Reports

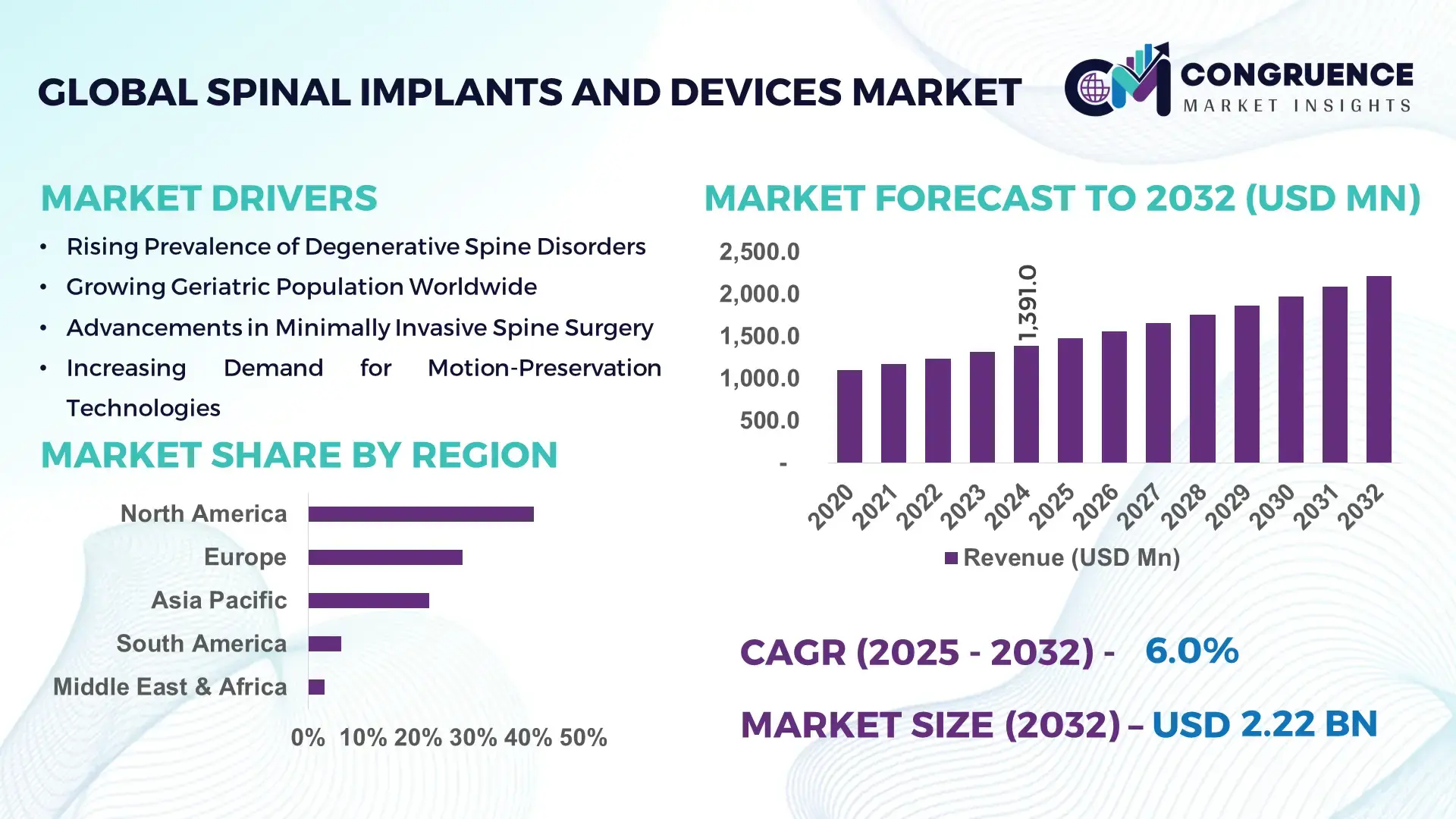

The Global Spinal Implants and Devices Market was valued at USD 1,391.0 Million in 2024 and is anticipated to reach a value of USD 2,217.0 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032, according to an analysis by Congruence Market Insights, driven by increasing surgical volumes for degenerative spine disorders and rapid adoption of minimally invasive spinal technologies.

The United States represents the dominant country in the global spinal implants and devices landscape, supported by advanced manufacturing capacity, strong capital investment, and high procedural volumes. The country performs over 1.6 million spinal procedures annually, supported by more than 6,000 specialized spine centers and tertiary hospitals. Domestic production accounts for a significant proportion of high-end spinal fixation systems, motion-preservation implants, and biologics, with manufacturers investing over USD 2.5 billion annually in spine-focused R&D. Robotic-assisted spine surgery is deployed in more than 35% of large U.S. hospitals, while 3D-printed patient-specific implants have crossed 18% adoption in complex deformity cases. The U.S. also leads clinical trials for next-generation spinal implants, hosting over 40% of global spine-related medical device trials, reinforcing its position as a technology and innovation hub.

Market Size & Growth: Valued at USD 1,391.0 Million in 2024, projected to reach USD 2,217.0 Million by 2032 at a 6.0% CAGR, supported by rising spinal surgery volumes and technology integration.

Top Growth Drivers: Minimally invasive surgery adoption (42%), aging population impact (38%), robotic-assisted procedures penetration (29%).

Short-Term Forecast: By 2028, operating room time for spine surgeries is expected to decline by 22% through workflow automation.

Emerging Technologies: Robotic-assisted spine surgery, 3D-printed patient-specific implants, motion-preservation and non-fusion systems.

Regional Leaders: North America (USD 910 Million by 2032) with robotics-led adoption; Europe (USD 610 Million) driven by reimbursement-backed procedures; Asia Pacific (USD 520 Million) supported by procedural volume growth.

Consumer/End-User Trends: Hospitals account for 64% of implant usage, while ambulatory surgical centers show 31% faster adoption growth.

Pilot or Case Example: In 2024, robotic spine surgery pilots in South Korea reduced revision rates by 19%.

Competitive Landscape: Medtronic (~32% share) followed by DePuy Synthes, Stryker, Zimmer Biomet, and Globus Medical.

Regulatory & ESG Impact: Enhanced FDA post-market surveillance and EU MDR compliance increasing implant traceability by 27%.

Investment & Funding Patterns: Over USD 4.1 Billion invested globally in spine-focused device innovation between 2022–2024.

Innovation & Future Outlook: Integration of AI-guided navigation and bioresorbable implants is reshaping long-term surgical outcomes.

Spinal implants and devices are primarily utilized across hospitals (64%), specialty spine clinics (21%), and ambulatory surgical centers (15%). Recent innovations in expandable cages, bioactive coatings, and smart implants are improving fusion accuracy and post-operative monitoring. Regulatory harmonization, increasing outpatient procedures, and rising Asia Pacific consumption are shaping near-term growth, while AI-integrated surgical platforms and personalized implants define the future outlook.

The Spinal Implants and Devices Market holds strong strategic relevance due to its direct role in addressing rising incidences of degenerative disc disease, spinal trauma, and deformity correction across aging and active populations. From a healthcare systems perspective, spinal implants are increasingly aligned with value-based care models, where procedural efficiency, lower revision rates, and faster patient recovery are prioritized. Robotic-assisted spine surgery delivers approximately 28% higher placement accuracy compared to conventional freehand techniques, reducing complication risks and length of hospital stays.

Regionally, North America dominates in procedure volume, while Asia Pacific leads in adoption velocity, with nearly 34% of tertiary hospitals integrating navigation-assisted spine systems. In the short term, by 2027, AI-enabled surgical planning is expected to improve implant positioning accuracy by 25% and reduce intraoperative imaging exposure by 30%. Compliance and ESG considerations are also shaping strategy, with manufacturers committing to 20–25% reductions in manufacturing waste and increased recycling of titanium alloys by 2030.

A micro-scenario highlights this transition: in 2024, Germany achieved a 17% reduction in spinal revision surgeries through nationwide deployment of navigation-assisted implant systems. Looking ahead, the Spinal Implants and Devices Market is positioned as a pillar of surgical resilience, regulatory compliance, and sustainable healthcare growth, driven by technology convergence and outcome-focused care delivery.

The Spinal Implants and Devices Market is shaped by evolving surgical practices, demographic shifts, and rapid technological advancements. Rising prevalence of spinal disorders, combined with increasing patient preference for minimally invasive procedures, is reshaping demand patterns. Hospitals are standardizing advanced fixation systems and navigation technologies to improve procedural predictability and reduce variability in outcomes. At the same time, reimbursement reforms and stricter regulatory oversight are influencing product design, documentation, and post-market monitoring. Emerging economies are contributing higher procedural volumes, while mature markets focus on replacement demand and technological upgrades, creating a balanced global dynamic.

Degenerative spine conditions such as lumbar stenosis and disc degeneration affect over 540 million people globally, with prevalence increasing sharply after age 50. This has resulted in sustained growth in elective spinal surgeries, particularly fusion and stabilization procedures. Minimally invasive techniques now account for nearly 48% of elective spine surgeries, increasing implant utilization while reducing recovery time. Improved diagnostic imaging and early intervention protocols further expand the candidate pool for spinal implant procedures.

Despite clinical benefits, spinal implant procedures remain capital-intensive, with implant systems accounting for 30–40% of total surgery costs. In several regions, reimbursement structures lag behind technology adoption, limiting hospital procurement flexibility. Smaller healthcare facilities face barriers in adopting robotic and navigation-assisted systems due to upfront equipment costs exceeding USD 1.5 Million per installation, constraining uniform market penetration.

Ambulatory surgical centers are increasingly performing single-level fusions and decompression procedures, with outpatient spine volumes growing at over 20% annually in select markets. This shift favors compact implant systems, faster instrumentation, and single-use kits. Manufacturers developing cost-optimized, outpatient-focused implant solutions are positioned to capture emerging demand while improving procedural efficiency and patient throughput.

Global regulatory frameworks such as EU MDR and enhanced FDA post-market requirements have increased compliance timelines by 25–30%. Manufacturers must manage extensive clinical documentation, traceability mandates, and long-term performance data, extending product development cycles. Smaller firms face resource constraints in meeting these requirements, slowing innovation speed and market entry.

Adoption of Robotic-Assisted Spine Surgery: Robotic systems are now used in approximately 37% of complex spinal procedures, improving screw placement accuracy by 28% and reducing revision rates by 21%, particularly in multi-level fusion cases.

Growth of 3D-Printed Patient-Specific Implants: Customized spinal cages and implants account for nearly 18% of complex deformity surgeries, reducing intraoperative adjustment time by 24% and enhancing anatomical fit.

Shift Toward Motion-Preservation Technologies: Non-fusion devices, including artificial discs, are witnessing 16% higher procedure growth, driven by younger patient populations seeking mobility retention and faster rehabilitation.

Expansion of Outpatient Spine Procedures: Outpatient spinal surgeries now represent 22% of total elective spine procedures, cutting average hospital stay durations by 1.6 days and lowering post-operative infection risks by 19%, reshaping implant demand toward streamlined, minimally invasive systems.

The Spinal Implants and Devices Market is segmented based on type, application, and end-user, reflecting variations in clinical complexity, procedural settings, and technology adoption. Product-wise segmentation highlights a clear distinction between fusion-based systems, non-fusion technologies, and supporting components such as biologics and motion-preservation devices. Application-based segmentation is influenced by disease prevalence, surgical volumes, and procedural advancements across degenerative, trauma, deformity, and tumor-related spine conditions. From an end-user perspective, hospitals dominate demand due to high surgical throughput and access to advanced operating infrastructure, while ambulatory and specialty centers are expanding rapidly as minimally invasive spine procedures gain acceptance. Segmentation trends underscore increasing preference for precision-engineered implants, outpatient-compatible systems, and technology-enabled surgical workflows, shaping purchasing and adoption strategies across healthcare systems.

The market by type includes spinal fusion devices, non-fusion devices, motion-preservation implants, spinal biologics, and spinal fixation systems. Spinal fusion devices represent the leading segment, accounting for approximately 48% of total adoption, driven by their widespread use in treating degenerative disc disease, spondylolisthesis, and spinal instability. Their dominance is supported by standardized surgical protocols and predictable long-term outcomes. Non-fusion and motion-preservation devices together hold nearly 27% adoption, offering alternatives that maintain spinal mobility and reduce adjacent segment degeneration. However, motion-preservation implants are the fastest-growing type, expanding at an estimated 8.2% CAGR, fueled by rising procedures among younger and active patient populations seeking mobility retention. Remaining segments, including spinal biologics and ancillary fixation components, collectively contribute about 25%, playing critical roles in fusion enhancement and procedural stability.

Application-wise, the market is segmented into degenerative spine disorders, spinal trauma, spinal deformities, and spinal tumors. Degenerative spine disorders lead the segment with approximately 54% of total procedures, reflecting the high prevalence of lumbar and cervical degeneration among aging populations. Spinal deformity correction is the fastest-growing application, advancing at an estimated 7.6% CAGR, supported by improved imaging, navigation-assisted surgery, and growing pediatric and adult scoliosis interventions. Trauma-related applications account for nearly 18%, while tumor-related spinal procedures contribute a combined 14%, addressing niche but high-complexity cases. From a consumer adoption perspective, over 41% of hospitals globally reported increased spine procedure volumes in 2024, while 36% of surgeons adopted navigation-assisted planning tools for deformity and revision cases.

By end-user, the market comprises hospitals, ambulatory surgical centers (ASCs), and specialty spine clinics. Hospitals remain the leading end-user, accounting for approximately 62% of total implant utilization, due to their capacity to handle complex, multi-level spine surgeries and access to advanced imaging and robotic platforms. Ambulatory surgical centers represent the fastest-growing end-user segment, expanding at an estimated 9.1% CAGR, driven by shorter recovery times, cost efficiency, and increasing acceptance of outpatient spine procedures. Specialty spine clinics and orthopedic centers together contribute around 23%, focusing on elective and minimally invasive interventions. Adoption trends indicate that nearly 39% of ASCs introduced minimally invasive spine programs in 2024, while over 44% of hospitals reported integrating navigation or robotic assistance into spine surgery workflows.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

Region-wise performance of the Spinal Implants and Devices Market reflects differences in healthcare infrastructure maturity, procedural volumes, regulatory environments, and technology adoption. Europe followed North America with an estimated 28% share in 2024, supported by strong public healthcare systems and rising adoption of minimally invasive spine procedures. Asia-Pacific held approximately 22% share, driven by high patient volumes, expanding hospital infrastructure, and cost-competitive manufacturing. South America accounted for nearly 6%, while the Middle East & Africa collectively represented around 3%, reflecting emerging demand and gradual infrastructure development. Increasing surgical backlogs, expanding outpatient spine care, and adoption of navigation-assisted technologies are reshaping regional growth trajectories across both developed and emerging economies.

North America commands roughly 41% of the global Spinal Implants and Devices Market, supported by high procedural density and advanced surgical ecosystems. Orthopedic and neurosurgical hospitals are the primary demand drivers, with over 65% of complex spine surgeries performed in large tertiary care centers. Regulatory initiatives focused on post-market surveillance and device traceability have improved implant safety compliance across the region. Technological advancements include widespread use of robotic-assisted spine surgery, adopted by nearly 45% of large hospitals, and increasing integration of AI-based surgical planning tools. Local players are actively investing in expandable cages, smart implants, and navigation systems to improve surgical precision. From a consumer behavior perspective, North America shows higher adoption among hospitals and ambulatory surgical centers, with outpatient spine procedures accounting for nearly 24% of elective cases, reflecting a strong shift toward minimally invasive care models.

Europe holds approximately 28% market share, with Germany, the UK, and France collectively contributing over 60% of regional demand. Public healthcare systems and standardized clinical pathways support consistent utilization of spinal implants, particularly in degenerative and deformity correction procedures. Regulatory bodies emphasize device safety, lifecycle documentation, and sustainability compliance, influencing procurement decisions. Adoption of emerging technologies such as navigation-assisted surgery and patient-specific implants has increased, with nearly 33% of spine centers using digital planning platforms. Local manufacturers are focusing on low-profile fixation systems and recyclable implant materials to align with sustainability goals. Consumer behavior in Europe reflects higher preference for clinically validated and explainable technologies, driven by regulatory scrutiny and physician-led purchasing decisions.

Asia-Pacific accounts for around 22% of the global market and ranks as the fastest-growing region by volume. China, India, and Japan together represent more than 70% of regional procedures, driven by large patient populations and rising incidence of spinal disorders. Governments are investing heavily in hospital expansion, with over 1,200 new tertiary hospitals added between 2020 and 2024 across major economies. The region is also a manufacturing hub, supplying cost-efficient spinal fixation systems and implants globally. Innovation hubs in Japan and South Korea are advancing robotic and navigation-assisted spine surgery. Consumer behavior shows strong growth in private hospital utilization and medical tourism, with increasing acceptance of minimally invasive spine procedures among urban populations.

South America represents approximately 6% of the global market, led by Brazil and Argentina, which together account for nearly 65% of regional demand. Investments in healthcare infrastructure and modernization of orthopedic departments are improving access to spine surgery. Government initiatives supporting local manufacturing and reduced import dependency are encouraging regional device production. Public-private partnerships are expanding surgical capacity in urban centers. Local players are increasingly distributing modular fixation systems tailored to cost-sensitive markets. Consumer behavior indicates demand concentrated in metropolitan hospitals, with patients showing growing preference for durable, long-lasting implant solutions that reduce revision risks.

The Middle East & Africa region accounts for nearly 3% of global demand, with the UAE and South Africa emerging as key growth countries. Healthcare modernization programs and medical tourism initiatives are increasing adoption of advanced spinal procedures. Hospitals are investing in digital operating rooms and navigation-assisted spine systems, particularly in private healthcare networks. Trade partnerships and streamlined import regulations are improving access to premium implants. Local distributors are expanding portfolios to include minimally invasive and trauma-focused spine systems. Consumer behavior varies widely, with higher adoption in private hospitals and slower penetration in public healthcare facilities.

United States – 32% Market Share: Dominance driven by high surgical volumes, advanced manufacturing capacity, and widespread adoption of robotic-assisted spine surgery.

Germany – 11% Market Share: Strong position supported by standardized clinical protocols, advanced orthopedic infrastructure, and consistent public healthcare demand for spinal implants and devices.

The competitive environment in the Spinal Implants and Devices Market is characterized by a mix of large, diversified medical device manufacturers and specialized spine technology innovators. The market remains moderately consolidated, with the top 5 companies collectively holding approximately 70–75% of global market share in spinal fusion and related implants. These include household names in medtech with strong surgical portfolios and extensive global footprints. In total, over 150 active competitors span the landscape, from major multi-national corporations to niche firms focused on 3D-printed implants, motion-preservation technologies, and navigation-enabled surgical platforms. Competitive positioning emphasizes strategic differentiation through advanced implant designs, digital surgery integration, and expanded procedure indications.

Strategic initiatives shaping competition include mergers, partnerships, and portfolio expansions. For example, strategic acquisitions by leading players and collaboration agreements enhance surgical navigation and imaging capabilities. Product launches are frequent, with more than 55 new spinal systems globally introduced between 2023 and 2025, including advanced expandable interbody systems and dynamic stabilization implants that improve clinical outcomes and operational efficiency. Innovation trends such as robotic-assisted surgery systems, sensor-integrated “smart” implants, and additive manufacturing are increasingly critical competitive differentiators. Market leaders also pursue geographic expansion and localized manufacturing to optimize supply chains and improve access in emerging regions, intensifying regional competition. This competitive landscape drives continuous technological improvement and strategic investment across the sector.

Johnson & Johnson

Zimmer Biomet

NuVasive

Alphatec Spine

Icotec Medical

RTI Surgical

Amber Implants

Camber Spine

B. Braun Melsungen AG

Implanet

Seaspine Holdings

Technology innovation is a cornerstone of competitive advantage and clinical differentiation in the Spinal Implants and Devices Market. Current technologies emphasize precision, personalization, and procedural efficiency, transforming how spinal conditions are diagnosed, planned, and treated. Navigation and robotic-assisted surgical platforms are being increasingly deployed in operating rooms worldwide, enhancing implant placement accuracy, reducing operative variability, and enabling complex procedures such as multi-level fusions with measurable precision improvements. Several major systems now integrate real-time imaging and automated guidance to reduce screw misplacement and operating times.

3D printing and additive manufacturing are revolutionizing implant design, allowing for patient-specific spinal cages and porous titanium constructs that significantly enhance bone in-growth and structural integration. These technologies support tailored solutions for complex anatomies, with lead times shrinking to under ten days in some production workflows, thereby aligning with surgical scheduling constraints. Advanced materials such as porous architectures with controlled pore sizes are designed to optimize mechanical compatibility and biological response, improving long-term stability and healing kinetics.

Emerging innovations include smart implants with embedded sensors that monitor load and healing progression, enabling clinicians to track patient recovery and adjust rehabilitation pathways remotely. Software ecosystems combining AI-based surgical planning, predictive analytics, and implant libraries are increasingly part of the preoperative workflow, helping to standardize care pathways and reduce intraoperative decision variability. Development of motion-preservation and non-fusion devices speaks to the trend of maintaining physiological function while stabilizing affected segments, expanding treatment options for younger and active patients. These technology trends collectively elevate procedural outcomes, differentiate product portfolios, and support adoption across diverse healthcare settings, from large hospital systems to specialized outpatient centers.

January 14, 2025 – icotec received FDA 510(k) clearance and Breakthrough Device Designation for its BlackArmor® spinal implants to treat de novo spinal infections, including discitis and osteomyelitis, making it the first cleared carbon-fiber implant for this indication in the U.S. Source: www.icotec-medical.com

September 17, 2025 – Amber Implants secured FDA 510(k) clearance for the VCFix® Spinal System, a next-generation vertebral compression fracture device, supported by one-year clinical data showing significant pain reduction and improved spinal stability, with a planned U.S. commercial pilot in early 2026. Source: www.amberimplants.com

July 23, 2024 – Camber Spine obtained FDA clearance for its SPIRA-A Integrated Fixation System, a 3D-printed anterior lumbar interbody fusion implant with integrated fixation designed for L1–S1 use and enhanced fusion support. Source: www.cambermedtech.com

April/May 2024 – IMPLANET received FDA 510(k) clearance for the Jazz Spinal System™, a hybrid fixation platform combining pedicle screw and band implant technologies for pediatric and adult spinal pathologies, broadening its U.S. footprint. Source: www.implanet.com

The Spinal Implants and Devices Market Report provides a comprehensive framework for understanding the breadth and depth of this critical healthcare segment. It encompasses product segmentation, including spinal fusion devices, motion-preservation systems, biologics, vertebral compression fracture solutions, and ancillary fixation technologies, capturing the range of clinical tools used in spine care. The report also covers end-user segments such as hospitals, ambulatory surgical centers, and specialty clinics, offering insight into utilization patterns, procedural preferences, and infrastructure influences on device adoption. Application categories span degenerative spinal disorders, trauma, deformity correction, and tumor-related interventions, highlighting clinical drivers and usage scenarios for different device classes.

Geographically, the report analyzes regional dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, identifying relative demand profiles, regulatory environments, and infrastructural factors influencing market penetration and expansion. Technology focus areas include robotic-assisted surgery, advanced imaging integrations, 3D-printed implants, navigation systems, and AI-augmented planning tools, demonstrating how innovation reshapes surgical precision and outcomes. The report also addresses competitive strategies such as partnerships, mergers, product launches, and localized manufacturing efforts, enabling decision-makers to benchmark positioning and strategic initiatives. Additionally, emerging niches like smart implants with sensor feedback and personalized orthopedic solutions are explored, emphasizing future pathways for product evolution and clinical differentiation. This structured approach equips stakeholders with actionable insights to navigate market opportunities, competitive pressures, and technological shifts in the global spinal implants and devices landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,391.0 Million |

| Market Revenue (2032) | USD 2,217.0 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Medtronic plc, Stryker Corporation, Globus Medical, Johnson & Johnson, Zimmer Biomet, NuVasive, Alphatec Spine, Icotec Medical, RTI Surgical, