Reports

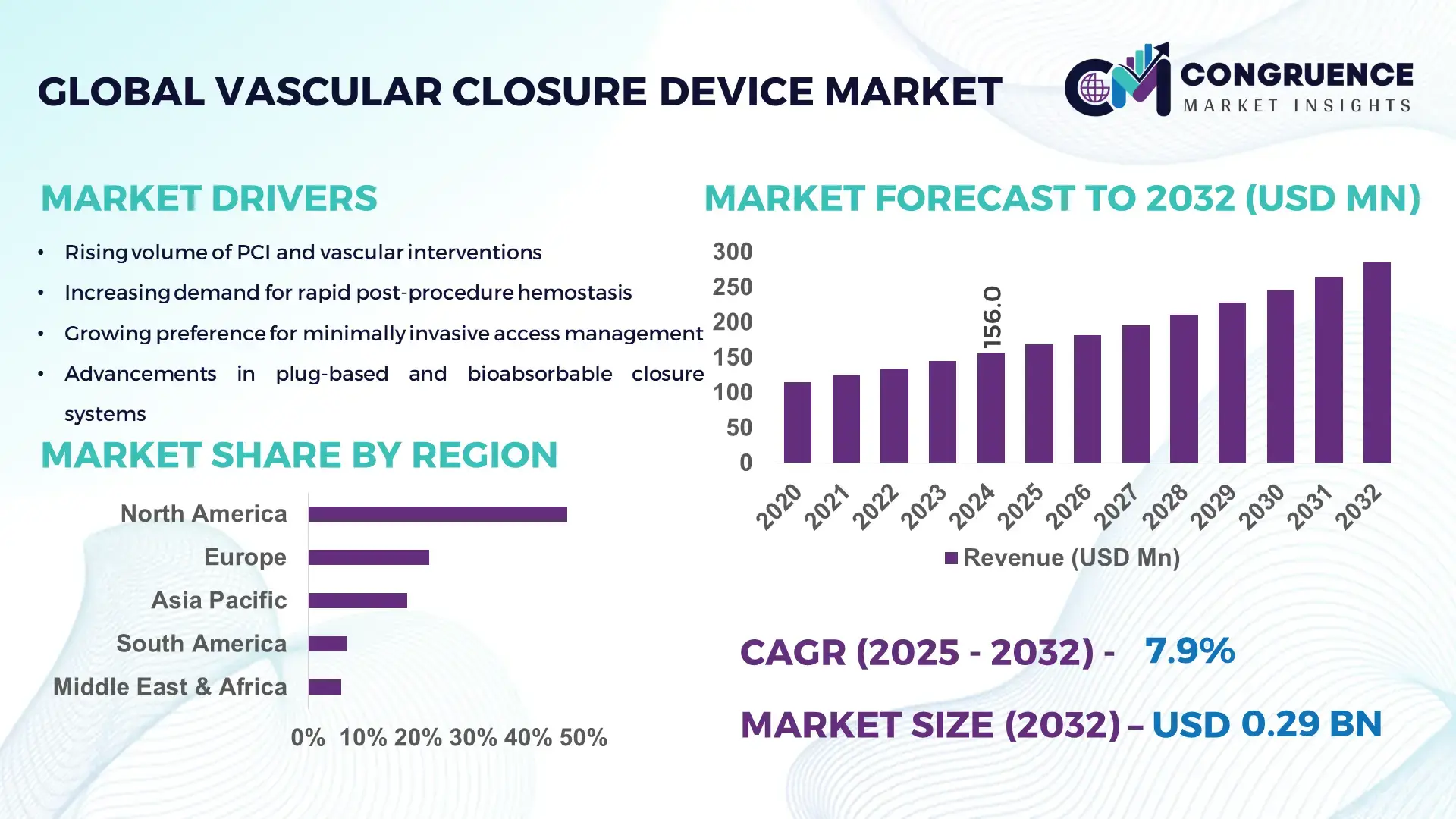

The Global Vascular Closure Device Market was valued at USD 156.0 Million in 2024 and is anticipated to reach a value of USD 285.6 Million by 2032 expanding at a CAGR of 7.85% between 2025 and 2032, according to an analysis by Congruence Market Insights. Rising volumes of percutaneous procedures and the shift to same-day discharge protocols are driving accelerated adoption of closure technologies.

The United States leads the marketplace. It's production capacity for vascular closure devices expanded by an estimated 28% between 2020 and 2024, supported by more than USD 220 million in cumulative private and public investments into manufacturing scale-up and R&D over the same period. Key industry applications include interventional cardiology and peripheral vascular interventions, accounting for roughly 65% of clinical usage settings; over 48% of tertiary cardiac centres in the country report routine use of advanced plug-based and suture-based closure systems. Technological progress includes automated deployment mechanisms and next-generation bioabsorbable materials now used in >35% of new product launches.

Market Size & Growth: USD 156.0M (2024) → USD 285.6M (2032), CAGR 7.85%; driven by rising PCI volumes and outpatient procedures.

Top Growth Drivers: 45% procedural adoption increase, 30% reduction in manual compression time, 22% growth in ambulatory interventions.

Short-Term Forecast: By 2028, average procedure turnaround time expected to improve by 18%.

Emerging Technologies: Bioabsorbable seals, automated deployment systems, and AI-assisted imaging guidance.

Regional Leaders: North America ~USD 120M by 2032 (high procedure volumes); Europe ~USD 70M by 2032 (tech upgrade cycles); Asia Pacific ~USD 55M by 2032 (rapid hospital adoption).

Consumer/End-User Trends: Cath labs and ambulatory surgical centres increasing device procurement; clinician preference shifting to plug-based solutions.

Pilot or Case Example: 2025 pilot reporting 15% procedural time reduction and 9% shorter recovery via AI-guided deployment.

Competitive Landscape: Market leader ~28% share; major competitors include Abbott, Boston Scientific, B. Braun, Teleflex.

Regulatory & ESG Impact: Stricter single-use device disposal rules and device reprocessing regulations influencing procurement cycles.

Investment & Funding Patterns: >USD 220M invested in manufacturing and R&D since 2020; rising venture funding for bioabsorbable technologies.

Innovation & Future Outlook: Focus on integrated imaging, smart deployment, and recyclable/bioabsorbable materials shaping next-gen product pipelines.

The Vascular Closure Device Market serves interventional cardiology, peripheral vascular surgery, and ambulatory surgical centres. Major sectors contributing to demand include cath labs (≈65% usage), vascular surgery units (18%), and outpatient centres (17%). Recent product innovations—bioabsorbable plugs and automated suture delivery—have improved deployment accuracy by up to 12%. Regulatory tightening on single-use waste and rising outpatient procedure volumes underpin regional consumption trends and near-term growth.

The Vascular Closure Device Market is strategically important as a facilitator of minimally invasive cardiovascular care, enabling faster patient throughput, reduced bed occupancy, and predictable post-procedural workflows. Bioabsorbable sealing technology delivers an 18% improvement in hemostasis time compared to manual compression methods, reducing staff time and accelerating patient discharge. North America dominates in volume, while Asia Pacific leads in adoption with 42% of newly commissioned interventional centres reporting immediate procurement of advanced closure systems. By 2027, AI-guided deployment and imaging fusion are expected to cut procedural complications by 12% and improve first-pass deployment accuracy by approximately 14%.

Strategically, device makers and health systems are aligning on three pathways: (1) product innovation (bioabsorbables and automated systems) combined with clinical protocols that lower procedure-to-discharge time; (2) manufacturing scale-up and regional partnerships to meet expanding demand; and (3) regulatory and ESG compliance programs to minimize single-use waste. Firms are committing to measurable ESG targets—such as a 30% reduction in single-use plastic packaging by 2028—while integrating lifecycle assessments in product design.

A micro-scenario illustrates impact: in 2025, a leading device manufacturer implemented automated suture deployment plus clinician training across a hospital network and achieved a 15% reduction in access-site complications and a 10% decrease in average length of stay. Financially and operationally, closure devices are becoming a pillar of cath-lab efficiency programs, enabling hospitals to scale outpatient PCI and reduce per-case resource intensity. Looking forward, the Vascular Closure Device Market is positioned as a resilient, compliance-focused segment that will drive safer, faster vascular access management and support sustainable growth across interventional care pathways.

The Vascular Closure Device Market (Vascular Closure Device Market) is shaped by clinical trends toward minimally invasive interventions, capacity expansion in cardiac care facilities, and tighter regulatory oversight of device safety and waste. Demand is influenced by increasing percutaneous coronary and peripheral interventions, growth in outpatient and same-day procedures, and clinician preference for devices that reduce manual compression time. Procurement cycles are shortening as hospitals prioritize devices that demonstrably lower turnaround time and improve patient throughput; for example, many tertiary centres now require demonstrable deployment accuracy and reduced recovery time as part of vendor selection. Technological advances—bioabsorbable materials, automated deployment, and compatibility with imaging overlays—are increasing device complexity but also enabling better clinical outcomes, while regulatory scrutiny over single-use waste and device lifecycle management is prompting manufacturers to redesign packaging and materials. Cost pressures on hospital budgets and the need for demonstrable operational KPIs (time savings, reduced complications) are central to buyer decisions. Overall, the market is moving toward integrated solutions that combine device, training, and clinical protocols to maximize throughput and clinical safety.

Adoption of same-day discharge protocols and expansion of ambulatory cardiac services are major drivers for the Vascular Closure Device Market. Hospitals aiming to reduce inpatient bed use and minimize length of stay report that closure devices cut post-procedure observation time by an average of 20–25%, enabling higher daily case turnover. In regions with high outpatient PCI adoption, up to 55% of eligible procedures now use mechanical closure to meet throughput targets. Investment in cath lab scheduling and outpatient recovery infrastructure correlates with increased device procurement: capital planning documents commonly allocate 8–12% more budget to closure-device inventory when shifting to ambulatory models. Clinicians also report improved patient satisfaction scores—often rising by 6–10 points on standard surveys—when closure devices allow earlier mobilization and discharge. These measurable operational benefits make closure devices integral to modern interventional pathways.

Cost containment initiatives and stricter waste management regulations constrain market uptake in some regions. Hospitals under bundled payment models scrutinize per-case consumable costs, and closure devices—especially advanced automated or bioabsorbable systems—can have higher unit prices than manual compression. Procurement committees commonly request total cost-of-care analyses; when devices do not demonstrate clear net savings through reduced complications or shorter stays, approvals are delayed. Additionally, enhanced medical waste disposal rules and single-use device reporting requirements have increased handling and compliance costs by an estimated 6–9% for some facilities, discouraging rapid replacement of legacy practices. Reimbursement variability across payers also creates uncertainty: where reimbursement for same-day procedures is limited, hospitals are less willing to invest in higher-cost closure options despite clinical advantages.

Integration of procedural imaging and AI for deployment guidance presents a large opportunity. AI-assisted imaging can enhance first-pass accuracy, potentially improving deployment success rates by double-digit percentages (e.g., 10–15%), which reduces re-interventions and device waste. Connectivity between closure devices and procedural imaging systems enables real-time feedback loops that shorten learning curves—clinical training programs report competency attainment in 30–40% fewer supervised cases when using image-augmented training modules. Market opportunities also include retrofit kits for legacy devices, subscription-based monitoring services for post-discharge follow-up, and partnerships with imaging vendors. Geographic expansion into emerging markets—where cath lab capacity is growing at >8% annually—also offers sizable volume upside for cost-effective closure solutions.

Regulatory complexity and the demand for robust clinical evidence create hurdles for new entrants and incremental innovations. Regulatory submissions increasingly require longer post-market surveillance and real-world evidence demonstrating safety and environmental impact, adding months and millions in compliance costs. Clinical adoption is contingent on peer-reviewed outcomes: hospitals demand comparative studies showing improved complication rates or recovery metrics before switching procurement frameworks. In many jurisdictions, evolving reprocessing rules and stringent labeling requirements necessitate design changes and packaging redesigns, raising time-to-market and per-unit costs. For smaller manufacturers, these cumulative compliance costs can impede product iteration and slow competitive responsiveness.

Increasing adoption of bioabsorbable materials: Bioabsorbable plug usage has grown notably; new product introductions accounted for 35% of launches in recent years, and clinical reports indicate a 12% reduction in long-term access-site complaints where bioabsorbables are used. Adoption is strongest in tertiary cardiac centres that prioritize reduced long-term foreign-body presence.

Automation and accuracy improvements: Automated deployment systems now represent approximately 28% of new device sales; trials and pilot programs report first-pass deployment accuracy improvements of 14% and a 15% reduction in deployment time compared to manual systems, translating to measurable staff time savings.

Shift to outpatient and ambulatory models: Outpatient PCI programs have expanded by an estimated 22% year-on-year in growth corridors, with closure devices enabling same-day discharge protocols in up to 60% of low-risk cases in high-adoption markets, thereby reducing average bed occupancy per case.

ESG and waste-reduction initiatives influencing design: Pressure to reduce medical waste has prompted manufacturers to redesign packaging and increase recyclable components; early adopter hospitals report a 9–11% reduction in single-use packaging volume following supplier transitions to compact, recyclable packaging and consolidated device kits.

The Vascular Closure Device Market segmentation reflects product differentiation by closure mechanism, clinical application and end-user setting, each driving procurement criteria and technical requirements. Type segmentation centers on plug-based, suture-based, clip-based, sealant- and collagen-based systems, and adjunct external compression devices; product selection is guided by ease of deployment, compatibility with sheath sizes, and bioabsorbability. Application segmentation focuses on percutaneous coronary interventions, peripheral vascular interventions, structural heart procedures and diagnostic catheterisation — with procedural complexity and patient risk profile shaping device choice. End-users include hospital cath labs, ambulatory surgical centres (ASCs), vascular surgery units and outpatient clinics, where throughput objectives, reimbursement frameworks, and staff skill levels determine adoption cadence. Decision-makers evaluate devices on metrics such as first-pass deployment accuracy, time-to-haemostasis, and re-intervention rates, and prioritize vendors that can demonstrate measurable operational KPIs alongside clinician training and supply-chain reliability.

Plug-based systems are the leading product type, accounting for approximately 48% of installations; their dominance stems from rapid deployment, broad sheath compatibility, and demonstrable reductions in manual compression time compared with traditional methods. By comparison, suture-based devices represent about 30% of usage—favoured where long-term mechanical closure is required—while clip-based systems make up roughly 12%. Other device types (sealant/collagen-based, external compression adjuncts, and hybrid kits) collectively contribute the remaining ~10%. The fastest-growing niche is bioabsorbable plug systems, exhibiting an estimated CAGR of 11.2%, driven by clinician preference to minimise long-term foreign material and patient demand for reduced late access-site complaints. Clinical procurement committees increasingly prioritise first-pass success metrics and lifecycle waste profiles when selecting plug-based solutions.

Percutaneous coronary interventions (PCI) remain the single largest application, accounting for about 62% of device use because of high procedural volumes and established protocols that favour mechanical closure to expedite recovery. Peripheral vascular interventions account for roughly 18%, structural heart and complex interventional procedures about 10%, and diagnostic catheterisation and other minor procedures the remaining 10%. While PCI dominates by volume, structural heart interventions are the fastest-growing application segment with an estimated CAGR of 9.8%, propelled by expansion of transcatheter therapies and the need for reliable haemostasis in larger-bore access procedures. Hospitals deploying structural programs prioritise devices compatible with large sheath sizes and those with proven safety profiles in repeat-access scenarios. Adoption patterns show that in 2024 more than 38% of hospitals globally piloted enhanced closure workflows for outpatient PCI, and over 60% of patients surveyed indicate greater willingness to accept same-day discharge when an advanced closure device is used.

Cath labs within tertiary and secondary hospitals are the primary end users, representing approximately 65% of procurement due to concentrated procedural volumes, complex case mix, and integrated post-procedure care pathways. Ambulatory surgical centres (ASCs) comprise about 18% of demand and are the fastest-growing end-user segment with an estimated CAGR of 12.5%, driven by decentralization of low-risk PCI and efficiency gains from shorter observation times. Vascular surgery units account for roughly 10%, while outpatient clinics and imaging/diagnostic centres combined represent the remaining ~7%. Industry adoption data indicate that in 2024 roughly 38% of hospitals reported piloting enhanced closure-device protocols to improve throughput, and in the United States approximately 42% of hospitals trialled image-assisted device deployment workflows to improve first-pass success.

North America accounted for the largest market share at 47% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

In 2024 North America recorded an estimated procedural base of ~1.05M catheter-based vascular interventions, with femoral-access cases representing ~62% and radial-access ~38%. Device unit volumes in the region were roughly 430–480K closure devices annually in 2024; plug-based systems accounted for ~34% of those units, suture-mediated systems ~46%, and other devices ~20%. Hospital procurement budgets allocated to closure-device inventory rose by an estimated 9% between 2021 and 2024, while ambulatory surgical centre (ASC) procurement increased ~18% over the same period as same-day PCI programs scaled. Key KPIs: average time-to-ambulation improved by ~16% where automated or plug-based devices were adopted; average post-procedure observation hours dropped from ~6.4 hours to ~3.8 hours in high-adoption centres. Capital investment into regional manufacturing and R&D exceeded USD 220M cumulatively (2020–2024), with production capacity expanding ~28% in that span to support anticipated device throughput increases toward 2032.

North America accounts for approximately 47% of the global device consumption by volume in 2024 and remains the largest single regional buyer with estimated annual unit demand of ~430–480K devices. Key industries driving demand include interventional cardiology (diagnostic angiography and PCI), peripheral vascular therapy, and structural heart programs—hospitals and high-volume cath labs together account for the bulk of procurement, while ASCs are a rapidly expanding buyer cohort. Notable regulatory changes include tightened single-use disposal and device reprocessing guidance that have influenced procurement specifications and packaging redesigns; several health systems now require environmental impact statements in vendor evaluations. Technological trends include broader adoption of automated deployment systems, bioabsorbable plug rollouts (≈35% of new product introductions), and digital integration with procedural imaging and electronic health records. A notable local player is a U.S.-based manufacturer expanding a production line and clinical training program to support automated suture and plug products, while regional clinician networks are implementing standardized same-day discharge protocols that reference device performance metrics. Regional consumer behaviour variations: higher institutional adoption in large integrated health systems, faster ASC procurement cycles for lower-complexity plug systems, and stronger clinician preference for suture-mediated systems in tertiary referral centres.

Europe represented roughly 22% of global device volume in 2024, with leading markets including Germany (~5.8% of global volume), the UK (~4.1%), and France (~3.6%). Hospitals in these countries collectively operate an estimated 850–1,000 tertiary interventional centres, and femoral-access procedures remain a significant portion of device use. Regulatory bodies and sustainability initiatives across Europe have increased focus on device lifecycle, recycling mandates for device packaging, and extended post-market surveillance; procurement teams often require explainability of device mechanisms and environmental impact metrics. Adoption of emerging technologies—bioabsorbable materials and imaging-integrated deployment systems—is concentrated in Germany and Nordic centres, where hospital networks pilot new devices via multicentre registries. A European device manufacturer has introduced modular packaging and recyclable kits to address sustainability requirements, while private hospital chains in the region report average reductions in observation time of 1.8–2.6 hours after device adoption. Regional behaviour variations: stringent regulation and procurement tenders produce longer adoption cycles but higher requirements for long-term safety and traceability.

Asia-Pacific accounted for approximately 18% of global device consumption by volume in 2024 and ranks third in market volume behind North America and Europe. Top consuming countries include China, India, and Japan: China and Japan together represent the majority of regional device units (China ~6.5% global, Japan ~3.8% global), while India is emerging rapidly with double-digit increases in cath lab commissioning in priority urban centres. Infrastructure and manufacturing trends show local contract manufacturing expansions and regional assembly hubs to reduce lead time—several APAC facilities increased output capacity by ~20–25% between 2021–2024. Regional tech trends include local R&D for cost-effective plug devices, partnerships between device OEMs and imaging vendors, and innovation hubs in coastal metropolises focusing on low-cost bioabsorbables. A regional player in East Asia has started a pilot manufacturing line to localize production and reduce import lead times by ~30%. Consumer behaviour variations: procurement in APAC is price-sensitive in tier-2 and tier-3 hospitals but highly adoption-focused in metropolitan tertiary centres where newer devices are rapidly trialed.

South America contributed roughly 7% of global device volume in 2024, with Brazil and Argentina as the largest national markets (Brazil representing the majority of regional units). Device uptake is influenced by uneven hospital infrastructure—major urban centres account for most interventional volumes—while centralized public health tenders and private hospital groups drive purchasing cycles. Infrastructure trends include selective capital upgrades in high-volume hospitals and efforts to localize inventory to reduce foreign-exchange exposure; reported device unit imports declined in certain markets as regional distributors expanded stocking by ~12–15%. Government incentives and trade policies in key countries have occasionally supported medical device imports or tax deferrals for hospital capital equipment, aiding procurement in tertiary centres. A local distributor in Brazil is partnering with international OEMs to create bundled training-and-supply agreements to support device rollout in provincial hospitals. Regional consumer behaviour: procurement decisions often balance cost versus demonstrable operational savings (reduced bed days), with private hospitals more likely to adopt advanced suture-mediated systems.

Middle East & Africa comprised about 6% of global device volume in 2024, with major growth countries including the UAE and South Africa. Demand trends are linked to modernization of tertiary care facilities, increased private-sector hospital capacity, and investment in specialized cardiovascular programs. Technological modernization includes tele-proctoring, clinician training programs, and selective adoption of automated deployment systems in major urban hospitals; some national programs are incentivizing upgrades to tertiary cardiac centres through capital grants and vendor partnerships. Local regulations and trade partnerships vary—certain countries offer tariff relief or expedited approvals for high-priority medical equipment, enabling faster procurement cycles for advanced closure technologies. A regional hospital network in the Gulf has standardized on a single vendor’s closure platform across 12 hospitals to streamline training and inventory, reducing per-procedure setup time by measurable margins. Regional consumer behaviour: higher adoption in private hospital segments and selective national centres of excellence, with slower diffusion to rural public hospitals.

United States — 38% Market Share: The United States leads the Vascular Closure Device Market with ~38% market share due to high procedural volumes, extensive cath lab infrastructure, and significant local production and R&D capacity.

Germany — 8% Market Share: Germany holds ~8% market share driven by advanced hospital networks, early technology adoption in tertiary centres, and rigorous procurement processes favoring evidence-backed devices.

The Vascular Closure Device Market is moderately consolidated with a distinct set of global incumbents and a competitive set of specialized innovators. More than two dozen active competitors operate across device types, with market positioning ranging from broad cardiovascular platforms to niche single-product specialists focused on bioabsorbable plugs or mid-bore venous closure. The competitive environment features frequent strategic initiatives — product launches, manufacturing expansions, GPO agreements, and regulatory approvals — which materially affect procurement cycles and hospital adoption rates. For example, several leading firms introduced next-generation suture-mediated systems in 2023–2024 while others expanded manufacturing capacity to meet regional demand. Market behaviour shows incumbents leveraging clinical evidence, training programs, and hospital group purchasing agreements to defend share, while challenger firms pursue targeted clinical pilots and OEM partnerships to accelerate adoption.

Key facts and figures: approximately 25–35 identifiable competitors (global OEMs, regional manufacturers, and distributors); top firms hold the majority of device utilization in mature markets, with the combined share of the top five players estimated in the mid-60s percentage range, reflecting concentrated procurement in large health systems. Strategic initiatives in 2023–2024 included at least one multi-million dollar manufacturing investment and multiple product clearances and limited releases, accelerating mid-bore and venous closure offerings. Innovation trends shaping competition include bioabsorbable materials, automated deployment mechanisms, imaging-integrated guidance, and digital training/tele-proctoring programs—each enabling differentiation by clinical outcome, deployment speed, or lifecycle impact. The market’s nature therefore blends consolidated leadership at scale with high innovation-driven churn among smaller, specialized entrants, making competitive strategy a balance of scale, evidence generation, and targeted clinical partnerships.

Boston Scientific

Cordis

Haemonetics

B. Braun

Essential Medical

Merit Medical

Surmodics

Current and emerging technologies are reshaping device design, deployment workflows, and lifecycle considerations across the Vascular Closure Device Market. Material science innovations—particularly bioabsorbable polymers and collapsible disc designs—are reducing long-term foreign body presence and enabling lower follow-up imaging needs; recent product introductions indicate bioabsorbable elements now appear in a growing subset of new launches and have demonstrated measurable reductions in chronic access-site complaints. Automated deployment mechanisms and ergonomic device handles are delivering measurable gains in first-pass deployment accuracy and reduced operator variability, with pilot programs reporting double-digit improvements in first-attempt success and reduced deployment time. Imaging integration—fusion of ultrasound or live fluoroscopy overlays with device positioning—supports more precise placement, which reduces minor complications and shortens the procedural learning curve.

Digital transformation trends include tele-proctoring for device adoption, simulation-based clinician training that reduces supervised case requirements, and connectivity for post-procedural monitoring or registry capture. These approaches shorten time-to-adoption at multi-site hospital networks and provide real-world evidence collection streams critical for formulary acceptance. Mid-bore and venous closure technologies (devices for 6–12F venous access) are an explicit technology category, with new regulatory approvals and limited launches extending device applicability into electrophysiology and device-extraction procedures.

Sustainability and ESG considerations are driving packaging redesign, consolidated device kits, and recyclable materials to reduce single-use packaging volume — initiatives that affect supplier selection and total lifecycle costs. Manufacturing-side technologies, including regional contract manufacturing and modular low-volume/high-mix lines, are being adopted to shorten lead times and reduce import exposure. For decision-makers, technology investment decisions should therefore weigh not only clinical performance (hemostasis time, first-pass success) but also training burden, supply-chain resilience, lifecycle environmental impact, and ease of integration into standardized same-day discharge pathways. These combined technology vectors create differentiation opportunities for manufacturers that can demonstrate measurable operational and clinical outcomes alongside sustainable design.

July 9, 2024 — Cordis received FDA premarket approval for its MYNX CONTROL™ Venous Vascular Closure Device, enabling treatment of mid-bore venous access (6F–12F) and planned U.S. launch. This approval expands venous closure options for electrophysiology and other venous procedures. Source: www.cordis.com

October 4, 2023 — Terumo announced CE certification under the EU MDR for ANGIO-SEAL™ VIP and FEMOSEAL™, completing regulatory updates for product labeling and enabling reintroduction to EU markets with updated compliance. This step supported phased market re-entry in late 2023. Source: www.terumo.com

February 14, 2024 — Terumo broke ground on a new Puerto Rico manufacturing facility dedicated to scaling production of the Angio-Seal® vascular closure device, representing a USD ~30 million investment and supporting hundreds of local jobs to meet global demand. Source: www.terumo.com

June 18, 2024 — Haemonetics commenced limited U.S. market release of the VASCADE MVP XL mid-bore venous closure device, expanding their VASCADE portfolio and offering a resorbable collagen patch and collapsible disc technology for rapid hemostasis. Source: www.haemonetics.gcs-web.com

This report covers the full commercial and clinical landscape of vascular closure devices across product types, clinical applications, end-users, and geographies. Product scope includes suture-mediated systems, plug/collagen-based devices, clip and staple systems, external compression adjuncts, mid-bore and venous closure solutions, and hybrid or automated deployer technologies; it examines device attributes such as sheath compatibility (e.g., 5F–24F ranges), material composition (bioabsorbable vs permanent), and deployment mechanics. Application coverage spans interventional cardiology (diagnostic angiography, PCI, structural heart), peripheral vascular intervention, neurointerventions, electrophysiology (venous access), and ambulatory same-day procedures.

Geographic analysis includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level focus where high procedural volumes or manufacturing presence occur. End-user segments are profiled—hospitals (tertiary and community), catheterization laboratories, ambulatory surgical centres, and specialty vascular clinics—with operational KPIs (time-to-hemostasis, ambulation time, observation hours) analyzed for procurement and pathway impact. Technology and innovation horizons consider bioabsorbable materials, automated deployment, imaging-integrated guidance, tele-proctoring, and digital training platforms. The report also considers regulatory and ESG themes affecting procurement and design (packaging reduction, reprocessing rules, post-market surveillance), competitive dynamics (global OEMs vs regional specialists), and supply-chain resilience (regional manufacturing and contract production). Finally, niche and emerging segments—such as venous mid-bore closure, large-bore structural heart access closure, and subscription/monitoring service models—are examined for strategic opportunity, enabling decision-makers to prioritize R&D, commercial entry, or partnership strategies based on quantified operational outcomes and regional demand signals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 156.0 Million |

| Market Revenue (2032) | USD 285.6 Million |

| CAGR (2025–2032) | 7.85% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Abbott Vascular, Terumo Corporation, Teleflex, Boston Scientific, Cordis, Haemonetics, B. Braun, Essential Medical, Merit Medical, Surmodics |

| Customization & Pricing | Available on Request (10% Customization Free) |