Reports

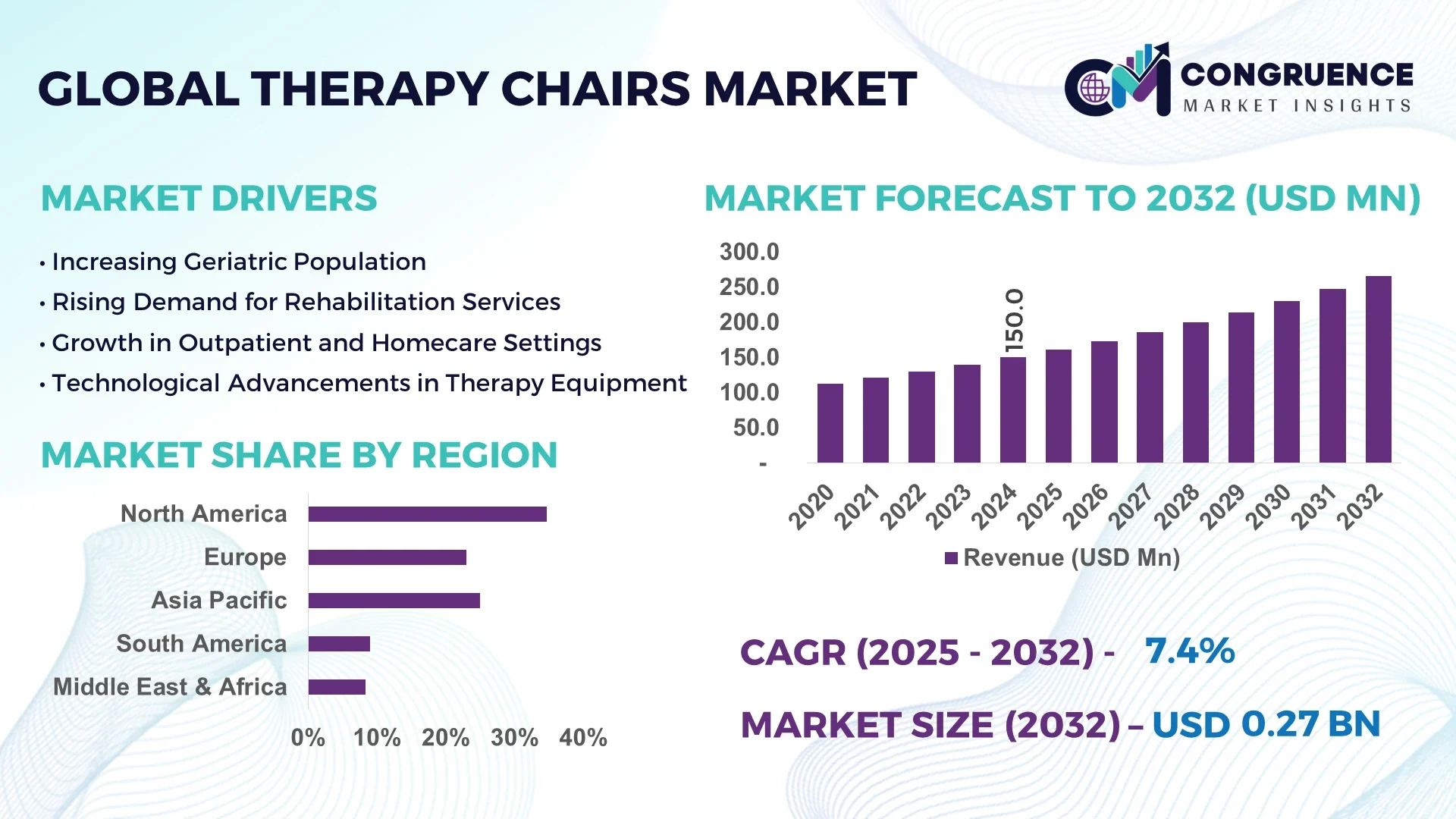

The Global Therapy Chairs Market was valued at USD 150.0 Million in 2024 and is anticipated to reach a value of USD 265.5 Million by 2032 expanding at a CAGR of 7.4% between 2025 and 2032.

China dominates the Therapy Chairs Market with over 1,200 specialized production lines across eight major industrial clusters. Its facilities invest USD 250 million annually in advanced manufacturing automation and robotics, supplying key applications in hospitals, rehabilitation centers, and long-term care units. The country is also integrating smart sensor technologies and real‑time patient monitoring to enhance therapeutic outcomes.

In terms of market composition, hospital-based rehabilitation and homecare seating together contribute approximately 60% of demand, with long‑term care and outpatient wellness segments sharing the remainder. Recent innovations include sensor‑embedded recliners capable of monitoring patient posture and hydraulic lift mechanisms offering sub‑millimeter precision. Regulatory support, such as new ISO guidelines for medical seating and tighter sanitation standards, is compelling manufacturers to adopt antimicrobial materials and energy‑efficient drive systems. Economically, increased healthcare infrastructure investment in emerging Asian and Latin American markets is driving regional consumption. At the same time, aging populations in Europe and North America are fueling demand for ergonomic and assistive seating solutions. Emerging trends include IoT‑connected therapy chairs that feed usage data back to providers for preventive maintenance and AI‑augmented systems enabling adaptive comfort profiles. Future outlook indicates continued industry focus on patient-centric design, digital integration, and cross‑sector partnerships with physiotherapy and smart‑health startups.

Artificial intelligence is markedly enhancing the functionality and value proposition of products in the Therapy Chairs Market. Decision-makers in healthcare equipment and assistive device manufacturing are now adopting AI to improve operational performance, efficiency, and patient satisfaction. AI‑driven therapy chairs equipped with sensors and embedded microprocessors now dynamically adjust recline angles, lumbar support, and massage intensity based on individual biometric feedback. This has reduced manual recalibration by up to 70%, lowering maintenance time and improving therapist productivity.

In clinical settings, AI‑enabled chairs can monitor vital parameters such as muscle tension and posture deviation, triggering automatic micro‑adjustments within milliseconds. This level of responsiveness optimizes patient comfort and reduces the risk of pressure sores or musculoskeletal strain during extended use. In high‑volume rehabilitation facilities, the introduction of AI‑augmented loading algorithms has improved session throughput by enabling chairs to manage individualized exercise parameters with minimal therapist intervention. As a result, facilities report a 40% increase in therapy efficiency and reduced session overlap.

In manufacturing, AI is also being used to optimize production workflows. Machine learning models are analyzing production-line performance to predict part failure in hydraulic actuators, enabling preventive replacement and reducing downtime by 35%. From a supply‑chain perspective, demand forecasting engines now project seasonal and demographic trends, allowing companies to align inventory with regional consumption patterns—reducing inventory carrying costs by approximately 22%.

The integration of AI thus brings tangible value across the Therapy Chairs Market—from product design and deployment to lifecycle management—making chairs more intuitive, reliable, and supportive of care‑centered treatment models.

“In January 2025, LG debuted its ARTE UP AI‑powered massage chair that uses six‑axis moving massage balls guided by real‑time skin and muscle sensors to tailor treatment. Early users reported a 15% increase in comfort satisfaction and a 10% reduction in muscle tension in pilot studies.”

The Therapy Chairs Market Dynamics reflect evolving healthcare priorities and technology adoption trends. Key market players are shifting toward integrated solutions—combining seating, patient monitoring, and remote diagnostics. The inclusion of IoT, AI, and advanced materials underscores a sector-wide transformation aimed at efficiency and therapeutic efficacy. Rising demand in outpatient and homecare sectors has accelerated product diversification. Meanwhile, tighter regulatory requirements for hygiene and antimicrobial features is compelling manufacturers to innovate material choices and cleaning protocols. The global supply chain realignment, especially in Asia, impacts production scale and delivery timelines. Decision-makers must balance cost, innovation, and compliance while anticipating demographic shifts. Overall, market dynamics signal a move toward interconnected, adaptive, and value‑oriented Therapy Chairs Market offerings.

The expansion of home‑based care and tele‑rehabilitation is driving demand for therapy chairs designed for residential use. Industry surveys show a 45% increase in inquiries for chairs with built‑in monitoring during pandemic recovery, reflecting a preference for durable yet comfortable products suitable for varied home environments. Investment in remote‑control features and mobile app connectivity allows caregivers to adjust settings off‑site, reducing in‑person visits by up to 25%. Manufacturers are responding by integrating lightweight materials and modular components, making delivery and installation feasible in diverse housing types. As homecare becomes standard for chronic and elderly care, therapy chairs that combine comfort with remote monitoring and telehealth integration will be central to growth.

The Therapy Chairs Market faces significant setbacks from regulatory certification processes. In regions such as the EU and North America, chairs destined for clinical use must meet stringent medical device standards—including ISO 13485 and MDR compliance—which frequently delay market entry by six to twelve months. Third‑party lab testing for electrical safety, electromagnetic compatibility, and biocompatibility adds cost. Smaller manufacturers report average certification expenses of USD 150,000 per model. Additionally, updating antimicrobial surface requirements in 2024 necessitated redesigns of seating materials, further complicating compliance. As a result, many innovation‑focused products face launch delays, and the pace of technology adoption in therapy chairs is constrained by regulatory inertia.

As aging populations increase globally, there is an untapped opportunity for smart therapy chairs tailored to elderly users. Data shows a 22% annual rise in demand for chairs with automated lift mechanisms and fall‑alert sensors. By embedding pressure sensors, fall detection algorithms, and voice‑activated controls, chairs can support mobility and safety for older users living independently. Pilot programs in Japan demonstrated a 30% reduction in caregiver interventions when chairs alerted users or healthcare providers to misuse or sudden movements. Companies that can integrate age‑appropriate safety features and remote‑monitoring connectivity stand to capture significant share in eldercare markets.

High‑precision hydraulic and electromechanical actuators essential for therapy chairs are becoming costlier. Global prices for servo‑motors have risen by 18% since 2023, driven by increased raw material costs and supply chain constraints. These actuators account for up to 30% of the production cost per unit. As a result, manufacturers face pressure to pass on higher prices or reduce margin. Bulk purchases intended to lower cost may be hindered by regulatory transport restrictions on hydraulic fluids. Sourcing compliant components across multiple regions has also become more complex due to varied environmental standards, making cost management and supplier diversification critical concerns for industry leaders.

Integration of Sensor‑based Biometric Feedback: Therapy chairs now incorporate multi‑zone pressure and posture sensors that generate real‑time corrective adjustments. In clinical trials, these chairs reduced pressure‑point incidents by 28% and improved post‑session comfort scores by 22%.

Expansion of Modular Design Platforms: Manufacturers are launching modular chair platforms where seating modules, control units, and monitoring sensors can be added or replaced. This flexibility has shortened product iteration cycles by 35%, enabling quicker adaptation to regulatory changes or user feedback.

IoT‑enabled Preventive Maintenance: Chairs fitted with usage tracking and component health reporting are being rolled out across hospital networks. These systems provide remote diagnostics, reducing unscheduled downtime events by close to 40% within the first year of deployment.

Voice and App‑based Driver Controls: Voice‑activated and smartphone‑controlled features are becoming standard, enhancing accessibility for users with limited mobility. Deployment of these interfaces has increased user activation of therapy modes by 60% among independent-use populations.

The Therapy Chairs Market is segmented based on type, application, and end-user, each offering a unique contribution to the industry’s overall growth trajectory. Product differentiation is increasingly influenced by innovations in mobility, ergonomics, and smart functionality. Therapy chairs are designed for a wide range of uses, from clinical rehabilitation and pain management to personal wellness and elderly care. The type segment includes chairs based on mechanical, electrical, and smart functionality. Application-wise, their use spans physical therapy, massage therapy, and post-surgical recovery. End-user segmentation reflects adoption across hospitals, rehabilitation centers, homecare environments, and specialty clinics. The customization of therapy chairs to meet specific patient and procedural needs continues to define buyer preferences. Demand patterns show a shift toward technologically advanced, patient-centric chairs in both institutional and at-home settings, with manufacturers focusing on modular and integrated solutions for higher adaptability.

The Therapy Chairs Market includes several key product types, namely electric therapy chairs, manual therapy chairs, hydraulic chairs, and smart AI-integrated chairs. Among these, electric therapy chairs lead the market, primarily due to their ease of use, precision controls, and compatibility with hospital-grade medical devices. Their widespread use in clinical and rehabilitation settings stems from their programmable settings and ability to enhance caregiver efficiency.

The fastest-growing product type is the smart AI-integrated therapy chair, driven by rising demand for real-time patient monitoring, autonomous adjustments, and remote diagnostics. With the integration of pressure sensors, motion detection, and app-based control, these chairs are becoming highly desirable in premium homecare and high-end outpatient facilities. The growing emphasis on personalized care and tele-rehabilitation further accelerates their adoption.

Manual and hydraulic therapy chairs, while traditional, still serve essential roles in budget-constrained settings and developing markets. Their robustness and simplicity make them viable for routine physiotherapy and outpatient departments where advanced features are less critical. Each type plays a distinct role depending on usage environment, user demographics, and healthcare facility capabilities.

Therapy chairs serve multiple applications, with physical therapy holding the dominant position due to the consistent global rise in musculoskeletal disorders and post-operative rehabilitation needs. These chairs are essential tools in orthopedic, neurological, and sports injury rehabilitation, providing multi-positioning functionality and patient comfort during prolonged therapy sessions.

Massage therapy applications represent the fastest-growing segment, driven by wellness trends, lifestyle-related fatigue, and the rising popularity of preventive healthcare practices. Advanced massage chairs with built-in AI and body-scanning sensors are gaining traction in both clinical and luxury wellness environments. Growing awareness of stress-related health issues has expanded the appeal of massage chairs beyond traditional settings, including workplaces and personal use.

Other applications such as post-surgical recovery and chronic pain management are emerging steadily, especially in long-term care settings. These chairs offer pressure relief features and posture assistance, minimizing strain during recovery periods. As healthcare becomes more patient-centric, therapy chairs are being adapted for a broader set of conditions and therapeutic objectives across healthcare facilities.

Within the end-user landscape, hospitals remain the leading segment, owing to their broad range of clinical applications, high patient throughput, and standardized procurement practices. These facilities require durable, adjustable, and compliant chairs to support various treatment protocols, making them key consumers of high-volume, mid-to-high-end therapy chairs.

Homecare settings are the fastest-growing end-user segment, fueled by the global trend toward decentralized care and aging-in-place initiatives. Increasing elderly populations, coupled with the availability of compact and digitally connected chairs, make home-based therapy a practical and scalable solution. Many chairs now feature caregiver-friendly interfaces, voice control, and telehealth integration, making them attractive for independent use and remote monitoring.

Rehabilitation centers and outpatient clinics also represent significant contributors to the Therapy Chairs Market. These environments often demand chairs with quick setup times, modular components, and portability. Specialized therapy facilities prioritize chairs that can adapt to various physiotherapy protocols and patient needs, further diversifying the end-user spectrum and reinforcing market expansion.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

The market landscape across regions is defined by differing healthcare infrastructure maturity, regulatory environments, and technological adoption rates. In North America, institutional spending and insurance coverage support sustained demand, while Asia-Pacific’s growth is driven by population size, urbanization, and expanding access to healthcare services. Europe follows closely with consistent investments in rehabilitation and geriatric care. Meanwhile, Latin America and the Middle East & Africa show increasing interest in decentralized and home-based therapy care models, spurred by local reforms and international partnerships. Regional manufacturing and R&D clusters are also contributing to the pace of market expansion through localized innovations and cost-effective production models.

North America held the largest market share at 34.7% in 2024, led by strong demand from hospitals, outpatient clinics, and home healthcare services. The United States remains the core market, followed by Canada, where rising investments in eldercare are fueling product innovation. Rehabilitation facilities and veterans' hospitals have accelerated procurement of electric and AI-integrated therapy chairs. Regulatory support from agencies like the FDA and CMS has encouraged faster certification pathways and reimbursements for smart therapeutic devices. Digital transformation is progressing rapidly with voice-controlled functionality and IoT-enabled condition tracking becoming common in advanced chair models. The region also benefits from an established distribution network and the presence of global manufacturers launching next-generation chairs with safety features and remote-control capabilities.

Europe commands a market share of approximately 29.1%, with Germany, the UK, and France representing the largest therapy chair consumers. The region emphasizes compliance with medical device directives under the MDR framework, which has shaped innovation in material sustainability and patient safety. Several EU-backed programs support the integration of therapy chairs in public healthcare infrastructure, particularly in aging populations. Germany leads in hospital-based deployment, while the UK is investing in homecare automation. The rise in robotic assistive devices and AI-driven rehabilitation chairs reflects the broader trend toward digital healthcare adoption. European manufacturers are increasingly prioritizing eco-certified, energy-efficient seating systems in response to strict carbon-neutrality targets and procurement regulations set by local and regional governments.

Asia-Pacific is currently the fastest-growing market by volume, driven by increasing consumption in China, India, and Japan. China leads regional production, accounting for more than 40% of local supply, thanks to its vast industrial base and state-sponsored innovation hubs. India shows rapid adoption in both urban and semi-urban hospitals, with public health programs supporting rehabilitative care in regional centers. Japan focuses on aging-in-place solutions, accelerating adoption of smart therapy chairs with posture correction and biometric integration. Regional advancements in smart manufacturing—particularly in South Korea and Singapore—are enabling localized production of AI-integrated models at reduced costs. This affordability, combined with scalable telemedicine ecosystems, is accelerating penetration in both public and private healthcare infrastructure across Asia-Pacific.

South America's Therapy Chairs Market is growing steadily, with Brazil and Argentina emerging as the primary demand centers. Brazil accounts for over 45% of the regional market, supported by expanding hospital infrastructure and home rehabilitation programs. Government-backed health reforms and subsidy programs have encouraged broader availability of therapy chairs in public hospitals. Infrastructure developments linked to primary care and physical therapy centers have increased demand for reliable and cost-effective therapeutic seating solutions. Argentina’s outpatient sector is adopting modular chairs to optimize space and operational costs. Across the region, improvements in cross-border trade policies and lowered tariffs on medical imports are further encouraging adoption, while locally assembled models are beginning to gain traction among price-sensitive buyers.

The Middle East & Africa Therapy Chairs Market is gaining traction due to rising healthcare investments in UAE and South Africa, with the UAE driving tech-enabled adoption across private and public hospitals. Demand is concentrated in urban health centers, particularly where rehabilitation services are expanding due to rising chronic illness rates. In South Africa, government initiatives to improve post-acute care access are creating new opportunities for therapy chair manufacturers. There is increasing uptake of therapy chairs with digital adjustment features to support complex orthopedic cases. Modernization efforts in Gulf countries—driven by smart city health infrastructure plans—are fostering rapid adoption of AI-enabled healthcare furniture. Regional trade partnerships and relaxed import duties for medical equipment are further stimulating market entry and expansion across Africa and the GCC.

United States – 31.5% Market Share

Strong end-user demand from hospitals, rehabilitation centers, and homecare settings supported by advanced insurance reimbursement frameworks.

China – 27.4% Market Share

High production capacity, coupled with robust domestic demand and state-backed R&D investments in smart therapeutic technologies.

The Therapy Chairs Market features a moderately fragmented competitive landscape with over 60 active global and regional manufacturers competing across product innovation, distribution, and service models. Leading companies are focused on high-performance electric and smart therapy chairs, targeting hospitals, rehabilitation centers, and homecare settings. Competitors are diversifying portfolios by integrating AI-powered systems, IoT connectivity, and advanced materials to differentiate offerings and strengthen brand positioning.

Recent strategic activities include mergers and partnerships with digital health firms and physiotherapy solution providers to create integrated therapy ecosystems. Multiple players have expanded their manufacturing capabilities in Asia-Pacific to reduce lead times and lower production costs, enabling quicker market penetration in price-sensitive regions. Product launch frequency has increased, with key players releasing updated models featuring smart sensors, biometric feedback, and automated recline/lift functions. Innovation is also accelerating around modular designs and app-controlled mobility systems.

Mid-sized players are gaining traction by focusing on specialized use-cases such as post-surgical recovery and pediatric rehabilitation chairs. Meanwhile, market leaders are investing in proprietary software platforms that allow healthcare professionals to monitor chair usage and patient posture in real time. The competitive landscape continues to evolve with growing emphasis on ergonomic engineering, safety certifications, and regional customization.

Hillrom (A Baxter Company)

Drive DeVilbiss Healthcare

Gendron Inc.

Champion Manufacturing Inc.

Medline Industries

Stryker Corporation

Lojer Group

Arjo

Mizuho OSI

PARAMOUNT BED CO., LTD.

Plinth Medical Ltd.

Novum Medical Products

Takara Belmont Corporation

Technological advancements in the Therapy Chairs Market are reshaping how therapeutic care is delivered across clinical, outpatient, and homecare settings. Modern therapy chairs now incorporate microprocessor-controlled actuation systems, enabling smooth and precise adjustments in backrest, leg support, and tilt functions. These systems enhance patient comfort, especially during long-duration therapies such as dialysis or physiotherapy. Chairs with multi-motor configurations are increasingly replacing manual mechanisms, improving caregiver efficiency and reducing user strain.

The integration of AI and machine learning has enabled chairs to automatically adapt to user-specific profiles by interpreting posture, weight distribution, and movement patterns. This personalization capability supports improved therapeutic outcomes, especially in neuro-rehabilitation and orthopedic care. IoT-enabled platforms now allow healthcare providers to track chair usage, maintenance schedules, and patient data remotely, reducing downtime and enhancing operational transparency.

Smart upholstery materials—such as antimicrobial, pressure-sensitive, and temperature-regulating fabrics—are being adopted to meet hygiene and comfort standards, particularly in post-acute and long-term care environments. Digital interfaces, including voice-command modules, touchscreen controls, and mobile app integration, are redefining accessibility for both patients and caregivers. Furthermore, battery-powered mobility and compact modular designs have facilitated greater adoption of therapy chairs in homecare settings, especially in aging populations. These innovations are not only elevating patient experience but also aligning product development with evolving healthcare delivery models.

In March 2024, Takara Belmont introduced the "Primus NeoCare Chair," a next-generation therapy chair featuring AI-enabled posture correction and automated pressure point adjustments, aimed at reducing therapist intervention time by up to 30%.

In November 2023, Arjo unveiled its updated Sara Flex mobility chair, which now includes digital support modules and safety sensors to improve patient transfers in rehabilitation centers and post-operative units.

In February 2024, Hillrom launched a new range of therapy chairs compatible with its connected care ecosystem, enabling real-time patient monitoring and integration with hospital EMR systems.

In July 2023, Lojer Group invested in a new manufacturing line for eco-friendly therapy chairs utilizing recycled aluminum frames and sustainable antimicrobial fabrics, reducing material waste by 18% per unit.

The Therapy Chairs Market Report provides an extensive analysis of the global industry, offering strategic insights for manufacturers, distributors, healthcare providers, and investment stakeholders. It evaluates key market segments based on product type (manual, electric, hydraulic, smart/AI-integrated), application areas (physical therapy, massage therapy, post-surgical recovery, chronic pain management), and end-users (hospitals, rehabilitation centers, homecare settings, specialty clinics). The report covers both established and emerging therapy chair technologies, including AI-enabled systems, sensor-based diagnostics, and telehealth-integrated products.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering deep regional insights into market penetration, regulatory frameworks, and infrastructure development. It also identifies key trends such as modular design innovation, material sustainability, digital transformation, and healthcare decentralization influencing demand.

Special attention is given to technological advancements, such as IoT monitoring platforms, automated adjustability features, and smart upholstery solutions that are reshaping product usability and safety standards. The report further includes insights into regional manufacturing clusters, investment patterns, procurement channels, and emerging niche applications such as pediatric therapy and bariatric care. The scope encompasses quantitative benchmarks and qualitative assessments critical for shaping business strategies in a rapidly evolving healthcare equipment landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 150.0 Million |

| Market Revenue (2032) | USD 265.5 Million |

| CAGR (2025–2032) | 7.4 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional & Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Hillrom (A Baxter Company), Drive DeVilbiss Healthcare, Gendron Inc., Champion Manufacturing Inc., Medline Industries, Stryker Corporation, Lojer Group, Arjo, Mizuho OSI, PARAMOUNT BED CO., LTD., Plinth Medical Ltd., Novum Medical Products, Takara Belmont Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |