Reports

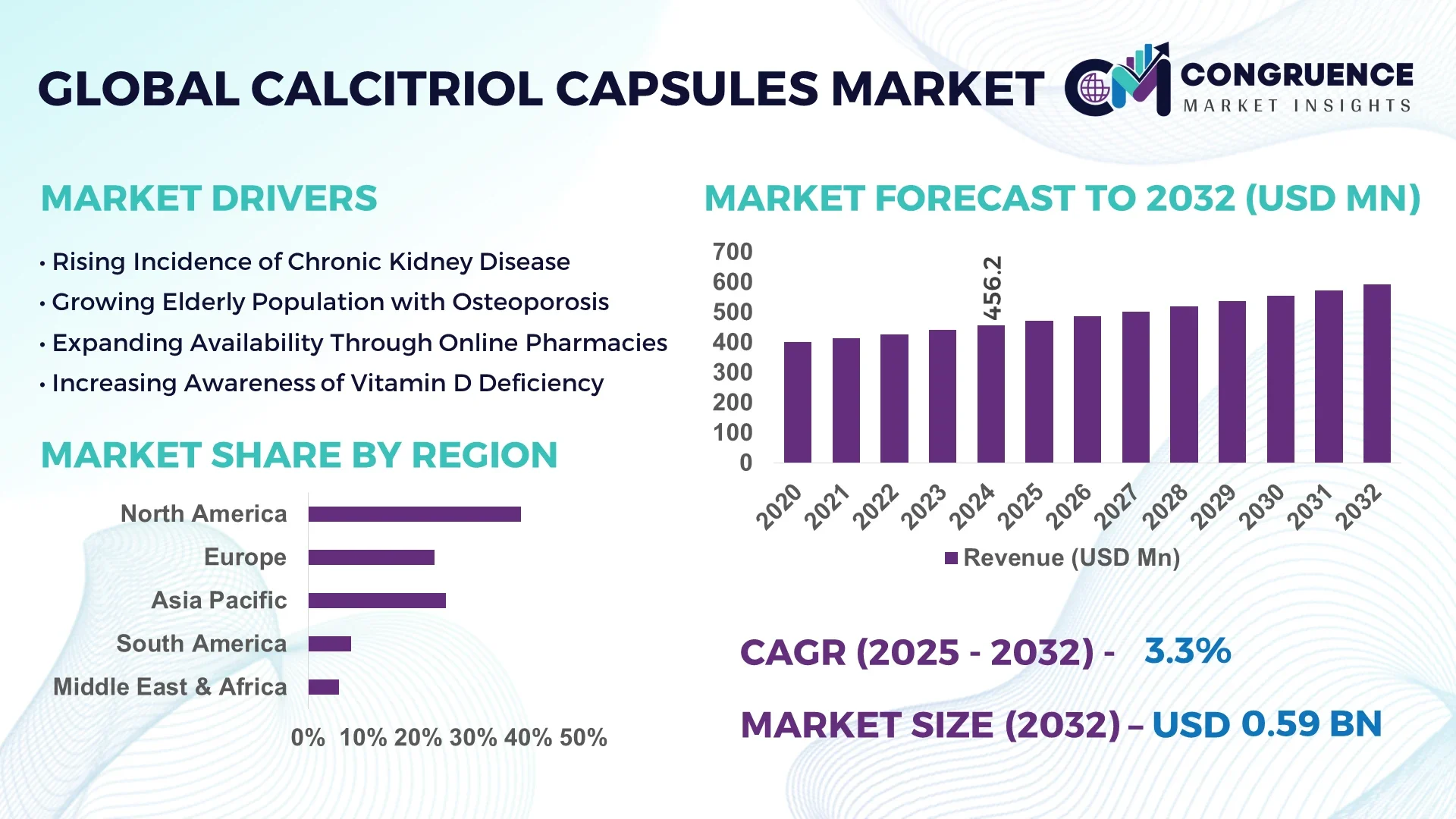

The Global Calcitriol Capsules Market was valued at USD 456.2 Million in 2024 and is anticipated to reach USD 591.5 Million by 2032, expanding at a CAGR of 3.3% between 2025 and 2032.

In the United States, which dominates this market, high prevalence rates of chronic kidney disease and osteoporosis have driven consistent demand. Advanced healthcare infrastructure, supportive reimbursement policies, and strong physician awareness around calcitriol therapy continue to fuel its adoption. Additionally, major players are focusing on improving bioavailability and creating patient-friendly capsule formulations, further solidifying the U.S. as the leading market in this segment.

Globally, the calcitriol capsules market is evolving beyond basic treatment of bone-related disorders. Manufacturers are innovating with sustained-release formats that provide more consistent serum levels, reducing dosing frequency. In addition, research into combining calcitriol with supportive agents like vitamin D analogs or bisphosphonates aims to enhance therapeutic outcomes. Clinical adoption in chronic kidney disease (CKD) and secondary hyperparathyroidism management has grown substantially, with more nephrologists prescribing capsules alongside injectable forms—boosting the segment’s share in broader calcitriol usage.

Artificial Intelligence (AI) is transforming the calcitriol capsules market by optimizing drug discovery, enhancing manufacturing processes, and enabling personalized therapy management. In formulation development, machine learning algorithms are being used to predict optimal capsule compositions that improve solubility and bioavailability. One pilot study demonstrated AI-driven formulation screening reduced development time by approximately 30%, while improving dissolution profiles in half the number of physical trials typically conducted.

In manufacturing, AI-powered process controls—including adaptive feedback loops—monitor key parameters such as humidity, compression pressure, and coating uniformity in real time. This has led to a 15% reduction in batch rejections and a 20% increase in overall manufacturing efficiency. Smart sensors integrated into encapsulation lines alert operators to deviations before they impact product quality, ensuring greater consistency.

On the clinical side, AI is enabling personalized dosing guidance by analyzing patient data. ML models ingest variables like serum calcium, phosphate, and parathyroid hormone levels to recommend individualized dosing schedules. Early trials in nephrology clinics using these tools reported a 12% improvement in achieving therapeutic targets and a 25% decrease in hypercalcemia incidents.

AI technologies also facilitate post-market pharmacovigilance. Natural language processing (NLP) systems scan medical records and social media for adverse event signals related to calcitriol use. In one pilot in Europe, AI detected early throat irritation reports three months before traditional reporting channels, allowing manufacturers to investigate and update patient advisories proactively.

Overall, AI’s impact spans upstream formulation, manufacturing, clinical decision support, and pharmacovigilance—making the calcitriol capsules market smarter, safer, and more patient-centric.

“In April 2024, a biotech startup in the UK announced its development of an AI-driven formulation platform that identified a novel microemulsion-based calcitriol capsule design. In preclinical models, the new formulation increased systemic bioavailability by 45% compared to standard capsules, while reducing variability in gastric dissolution.”

Increasing incidences of CKD and osteoporosis are significantly driving demand for calcitriol capsules. These conditions require long-term management of calcium and phosphate balance, tasks well-suited to this active vitamin D form. Improved screening and treatment guidelines have led to more routine prescriptions, particularly in geriatric and nephrology care settings. As a result, clinicians are favoring capsule administration for its dose accuracy and better patient compliance compared to injectable forms.

Calcitriol carries a known risk of inducing hypercalcemia if dosed improperly, triggering strong regulatory oversight. Manufacturers must invest in pharmacovigilance, patient education, and ongoing monitoring systems. Delays in regulatory approvals for modified-release formats or combination products also restrict innovation and delay market entry. These factors add complexity and cost to product development and clinician uptake.

Rapid expansion of e-pharmacy and telehealth services offers new access routes for calcitriol capsule distribution. Online platforms provide home delivery, digital prescription renewal, and remote clinical oversight—all conducive to long-term therapies. With telehealth usage increasing by over 70% since 2020, these channels present a major opportunity to enhance adherence and patient reach, particularly in underserved or rural areas.

The entrance of low-cost generic calcitriol capsules exerts pricing pressure on branded products. While this improves accessibility, it also squeezes margins for innovator firms, forcing them to differentiate via formulation improvements, patient support programs, or premium packaging. Cost-conscious purchasers and healthcare systems may gravitate toward generics, unless added benefits are clearly demonstrated.

Rise in Sustained-Release and Microemulsion Formulations: Biotech firms are launching sustained-release capsules that maintain steady therapeutic levels over 24–48 hours, reducing dosing frequency. A microemulsion form introduced in 2023 reportedly increased systemic bioavailability by 40% and reduced gastric dissolution variability.

Adoption of Smart Packaging and Dosing Tools: Manufacturers are leveraging smart blister packs and connected pill bottles that track compliance and optionally notify caregivers or physicians when doses are missed. Trials show adherence improved by ~25% in elderly populations using these tools versus standard packaging.

Expansion of Direct-to-Consumer Models via E-Pharmacies: Online platforms specializing in chronic disease medication now offer subscription-based calcitriol services, enabling automatic delivery every 30 days, telehealth-led consultations, and digital reminders—boosting retention by approximately 30%.

