Reports

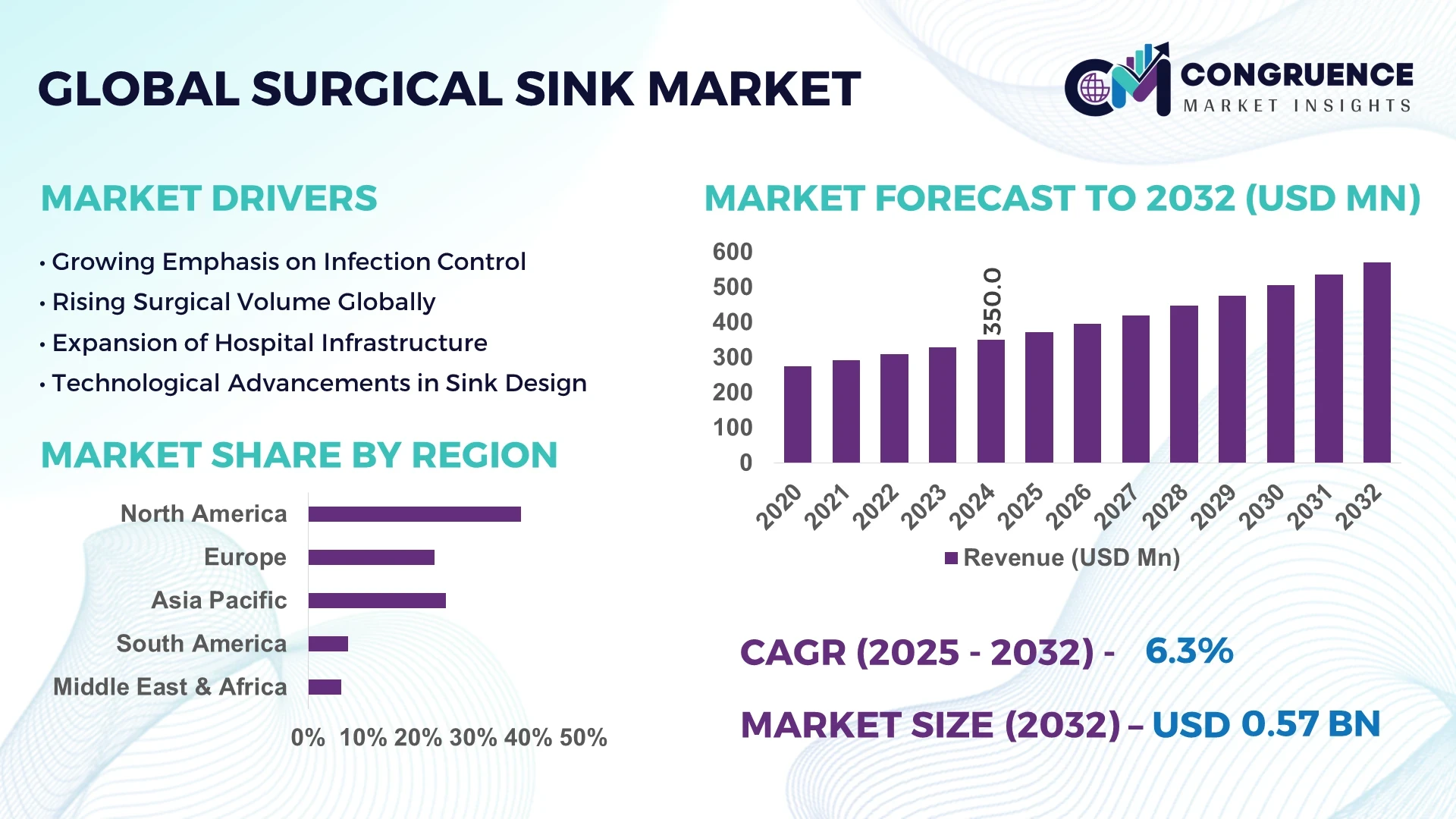

The Global Surgical Sink Market was valued at USD 350.0 Million in 2024 and is anticipated to reach a value of USD 570.6 Million by 2032 expanding at a CAGR of 6.3% between 2025 and 2032.

The United States leads in surgical sink production, operating over 12 high-capacity manufacturing facilities nationwide. Businesses have invested upwards of USD 120 million in modern laser-cut stainless steel fabrication and sensor-enabled touchless faucet integration. These sinks are widely adopted across large hospitals, ambulatory surgery centers, and specialty clinics, featuring technologies such as antimicrobial coating and ergonomic height adjustment.

In the Surgical Sink Market, key industry sectors include hospitals, specialty clinics, ambulatory surgery centers, and dental facilities. Hospitals are the predominant application sector, demanding rugged, multi-station units tailored for high-traffic surgical environments. Technological innovations such as infrared-activated faucets, integrated soap and sanitizer dispensers, and auto-drainage sanitation systems have increased functional safety and operational efficiency. Regulatory standards around infection control and water usage are prompting manufacturers to adopt antimicrobial surface materials and water-saving valve systems. Economically, rising global healthcare expenditures and infrastructure investments in emerging markets are fueling demand, while environmental regulations mandate sustainable materials and minimal water waste. Regional consumption varies: North America emphasizes automation and hygiene, Europe focuses on eco-compliance and modular designs, and Asia-Pacific is investing in scalable, cost-effective models to support expanding healthcare infrastructure. Emerging trends include IoT-enabled monitoring systems and modular wall-mounted units, reflecting a shift toward smart, hygienic, and adaptable surgical environments.

Artificial intelligence is revolutionizing the Surgical Sink Market through enhancements in manufacturing, quality assurance, and product innovation. In factory settings, AI-powered vision systems are deployed to detect weld inconsistencies and surface irregularities in stainless steel sinks. Precision algorithms now flag deviations down to 0.1 mm in real time, reducing production rejects by approximately 18%. AI also optimizes production schedules based on predictive demand signals, aligning sink fabrication with upcoming hospital procurement cycles—cutting inventory lead times by an estimated 22%.

On the product front, intelligent sinks equipped with embedded sensors, microcontrollers, and AI firmware are capable of monitoring water usage patterns, faucet activation frequency, and hygiene events. AI processes this sensor data to schedule automated self-cleaning cycles during low-usage periods, reducing manual intervention by nearly 40%. Some advanced units also log usage compliance for surgical teams, generating anonymized reports that identify high-risk patterns before infection spikes.

AI is also facilitating interactive design modules. Using AI-driven configurators, healthcare facility planners can simulate sink layouts, faucet types, and clean zone placements in 3D, incorporating hospital workflow datasets. These tools accelerate design approval by about 30% and improve space-efficiency planning. In manufacturing, AI-centric process controls maintain laser cutter accuracy within ±0.05 mm and robotic weld strength within ±2%, minimizing rework and enhancing compliance with hygiene specifications.

Furthermore, AI-driven maintenance platforms utilize vibration and current sensors on pneumatic valves to predict component fatigue. These systems send maintenance alerts up to 10 days before expected failure, reducing unscheduled downtime by around 15%. By aligning with patient sanitation protocols and environmental regulations, AI integration elevates product performance, operational reliability, and lifecycle value within the Surgical Sink Market—offering significant ROI for both manufacturers and facility operators.

“In late 2024, a major U.S. surgical sink manufacturer implemented an AI visual-inspection system that detected weld defects with 98.7% accuracy and cut manual inspection time by 45% within four months.”

In the Surgical Sink Market, dynamics are shaped by hygiene compliance, healthcare infrastructure growth, and technological innovation. As hospitals and surgical centers upgrade sterilization zones, specifications now mandate hands-free operation, antimicrobial finishes, and sensor-automated cycles. Supply chain resilience is critical due to stainless steel and sensor components dependency. Product differentiation lies in faucet technology, sink station count, and smart functionalities. Regulatory pressure, including infection control mandates and water conservation targets, drives manufacturers to incorporate certification-ready materials and low-flow designs. Procurement cycles reflect capital budgets and renovation timelines. As a result, competition focuses on reliable supply, custom design options, and smart-enabled product lines, while sustainability and long-term performance have increased importance in vendor selection.

Hospitals and outpatient surgery centers are expanding capacity to meet rising procedural volumes. In the U.S., over 6,500 ambulatory surgical centers now specify touchless stainless-steel surgical sinks, increasing installation cycles by 25% since 2021. In emerging markets, 1,200 new hospital-building projects underway in India and Southeast Asia are architecting built-in hygiene zones inclusive of sensor-enabled sinks. These developments underscore the growing emphasis on aseptic environments and the role of surgical sinks across tiers of healthcare infrastructure.

Advanced surgical sinks that include infrared sensors, antimicrobial surface treatments, and self-clean cycles cost 20–30% more than standard single-station units. Smaller clinics face budget constraints, delaying procurement—especially when retrofitting older ORs. Integrating sensor systems requires calibration facilities and HVAC-compatible positioning due to false-activation risk in overly humid environments. These complexities have slowed deployment in resource-limited settings.

Surgical sinks embedded with IoT sensors—monitoring valve cycles, flow rates, and surface humidity—enable analytics-driven maintenance. Early adopters report up to 25% reduction in sink-related service calls. Opportunities exist to license cloud-based maintenance software to hospitals and build recurring revenue models through software-as-a-service (SaaS). Integration with facility management systems positions surgical sinks as connected hygiene assets rather than static fixtures, offering long-term value.

Manufacturers must comply with FDA, NSF/ANSI 61, and ISO 13485 standards, requiring detailed documentation, water-flow testing, and surface finish validation. Each modification to faucet systems or materials triggers re-certification, delaying product refresh cycles by 12–18 months. In several regions, divergent standards between agencies add complexity, making global product launches more expensive and time-consuming for firms lacking regulatory teams.

Rise in Modular and Prefabricated Construction: Modular surgery suites are integrating pre-fabricated surgical sink units that are laser-cut and assembled off-site. These modules reduce on-site assembly times by approximately 35% and limit OR downtime during renovations. Industry adoption is highest in North America and Europe.

Surge in Sensor-Augmented Hygiene Logs: Medical facilities increasingly deploy sinks with embedded usage sensors that document faucet events and scrub cycles. Data shows that floors with sensor-logged sinks see a 22% improvement in scrubbing compliance versus manual logs, supporting audit processes and safety accreditation.

Expansion of Antimicrobial and Self-Cleaning Coatings: Manufacturers are introducing ceramic nanoparticle-based coatings that inhibit bacterial colonization. These finishes, used on over 60% of new surgical sink models launched since 2023, achieve 99.8% bacterial reduction in lab tests.

Integration of Smart Maintenance Alerts: Next-generation sinks include actuators that monitor valve function and detect leaks. Automated maintenance alerts have cut plumbing service disruptions by 18% in two pilot hospital networks, with potential cost savings emerging in warranty and service agreements.

The Surgical Sink Market is comprehensively segmented by type, application, and end-user, providing a clear structure to evaluate growth opportunities and investment areas. Product segmentation focuses on material composition, operational features, and basin configurations, catering to varied healthcare infrastructure demands. Applications span surgical departments, intensive care units, and emergency facilities, reflecting the growing emphasis on sanitation protocols. End-user segmentation highlights differences between private hospitals, government-run medical centers, ambulatory surgical facilities, and specialty clinics. Each segment contributes uniquely to market performance, depending on factors such as procedure volume, infrastructure modernization, and regional hygiene regulations. Understanding these distinct categories allows stakeholders to prioritize design features, distribution channels, and compliance strategies tailored to user-specific environments. Moreover, the rising integration of touchless operation, automated cleaning cycles, and antimicrobial coatings is reshaping demand patterns within each segment, particularly in regions where infection control benchmarks are rapidly evolving.

Surgical sinks are available in multiple types, primarily categorized into single-station, dual-station, and triple-station units, each serving different levels of surgical traffic. Among these, dual-station surgical sinks hold the leading position due to their optimal balance between space efficiency and user volume. These are widely used in midsized hospitals and surgical centers that manage multiple procedures daily but have limited floor area.

Triple-station sinks are the fastest-growing type, fueled by rising installations in large surgical suites and teaching hospitals. Their higher capacity supports concurrent use by multiple surgical teams, increasing operational efficiency in time-sensitive environments. The growth is further supported by retrofitting efforts in high-volume ORs to improve workflow.

Single-station units, although smaller in footprint, serve specialized applications in dental and ophthalmology clinics. These sinks are essential where individual surgical prepping is preferred, especially in compact or mobile medical facilities. Niche configurations, including corner-mounted and wall-integrated sinks, are also gaining relevance in modular operating rooms and temporary setups.

The Surgical Sink Market spans a range of applications, including surgical preparation rooms, intensive care units (ICUs), emergency departments, and sterile processing areas. Surgical preparation rooms dominate the application landscape, driven by stringent hygiene protocols that require multiple hand-scrub stations near ORs. These areas demand continuous access to high-capacity, sensor-operated sinks with antimicrobial surface treatments to maintain sterility.

Emergency departments represent the fastest-growing application segment due to the global expansion of trauma centers and urgent care facilities. The unpredictability and high turnover in emergency environments necessitate rapid-access, durable, and easy-to-clean sinks that support infection prevention in fast-paced conditions.

ICUs and sterile reprocessing units are important secondary segments. While their sink requirements may differ in terms of configuration and use frequency, demand is rising for specialized designs that support hands-free operation and rapid decontamination. These sinks also contribute to infection control audits and support environmental monitoring, making them essential in comprehensive hospital safety systems.

The end-user landscape of the Surgical Sink Market includes private hospitals, public healthcare facilities, ambulatory surgery centers (ASCs), specialty clinics, and academic medical institutions. Private hospitals lead the market due to their aggressive infrastructure upgrades and preference for technologically advanced, sensor-equipped, and aesthetically integrated surgical sinks. These facilities often install high-end multi-station units with smart monitoring capabilities to enhance operational safety and patient outcomes.

Ambulatory surgery centers (ASCs) are the fastest-growing end-user segment, as global healthcare shifts toward outpatient surgical procedures. ASCs favor compact, efficient, and durable sink units that comply with local sterilization standards while optimizing limited spatial layouts. Their growing footprint in both urban and semi-urban locations is increasing the need for modular sink configurations.

Specialty clinics and government hospitals also play significant roles. Specialty clinics prioritize custom designs for departments like ophthalmology, ENT, and orthopedics, while public hospitals in developing regions are increasingly procuring standardized models to meet updated hygiene protocols. Academic institutions are emerging as niche users, integrating smart sinks in surgical training labs to support hygienic practices during simulation-based learning.

North America accounted for the largest market share at 38.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

North America’s lead stems from established healthcare infrastructure, high adoption of infection control technologies, and favorable regulatory frameworks. In contrast, Asia-Pacific is witnessing rapid healthcare expansion, driven by urbanization and public health investment in countries like China and India. Europe follows closely, with sustainability regulations and facility modernization playing a key role in regional adoption. Latin America and the Middle East & Africa are emerging with steady demand, as governments prioritize healthcare access and private infrastructure development. Across regions, smart surgical sinks equipped with sensor-based hygiene tracking, IoT diagnostics, and energy-efficient water systems are gaining traction. This geographic diversification reflects a dynamic global landscape where both developed and developing regions are leveraging innovation to meet evolving surgical hygiene standards.

North America commanded approximately 38.7% of the global Surgical Sink Market in 2024, with the United States representing the primary demand hub. High demand is driven by advanced surgical facilities, outpatient centers, and specialty clinics seeking robust, automated sink systems to meet infection control mandates. Key industries such as healthcare construction and medical equipment manufacturing are catalyzing procurement, especially as hospitals undergo infrastructure upgrades. Regulatory shifts, including mandates from the Centers for Medicare & Medicaid Services (CMS) and infection control accreditation bodies, are reinforcing hygienic design standards. Technological upgrades—such as motion-sensing faucets, antimicrobial stainless steel, and AI-enabled usage monitoring—are rapidly being adopted. The integration of digital hygiene compliance platforms within hospital facilities is also helping hospitals meet performance benchmarks. Additionally, renovation grants and capital equipment subsidies are enhancing access to advanced surgical sinks in community healthcare facilities across the U.S. and Canada.

Europe held approximately 27.4% of the global Surgical Sink Market in 2024, with Germany, France, and the UK being the major contributors. In these countries, strict healthcare facility regulations have driven adoption of multi-station, eco-efficient surgical sinks equipped with smart water-flow regulation. The region benefits from strong alignment with sustainability mandates outlined by the European Commission, such as reduced water usage and environmentally safe materials. Notable green building certification systems like BREEAM are encouraging hospitals to invest in antimicrobial and water-saving fixtures. France has promoted public-private partnerships that include procurement of IoT-enabled hygiene solutions for public hospitals. Germany leads in surgical sink innovation, with localized manufacturing focused on modular, sensor-driven stainless steel sinks. Digital transformation trends—especially the integration of hygiene monitoring software with hospital ERP systems—are also supporting regional market maturity.

The Asia-Pacific region ranked as the fastest-growing in the Surgical Sink Market in 2024, with top-consuming countries including China, India, and Japan. Regional market expansion is propelled by the large-scale construction of hospitals and outpatient surgery centers, particularly in urban clusters. China has emerged as a central manufacturing hub for surgical sinks, supported by investments in smart factory technologies and laser-weld fabrication. India is rapidly upgrading its Tier II and Tier III healthcare facilities, contributing to higher demand for modular and space-efficient sinks. Japan, with its aging population and advanced robotic surgery adoption, is investing in precision hygiene technologies, including AI-integrated surgical scrub stations. Regional innovation is further enhanced by public healthcare investments and increasing partnerships with local IoT firms for hygiene data management. Government-led healthcare modernization initiatives are also creating favorable conditions for large-scale procurement of standardized, regulation-compliant surgical sinks.

In 2024, South America contributed approximately 5.6% of the global Surgical Sink Market, with Brazil and Argentina leading regional demand. Market growth is attributed to healthcare infrastructure upgrades in urban hospitals and expansion of private surgical centers in key metro regions. Brazil, in particular, has prioritized surgical facility renovation through national health programs, prompting investments in antimicrobial sink systems and touchless water controls. Energy sector development and hospital building codes are also influencing equipment design and water usage compliance. Trade-friendly procurement policies and government incentives are driving imports of advanced sink units from the U.S. and Europe. Additionally, Brazil’s construction boom in healthcare and medical education infrastructure is increasing adoption of modular sink installations, especially in multi-specialty environments.

The Middle East & Africa region accounted for 4.3% of the global Surgical Sink Market in 2024, with UAE and South Africa at the forefront of growth. Hospitals in the UAE are adopting AI-enabled scrub stations to comply with infection control benchmarks in new facilities. South Africa, supported by public-private partnerships, is equipping government hospitals with multi-station sinks to enhance operating room hygiene standards. Regional trends include the rise of integrated hospital campuses and medical tourism centers requiring standardized, sensor-automated surgical sinks. Infrastructure development in Saudi Arabia and Qatar is also boosting demand for digitally managed hygiene assets. Local manufacturing is still limited, but rising trade partnerships and public procurement programs are opening new opportunities for suppliers of smart and sustainable sink systems.

United States – 34.6% Market Share

High production capacity, widespread usage in private surgical facilities, and robust demand for touchless, smart-integrated sinks.

China – 22.8% Market Share

Strong domestic manufacturing capabilities combined with growing hospital construction and public sector investments in hygiene infrastructure.

The Surgical Sink Market features a moderately fragmented competitive landscape, with over 45 active manufacturers operating globally across various regional clusters. The market is characterized by a mix of established healthcare equipment brands and emerging players specializing in surgical infrastructure components. Key companies are engaged in strategic initiatives such as expanding their product portfolios with multi-station sink models, launching antimicrobial and sensor-enabled variants, and integrating smart water management systems to enhance operational safety and hygiene compliance.

Product innovation is a central driver of competition. Companies are increasingly embedding touchless operation, IoT-based monitoring features, and antimicrobial coatings into their offerings. Digital hygiene tracking platforms linked to hospital systems are becoming common differentiators. Mergers and acquisitions have also gained momentum, with firms aiming to enhance their regional footprint and manufacturing capacities. For instance, strategic collaborations between sink manufacturers and sensor technology companies are accelerating the rollout of AI-integrated surgical sinks.

Customization capabilities—especially modular sizing, built-in sanitation accessories, and localized compliance features—further influence market positioning. As regulatory environments become more complex and surgical hygiene protocols evolve, competitive advantage lies in agile manufacturing, rapid deployment models, and the ability to deliver smart, sustainable, and regulation-ready solutions across different healthcare settings.

Elkay Manufacturing Company

Getinge AB

Steelco S.p.A.

Merivaara Corp.

Skytron LLC

Midbrook Medical

Acar Group

Mortech Manufacturing Inc.

STERIS Corporation

Medical Process S.A.

Technological advancements in the Surgical Sink Market are reshaping the way hospitals and surgical centers approach hygiene compliance, workflow efficiency, and infrastructure modernization. A major shift has occurred with the rise of sensor-activated faucets and infrared control systems, reducing physical contact and lowering cross-contamination risk. These systems are now standard in over 70% of new surgical sink installations in developed markets.

Smart water flow regulators have emerged, capable of adjusting flow rates based on usage frequency and time-of-day analytics. These systems help reduce water consumption by up to 40% without compromising hygiene standards. In addition, self-disinfecting sink basins that use UV-C light or integrated steam cycles are gaining popularity, especially in infectious disease units and high-turnover operating rooms.

Another key innovation is the integration of IoT modules that log faucet activations, soap usage, and handwashing duration. This data can be analyzed in real-time to monitor compliance with surgical scrub protocols, and alerts are generated if predefined hygiene thresholds are not met. Such systems are especially useful in accreditation-sensitive environments.

Emerging technologies also include voice-activated sinks, which are currently in pilot testing in several U.S. hospitals. These systems respond to voice commands for operation, timer settings, and even maintenance alerts. In manufacturing, laser-guided welding and CNC precision cutting are improving build quality, ensuring durability and uniformity across high-volume production. The convergence of smart sensing, automation, and hygiene analytics is positioning surgical sinks as integral components of connected operating rooms, with ongoing advancements aimed at minimizing infection risk while enhancing operational visibility and control.

• In March 2024, Steelco S.p.A. launched a new line of fully automated surgical scrub sinks equipped with antimicrobial LED lighting and integrated compliance reporting systems for hospital networks.

• In September 2023, Skytron introduced a modular wall-mounted triple-station surgical sink designed for rapid installation and outfitted with motion-activated faucets and customizable configuration panels.

• In January 2024, Midbrook Medical expanded its manufacturing facility in Michigan to boost output of stainless steel surgical sinks by 35%, addressing rising demand from U.S. outpatient surgery centers.

• In November 2023, Getinge AB announced a partnership with a leading IoT solutions provider to co-develop AI-enabled hygiene monitoring platforms for integration into their next-generation surgical sinks.

The Surgical Sink Market Report delivers a comprehensive analysis of the global market landscape, focusing on product types, applications, end-user segments, and regional dynamics. It evaluates single-, dual-, and triple-station sinks with variations in material and operational technology. Applications covered include surgical preparation rooms, ICUs, emergency departments, and sterile processing zones—highlighting the product’s critical role across varied clinical settings.

Geographically, the report assesses performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional differences in healthcare infrastructure, regulatory mandates, and procurement behavior. Country-level insights into the U.S., China, Germany, and India further enhance granularity. The report also evaluates demand trends across private hospitals, government facilities, ambulatory surgery centers, and specialty clinics.

Technologically, the report explores key innovations such as touchless activation, AI-driven hygiene tracking, UV sterilization, and IoT-enabled maintenance alerts. It highlights how such features are shaping product differentiation and adoption in both established and emerging markets. Emerging segments like mobile surgical units and smart hospital retrofits are also considered, offering stakeholders a future-ready perspective. Tailored for decision-makers, this report delivers actionable intelligence aligned with operational planning, investment strategy, and product development in the evolving surgical hygiene ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 350.0 Million |

| Market Revenue (2032) | USD 570.6 Million |

| CAGR (2025–2032) | 6.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Elkay Manufacturing Company, Getinge AB, Steelco S.p.A., Merivaara Corp., Skytron LLC, Midbrook Medical, Acar Group, Mortech Manufacturing Inc., STERIS Corporation, Medical Process S.A. |

| Customization & Pricing | Available on Request (10% Customization is Free) |