Reports

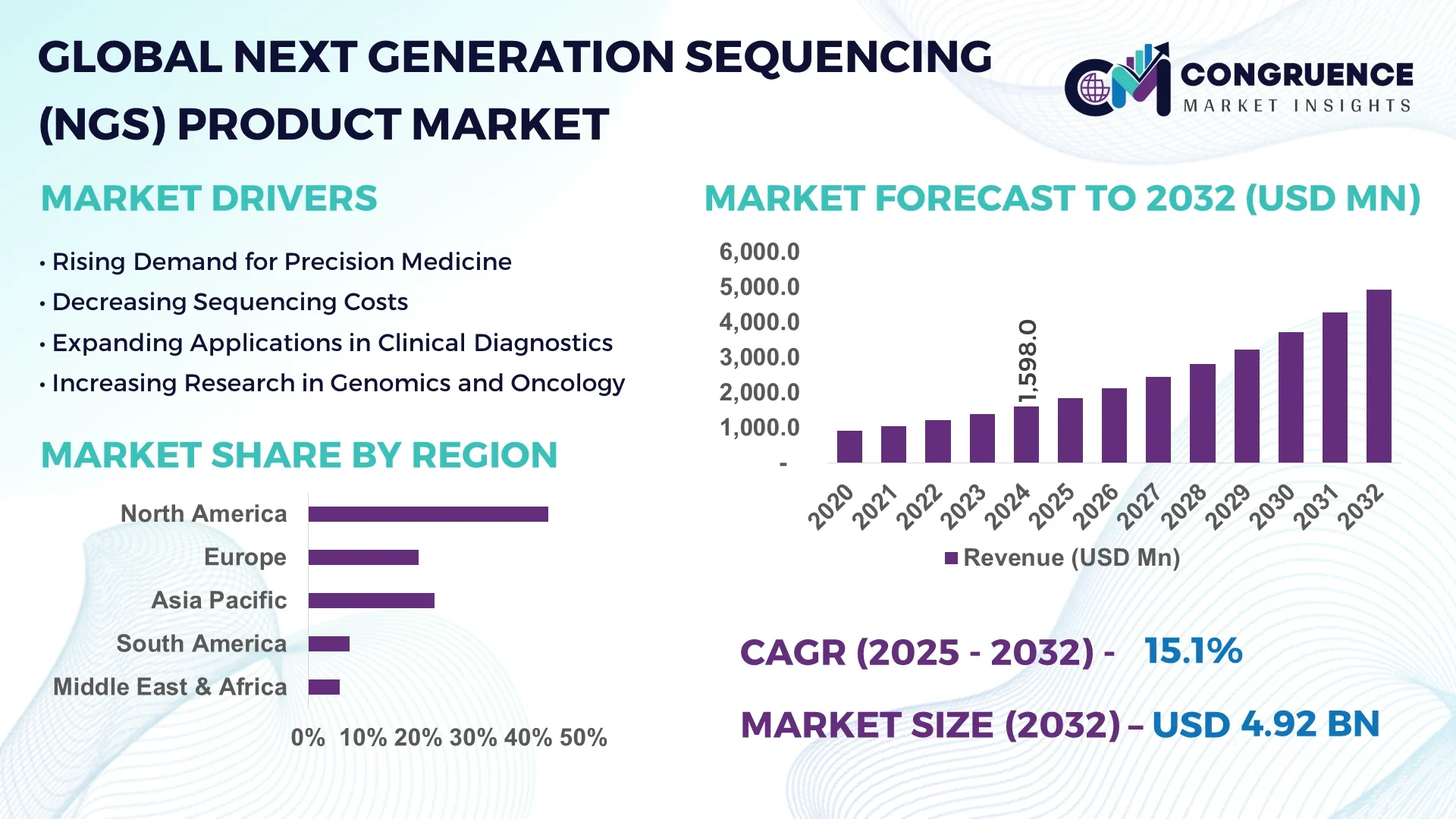

The Global Next Generation Sequencing (NGS) Product Market was valued at USD 1,598.0 Million in 2024 and is anticipated to reach a value of USD 4,922.4 Million by 2032 expanding at a CAGR of 15.1% between 2025 and 2032.

In 2024, the United States continues to dominate the Next Generation Sequencing (NGS) Product Market, with world-leading genomic research centers and large-scale sequencing initiatives driving demand for instruments, reagents, and consumables. The strong presence of major biotechnology hubs in California and Massachusetts supports rapid adoption of high-throughput NGS solutions, reinforcing the US position at the forefront of NGS innovation. Across the globe, advancements in sequencing chemistry, instrument miniaturization, and automation have accelerated product development cycles, propelling the NGS Product Market forward. Manufacturers are investing heavily in expanding NGS platforms, panel kits, and bioinformatics tools to meet growing demands from clinical diagnostics, precision medicine, and academic research institutions. The heightened focus on cost reduction and workflow efficiency continues to shape the Next Generation Sequencing (NGS) Product Market landscape in 2024 and beyond.

Artificial intelligence is revolutionizing the Next Generation Sequencing (NGS) Product Market by enabling smarter data interpretation, enhanced error correction, and automated workflow optimization. Advanced AI-driven algorithms now support real-time base calling, adjusting signal calibration on the fly to improve read quality and throughput. Machine learning models are being deployed to detect novel variants, reduce false positives, and annotate genomic regions with unprecedented accuracy. For example, deep learning tools integrated within sequencing software can automatically classify structural variations and rare mutations, reducing manual review time by over 50% in large-scale projects. AI-powered quality control modules continuously monitor sequencing runs, identifying potential issues with sample quality or reagent performance and proactively recommending corrective actions. This leads to significant reductions in instrument downtime and sample re-runs.

Additionally, AI-based predictive maintenance platforms now analyze instrument sensor data to forecast hardware failures up to two weeks in advance, enabling scheduled service and minimizing disruptions. Combined with cloud-based AI analytics pipelines, AI integration is transforming raw NGS output into actionable clinical insights more efficiently than traditional bioinformatics workflows. The result is accelerated turnaround times in clinical sequencing services, stronger confidence in variant calls, and streamlined R&D workflows across agrigenomics, oncology, and infectious disease applications.

“In early 2025, a leading sequencing instrument provider introduced AI-enabled signal processing that improved base call accuracy by 30%, reducing error rates in homopolymer regions markedly.”

The growing implementation of clinical genomic testing programs in hospitals and reference labs is driving higher adoption of NGS products. In 2024, more than 200 healthcare institutions globally initiated in-house NGS for oncology panels and inherited disease diagnosis. Laboratories are increasingly investing in mid- to high-throughput sequencers and associated consumables to meet rising patient testing volumes. This trend is particularly strong in pediatric rare disease testing, where faster diagnostic yields drive sequencing adoption. The Next Generation Sequencing (NGS) Product Market benefits significantly from these expanded clinical pipelines, as labs replenish reagent kits monthly and upgrade NGS platforms to support multiplexed test menus and larger sample throughput.

The significant capital expenditure required to acquire advanced NGS platforms remains a major market restraint. Entry-level sequencers can cost over USD 200,000, while high-throughput systems exceed USD 1 million. This high cost limits adoption among smaller research centers and in emerging markets. Additionally, the need for dedicated infrastructure such as clean rooms, IT storage, and trained technical staff further increases total cost of ownership. As a result, many institutions delay upgrades or continue using outdated platforms, slowing penetration of next-generation NGS products in mid-tier markets around the globe.

With growing healthcare infrastructure and increasing focus on genomics, emerging economies in Latin America, Southeast Asia, and Africa represent significant growth opportunities for the NGS Product Market. Governments in these regions are allocating funds toward precision medicine, with pilot programs deploying genomic sequencing for infectious disease surveillance and oncology profiling. As local institutions acquire benchtop NGS instruments and reagent supplies, global suppliers have an opportunity to establish distribution partnerships and training programs. This expansion could increase annual product revenues in these regions by over 15%, tapping into new customer segments and promoting wider adoption of NGS solutions.

Handling the massive volume of sequencing data generated by NGS instruments poses a significant challenge for laboratories. A single high-throughput run can produce over 1 terabyte of data, requiring scalable storage and robust data management solutions. Many labs struggle with on-premises infrastructure limitations, leading to bottlenecks in data transfer, processing, and long-term archival. This creates delays in bioinformatics pipelines and increases costs related to cloud storage and cybersecurity. Addressing this challenge requires NGS product providers to offer seamless end-to-end solutions that include data compression, encrypted storage, and integrated analytics platforms to support modern genomic workflows.

Surge in Portable and Real-Time Sequencing: Compact, handheld sequencers are transforming point-of-care applications in clinical and remote settings. These devices enable real-time sequencing during surgical procedures or field epidemiology, reducing turnaround times from days to hours. In 2024, portable sequencers were deployed in over 30 hospitals and mobile labs worldwide to support infectious disease surveillance, diagnostics, and environmental monitoring.

Growth of Long-Read Sequencing Platforms: Long-read NGS technologies are gaining traction due to their ability to resolve structural variants and repetitive genomic regions more effectively than short-read methods. More than 70 research labs globally added long-read capability in 2024, increasing demand for associated product kits and flow cells. This trend enhances applications in de novo genome assembly and complex disease genomics.

Rise of multiplexed Custom Panels: Customizable gene panels allow researchers and clinicians to create targeted sequencing assays tailored to specific disease signatures. In 2024, usage of customizable NGS panels grew by approximately 35% in clinical diagnostics laboratories. These panels require specific reagent trays and automated liquid handling products, boosting NGS consumable sales and supporting upselling of platform-specific offerings.

Expansion of End-to-End NGS Platforms with Built-In Analytics: Instrument vendors are offering fully integrated NGS solutions that include sequencers coupled with onboard analysis software and cloud-based pipelines. Over half of new NGS product launches in 2024 included bundled analytics, reducing time from data generation to interpretation. This trend simplifies product adoption for labs by reducing the need for separate bioinformatics investments and enhances platform lock-in through continuous software updates.

The Next Generation Sequencing (NGS) Product Market is segmented by type, application, and end-user. Each segment plays a critical role in shaping market dynamics, driven by technological advancement, expanding research initiatives, and clinical integration. By product type, the market includes consumables, platforms/instruments, and services. Consumables dominate due to recurring purchases tied to each sequencing run, while platforms are evolving rapidly with innovations in miniaturization and throughput. By application, oncology leads with the largest market share, propelled by the demand for tumor profiling and personalized cancer treatment. Infectious disease diagnostics and reproductive health testing are among the fastest-growing areas. By end-user, research institutions and academic labs hold a significant share, but clinical diagnostic laboratories are emerging as the fastest-growing segment due to the rising adoption of genomics in routine patient care. As precision medicine gains global traction, understanding these segmentation insights is crucial to identifying opportunities in the NGS Product Market landscape.

The NGS Product Market by type includes consumables, platforms/instruments, and services. Consumables are the leading segment, accounting for the majority of market share in 2024. This dominance stems from the need for regular and repeat purchases of reagent kits, flow cells, and sample prep materials with every sequencing run. Laboratories performing hundreds of sequencing assays per month generate strong demand for consumables, making this segment highly profitable. Platforms/instruments represent the second-largest share and continue to grow steadily due to increasing adoption of benchtop and high-throughput sequencers across both clinical and research labs. The fastest-growing segment is services, particularly data analysis and cloud-based bioinformatics. With increasing complexity of genomic data and limited in-house IT capabilities in many labs, outsourcing analysis to service providers is gaining popularity. Service-based offerings that include raw data conversion, variant calling, and annotation are seeing significant year-on-year growth. Vendors are also offering service bundles with instrument leasing to attract mid-tier buyers.

The application segmentation of the NGS Product Market includes oncology, inherited diseases, infectious diseases, reproductive health, agricultural and animal research, and metagenomics. Oncology dominates the market with the highest share, driven by the integration of NGS in tumor profiling, minimal residual disease detection, and therapy selection in both solid and hematologic malignancies. In 2024, over 60% of all clinical sequencing volumes globally were for oncology use cases. Infectious diseases represent the fastest-growing application, particularly due to real-time pathogen surveillance and outbreak management, including COVID-19 variants, monkeypox, and antimicrobial resistance tracking. Reproductive health, including non-invasive prenatal testing (NIPT) and preimplantation genetic testing (PGT), is another expanding segment as regulatory frameworks evolve to support clinical adoption. Although agricultural and environmental genomics is a niche, its applications in crop genome editing and soil microbiome analysis are gaining academic traction. The diverse and expanding range of applications positions NGS as a transformative force in healthcare and life sciences.

The key end-user segments in the NGS Product Market include academic and research institutions, clinical diagnostic laboratories, pharmaceutical and biotechnology companies, and hospitals. Academic and research institutions currently lead the market due to sustained funding from public and private sources, which supports large-scale genomic projects and fundamental research. These institutions often operate high-throughput platforms and contribute significantly to consumables demand through continuous experimentation. Clinical diagnostic laboratories are the fastest-growing segment, with a surge in adoption of NGS-based testing panels for oncology, infectious diseases, and hereditary conditions. Advancements in regulatory approvals and validation protocols are easing the clinical adoption process. Pharmaceutical and biotechnology companies are leveraging NGS in drug discovery, pharmacogenomics, and biomarker development, further expanding their contribution to market revenue. Hospitals, especially those with advanced pathology departments, are increasingly integrating NGS to provide personalized treatment plans. The cross-sectoral adoption of NGS technologies reflects the growing maturity and essential utility of sequencing across healthcare ecosystems.

North America accounted for the largest market share at 43.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.7% between 2025 and 2032.

The dominance of North America stems from early adoption of NGS technologies, high R&D spending, and the presence of major industry players. The U.S. leads due to strong government genomics initiatives, a matured diagnostic ecosystem, and a vast base of precision medicine adopters. Meanwhile, Asia-Pacific is rapidly scaling its capabilities in clinical genomics, largely due to increasing investments in healthcare infrastructure and genomic sequencing hubs across China, India, Japan, and South Korea. The region's growing population, rising chronic disease burden, and government-led precision health projects are creating robust growth prospects. Europe maintains a significant market position through pan-EU genomic strategies, while South America and the Middle East & Africa are emerging steadily with localized adoption trends and capacity-building programs.

Clinical Integration and Oncology Research Fuel Market Expansion

North America continues to dominate the NGS Product Market due to its well-established genomics ecosystem and robust healthcare funding. In 2024, the U.S. alone contributed over USD 580 million in NGS product revenue, driven largely by widespread application in cancer diagnostics and monitoring. Several large-scale cancer genomic initiatives, such as those by leading cancer centers and national health agencies, support the use of NGS panels in routine oncology workflows. Additionally, Canada is investing in population genomics and rare disease diagnostics, which is driving increased utilization of sequencing platforms and consumables. The market also benefits from partnerships between biotech firms and research institutions to develop novel sequencing tools and panels. Accelerated regulatory approvals for clinical-grade NGS tests are pushing laboratories and hospitals to adopt sequencing-based diagnostics. The expansion of clinical exome sequencing and whole genome sequencing services is further enhancing the regional market footprint.

Regulatory Support and Biobank Initiatives Drive Regional Growth

Europe holds a strong share in the NGS Product Market, supported by government-funded genomic projects, a favorable regulatory environment, and an extensive network of biobanks and academic research centers. In 2024, the region’s market revenue reached approximately USD 340 million, with the UK, Germany, and France leading adoption. The UK’s Genomics England project continues to boost demand for sequencing products in rare disease and oncology applications. Germany has invested heavily in hospital-based genomic diagnostics under its health digitization efforts. The implementation of EU-wide guidelines for clinical genomic testing has accelerated the integration of sequencing platforms in diagnostic workflows. Furthermore, the rise in personalized medicine programs and collaborative research across borders is increasing demand for sequencing services and consumables. Europe is also emerging as a key exporter of sequencing-based clinical trial services, boosting regional product adoption.

Government Funding and Rapid Infrastructure Expansion Propel Market Growth

Asia-Pacific is the fastest-growing region in the NGS Product Market due to aggressive government investments and an expanding base of NGS service providers. In 2024, the market revenue from this region crossed USD 270 million, with China, Japan, and India spearheading growth. China’s “Precision Medicine Initiative” and rising domestic production of sequencing platforms have made it a leading NGS consumer. Japan's focus on rare disease diagnostics and hereditary cancer screening is creating new use cases. India is also investing in genomic databases and public-private genomics labs, supporting local sequencing service development. Across the region, increasing public health awareness and reduced sequencing costs have driven higher adoption of NGS in infectious disease surveillance, reproductive health, and oncology. Multinational NGS companies are expanding their footprint in Asia by setting up R&D and distribution hubs, making products more accessible and cost-effective.

Emerging Adoption in Public Healthcare and Academic Research

South America is gradually gaining momentum in the NGS Product Market, with Brazil and Argentina leading the charge. In 2024, the market size in the region surpassed USD 85 million. Brazil’s public healthcare system is incorporating NGS-based diagnostics into its cancer and rare disease programs. Academic institutions and hospitals are increasingly participating in international genomic research, driving local demand for sequencing reagents and instruments. Argentina is investing in genomics for agricultural biotechnology and pathogen research. While the market is in a developmental stage, the presence of government-sponsored initiatives and improving reimbursement models is encouraging new entrants and service providers. Language-localized sequencing platforms and rising partnerships with global genomic players are accelerating market accessibility. The demand for cost-effective sequencing solutions is particularly high in public and university-affiliated laboratories.

Capacity Building and Rare Disease Focus Catalyze Market Activity

The Middle East & Africa region is witnessing growing adoption of NGS technology, particularly in the UAE, Saudi Arabia, and South Africa. In 2024, the regional market reached a valuation of around USD 58 million. The UAE’s national genomics program is focused on building a large-scale genetic reference database for its population, creating demand for sequencing systems and consumables. Saudi Arabia is investing in genome centers to address inherited disease prevalence. In Africa, the use of NGS for studying endemic infectious diseases and conducting pathogen surveillance is gaining traction. Academic collaborations with global research institutions have improved access to sequencing training and infrastructure. Although the region faces challenges such as high costs and limited bioinformatics support, initiatives from ministries of health and international funding agencies are helping expand NGS accessibility and literacy among healthcare professionals.

United States – values at USD 580+ Million, due to widespread clinical and research applications of NGS across oncology, infectious diseases, and hereditary conditions.

China – values at USD 210+ Million, is driven by national precision medicine programs, domestic NGS instrument production, and large-scale sequencing projects.

The Next Generation Sequencing (NGS) Product Market remains intensely competitive, with several major players investing heavily in innovation, acquisitions, and strategic alliances. Illumina leads in terms of installed base for high-throughput and benchtop systems, regularly launching instruments like the MiSeq i100 Series optimized for sustainability and streamlined workflows. BGI and Complete Genomics are recognized for offering cost-effective sequencing platforms tailored toward large-scale genomics projects, especially in Asia. Companies like Oxford Nanopore bring disruptive long-read and portable sequencing solutions with improving accuracy powered by AI-based basecalling. Sophia Genetics, although focused on bioinformatics, commands a strong position with its AI-driven analysis platform and over 2 million genomic profiles processed. Qiagen has integrated AI into its clinical insight tools, while Nvidia’s Parabricks enables GPU-accelerated variant processing, empowering labs with faster bioinformatics pipelines. New entrants, including GenBio AI, are pushing boundaries with advanced AI frameworks for molecule-level analysis. Consolidation is common—such as Illumina's acquisition of Fluent BioSciences—making competitive differentiation increasingly reliant on AI, integrated analytics, lower per-base costs, and end-to-end services. The dynamic environment fosters continuous product enhancements, pricing competition, and collaborations, driving rapid evolution of the NGS landscape.

Illumina

BGI (BGI Genomics / Complete Genomics)

Oxford Nanopore Technologies

Sophia Genetics

Qiagen

Nvidia Parabricks

GenBio AI

Innovations in sequencing technology continue to shape the NGS market’s trajectory. Short-read sequencers dominate in cost-efficiency and accuracy, catering primarily to clinical and academic users. Long-read sequencing platforms, like those from Oxford Nanopore, now leverage machine learning-enhanced basecalling to address previously challenging genomic regions and structural variants. Portability and speed are also advancing; Complete Genomics launched the AI-enhanced DNBSEQ‑E25 Flash, capable of rapid, high-precision runs in under two hours using CMOS flow cells—and replicable in field settings. AI-accelerated variant calling frameworks, such as Nvidia Parabricks, allow GPU-optimized pipelines to process terabytes of data in hours rather than days, with compliance for germline and somatic mutation detection. On-device basecalling accelerators like CiMBA handle ~4.77 million bases per second with drastically reduced power and improved efficiency. In clinical bioinformatics, platforms like PromoterAI by Illumina can interpret noncoding genomic regions, increasing rare disease diagnostic rates by approximately 6%. GenBio AI’s foundational models (e.g., AIDO-DNA/RNA) are being deployed for molecular-level data interpretation. Across the ecosystem, seamless integration of advanced chemistry, hardware, and AI-powered analytics is propelling the market into the era of precision, speed, and scalability.

In August 2024, BioAro launched PanOmiQ, an AI-driven whole-genome sequencing analysis tool that achieved a perfect 100% match in variant calling during CAP proficiency testing.

In June 2024, Illumina introduced the MiSeq i100 Series, featuring a 35% reduction in climate impact through sustainable reagent packaging and improved run efficiency.

In May 2025, Illumina unveiled PromoterAI, a deep learning tool that identifies pathogenic noncoding variants, estimating its contribution to rare disease diagnosis at around 6% of cases.

In March 2025, Sophia Genetics announced reaching 2 million genomic profiles analyzed using its SOPHiA DDM AI-platform, underscoring its leadership in data-driven genomics.

The scope of the NGS Product Market Report encompasses the full spectrum of sequencing solutions and services, including instruments (benchtop to high-throughput), consumables (reagents, flow cells, library prep kits), and integrated bioinformatics platforms. It also covers AI-enhanced analysis tools, quality-control software, and cloud-based pipelines used across clinical, research, and commercial applications. Product coverage extends to short-read, long-read, and targeted panels, with attention to sustainability, reagent cost per sample, and throughput scalability. Geographically, the report assesses market penetration across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, including regional infrastructure and policy environments. Key end users analyzed include diagnostic labs, hospitals, pharma/biotech, and academic research centers. The report addresses emerging use cases like infectious disease surveillance, oncology panels, NIPT, microbiome research, and agricultural genomics. It also explores the impact of regulatory frameworks, reimbursement environments, and technology trends such as on-device basecalling, GPU-accelerated pipelines, AI variant classification, and portable sequencing. This expansive perspective captures current and future directions driving value, accessibility, and clinical integration of NGS products.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Next Generation Sequencing (NGS) Product Market |

| Market Revenue (2024) | USD 1,598.0 Million |

| Market Revenue (2032) | USD 4,922.4 Million |

| CAGR (2025–2032) | 15.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Illumina, Thermo Fisher Scientific, BGI (BGI Genomics / Complete Genomics), Pacific Biosciences, Agilent Technologies, F. Hoffmann-La Roche Ltd., Oxford Nanopore Technologies, Sophia Genetics, Qiagen, Nvidia Parabricks, GenBio AI, PerkinElmer |

| Customization & Pricing | Available on Request (10% Customization is Free) |