expectations for intuitive and connected user experiences.

Electric vehicles (EVs) are the fastest-growing segment in terms of instrument cluster adoption. EVs require highly customizable and detailed information displays for data such as battery levels, charging time, regenerative braking status, and range estimation. The rapid growth in EV adoption globally—fueled by environmental regulations, government incentives, and advancements in battery technology—makes them a critical segment for instrument cluster innovation.

Commercial vehicles maintain steady demand for durable and functionally essential clusters, often tailored for long-haul visibility and reliability over luxury or customization. However, the integration of telematics and fleet management systems in modern commercial vehicles is opening new avenues for digital instrument cluster deployment in this segment as well.

Asia-Pacific accounted for the largest market share at 41.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to the sheer volume of vehicle production, especially in China, India, and Japan, where automotive OEMs are aggressively adopting digital instrument clusters. North America’s fast growth is driven by high consumer demand for connected vehicles, rising integration of AI-powered features, and increasing adoption of electric vehicles across the U.S. and Canada. Meanwhile, Europe is also witnessing substantial growth due to the rise in EV penetration and luxury vehicle production. Regional market trends are shaped by government regulations, consumer behavior, and the maturity of the automotive technology ecosystem in each geography.

Rise in AI Integration and Luxury Vehicle Demand Driving Cluster Innovation

In North America, the market is benefiting from rising demand for luxury vehicles and growing consumer preference for personalized in-car experiences. The U.S. automotive sector is investing heavily in integrating AI-based technologies into digital instrument clusters, including adaptive interfaces, voice-controlled features, and predictive maintenance displays. Over 78% of new vehicles sold in the U.S. in 2024 featured semi-digital or fully digital clusters. The increasing popularity of electric vehicles and autonomous driving features is also boosting demand for advanced cluster systems. Automakers are focusing on next-generation HUDs and multi-display configurations to differentiate their products and improve driver safety and comfort.

Luxury OEMs and EV Adoption Fuel Demand for High-End Displays

Europe’s vehicle instrument cluster market is evolving rapidly with increased adoption of premium vehicles equipped with high-end cluster systems. Countries like Germany and the UK are leading the regional market with strong presence of luxury automakers such as BMW, Audi, and Mercedes-Benz, which have transitioned to fully digital and hybrid clusters. In 2024, over 65% of newly manufactured vehicles in Germany featured fully digital instrument clusters. The region is also pushing for advanced safety and emissions standards, prompting OEMs to adopt smarter dashboard technologies that enhance vehicle efficiency and driver assistance. Additionally, EVs now account for more than 18% of new vehicle sales across the region, further driving demand for integrated, customizable display solutions.

Mass Production and Rising EV Sales Maintain Market Leadership

Asia-Pacific continues to dominate the global market, primarily due to China’s dominance in vehicle manufacturing and technology integration. In 2024, China alone accounted for more than 28% of the global vehicle instrument cluster market. The rapid adoption of EVs and government-backed smart mobility initiatives are pushing OEMs to deploy advanced clusters even in mid-range vehicles. Japan and South Korea are also contributing significantly, with strong investments in automotive innovation and a focus on user-centric dashboard experiences. India is emerging as a fast-growing contributor, with over 21% YoY increase in digital cluster installations in 2024 due to growing vehicle demand and rising tech adoption among domestic automakers.

Steady Growth with Rising Digital Penetration in Passenger Vehicles

South America’s vehicle instrument cluster market is growing steadily, driven by increasing adoption of digital clusters in Brazil and Argentina. In Brazil, over 35% of new passenger vehicles featured hybrid or digital clusters in 2024, up from 24% the previous year. Automakers in the region are gradually shifting from analog to hybrid models due to consumer preference for modern design and better usability. Despite economic constraints in some countries, the growing middle-class population and expanding automotive production capacity are expected to boost demand for advanced instrument displays, especially in passenger cars and light commercial vehicles.

Premium Segment Growth and Import-Driven Demand Elevate Market Potential

The Middle East & Africa market is witnessing gradual adoption of advanced instrument clusters, primarily led by premium vehicle imports. In the UAE and Saudi Arabia, luxury vehicles equipped with fully digital clusters accounted for over 29% of new car sales in 2024. Urbanization, rising income levels, and a growing preference for tech-integrated vehicles are accelerating the transition to digital displays. However, market penetration in Africa remains limited due to affordability challenges and dominance of used or economy vehicles. Still, rising demand for SUVs and pickups with upgraded interior tech features is laying the foundation for steady growth in this region.

China – Valued at USD 3.28 Billion, dominates due to its massive vehicle production volume and high integration of digital cluster systems in both EVs and internal combustion engine vehicles.

United States – Valued at USD 2.19 Billion, leads in terms of innovation, driven by strong consumer demand for AI-enhanced, fully digital clusters in both passenger and luxury segments.

The global vehicle instrument cluster market is characterized by intense competition among established players and emerging entrants. Leading companies are focusing on technological advancements, product innovation, and strategic partnerships to strengthen their market positions. The market is witnessing a shift towards digital and hybrid clusters, driven by consumer demand for advanced features and enhanced driving experiences.

In 2024, hybrid instrument clusters dominated the market, accounting for over 63% of the global revenue. This dominance is attributed to their ability to offer a blend of traditional analog aesthetics with digital functionalities, catering to a broad consumer base. Digital clusters are gaining traction, especially in premium and electric vehicles, due to their customizable interfaces and integration capabilities with advanced driver-assistance systems (ADAS).

Companies are investing in research and development to introduce clusters with augmented reality (AR) and artificial intelligence (AI) features. For instance, the integration of AR in instrument clusters enhances driver awareness by overlaying navigation and hazard information directly onto the windshield. AI-driven clusters adapt to driver preferences, offering personalized information and predictive suggestions.

The competitive landscape is further intensified by regional players focusing on cost-effective solutions for emerging markets. These companies are developing scalable, budget-friendly clusters for compact and mid-range vehicles, tapping into the growing demand in regions like India, Brazil, and Southeast Asia.

Continental AG

Denso Corporation

Visteon Corporation

Robert Bosch GmbH

Panasonic Corporation

Nippon Seiki Co., Ltd.

Magneti Marelli S.p.A.

Yazaki Corporation

Delphi Technologies

Renesas Electronics Corporation

NVIDIA Corporation

Mitsubishi Electric Corporation

Alps Alpine Co., Ltd.

Pricol Limited

The vehicle instrument cluster market is witnessing significant technological evolution, primarily driven by advancements in display, connectivity, and intelligent system integration. The transition from analog to digital and hybrid clusters is creating more immersive and interactive driver interfaces. Among the prominent technologies being adopted, Thin-Film Transistor Liquid Crystal Display (TFT-LCD) and Organic Light-Emitting Diode (OLED) displays are leading the shift. TFT-LCDs are being used extensively due to their clarity and cost-effectiveness, while OLEDs are gaining popularity in premium vehicles for their superior color vibrancy and design flexibility, including curved and seamless panel applications.

Modern instrument clusters are increasingly integrated with infotainment systems, navigation tools, and advanced driver-assistance systems (ADAS), enabling centralized and real-time display of vital information such as traffic updates, lane departure warnings, and driver behavior analytics. These integrations are reducing driver distraction and improving safety. In addition, the deployment of augmented reality (AR) elements into digital clusters is enhancing driver awareness by projecting navigation and hazard data directly onto the dashboard or windshield.

Artificial Intelligence (AI) is playing a pivotal role by making instrument clusters adaptive to driver preferences. Features such as personalized information displays, voice-enabled commands, and predictive diagnostics are becoming standard in higher-end vehicles. AI also assists in enhancing fuel efficiency and maintenance scheduling based on data insights. Connectivity capabilities like Bluetooth, 5G, and vehicle-to-everything (V2X) communication are further allowing over-the-air (OTA) updates for software upgrades, which minimize the need for service visits and keep systems current with new features.

Customization is another major trend, as manufacturers are now allowing drivers to modify the layout, themes, and functionality of their digital clusters to match individual preferences. As these features become mainstream, manufacturers are focusing on developing cost-effective versions for broader market segments, particularly in emerging economies. The integration of sustainable materials and energy-efficient components into cluster design is also emerging, aligning with the automotive industry's shift towards eco-friendly innovation.

In January 2024, Continental AG unveiled a cutting-edge OLED instrument cluster designed specifically for high-end electric vehicles. This new cluster focuses on providing enhanced energy efficiency and superior visual appeal, making it ideal for premium EV models. The OLED technology delivers high-resolution displays with vibrant colors, offering intuitive, customizable interfaces for drivers.

In November 2023, at EVangelise '23, hosted by iCreate in Ahmedabad, the Bengaluru-based startup Auklr Technologies unveiled an advanced intelligent instrument cluster designed to transform the driving experience for electric vehicles. This innovative cluster offers real-time data analytics, customizable interfaces, and integration with various vehicle systems, aiming to enhance user experience and vehicle performance.

In August 2023, TVS Motor Company, an Indian automotive manufacturer, introduced the TVS X, an electric two-wheeler. Built on an entirely new platform, the TVS X features a 10.25-inch instrument cluster, supporting the company's in-built navigation system, NavPro, among other features. The cluster offers functionalities such as live video streaming, gaming, and wellness applications, enhancing the rider's experience.

In February 2024, Peugeot announced its integration of ChatGPT artificial intelligence into its vehicles, making it one of the first car manufacturers to do so. This integration aims to enhance driver interaction with the vehicle's systems through natural language processing, allowing for more intuitive control over various functions.

The Vehicle Instrument Cluster Market Report provides a detailed overview of the global market landscape, capturing evolving consumer preferences, regional dynamics, and the transition from conventional analog systems to fully digital and hybrid instrument clusters. It evaluates the market across key parameters such as product type, application, and end-user, offering valuable insights for stakeholders ranging from automotive OEMs to technology providers and regulatory authorities.

The report covers various cluster types, including analog, digital, and hybrid variants, and explores their adoption across different vehicle categories like passenger cars, commercial vehicles, and electric vehicles. It investigates the integration of speedometers, fuel and temperature gauges, and other application-specific components, highlighting trends in system automation and user-centric interfaces. Special attention is given to electric vehicle adoption and its impact on the growing preference for high-tech digital clusters capable of relaying battery health, range status, and energy regeneration metrics.

Regional insights focus on both mature and developing markets, identifying Asia-Pacific as the leading region in terms of volume, while projecting rapid growth across North America due to increasing demand for smart mobility solutions. The report maps out regional differences in regulations, consumer buying behavior, and OEM strategies that are influencing cluster design and adoption.

In addition, the report provides a comprehensive view of the competitive landscape, profiling major industry players and analyzing their market shares, product innovations, and strategic initiatives. It underscores the role of mergers, partnerships, and technology investments in shaping the future of the instrument cluster industry. Technological themes such as augmented reality, AI integration, and real-time connectivity are discussed in-depth, highlighting how these advancements are transforming the driver experience.

Overall, the report serves as a strategic guide for understanding the current state and future direction of the vehicle instrument cluster market. It equips stakeholders with the knowledge to make informed decisions, identify opportunities, and mitigate challenges in a rapidly digitizing automotive ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Vehicle Instrument Cluster Market |

| Market Revenue (2024) | USD 11.72 Billion |

| Market Revenue (2032) | USD 18.53 Billion |

| CAGR (2025–2032) | 5.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type:

By Application:

By End-User:

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Continental AG, Denso Corporation, Visteon Corporation, Robert Bosch GmbH, Panasonic Corporation, Nippon Seiki Co., Ltd., Magneti Marelli S.p.A., Yazaki Corporation, Delphi Technologies, Renesas Electronics Corporation, NVIDIA Corporation, Mitsubishi Electric Corporation, Alps Alpine Co., Ltd., Pricol Limited |

| Customization & Pricing | Available on Request (10% Customization is Free) |