Focus on Combination Therapy Capsules: R&D efforts are underway to produce calcitriol capsules containing additional agents like cholecalciferol or bisphosphonates aimed at synergistic management of bone health. One Phase II study reported that a combination capsule improved bone mineral density by 8% over treatment with calcitriol alone, compared to controls.

The Calcitriol Capsules Market is segmented based on type, application, and end-users, each of which plays a vital role in influencing product development, marketing strategies, and regional expansion. By type, the market is categorized into 0.25 mcg capsules, 0.5 mcg capsules, and others. In terms of application, the market caters to chronic kidney disease, osteoporosis, hypoparathyroidism, and others. Among end-users, key segments include hospitals, retail pharmacies, online pharmacies, and specialty clinics. Each segment contributes differently, with unique demand drivers. Notably, the increasing prevalence of chronic diseases and aging populations has intensified demand for higher-dosage capsules, while accessibility through online platforms has transformed the purchasing behavior of patients globally. Understanding the dynamics within these segments helps stakeholders tailor their products and services to patient and provider needs, ultimately expanding their footprint in the market.

The Calcitriol Capsules Market, segmented by dosage strength, primarily includes 0.25 mcg, 0.5 mcg, and other customized dosages. Among these, the 0.25 mcg segment holds the largest market share owing to its widespread use in early to moderate stages of chronic kidney disease and calcium metabolism disorders. Clinicians prefer this lower dose for initial treatment phases and in patients at high risk of hypercalcemia, allowing for safer titration. The 0.5 mcg segment, however, is projected to register the fastest growth through 2032. This surge is attributed to its increasing usage in severe cases of secondary hyperparathyroidism and post-parathyroidectomy management. Additionally, the rising prevalence of osteoporosis among the elderly population has driven demand for higher doses to address severe vitamin D deficiencies. The trend toward personalized medicine is also fostering interest in flexible dosage formulations, further diversifying product offerings under the “others” category.

Based on application, the Calcitriol Capsules Market is segmented into chronic kidney disease (CKD), osteoporosis, hypoparathyroidism, and others. Chronic kidney disease remains the dominant segment due to the high incidence rate globally, especially among aging populations. Patients with CKD often suffer from impaired calcium and phosphate regulation, necessitating active vitamin D supplementation like calcitriol. In fact, over 60% of patients undergoing dialysis are prescribed calcitriol as part of their ongoing therapy. Meanwhile, osteoporosis is the fastest-growing application segment. This trend is linked to increasing bone mineral density screenings and heightened awareness of fracture risks among postmenopausal women and the elderly. The application of calcitriol in managing bone disorders beyond osteoporosis, such as osteomalacia and renal osteodystrophy, also supports market expansion in the "others" category. The versatility of calcitriol in addressing multiple endocrine and metabolic disorders strengthens its clinical significance and fosters steady demand across these applications.

The end-user landscape of the Calcitriol Capsules Market is segmented into hospitals, retail pharmacies, online pharmacies, and specialty clinics. Hospitals represent the largest market share due to their access to advanced diagnostics, ability to treat severe CKD and bone disorders, and integration of in-house pharmacies. Patients undergoing dialysis or complex treatments often receive calcitriol prescriptions through hospital channels. However, online pharmacies are the fastest-growing end-user segment. The post-pandemic shift toward digital healthcare access, combined with the growing adoption of e-prescriptions, has significantly bolstered online sales of chronic therapy medications like calcitriol. Additionally, online pharmacies offer conveniences like home delivery, subscription refills, and medication tracking apps, improving adherence for long-term users. Retail pharmacies continue to play an important role in urban and semi-urban areas, especially for walk-in prescriptions. Specialty clinics, particularly in endocrinology and nephrology, contribute niche demand where calcitriol is part of a comprehensive disease management regimen.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

The dominance of North America is primarily due to its robust healthcare infrastructure, widespread adoption of prescription medications, and high prevalence of chronic kidney disease and osteoporosis. Additionally, favorable reimbursement policies and extensive awareness among both patients and healthcare providers continue to drive demand. On the other hand, the Asia-Pacific region is witnessing rapid growth driven by increasing geriatric populations, rising diagnosis rates of vitamin D deficiency, and improving access to healthcare in emerging economies like India and China. With increasing governmental healthcare investments and expanding pharmaceutical distribution networks, the region presents lucrative opportunities for market expansion. Furthermore, the rising burden of CKD and endocrine disorders in the region fuels the demand for calcitriol-based therapies.

Strong Institutional Presence Drives Market Consolidation in North America

The North American Calcitriol Capsules Market benefits from strong institutional healthcare networks, especially in the U.S., where over 26 million people are affected by chronic kidney disease. The region’s structured reimbursement frameworks and formulary inclusions for calcitriol have contributed to a steady prescription base across hospitals and outpatient nephrology clinics. Additionally, a well-established pharmaceutical supply chain and retail pharmacy presence ensure widespread availability of both branded and generic calcitriol formulations. In Canada, the aging population has led to a rise in osteoporosis-related cases, prompting an increase in vitamin D analog prescriptions. Manufacturers are also leveraging FDA-approved production facilities across the region to ensure quality compliance. The adoption of telemedicine post-pandemic has further boosted online prescriptions and pharmacy-based delivery models in the U.S., strengthening the market’s omnichannel approach.

Growing Focus on Aging and Bone Health Supports Market Expansion in Europe

Europe’s Calcitriol Capsules Market is driven by its aging demographic, with more than 20% of its population aged over 65. Countries like Germany, France, and Italy report a high prevalence of age-related bone disorders such as osteoporosis and osteomalacia, increasing the demand for calcitriol supplementation. Public healthcare initiatives promoting early diagnosis and preventive care have led to routine prescription of vitamin D analogs. In Germany, calcitriol capsules are often prescribed as part of dialysis regimens, especially in state-funded nephrology centers. The UK has seen a steady demand in both public NHS hospitals and private specialty clinics. Moreover, European regulatory agencies are focused on expanding access to generic alternatives, allowing cost-effective treatments. The region’s pharmaceutical players are also engaging in cross-border partnerships to streamline distribution and mitigate drug shortages across the EU.

Rapid Urbanization and Healthcare Infrastructure Spur Market Growth in Asia-Pacific

Asia-Pacific’s Calcitriol Capsules Market is witnessing significant momentum due to a surge in chronic disease cases and rising urban healthcare penetration. Countries like China and India are leading the charge, with rapidly increasing cases of chronic kidney disease and vitamin D deficiency. In China alone, over 10% of the adult population is believed to be suffering from varying stages of CKD. Increased healthcare investments, coupled with the expansion of generic drug manufacturing, have improved the affordability and accessibility of calcitriol capsules. In India, awareness campaigns and rural healthcare programs have helped broaden the prescription base. Meanwhile, Japan and South Korea have well-developed eldercare systems, where calcitriol is frequently used to manage bone mineral disorders. Market entry for foreign manufacturers is also easing with regulatory reforms across ASEAN nations, enabling a competitive and diverse product landscape.

Government-Supported Healthcare Access Enhances Growth Potential in South America

In South America, the Calcitriol Capsules Market is being shaped by increased government support for essential medications and a higher burden of kidney disorders. Brazil dominates the regional market, accounting for a substantial share due to its large patient population undergoing dialysis and its national health programs that subsidize calcitriol prescriptions. Argentina and Colombia have also witnessed a rise in osteoporosis and endocrine disorders, propelling demand in urban hospital networks. Moreover, regional pharmaceutical firms are expanding their presence with affordable generic options, improving market penetration across semi-urban and rural zones. Distribution through public and private channels has become more efficient post-COVID-19, with online pharmacies gaining momentum. Local contract manufacturing and favorable import-export policies are further supporting domestic and international product availability.

Chronic Disease Awareness and Import-Driven Markets Boost Regional Demand

The Middle East & Africa Calcitriol Capsules Market is primarily driven by increased awareness of kidney disease and bone health, especially in the Gulf countries and South Africa. The United Arab Emirates and Saudi Arabia lead in regional market share, supported by modern healthcare facilities and rising private sector investments. The region continues to rely heavily on imported calcitriol formulations, with most supply chains linked to European or Indian manufacturers. South Africa has also shown increased uptake of calcitriol for postmenopausal osteoporosis, especially through government-funded programs. Despite infrastructural limitations in parts of Sub-Saharan Africa, NGOs and international health collaborations have enhanced access to essential medications like calcitriol. The ongoing expansion of health insurance coverage across the Middle East is expected to further support future market growth.

United States - Holds the highest market share at USD 132.8 million in 2024 due to the high prevalence of CKD, strong healthcare infrastructure, and wide insurance coverage.

China - Ranked second with a market value of USD 84.5 million in 2024, driven by its large CKD population and growing demand for cost-effective vitamin D therapies.

The Calcitriol Capsules market features a competitive environment with several key players leading in innovation, product development, and distribution. Pfizer holds a strong position thanks to its well-established manufacturing network and wide clinical adoption across CKD and osteoporosis indications. Teva Pharmaceuticals is notable for its extensive portfolio of affordable generic calcitriol capsules, securing significant market share in cost-sensitive regions. Cardinal Health leverages its vast distribution infrastructure to ensure broad availability in hospital, pharmacy, and e-commerce channels. Roche also contributes through its strong presence in specialty clinics, particularly in hormone-related conditions. Other significant players such as Strides Pharma and Avet Pharmaceuticals offer region-specific strengths; for instance, Strides leads in India’s generic landscape, while Avet focuses on emerging markets. Specialty firms like Colmed International and Aphena Pharma streamline production of niche formulations for focused therapy segments. These players compete by optimizing manufacturing practices, investing in R&D for sustained-release variants, and reinforcing alliances with healthcare systems worldwide. As competition intensifies, partnerships and pipeline innovation will continue to shape the market’s landscape, ultimately benefiting end-users and patients.

Pfizer

Teva Pharmaceuticals

Cardinal Health

Roche

Colmed International

Aphena Pharma Solutions

Strides Pharma Science Limited

Avet Pharmaceuticals

Advancements in formulation and manufacturing technologies are enhancing the calcitriol capsules market. Smart process-control systems incorporating real-time analytics and sensor integration are minimizing batch failures and ensuring dosing precision. High-throughput screening, supported by AI, has accelerated solubility and excipient optimization—studies indicate such approaches can reduce formulation development timelines by nearly 40%. More recently, digital tableting platforms equipped with adaptive algorithms have enabled single-batch production of up to 1,440 capsules within 24 hours, using minimal active pharmaceutical ingredient, ideal for pilot-scale and personalized medicine applications. These systems link powder properties like flowability and porosity to tablet quality attributes, allowing dynamic process parameter adjustments.

In manufacturing, continuous encapsulation plants, where capsule filling, sealing, and coating occur in a nonstop sequence, are gaining traction for their ability to maintain consistent product quality and reduce contamination risk. These plants can quadruple throughput compared to batch methods while reducing waste by 25%.

Personalized medicine trends are reflected in small-scale "n-of-1" production runs enabled by miniaturized encapsulation units integrated with digital oversight. This allows creation of bespoke therapies at clinical sites, tracked through serialization and barcode systems to ensure dosing accuracy.

Moreover, manufacturers are testing polymer-based sustained-release coatings to achieve controlled calcitriol release over 12 to 48 hours. Early trials show these designs can maintain therapeutic serum levels with fewer daily doses, enhancing patient compliance and convenience.

In March 2025, New Zealand pharmacy authorities reported a supply disruption for 0.25 mcg and 0.5 mcg calcitriol capsules, prompting a temporary switch to EL‑branded alternatives from April 2025.

In July 2024, Canadian regulatory updates led to temporary importation of U.S.‑labelled calcitriol injection due to domestic shortages, ensuring continuity of therapy.

In June 2024, a UK biotech startup unveiled a pilot AI-driven microemulsion-based calcitriol capsule formulation that demonstrated a roughly 45% increase in systemic bioavailability in preclinical studies.

In May 2025, the FDA began internal deployment of generative AI tools—previously piloted—to accelerate review processes for new therapies, including advanced formulations like microemulsion capsules.

This Calcitriol Capsules Market Report delivers a comprehensive overview of the global active vitamin D capsule segment. It covers segment-level analysis by dosage strength (0.25 mcg, 0.5 mcg, others), therapeutic application (CKD, osteoporosis, hypoparathyroidism, etc.), and end-user channels (hospitals, retail and online pharmacies, specialty clinics). The report evaluates region-wise market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, reflecting both mature and emerging therapy environments. Competitive analysis includes leading pharmaceutical companies, their product pipelines, and marketing strategies. Additionally, the report examines technological innovations in formulation (e.g., sustained release, microemulsions), digital manufacturing platforms, and AI-enabled processes. Recent developments and supply chain disruptions are analyzed to highlight their impact on therapeutic availability. This report is intended for manufacturers, healthcare providers, policy makers, and market strategists seeking actionable insights into dosage trends, regulatory requirements, distribution channels, and long-term growth opportunities in the calcitriol capsules sector.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Calcitriol Capsules Market |

| Market Revenue (2024) | USD 456.2 Million |

| Market Revenue (2032) | USD 591.5 Million |

| CAGR (2025–2032) | 3.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GlaxoSmithKline plc, Pfizer, Teva Pharmaceuticals, Cardinal Health, Roche, Colmed International, Aphena Pharma Solutions, Strides Pharma Science Limited, Avet Pharmaceuticals, Sun Pharmaceutical Industries Ltd., Akorn, Inc., Cipla Ltd., Torrent Pharmaceuticals Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |