Reports

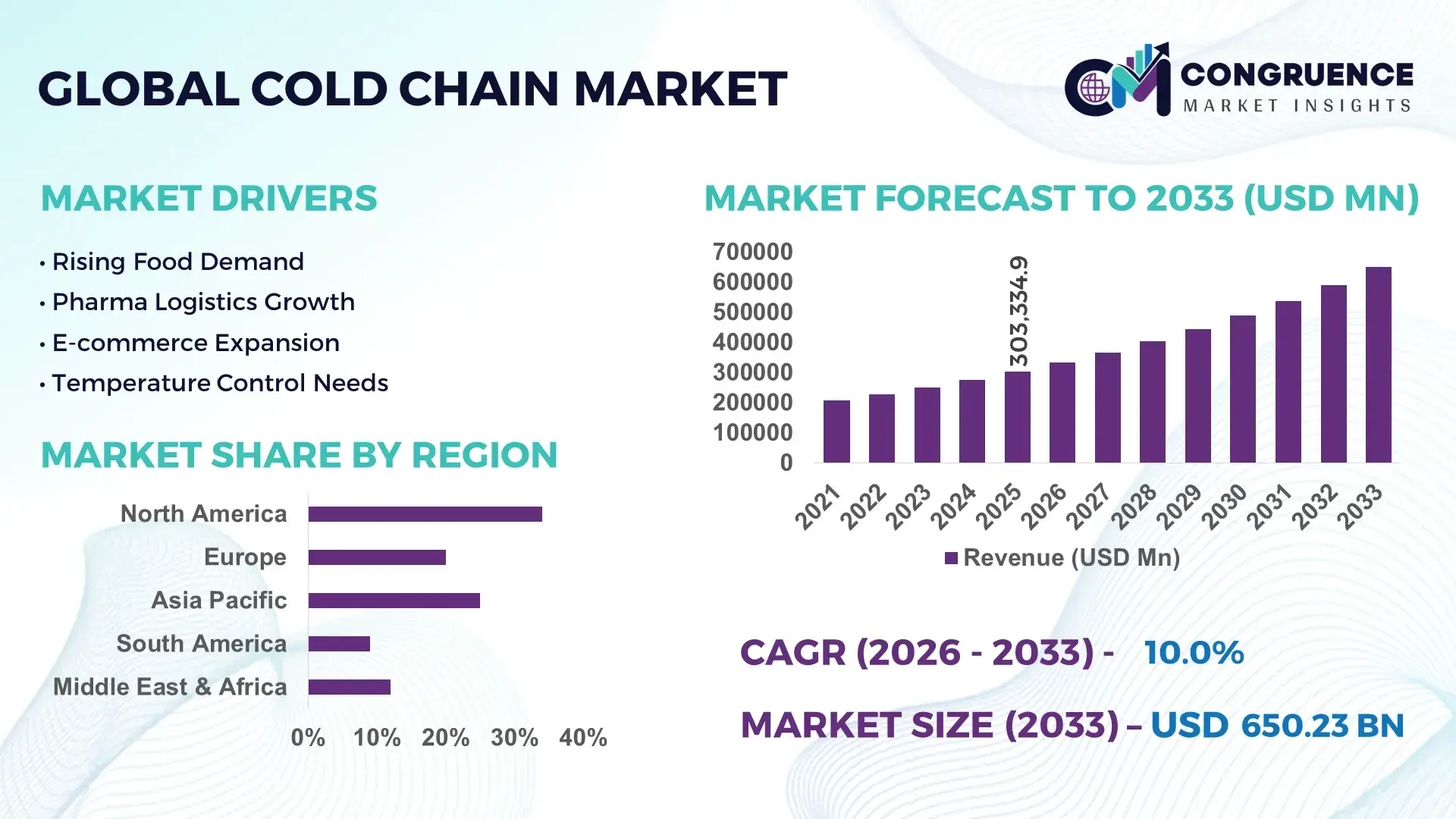

The Global Cold Chain Market was valued at USD 303334.9 Million in 2025 and is anticipated to reach a value of USD 650225.29 Million by 2033 expanding at a CAGR of 10% between 2026 and 2033. Growth is being accelerated by pharmaceutical temperature-control requirements, expanding frozen food logistics networks, and large-scale deployment of IoT-enabled refrigeration monitoring across international supply chains.

The United States remains the dominant country in the global cold chain market, accounting for approximately 28% of total refrigerated warehousing capacity, supported by over USD 8 billion in ongoing logistics infrastructure modernization programs and strong pharmaceutical distribution demand. Compared with India, where organized cold storage penetration remains below 40%, the U.S. operates significantly higher automation levels, with more than 60% of large facilities utilizing sensor-based temperature monitoring and warehouse management technologies. Strategic inventory diversification following Red Sea shipping disruptions has further strengthened domestic cold chain investments.

Businesses prioritizing automated storage, resilient regional distribution hubs, and temperature-traceability capabilities are positioned to secure long-term operational advantages in this high-growth market.

Market Size & Growth: Expanded from USD 303334.9 Million in 2025 to USD 650225.29 Million by 2033 at 10% CAGR, driven by advanced refrigerated logistics and pharmaceutical distribution digitization.

Top Growth Drivers: Pharmaceutical cold logistics (+18%), frozen food demand (+14%), and temperature-monitoring technology adoption (+22%) remain the strongest growth catalysts.

Short-Term Forecast: By 2028, route optimization and warehouse automation are expected to reduce logistics costs by 12% while improving delivery efficiency by 15%.

Emerging Technologies: AI-driven fleet management, IoT temperature sensors, and automated cold storage systems improve monitoring accuracy by over 25%.

Regional Leaders: North America exceeds USD 210 billion, Asia-Pacific approaches USD 180 billion, and Europe surpasses USD 145 billion, supported by automation and traceability adoption.

Consumer/End-User Trends: More than 70% of pharmaceutical manufacturers now require end-to-end temperature visibility across distribution networks.

Pilot/Case Example: In 2025, automated refrigerated warehouse deployments improved storage utilization by 20% and reduced product spoilage by 15%.

Competitive Landscape: Top operators collectively control roughly 30% market share, with leadership concentrated among global logistics and cold storage specialists.

Regulatory & ESG Impact: Energy-efficient refrigeration systems lower facility energy consumption by approximately 18% while supporting stricter compliance standards.

Investment & Funding: Annual sector investments exceed USD 20 billion, with expansion focused on regional distribution hubs and automation upgrades amid supply-chain realignment.

Innovation & Future Outlook: Digital twins, predictive maintenance, and autonomous cold logistics solutions are strengthening operational resilience and network scalability.

The Cold Chain Market is increasingly shaped by pharmaceutical biologics, frozen food distribution, and temperature-sensitive e-commerce fulfillment. Advanced sensor platforms and AI-based monitoring systems now improve temperature compliance rates by more than 20% across major logistics networks. A notable trend is the expansion of decentralized cold storage facilities near consumption centers, supported by stricter product integrity requirements and evolving cross-border supply-chain resilience strategies, setting the stage for deeper strategic market evaluation.

Cold chain infrastructure has evolved from a logistics support function into a strategic asset influencing food security, pharmaceutical integrity, and supply-chain resilience. Competitive differentiation increasingly depends on temperature-controlled distribution capabilities as manufacturers restructure sourcing networks and governments strengthen traceability requirements. Infrastructure modernization and digital monitoring adoption are accelerating, particularly across pharmaceutical and high-value food supply chains where product loss reduction and compliance performance directly affect profitability and market access.

Technology deployment is reshaping operational economics. IoT-enabled refrigeration systems and predictive monitoring platforms reduce temperature excursion incidents by nearly 30% compared with conventional manual inspection models while lowering maintenance costs by approximately 15%. The United States leads in warehouse automation and sensor integration, whereas India is expanding capacity through large-scale cold storage modernization programs and integrated agricultural logistics corridors. This contrast highlights a shift from capacity-led expansion toward efficiency-led network optimization and data-driven asset utilization.

Over the next two to three years, automated cold facilities are expected to exceed 65% adoption among large logistics operators in major industrial markets. For example, pharmaceutical distributors are integrating real-time tracking with refrigerated transport fleets while forming partnerships with specialized storage providers. Companies prioritizing digital visibility, energy-efficient infrastructure, and strategically located distribution networks will strengthen operational control, enhance compliance performance, and secure long-term competitive positioning.

Biopharmaceutical distribution expansion and growing demand for temperature-sensitive food products remain the primary structural drivers of cold chain development. More than 70% of newly approved biologic therapies require controlled-temperature transportation, while automated refrigerated warehouses improve inventory accuracy by approximately 25%. In India, national cold storage modernization initiatives and integrated logistics investments are reducing product wastage across agricultural supply chains. The operational impact is significant: lower spoilage rates, stronger compliance performance, and improved product availability. In response, logistics providers are expanding multi-temperature facilities, deploying IoT-enabled monitoring systems, and forming partnerships with pharmaceutical manufacturers. A key strategic insight is that companies controlling both storage and transportation assets achieve higher service reliability and stronger contract retention than operators focused solely on warehousing.

High capital intensity and uneven infrastructure distribution continue to limit market scalability. Refrigerated warehouses typically consume 35–50% more energy than conventional storage facilities, while refrigeration equipment can account for nearly 40% of facility development costs. In countries such as India and Brazil, significant portions of cold storage capacity remain concentrated near production hubs rather than consumption centers, creating network inefficiencies. These constraints increase transportation costs, reduce asset utilization, and pressure operating margins. To mitigate risks, companies are adopting modular storage models, negotiating long-term energy contracts, and localizing distribution networks. A notable operational insight is that network design inefficiencies often generate higher costs than refrigeration technology itself, making facility placement a critical profitability determinant.

The next phase of market expansion is being shaped by intelligent infrastructure, automation, and advanced analytics. AI-enabled route optimization can reduce transportation fuel consumption by nearly 12%, while predictive maintenance platforms lower refrigeration downtime by approximately 20%. In China, smart logistics parks integrating automated storage, robotics, and digital tracking are accelerating operational efficiency gains. Companies are increasingly investing in digital twins, autonomous material handling systems, and cloud-based visibility platforms to unlock productivity improvements beyond traditional capacity expansion. A particularly valuable opportunity lies in mid-sized pharmaceutical and specialty food networks where digital adoption remains below 50%. Firms developing integrated ecosystems combining monitoring, analytics, and compliance management are creating differentiated service offerings and stronger customer retention.

As cold chain networks become more digitized, execution complexity is emerging as a major long-term challenge. Large operators often manage facilities using multiple software platforms, and integration projects can increase deployment timelines by 20–30%. At the same time, demand for technicians skilled in refrigeration automation, sensor networks, and data analytics is growing faster than workforce availability. In the United States, expanding regulatory documentation requirements are increasing operational oversight burdens across pharmaceutical logistics. These pressures affect scalability, deployment consistency, and system reliability. Companies must address this challenge through workforce development programs, interoperable technology architectures, and strategic technology partnerships. Organizations that successfully integrate infrastructure, software, and skilled talent will achieve stronger operational resilience and sustain competitive advantages as network complexity increases.

AI-Driven Fleet Optimization: Logistics operators are deploying AI-based route orchestration platforms across refrigerated transport networks, reducing idle time by 18% and improving asset utilization by nearly 15%. Rising fuel volatility and tighter delivery windows are accelerating adoption in the United States and Germany. Companies are integrating predictive dispatch systems with telematics platforms, enabling faster route adjustments and lowering temperature excursion incidents by approximately 20% during long-haul distribution.

Expansion of Urban Micro-Cold Hubs: Retail and food distribution companies are increasing investment in localized cold storage facilities located near consumption centers. Average delivery distances have declined by 12%, while same-day fulfillment capacity has improved by over 25% in major metropolitan markets. This shift is being driven by e-commerce grocery growth and labor efficiency requirements. Operators are restructuring networks through smaller automated facilities rather than building large centralized warehouses, creating a more flexible inventory model.

Advanced Refrigerant Transition Programs: Regulatory pressure on high-emission cooling systems is accelerating the deployment of low-global-warming-potential refrigerants. More than 35% of newly commissioned cold storage facilities now incorporate alternative refrigerant technologies, while energy consumption improvements average 10–15% compared with older systems. Companies are modernizing infrastructure portfolios through phased equipment replacement programs and strategic engineering partnerships to improve sustainability performance and compliance readiness.

End-to-End Temperature Visibility: Pharmaceutical and specialty food supply chains are rapidly adopting real-time monitoring platforms. Sensor deployment rates have exceeded 60% among large cold chain operators, improving traceability accuracy by nearly 30%. A notable trend is the integration of temperature data into procurement and inventory planning workflows rather than using it solely for compliance. Companies are scaling cloud-connected monitoring ecosystems to strengthen quality assurance, reduce product losses, and improve operational decision-making.

Refrigerated Storage remains the leading type segment due to its central role in preserving temperature-sensitive products across pharmaceutical, food, and agricultural supply chains. Large-scale facilities support high inventory volumes, network consolidation, and operational scalability, making them critical infrastructure assets. More than 45% of organized cold chain capacity is concentrated in refrigerated storage operations, supported by automation investments and warehouse modernization initiatives. Refrigerated Transport remains essential for network connectivity, while Cold Chain Services continue expanding through outsourced logistics and integrated distribution models.

Temperature Monitoring is the fastest-growing type as enterprises prioritize compliance, traceability, and product integrity. Sensor-enabled monitoring systems have improved temperature accuracy by approximately 25% while reducing spoilage incidents by nearly 15%. Cold Chain Packaging is also gaining strategic importance as pharmaceutical shipments become more specialized and globally distributed. Companies are responding through smart sensor integration, packaging innovation, and multi-site facility expansion. Investment priorities are increasingly shifting from capacity creation alone toward visibility, control, and performance optimization across the entire cold chain ecosystem.

Food and Beverages represent the dominant application segment, supported by extensive distribution requirements across processed foods, beverages, ready-to-eat products, and retail grocery channels. The segment accounts for the largest share of refrigerated storage and transportation activity because of high shipment frequency and broad consumer demand. Product quality preservation remains a key operational priority, with temperature-controlled logistics reducing spoilage losses by approximately 20%. Fresh Produce and Dairy Products continue to generate stable utilization rates due to year-round supply requirements and expanding retail distribution networks.

Pharmaceuticals are the fastest-growing application segment as biologics, vaccines, and specialty therapies require stricter temperature management protocols. More than 70% of advanced biologic products depend on controlled-temperature logistics throughout distribution. Frozen Products remain a mature but strategically important category, benefiting from automation-driven inventory handling and growing organized retail penetration. Companies are expanding dedicated pharmaceutical facilities, increasing monitoring capabilities, and integrating specialized packaging solutions. Demand is increasingly shifting toward high-value products where compliance, traceability, and product integrity directly influence operational performance and customer retention.

Food Manufacturers remain the largest end-user group because they depend heavily on refrigerated storage, transportation, and inventory management throughout production and distribution cycles. Their large shipment volumes, broad retail reach, and continuous replenishment requirements create sustained cold chain utilization. More than 50% of cold storage throughput in many developed markets is linked to food manufacturing activity. Logistics Providers also represent a significant buyer segment as outsourcing models continue expanding across integrated supply chains.

E-commerce Companies are the fastest-growing end-user segment, driven by rising online grocery sales, direct-to-consumer food distribution, and rapid fulfillment requirements. Same-day delivery networks have increased refrigerated handling volumes by more than 20% in several major urban markets. Pharmaceutical Companies and Healthcare Organizations are increasing investments in specialized temperature-controlled infrastructure to support biologics and advanced therapies, while Retail Chains continue expanding localized cold storage capacity. Providers are responding with customized service offerings, dedicated transport fleets, flexible pricing structures, and strategic partnerships designed to capture growing demand from digitally enabled distribution ecosystems.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

Automation-Led Network Optimization

North America maintains the largest concentration of advanced cold chain infrastructure, supported by pharmaceutical logistics, organized food distribution, and highly integrated transportation networks. The region accounts for approximately 34% of global cold chain activity, with strong deployment of warehouse automation and IoT-based monitoring systems. More than 60% of large refrigerated facilities utilize digital temperature management platforms to improve compliance and inventory visibility. Operators continue investing in multi-temperature distribution centers and automated storage systems to increase throughput efficiency. Strategic partnerships between logistics providers and pharmaceutical manufacturers are strengthening specialized cold logistics capabilities while reducing product handling risks across complex distribution networks.

United States Market Outlook: The United States remains the region’s operational center due to its extensive refrigerated warehousing footprint, advanced transportation infrastructure, and strong pharmaceutical manufacturing ecosystem. Large-scale operators continue expanding automated facilities near major consumption corridors. More than 70% of high-value pharmaceutical shipments utilize digitally monitored cold logistics networks. Continued investment in predictive maintenance systems, robotics, and temperature-traceability platforms supports higher asset utilization and strengthens service reliability across national distribution operations.

Sustainability-Driven Infrastructure Modernization

Europe's market is shaped by energy efficiency mandates, food safety standards, and modernization of refrigerated logistics assets. The region represents nearly 28% of global cold chain deployment, with increasing adoption of low-emission refrigeration technologies and smart monitoring solutions. More than 40% of newly commissioned facilities incorporate alternative refrigerant systems to meet sustainability objectives. Pharmaceutical exports and cross-border food distribution continue driving infrastructure upgrades. Operators are integrating automated handling systems and centralized control platforms to improve operational consistency while reducing energy intensity across large-scale facilities.

Germany Market Outlook: Germany serves as the region’s leading cold chain hub due to its industrial scale, logistics connectivity, and advanced food processing sector. The country benefits from extensive refrigerated transportation networks connecting major manufacturing and distribution centers. Automated warehouse penetration exceeds several neighboring markets, supporting faster inventory turnover and improved temperature compliance. Investments in sustainable refrigeration systems and digitally connected logistics platforms continue strengthening Germany’s position as a key operational gateway for temperature-controlled products across Europe.

Rapid Capacity Expansion and Digital Deployment

Asia-Pacific is emerging as the fastest-expanding cold chain market, driven by urbanization, pharmaceutical manufacturing growth, and food supply modernization. The region accounts for roughly 26% of global market activity and is experiencing accelerated investment in refrigerated warehousing and integrated transport networks. Several countries have increased organized cold storage deployment by over 20% during recent expansion cycles. Automation adoption and cloud-based monitoring systems are improving operational efficiency while reducing product losses. Large-scale infrastructure programs and growing domestic consumption continue supporting sustained network development.

China Market Outlook: China remains the most influential market in the region because of its vast food distribution ecosystem, pharmaceutical production capacity, and logistics infrastructure investments. The country continues expanding automated refrigerated warehouses and intelligent logistics parks to support nationwide distribution requirements. Digital monitoring deployment has accelerated across major operators, improving visibility and inventory management. Strong integration between manufacturing clusters and cold logistics providers is enhancing supply-chain performance while supporting large-scale temperature-controlled product movement across domestic and export channels.

Food Export Logistics Strengthening Demand

South America is benefiting from expanding food exports, growing organized retail networks, and modernization of temperature-controlled logistics systems. The region contributes approximately 7% of global cold chain activity, with refrigerated transport receiving significant investment attention. Cold storage capacity expansion programs are improving distribution reliability, particularly for meat, seafood, and fresh produce exports. However, infrastructure disparities and transportation bottlenecks continue affecting network efficiency in several markets. Companies are responding through facility upgrades, logistics partnerships, and deployment of advanced monitoring technologies to improve operational consistency.

Brazil Market Outlook: Brazil dominates regional demand through its large agricultural production base, extensive food processing industry, and export-oriented logistics network. Refrigerated logistics infrastructure plays a critical role in supporting meat and fresh produce distribution. Operators continue expanding strategically located storage facilities near production zones and export corridors. Increased deployment of temperature monitoring technologies is helping reduce spoilage risks while improving export compliance requirements, strengthening Brazil’s position as the region’s primary cold chain market.

Infrastructure Investment Reshaping Distribution Networks

The Middle East & Africa market is advancing through logistics infrastructure development, healthcare investment, and modernization of food distribution systems. The region accounts for roughly 5% of global cold chain activity but is attracting increasing capital toward refrigerated warehouses and pharmaceutical logistics facilities. New logistics corridors and integrated distribution hubs are improving temperature-controlled product movement across major trade routes. Digital monitoring adoption is increasing steadily as operators seek greater traceability and compliance capabilities. Infrastructure expansion remains a central competitive differentiator across leading markets.

United Arab Emirates Market Outlook: The United Arab Emirates functions as a strategic logistics gateway linking Asia, Europe, and Africa through highly developed transport infrastructure. Investments in specialized pharmaceutical logistics facilities and advanced warehousing systems continue accelerating. Major logistics operators are deploying automated temperature monitoring and integrated warehouse management platforms to improve service quality. Strong connectivity through ports, airports, and free-trade zones supports efficient movement of temperature-sensitive products and reinforces the country’s leadership position within the regional cold chain ecosystem.

The market is characterized by competition between global cold storage leaders such as Lineage Logistics, Americold Realty Trust, NewCold, DHL Supply Chain, and Kuehne+Nagel, alongside regional logistics specialists competing on proximity and service flexibility. The top five players collectively control approximately 28–32% of the market, creating a fragmented but increasingly scale-driven structure. Competition centers on automation, network density, temperature visibility, and fulfillment speed rather than price alone. Automated facilities can improve warehouse productivity by 20–30%, while digital monitoring systems reduce product loss by nearly 15%. Companies are expanding through strategic acquisitions, pharmaceutical logistics partnerships, and vertically integrated transportation-storage models. A notable competitive shift is the movement toward AI-enabled warehouse operations and end-to-end traceability platforms. High infrastructure costs, regulatory compliance requirements, and specialized facility development remain major entry barriers. Winning requires scalable infrastructure, technology-enabled visibility, operational reliability, and strong customer integration across the cold chain ecosystem.

Lineage Logistics

Americold Realty Trust

NewCold

DHL Supply Chain

Kuehne+Nagel

DB Schenker

United States Cold Storage

Nichirei Logistics Group

VersaCold Logistics Services

AGRO Merchants Group

Burris Logistics

Congebec Logistics

Snowman Logistics

Coldman Logistics Pvt. Ltd.

Cold chain operators are increasingly relying on IoT sensors, cloud-connected temperature monitoring, and automated warehouse management systems to improve product integrity and inventory control. By 2026, more than 60% of large refrigerated facilities are expected to utilize real-time monitoring platforms. These technologies reduce temperature excursion incidents by approximately 25% and improve inventory accuracy by nearly 20%. Integration between warehouse systems and transportation management software enables continuous product visibility, strengthening compliance performance while lowering spoilage-related operational costs.

Emerging technologies are shifting focus toward predictive intelligence and autonomous operations. AI-enabled route optimization improves fleet utilization by 15% while reducing fuel consumption by around 12%. Digital twin platforms are gaining traction for simulating warehouse performance and refrigeration efficiency before deployment. Compared with traditional manual monitoring processes, AI-driven predictive maintenance lowers equipment downtime by nearly 30%, providing a measurable operational advantage. Pharmaceutical logistics providers and large food manufacturers benefit most because temperature deviations directly impact product quality and regulatory compliance.

Between 2026 and 2028, disruptive technologies including robotics, machine vision inspection, and blockchain-enabled traceability are expected to accelerate across high-value supply chains. Automated cold warehouses process inventory movements up to 35% faster than conventional facilities. Companies investing early in integrated automation ecosystems, predictive analytics, and intelligent refrigeration infrastructure are positioned to secure stronger service reliability, higher asset utilization, and differentiated competitive positioning in increasingly performance-driven cold chain networks.

March 2025 – Americold Realty Trust announced the acquisition of a Houston temperature-controlled facility with planned upgrades, adding approximately 35,700 pallet positions. The expansion strengthens high-turn retail distribution capabilities and increases network capacity in a major logistics corridor. Source: Americold

March 2025 – DHL Supply Chain acquired CRYOPDP and established a strategic partnership with Cryoport, expanding specialized pharmaceutical cold chain services. The transaction covers 100% ownership of CRYOPDP, enhancing clinical trial and cell-and-gene therapy logistics capabilities worldwide. Source: DHL Group

August 2025 – DHL Global Forwarding launched a dual-certified cold chain facility at Kuala Lumpur International Airport supporting both 15–25°C and 2–8°C storage requirements. The development strengthens a regional network comprising 37 Air GxP-certified stations, improving pharmaceutical logistics performance. Source: DHL Global Forwarding

September 2025 – Americold and DP World opened a flagship import-export cold storage hub in Dubai featuring 40,000 pallet positions and 27 loading docks. The facility improves food distribution efficiency across Gulf markets and expands temperature-controlled trade infrastructure.

This report provides comprehensive analysis of the global cold chain market across Refrigerated Storage, Refrigerated Transport, Cold Chain Packaging, Temperature Monitoring, and Cold Chain Services. It evaluates demand patterns across Food and Beverages, Pharmaceuticals, Frozen Products, Fresh Produce, and Dairy Products while assessing adoption trends among Food Manufacturers, Pharmaceutical Companies, Retail Chains, Logistics Providers, Healthcare Organizations, and E-commerce Companies. The study examines deployment concentration, technology penetration, and infrastructure utilization patterns shaping operational performance across the industry.

The report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting country-level investment activity, modernization initiatives, and competitive positioning. Analysis includes IoT monitoring, warehouse automation, AI-enabled logistics optimization, digital traceability systems, and sustainable refrigeration technologies. More than 60% monitoring-system adoption among large facilities and rising automation deployment rates are evaluated to identify future operational shifts. The report supports expansion planning, infrastructure investment decisions, partnership strategies, risk assessment, and long-term competitive positioning between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 303334.9 Million |

|

Market Revenue in 2033 |

USD 650225.29 Million |

|

CAGR (2026 - 2033) |

10% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lineage Logistics, Americold Realty Trust, NewCold, DHL Supply Chain, Kuehne+Nagel, DB Schenker, United States Cold Storage, Nichirei Logistics Group, VersaCold Logistics Services, AGRO Merchants Group, Burris Logistics, Congebec Logistics, Snowman Logistics, Coldman Logistics Pvt. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |