Reports

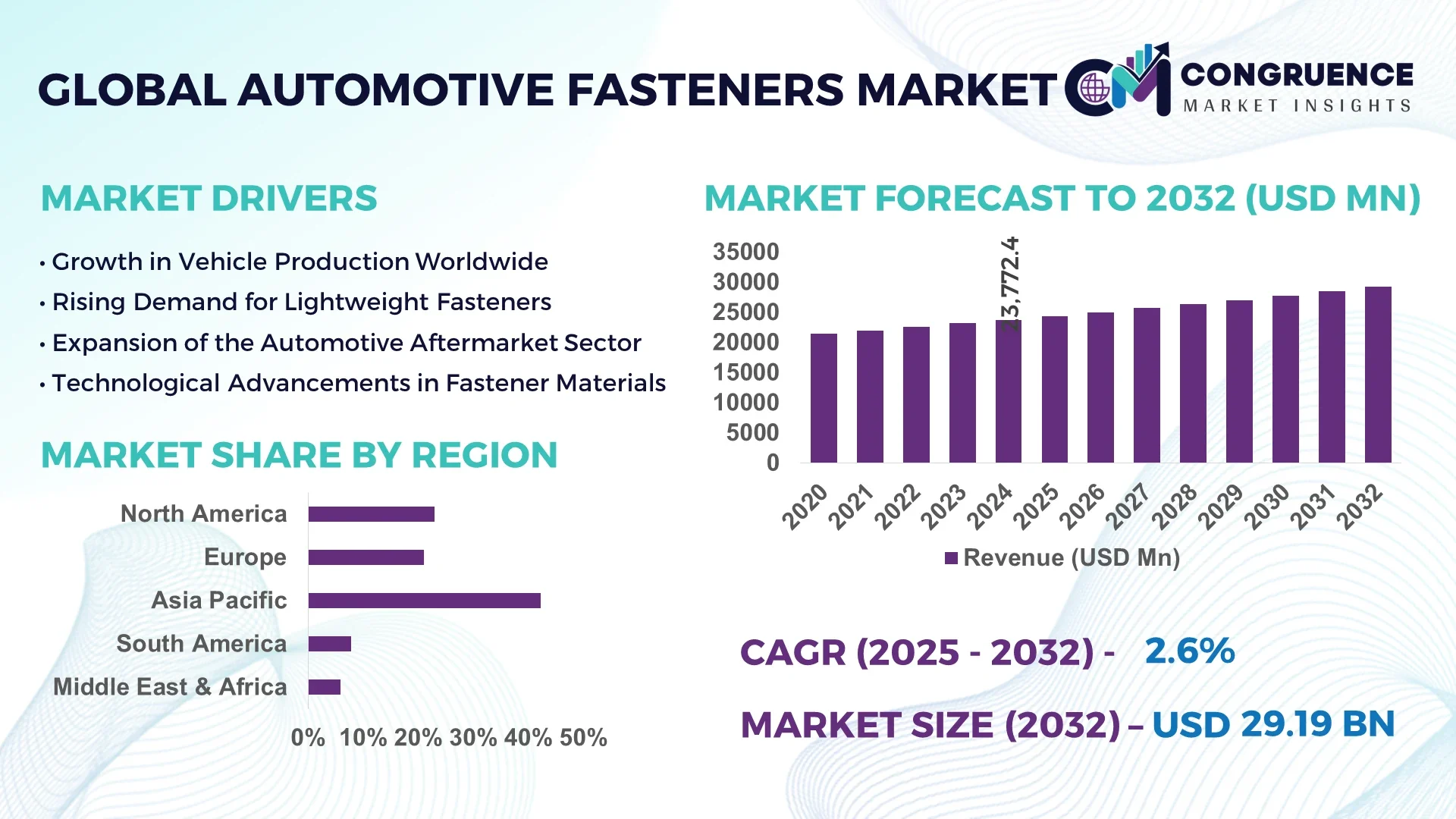

The Global Automotive Fasteners Market was valued at USD 23,772.42 Million in 2024 and is anticipated to reach a value of USD 29,191.22 Million by 2032 expanding at a CAGR of 2.6% between 2025 and 2032.

Japan continues to hold a significant position in the Automotive Fasteners market with advanced manufacturing clusters, extensive automation in precision forging, and consistent investment in EV-specific fastening technologies supporting lightweight and durable component production across engine and body applications.

The Automotive Fasteners Market serves critical sectors including passenger cars, commercial vehicles, and electric vehicle manufacturing, with increasing demand for high-tensile fasteners and lightweight aluminum-based solutions driving product innovation globally. Recent advancements such as smart fastening systems for enhanced torque monitoring, anti-loosening technologies, and corrosion-resistant coatings are reshaping product performance and reliability standards across regions. Environmental regulations are encouraging the adoption of recyclable and low-emission materials within automotive fastener production, particularly in North America and Europe, while Asia-Pacific is witnessing strong growth due to increased vehicle production and infrastructure investment. Shifts towards modular vehicle platforms and the growing integration of advanced electronics in vehicles are influencing fastener design trends, reinforcing the Automotive Fasteners Market’s pivotal role in modern mobility solutions and the future of vehicle manufacturing ecosystems.

Artificial intelligence is transforming the Automotive Fasteners Market by advancing predictive maintenance, improving process efficiency, and reducing operational waste across production lines. AI-driven vision inspection systems now detect micro-cracks, dimensional variances, and coating inconsistencies in fasteners with a significantly higher accuracy rate, reducing defect rates by up to 45% in advanced facilities. In the Automotive Fasteners Market, AI-powered demand forecasting models enable manufacturers to align production schedules with OEM requirements, reducing lead times while optimizing inventory levels, which is critical in just-in-time manufacturing systems. Machine learning algorithms assist in tool wear prediction during cold and hot forging processes, minimizing downtime and ensuring consistent quality output within the Automotive Fasteners Market.

AI-enabled robotics and cobot systems facilitate automated sorting, assembly, and packaging of fasteners, ensuring precision alignment with stringent OEM tolerances and enhancing worker safety by reducing manual handling. Predictive analytics support the Automotive Fasteners Market by providing real-time insights into machinery health, reducing unplanned stoppages and optimizing resource allocation. Additionally, AI contributes to material optimization in fastener design by simulating stress and load patterns across various automotive components, aiding the development of lightweight, high-durability fasteners for EV platforms. With evolving consumer demand for customized vehicle options, AI-enabled flexible manufacturing within the Automotive Fasteners Market is helping manufacturers efficiently manage multiple fastener variants without compromising throughput. These advancements position AI as a critical enabler for manufacturers aiming to enhance operational excellence, quality control, and adaptability in the Automotive Fasteners Market.

“In March 2025, a major Japanese automotive fastener manufacturer implemented an AI-driven inspection system that reduced inspection cycle times by 38% while improving defect detection rates by 41%, enabling precise identification of coating inconsistencies and dimensional defects in high-tensile fasteners for electric vehicle production.”

The Automotive Fasteners Market is experiencing evolving dynamics shaped by advancements in electric vehicle manufacturing, increasing demand for lightweight materials, and a rising focus on precision-engineered fastening solutions for modern vehicle platforms. The market benefits from sustained growth in automotive production, particularly in Asia-Pacific, while stringent regulatory frameworks are pushing manufacturers toward the adoption of sustainable and recyclable materials within fastener production. Technological progress in corrosion-resistant coatings and smart fastening systems is influencing product development trends in the Automotive Fasteners Market. Additionally, the adoption of modular vehicle architecture and advanced driver assistance systems (ADAS) integration are impacting the demand for high-performance fasteners, driving product diversification to cater to evolving OEM requirements across global markets.

The rapid increase in electric vehicle production globally is a significant driver for the Automotive Fasteners Market, influencing the demand for lightweight and high-durability fastening solutions. With EV production surpassing 10 million units globally in 2024, manufacturers require fasteners that can handle the unique stress, vibration, and thermal management needs of battery systems and lightweight vehicle bodies. High-tensile and aluminum alloy fasteners are increasingly being used for EV battery enclosures and powertrain components to maintain structural integrity while reducing overall vehicle weight. This shift is also accelerating the adoption of advanced anti-corrosion coatings and specialized designs that ensure reliability under high-voltage environments, strengthening the Automotive Fasteners Market’s relevance in the evolving automotive landscape.

Fluctuating prices of essential raw materials such as steel, aluminum, and specialty alloys are posing challenges within the Automotive Fasteners Market by increasing manufacturing costs and impacting production planning. In 2024, global steel prices witnessed volatility due to supply chain disruptions and geopolitical factors, causing automotive fastener manufacturers to navigate unpredictable procurement costs while maintaining quality standards. This volatility complicates long-term contracts with OEMs, who demand cost stability in their supply chains. Additionally, the scarcity of high-grade aluminum and specialized coatings required for corrosion resistance further limits manufacturers' ability to scale production efficiently, adding layers of complexity to pricing strategies within the Automotive Fasteners Market.

The increasing integration of smart fastening systems represents a promising opportunity within the Automotive Fasteners Market, driven by the automotive industry’s shift towards intelligent assembly lines and quality control. Smart fasteners embedded with sensors can monitor torque, vibration, and tension in real-time, significantly reducing assembly errors and enabling predictive maintenance in vehicle production facilities. In 2024, several Tier 1 suppliers initiated pilot programs using IoT-enabled fasteners to enhance traceability in assembly lines while ensuring compliance with tight OEM tolerances. This trend is opening opportunities for fastener manufacturers to expand their product portfolios with sensor-integrated solutions, catering to the need for enhanced operational efficiency within automated automotive manufacturing environments.

Complex and evolving regulatory compliance requirements related to environmental sustainability and safety standards pose challenges within the Automotive Fasteners Market. Regions like Europe and North America have imposed stricter directives on the use of hazardous substances and the recyclability of automotive components, requiring fastener manufacturers to reformulate coatings and material compositions to remain compliant. Additionally, achieving consistent compliance across varying regional standards while maintaining production efficiency and product performance creates operational complexity for global manufacturers. The need to invest in testing, certification, and advanced material research to align with regulatory expectations increases operational costs and impacts time-to-market, posing a significant challenge for the Automotive Fasteners Market as it adapts to stricter sustainability frameworks.

• Integration of Lightweight Materials: Automotive manufacturers are increasingly adopting lightweight aluminum and advanced composite fasteners to reduce vehicle weight and improve fuel efficiency. In 2024, the deployment of aluminum fasteners grew notably in electric vehicle battery housing and body-in-white applications due to their favorable strength-to-weight ratio. These lightweight fasteners help reduce vehicle mass by up to 10%, enhancing range and energy efficiency in electric and hybrid vehicles while maintaining structural integrity in high-stress zones.

• Expansion of Smart Fastening Technologies: The Automotive Fasteners market is witnessing the deployment of sensor-embedded fasteners that can measure tension, vibration, and torque in real-time on assembly lines. In several European automotive manufacturing plants, these intelligent fasteners have reduced assembly error rates by 30% while providing predictive maintenance data, helping OEMs maintain strict quality standards. This trend is fueling demand for smart fastening solutions across premium vehicle manufacturers integrating advanced driver assistance and electrified systems.

• Shift Toward Corrosion-Resistant Coatings: The demand for automotive fasteners with advanced anti-corrosion coatings has grown, particularly for applications in EV battery systems and underbody assemblies exposed to harsh environments. Zinc-aluminum and ceramic-based coatings now dominate critical areas, with testing in 2024 showing a 25% improvement in salt spray resistance over traditional coatings. This trend aligns with OEM sustainability objectives and extends vehicle lifecycle performance in diverse climate conditions.

• Adoption of Modular Vehicle Platforms: The increasing use of modular platforms in vehicle manufacturing is influencing the Automotive Fasteners market, requiring high-consistency fasteners for standardized interfaces across multiple vehicle models. Global OEMs adopting modular EV platforms are now prioritizing fasteners that enable quick assembly while ensuring vibration resistance and torque accuracy, reducing production time by up to 15% during assembly while maintaining flexibility in variant production.

The Automotive Fasteners market segmentation is structured across types, applications, and end-user categories, each reflecting unique demand drivers and technological integrations shaping the market’s direction. In terms of types, the market covers threaded, non-threaded, clips, and specialty fasteners used across various automotive components. Application-wise, automotive fasteners are utilized in engine assemblies, chassis, transmission systems, and body-in-white sections, with demand patterns shifting in response to the rise of electric vehicles and advanced safety systems. End-user segmentation primarily includes OEMs and aftermarket service providers, with OEMs dominating consumption due to consistent, large-scale demand for high-quality, precision-engineered fasteners supporting global vehicle production. This structured segmentation helps stakeholders identify high-potential segments within the Automotive Fasteners market while aligning strategies with emerging technological and regional consumption trends.

Threaded fasteners remain the leading type within the Automotive Fasteners market, driven by their essential role in engine assembly, suspension systems, and critical load-bearing areas requiring high-torque retention and vibration resistance. In 2024, threaded fasteners saw a notable increase in deployment across EV platforms for battery enclosure assemblies due to their proven mechanical strength. Non-threaded fasteners are experiencing the fastest growth, driven by demand for lightweight solutions in interior and exterior trim applications where quick installation and disassembly are necessary for modular design strategies. Clips and specialty fasteners, while niche in their contributions, are integral for wiring harness management and lightweight panel assemblies in modern vehicles, especially in electric vehicles where space and weight are critical. These fastener types collectively align with evolving vehicle designs, including modular and lightweight structures, underscoring the importance of precision and adaptability within the Automotive Fasteners market.

Engine assembly remains the leading application for fasteners within the Automotive Fasteners market, as precision fastening ensures engine durability and operational safety in high-temperature and high-vibration conditions. In 2024, the market noted a significant rise in demand for corrosion-resistant and high-tensile fasteners within engine compartments due to the integration of hybrid powertrains requiring reliable component securing. Chassis and body-in-white applications are emerging as the fastest-growing areas for fasteners, driven by the adoption of modular vehicle platforms and increasing production of electric vehicles requiring lightweight yet durable fastening solutions for structural integrity. Transmission system applications continue to hold relevance, as precision fasteners are critical in maintaining performance efficiency, while interior trim and electronics assembly applications are steadily growing due to advanced driver assistance and infotainment system integration in modern vehicles, collectively influencing demand within the Automotive Fasteners market.

OEMs remain the dominant end-users in the Automotive Fasteners market, attributed to their direct involvement in large-scale vehicle production requiring consistent, high-quality fasteners to support various vehicle segments, including conventional, hybrid, and electric platforms. OEMs are increasingly prioritizing fasteners with advanced coatings and sensor-enabled features to meet modern assembly line requirements and enhance production efficiency. The aftermarket segment is the fastest-growing end-user, driven by increasing vehicle parc globally, with consistent demand for replacement fasteners to support maintenance, repair, and customization needs across aging vehicle fleets. Specialty vehicle manufacturers, including electric vehicle startups and off-highway vehicle producers, also contribute to the Automotive Fasteners market by adopting specialized fasteners for niche applications requiring high performance, corrosion resistance, and lightweight attributes, shaping demand patterns and technological adoption within the market landscape.

Asia-Pacific accounted for the largest market share at 42.3% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 3.2% between 2025 and 2032.

Asia-Pacific continues to lead the Automotive Fasteners Market, driven by high automotive production volumes in China, Japan, and India, coupled with a well-established component supply chain supporting fastener manufacturing at scale. The region benefits from increasing domestic consumption of vehicles, a rising shift toward electric vehicles, and expanding investments in lightweight fasteners across new assembly lines. Meanwhile, North America’s expected rapid growth is supported by the surge in EV manufacturing initiatives, advanced manufacturing infrastructure, and rising adoption of precision-engineered fasteners aligned with modular vehicle production trends. Regulatory shifts toward sustainable manufacturing, coupled with advanced R&D clusters, are also reinforcing the growth momentum in the Automotive Fasteners Market across these key regions.

Emerging Lightweight Innovations Drive Fastener Adoption in Vehicle Assembly

The Automotive Fasteners Market in this region accounted for 21.5% of the global market volume in 2024, with demand driven by the passenger and commercial vehicle manufacturing industries, which are shifting toward lightweight assembly practices. Sectors including EV manufacturing, off-highway vehicles, and advanced automotive component suppliers are central to the growing adoption of high-tensile and lightweight fasteners. The implementation of the United States-Mexico-Canada Agreement (USMCA) is supporting supply chain resilience, while government incentives for local manufacturing and electrification are creating a favorable demand environment. Technological advancements, including AI-based quality inspection systems and the adoption of smart fastening solutions in automated assembly lines, are transforming operational efficiencies for manufacturers in the Automotive Fasteners Market, aligning with regulatory frameworks focused on safety and sustainability across the vehicle assembly landscape.

Advanced Sustainability Directives Fuel Demand for High-Performance Fasteners

The Automotive Fasteners Market in this region held a 26.8% volume-based share globally in 2024, with Germany, France, and the UK representing the leading consumer markets due to their robust automotive production ecosystems. The European Union’s Green Deal and stringent emissions reduction frameworks are encouraging the adoption of lightweight and recyclable fasteners, aligning with OEM sustainability objectives. Regulatory bodies are actively promoting circular economy practices within automotive manufacturing, influencing fastener material selection and coating technologies. Technological adoption, including sensor-enabled and corrosion-resistant fasteners, is rising across premium automotive segments and electric vehicle platforms in the region, enabling manufacturers in the Automotive Fasteners Market to maintain quality standards while meeting new efficiency and sustainability benchmarks set by evolving European directives.

Surge in EV and Automotive Manufacturing Expands Regional Fastener Demand

This region leads the Automotive Fasteners Market with the highest consumption volume, driven by China, India, and Japan as the top-consuming countries supporting high vehicle production and rapid electrification initiatives. The region is witnessing increased deployment of lightweight and high-tensile fasteners across electric and hybrid vehicle assembly lines as manufacturers aim to reduce vehicle weight while ensuring structural integrity. Infrastructure development and expansion of automotive clusters are enabling large-scale fastener production aligned with local demand. Technological innovation hubs in China and Japan are fostering advancements in smart fastening systems and AI-integrated quality inspection, positioning the Automotive Fasteners Market in this region to support rapid scaling while meeting global standards in performance, safety, and environmental compliance.

Vehicle Production Recovery and Trade Policies Drive Component Demand

The Automotive Fasteners Market in this region is showing a steady demand led by Brazil and Argentina, where local automotive production and aftermarket service sectors are key drivers of fastener consumption. The region accounted for approximately 5.7% of global volume in 2024, with growing investment in vehicle assembly infrastructure and localized supply chain development supporting demand for precision-engineered fasteners. Government incentives, such as tax benefits for component manufacturers and local assembly, are further boosting market activity. Trends in the infrastructure and energy sectors, including investments in transportation and logistics, are indirectly supporting vehicle demand, which in turn strengthens the Automotive Fasteners Market in the region while aligning with emission control and safety regulations.

Infrastructure Expansion and EV Pilots Drive Fastener Market Momentum

The Automotive Fasteners Market in this region is driven by rising demand across the construction, logistics, and oil & gas sectors, influencing vehicle fleet expansion and maintenance needs. Countries like the UAE and South Africa are leading regional consumption with the integration of advanced vehicle technologies and local assembly initiatives. Local regulations encouraging sustainable vehicle adoption and trade partnerships with global OEMs are creating opportunities for fastener manufacturers. Technological modernization, including the introduction of AI-enabled quality checks in fastener production and the gradual adoption of lightweight fasteners for fleet vehicles, is supporting quality and operational efficiency improvements. The Automotive Fasteners Market in this region is positioned to benefit from ongoing economic diversification and investment in mobility infrastructure.

China: 28.1% market share

High automotive production capacity with an established supply chain for both ICE and EV manufacturing drives China's dominance in the Automotive Fasteners Market.

Germany: 13.6% market share

Strong end-user demand from premium vehicle manufacturing and advanced engineering practices ensures Germany’s leadership in the Automotive Fasteners Market.

The Automotive Fasteners market is characterized by a competitive environment with over 150 active global and regional manufacturers providing a diverse range of threaded, non-threaded, specialty, and smart fasteners to OEMs and aftermarket suppliers. Market participants focus on strategic initiatives, including product innovations such as sensor-embedded fasteners for torque monitoring and advanced anti-corrosion coatings to enhance performance across diverse automotive applications. Companies are expanding production capacities in Asia-Pacific and North America to align with the rising demand for lightweight and high-tensile fasteners within EV and hybrid vehicle manufacturing. Mergers and partnerships with local component suppliers and OEMs are common strategies aimed at strengthening market positioning while ensuring resilient supply chains. Innovation trends, including the integration of AI-enabled inspection technologies, automation in production lines, and advancements in material science, are influencing competition, pushing manufacturers to maintain quality standards while reducing operational costs. These competitive dynamics are shaping the Automotive Fasteners market as companies align with evolving customer requirements and sustainability goals across global automotive manufacturing ecosystems.

Illinois Tool Works Inc. (ITW)

LISI Group

Bulten AB

Stanley Black & Decker Inc.

Nifco Inc.

Penn Engineering

Sundram Fasteners Limited

Shanghai Prime Machinery Company Limited

Kamax Holding GmbH & Co. KG

SFS Group AG

Technological advancements are reshaping the Automotive Fasteners Market by enhancing production efficiency, product reliability, and sustainability in vehicle assembly. Cold and hot forging remain core manufacturing methods, but manufacturers are adopting precision forging and multi-station cold heading machines to achieve tighter tolerances and consistent quality in high-volume production. Smart fastener technologies incorporating embedded sensors enable real-time monitoring of torque, tension, and vibration during vehicle assembly, improving quality control and enabling predictive maintenance for manufacturers. AI-enabled automated inspection systems are reducing defect rates in fastener production by up to 45%, while advanced robotics are being integrated into sorting and packaging lines for higher operational efficiency.

Material innovations include the adoption of high-tensile steel, aluminum alloys, and composite materials for lightweight fasteners that reduce vehicle weight while maintaining strength, particularly important for electric and hybrid vehicle platforms. Anti-corrosion coating technologies, including zinc-aluminum flake coatings and eco-friendly ceramic coatings, are enhancing fastener lifespan in harsh environments, ensuring performance stability in chassis, engine, and underbody applications. Digital twin technology is emerging within the Automotive Fasteners Market to simulate load and stress factors on fasteners during vehicle operation, aiding in optimizing designs for safety and longevity. These technology trends are aligned with the industry’s focus on lightweight, high-performance, and sustainable solutions in automotive manufacturing.

• In March 2023, Stanley Engineered Fastening launched a new range of lightweight aluminum fasteners designed specifically for electric vehicle battery assemblies, reducing the component weight by up to 12% while maintaining high tensile strength for enhanced structural safety.

• In September 2023, Nifco Inc. expanded its production facility in Mexico to increase the output of precision-engineered plastic fasteners for the North American market, adding 40% more production capacity to meet growing EV and hybrid vehicle manufacturing demands.

• In February 2024, Bulten AB introduced a sensor-enabled fastener system capable of monitoring torque and vibration in real-time during vehicle assembly, helping OEMs reduce assembly errors by 30% and ensuring compliance with tightening specifications.

• In May 2024, LISI Group developed a corrosion-resistant coating for high-tensile steel fasteners, increasing salt spray resistance by 25% over previous coatings, aiming to support the durability of fasteners used in underbody and chassis components in harsh environmental conditions.

The Automotive Fasteners Market Report comprehensively covers the production, consumption, and technological trends influencing the global fasteners landscape across automotive manufacturing. It analyzes threaded, non-threaded, specialty, and smart fasteners used in critical automotive systems, including engine, chassis, transmission, and body-in-white applications. The report includes insights into lightweight and high-tensile material adoption, advanced coating technologies, and the integration of sensor-based fasteners supporting the transition to smart manufacturing environments.

Geographically, the report examines key markets including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, detailing unique demand patterns across China, Japan, Germany, the United States, and Brazil. It addresses the rising demand for fasteners in electric and hybrid vehicle production while exploring the impacts of modular vehicle platforms on fastener design and adoption.

The Automotive Fasteners Market Report also evaluates the role of digital transformation, AI-enabled quality control, and automation in fastener manufacturing, assessing their influence on production efficiency and product quality. Additionally, it covers sustainability trends, such as eco-friendly coatings and recyclable materials, and includes analysis of the aftermarket segment for maintenance and repair demands. This structured scope ensures decision-makers and industry professionals gain actionable insights into emerging opportunities, supply chain shifts, and innovation priorities within the global Automotive Fasteners Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 23772.42 Million |

|

Market Revenue in 2032 |

USD 29191.22 Million |

|

CAGR (2025 - 2032) |

2.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Illinois Tool Works Inc. (ITW), LISI Group, Bulten AB, Stanley Black & Decker Inc., Nifco Inc., Penn Engineering, Sundram Fasteners Limited, Shanghai Prime Machinery Company Limited, Kamax Holding GmbH & Co. KG, SFS Group AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |