Reports

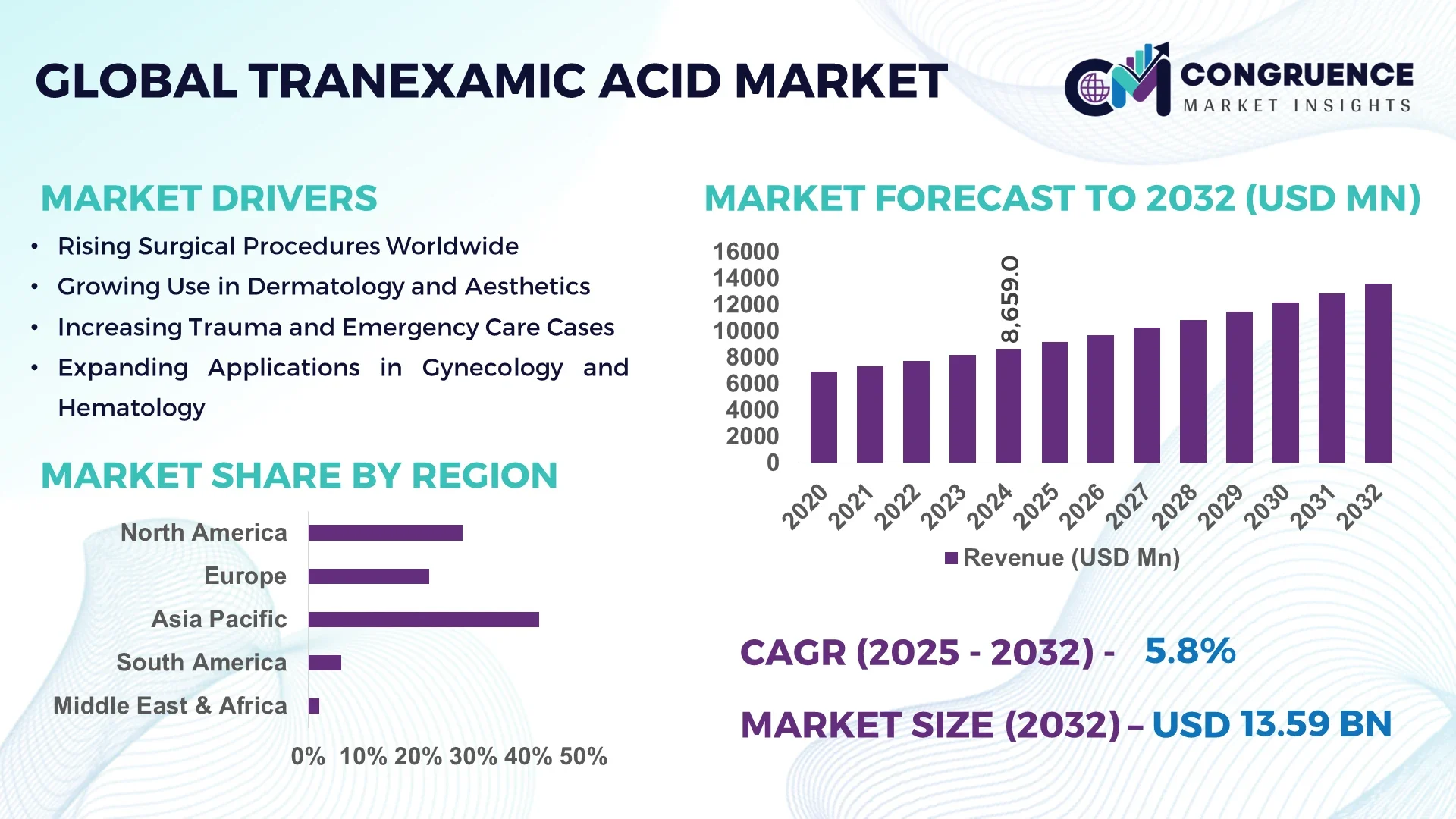

The Global Tranexamic Acid Market was valued at USD 8,659.0 Million in 2024 and is anticipated to reach a value of USD 13,594.2 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032.

Japan has established advanced production capabilities for tranexamic acid, supported by significant investments in pharmaceutical manufacturing facilities, robust research in antifibrinolytic therapies, and integration of high-precision chemical synthesis technologies to serve diverse healthcare and industrial applications.

The Tranexamic Acid Market is characterized by strong adoption across pharmaceuticals, cosmetics, and healthcare sectors. In pharmaceuticals, the compound is extensively used for controlling bleeding disorders and in surgical procedures, with injectable and oral formulations witnessing consistent demand. The cosmetics sector has experienced rapid growth due to its skin-brightening and anti-pigmentation properties, driving investments in dermatological research and formulation technologies. Regulatory frameworks focusing on patient safety and clinical efficacy have shaped product innovation and quality standards globally. Environmental considerations are also impacting the market, with sustainability in chemical synthesis and waste management gaining prominence. Regionally, Asia-Pacific has become a key consumption hub owing to rising healthcare expenditure and cosmetic applications, while North America and Europe maintain steady demand through hospital-based and clinical usage. Emerging trends highlight innovations in drug delivery systems, combination therapies, and AI-driven formulation optimization, indicating strong growth prospects for the industry over the coming years.

Artificial intelligence is significantly transforming the Tranexamic Acid Market by enhancing efficiency across manufacturing, research, and clinical applications. AI-powered predictive analytics are streamlining production workflows, reducing batch variability, and minimizing resource wastage in chemical synthesis. In laboratory environments, machine learning models are accelerating the discovery of advanced formulations, particularly in topical and oral drug delivery systems, by analyzing extensive datasets of chemical interactions and patient responses. In the cosmetics domain, AI is improving product personalization, with algorithms helping to identify optimal concentrations of tranexamic acid in skin care formulations tailored to individual skin profiles.

AI also enables real-time monitoring of quality control in pharmaceutical manufacturing, utilizing computer vision and automated inspection systems to detect impurities or inconsistencies at the molecular level. This has resulted in higher compliance with stringent regulatory frameworks while lowering operational risks. Furthermore, AI-driven simulations are assisting researchers in evaluating safety profiles and potential side effects before initiating clinical trials, thereby accelerating the approval timeline of new products. In logistics and distribution, AI-enabled demand forecasting tools are improving supply chain reliability by predicting shifts in market demand for tranexamic acid formulations across regions. Overall, AI integration is not only improving productivity but also driving precision, safety, and innovation throughout the Tranexamic Acid Market.

"In 2025, a leading pharmaceutical manufacturer integrated AI-based predictive analytics into its tranexamic acid production facilities, achieving a 17% reduction in energy consumption and a 12% improvement in yield consistency through optimized synthesis pathways."

The Tranexamic Acid Market is experiencing significant momentum, driven by expanding applications across pharmaceuticals, cosmetics, and clinical treatments. Growing adoption in surgical procedures and trauma care highlights its importance as a critical antifibrinolytic agent. Rising consumer awareness of skincare solutions has further boosted demand in the cosmetics industry, where tranexamic acid is a preferred active ingredient in pigmentation control formulations. On the supply side, continuous innovation in chemical synthesis methods, alongside stricter regulatory standards, has shaped the competitive landscape. Additionally, regional healthcare expenditure patterns and evolving environmental policies are influencing production strategies, while technological advancements are creating new opportunities for efficiency and product innovation.

The increasing use of tranexamic acid in surgical procedures, trauma care, and hematology is a major driver of growth in the Tranexamic Acid Market. Hospitals are adopting intravenous tranexamic acid to minimize blood loss during orthopedic and cardiac surgeries, where it plays a critical role in reducing transfusion needs and improving patient recovery times. Furthermore, its application in treating hemophilia and heavy menstrual bleeding underscores its versatility in clinical practice. The consistent demand from these medical fields has encouraged pharmaceutical companies to invest in expanding production capacity and enhancing drug formulations. This broadening clinical adoption positions tranexamic acid as a cornerstone of modern healthcare practices.

The Tranexamic Acid Market faces restraints due to increasingly stringent regulatory standards governing pharmaceutical manufacturing and quality assurance. Compliance with global frameworks requires advanced testing protocols, extensive clinical trials, and continuous monitoring of production processes. While these regulations ensure patient safety and therapeutic efficacy, they increase development timelines and operational costs for manufacturers. Smaller firms, in particular, face challenges in scaling their operations to meet such requirements, which can limit innovation and market entry. These compliance demands, although essential, act as a bottleneck in accelerating the availability of new and innovative tranexamic acid products.

The rising demand for advanced skin care treatments presents a significant opportunity in the Tranexamic Acid Market. Dermatologists and cosmetic companies are increasingly formulating tranexamic acid into topical creams, serums, and oral supplements to address hyperpigmentation, melasma, and uneven skin tone. The compound’s proven effectiveness in reducing melanin synthesis without causing skin irritation has led to its widespread adoption in premium cosmetic product lines. With consumer spending on personal care and dermatology treatments steadily increasing in Asia-Pacific and Europe, manufacturers are investing heavily in dermatology-focused R&D. This opportunity is further amplified by the integration of novel drug delivery technologies, such as liposomal and nanoencapsulation methods, to improve efficacy and absorption rates.

The Tranexamic Acid Market is facing challenges from increasing costs of raw materials, energy, and advanced production technologies. Manufacturers are under pressure to balance affordability with the need for precision in synthesis and compliance with stringent quality standards. Fluctuations in chemical feedstock prices, coupled with rising utility expenses, have added further strain on profitability. Additionally, specialized equipment for antifibrinolytic drug production requires significant capital investment and ongoing maintenance, which adds to operational burdens. These factors collectively create cost-related challenges that may restrict scalability, particularly for small- and mid-sized pharmaceutical firms, and could limit the pace of innovation within the industry.

Integration of AI in Chemical Synthesis: AI-driven tools are being increasingly applied in the Tranexamic Acid Market to optimize synthesis pathways and reduce waste. By utilizing predictive models, manufacturers have reported improved reproducibility in batch production, lowering both time and resource expenditure.

Expansion of Topical Dermatology Applications: The cosmetics industry is rapidly adopting tranexamic acid in advanced formulations for pigmentation control. Clinical studies have validated its effectiveness in reducing melasma, driving its use in next-generation skincare lines.

Sustainability in Pharmaceutical Manufacturing: Environmental concerns are influencing the Tranexamic Acid Market, with firms investing in green chemistry and waste-reduction technologies. Energy-efficient production units and eco-friendly solvents are increasingly being deployed to minimize environmental impact.

Advancements in Drug Delivery Systems: Novel delivery platforms, including liposomal encapsulation and microneedle-based applications, are reshaping how tranexamic acid is administered. These technologies enhance bioavailability and therapeutic outcomes, offering competitive differentiation for pharmaceutical companies.

The Tranexamic Acid Market is segmented by type, application, and end-user, each contributing uniquely to its overall growth trajectory. By type, the market spans injectable formulations, oral solutions, topical preparations, and others, reflecting diverse therapeutic and cosmetic uses. Injectable forms dominate due to their clinical adoption in hospitals and surgical environments, while topical and oral solutions are gaining traction in dermatology and consumer healthcare. By application, usage in surgical procedures and trauma management stands out as the most critical segment, with dermatology and gynecology applications emerging rapidly due to consumer demand for advanced skincare and women’s health solutions. From an end-user perspective, hospitals and surgical centers hold the strongest position due to consistent demand for tranexamic acid in emergency and operative care, while dermatology clinics and cosmetic companies are driving growth in consumer-focused segments. Together, these dimensions of segmentation highlight a balanced mix of established and emerging demand sources shaping the market’s future.

Injectable tranexamic acid remains the leading product type in the market, primarily due to its widespread adoption in hospitals and surgical centers. It is the preferred choice for reducing intraoperative and postoperative blood loss, particularly in orthopedic, cardiac, and trauma-related surgeries, where rapid and reliable results are critical. This dominance is reinforced by clinical guidelines that recommend injectable formulations for acute bleeding conditions. On the other hand, topical tranexamic acid is the fastest-growing type, driven by increasing integration into dermatology and cosmetic formulations. Its proven efficacy in treating hyperpigmentation and melasma, combined with consumer demand for non-invasive treatments, has fueled rapid product development in skincare lines. Oral solutions also hold a notable position, serving long-term therapeutic needs such as managing menorrhagia and other chronic bleeding disorders. Although smaller in market share, emerging formats like combination therapies and advanced delivery systems are gaining niche relevance, reflecting broader diversification in the Tranexamic Acid Market.

Surgical procedures represent the leading application area in the Tranexamic Acid Market, owing to the critical role the compound plays in reducing blood loss and minimizing transfusion requirements during major operations. Its application in trauma care and emergency medicine further consolidates this leadership position, where immediate intervention is vital. Dermatology, however, stands out as the fastest-growing application segment, as tranexamic acid is increasingly adopted in cosmetic and therapeutic skincare products. Rising consumer awareness of hyperpigmentation treatments, combined with technological advancements in topical and oral delivery, is propelling this growth. Gynecology also represents a key application, with tranexamic acid being widely prescribed for conditions such as heavy menstrual bleeding. Hematology and other niche applications contribute meaningfully by expanding the therapeutic footprint, ensuring consistent demand across diverse medical disciplines. This multi-sector adoption underscores the compound’s versatility and highlights the expanding role of tranexamic acid in both clinical and consumer-focused industries.

Hospitals are the leading end-user segment in the Tranexamic Acid Market, driven by continuous demand for injectable formulations in surgical, trauma, and emergency care. Their established infrastructure and reliance on standardized treatment protocols ensure consistent utilization across diverse clinical settings. Dermatology clinics and cosmetic companies are emerging as the fastest-growing end-user group, propelled by rising consumer interest in advanced skin treatments and the increasing commercialization of tranexamic acid-based cosmetic products. These organizations are investing in product innovation, expanding the availability of topical and oral formulations designed for pigmentation control and skincare. Research institutions also play a role, focusing on the development of novel formulations and exploring expanded therapeutic indications. Additionally, pharmaceutical manufacturers themselves act as significant end-users, channeling investments into advanced drug delivery systems and large-scale production. Collectively, this diverse end-user landscape highlights the broad adaptability of tranexamic acid, ensuring sustained market growth across both healthcare and consumer-driven industries.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

The dominance of Asia-Pacific is driven by the significant pharmaceutical and healthcare manufacturing base across countries such as Japan, China, and India, where advanced drug formulation capabilities, growing investments in healthcare infrastructure, and strong adoption of tranexamic acid in surgical and therapeutic procedures play a central role. Meanwhile, North America benefits from rapid innovation, higher adoption in dermatology and cosmetic applications, and supportive regulatory pathways driving future expansion.

The North America Tranexamic Acid Market represented nearly 28% of the global volume in 2024, with strong demand emerging from pharmaceutical, cosmetic, and clinical sectors. Increasing adoption in dermatology and aesthetic medicine is supported by regulatory approvals for topical formulations, while the pharmaceutical industry leverages tranexamic acid in trauma and surgery management. The U.S. and Canada benefit from digital transformation in healthcare supply chains, advanced R&D investments, and automation in drug manufacturing, which enhances overall efficiency. Additionally, supportive government frameworks encouraging innovation in biopharmaceuticals have accelerated product availability across clinical and cosmetic applications.

The Europe Tranexamic Acid Market accounted for approximately 22% of global share in 2024, with Germany, France, and the UK being the largest contributors. Demand is driven by increasing use in surgical procedures and dermatological therapies. European regulatory bodies emphasize quality and safety in pharmaceuticals, encouraging sustainable manufacturing and ethical sourcing practices. Notably, the EU’s focus on green chemistry and low-emission processes has pushed companies to innovate. Cosmetic applications of tranexamic acid, particularly in skin-brightening and hyperpigmentation treatments, are also gaining momentum, fueled by higher consumer awareness and the adoption of advanced formulation technologies.

The Asia-Pacific Tranexamic Acid Market stood as the global leader in 2024 with 42% market share, supported by high consumption in Japan, China, and India. Japan remains a major hub with advanced drug development capabilities and widespread integration of tranexamic acid in both therapeutic and cosmetic formulations. China’s strong pharmaceutical manufacturing base and India’s expanding healthcare sector further strengthen the region’s position. Investments in production facilities, coupled with advanced R&D initiatives, are enabling Asia-Pacific to remain the supply backbone. Regional innovation hubs are also focusing on new delivery formats like dissolvable tablets and topical solutions for dermatology.

The South America Tranexamic Acid Market accounted for nearly 6% of global volume in 2024, led by Brazil and Argentina. Healthcare reforms and increasing investments in surgical infrastructure have driven demand for hemostatic drugs. Brazil, with its expanding pharmaceutical manufacturing capabilities, has emerged as a key contributor. Additionally, policies encouraging local production are improving access and affordability of drugs across the region. Adoption in cosmetic and dermatology applications is gradually increasing, with a particular focus on urban centers that are witnessing higher consumer demand for advanced skincare and clinical treatments.

The Middle East & Africa Tranexamic Acid Market accounted for around 2% of global share in 2024, with the UAE, Saudi Arabia, and South Africa emerging as key contributors. Expanding healthcare infrastructure, particularly in trauma care and surgical facilities, is driving demand for tranexamic acid. Technological modernization in pharmaceutical production facilities, combined with supportive government partnerships, is enhancing regional capacity. Growing medical tourism in the UAE and Saudi Arabia further adds to market expansion. The region’s regulatory authorities are increasingly aligning with global standards, improving the adoption of safe and effective hemostatic drugs.

Japan – 21% Market Share

Japan leads the Tranexamic Acid Market due to its advanced pharmaceutical R&D ecosystem, strong clinical application base, and widespread use of the compound in both medical and cosmetic sectors.

China – 15% Market Share

China follows with a robust production capacity supported by a large-scale pharmaceutical manufacturing sector and rapidly expanding healthcare infrastructure driving domestic demand.

The Tranexamic Acid Market is characterized by a moderately consolidated competitive landscape, with approximately 30–35 active global and regional players shaping the industry. Leading manufacturers are positioned through extensive production capacity, diversified product portfolios, and strong distribution networks targeting both therapeutic and cosmetic applications. Companies are adopting strategic initiatives such as acquisitions to strengthen supply chains, joint ventures to expand global reach, and product launches focused on advanced formulations such as oral dispersible tablets and topical solutions. Innovation remains a key differentiator, with firms investing in process optimization technologies that improve purity levels and reduce production costs. Increasing collaboration between pharmaceutical manufacturers and dermatology specialists is also influencing market growth. Competitive intensity is further heightened by the entry of mid-sized firms from Asia-Pacific, leveraging cost-competitive production and rising demand in regional markets. Overall, the landscape reflects a mix of established leaders and agile new entrants, creating an environment driven by technological progress and clinical application expansion.

Pfizer Inc.

Teva Pharmaceutical Industries Ltd.

Sun Pharmaceutical Industries Ltd.

Takeda Pharmaceutical Company Limited

Zydus Lifesciences Ltd.

Mylan N.V. (Viatris Inc.)

Hikma Pharmaceuticals PLC

Cipla Ltd.

Apotex Inc.

Glenmark Pharmaceuticals Ltd.

Technological advancements are reshaping the Tranexamic Acid Market, particularly in manufacturing, formulation, and delivery systems. Continuous improvements in synthesis and purification technologies have enabled producers to achieve higher yields and greater consistency in active pharmaceutical ingredients. For instance, advanced crystallization and filtration systems have minimized impurities, ensuring compliance with stricter global quality standards.

In drug delivery, new oral dispersible tablets and topical formulations are gaining traction for their enhanced patient compliance and faster therapeutic action. Dermatology applications, particularly for hyperpigmentation treatments, are benefiting from nanotechnology-based carriers that improve skin penetration and increase bioavailability. Moreover, injectable delivery systems are being refined with sustained-release technologies, reducing dosage frequency and enhancing clinical outcomes.

Digital transformation is also evident, with the integration of AI-driven predictive analytics in production planning and quality assurance. Automated manufacturing lines, combined with real-time monitoring, are reducing downtime and improving cost efficiency. Additionally, blockchain-enabled traceability solutions are being piloted to ensure transparency in pharmaceutical supply chains.

The future trajectory of the market is expected to see further integration of green chemistry practices to reduce environmental impact and the adoption of biotechnological methods to innovate alternative production pathways. These developments collectively support a more efficient, sustainable, and patient-centric approach in the global Tranexamic Acid Market.

In February 2024, Takeda Pharmaceutical expanded its production facility in Japan to increase the output of tranexamic acid formulations, integrating advanced purification systems to meet rising clinical and cosmetic demand.

In October 2023, Sun Pharmaceutical launched a new line of topical tranexamic acid gels targeting dermatology applications, particularly for hyperpigmentation, with initial availability across key Asian and European markets.

In July 2024, Pfizer announced the adoption of continuous manufacturing technologies for tranexamic acid production in the United States, significantly improving efficiency and reducing cycle times.

In March 2023, Cipla introduced an oral dispersible tablet form of tranexamic acid in India, improving patient compliance in both hospital and outpatient treatment scenarios.

The scope of the Tranexamic Acid Market Report encompasses a detailed analysis of global market dynamics, covering types, applications, end-users, and geographic regions. By type, the report evaluates injectable, oral, topical, and other emerging formulations, reflecting the growing diversification in clinical and cosmetic uses. By application, the report highlights critical sectors such as surgical procedures, trauma care, dermatology, gynecology, and hematology, offering insights into how each contributes to overall demand. End-user analysis includes hospitals, surgical centers, dermatology clinics, pharmaceutical manufacturers, and research institutions, reflecting the broad scope of market adoption.

Geographically, the report examines key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each with unique consumption drivers, regulatory environments, and technological developments. The analysis also covers production hubs, emerging consumption centers, and regional innovation ecosystems.

The report’s technology focus explores advancements in drug formulation, manufacturing efficiencies, and digital integration, while also considering sustainability initiatives and green chemistry practices. Additionally, it identifies emerging niche segments such as nanotechnology-enabled topical solutions and biotechnological production pathways.

Overall, the report provides decision-makers with comprehensive insights into current industry dynamics, regional opportunities, competitive strategies, and technological trends, serving as a strategic guide for stakeholders across the global Tranexamic Acid Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 8,659.0 Million |

| Market Revenue (2032) | USD 13,594.2 Million |

| CAGR (2025–2032) | 5.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Pfizer Inc., Teva Pharmaceutical Industries Ltd., Sun Pharmaceutical Industries Ltd., Takeda Pharmaceutical Company Limited, Zydus Lifesciences Ltd., Mylan N.V. (Viatris Inc.), Hikma Pharmaceuticals PLC, Cipla Ltd., Apotex Inc., Glenmark Pharmaceuticals Ltd., Amneal Pharmaceuticals |

| Customization & Pricing | Available on Request (10% Customization is Free) |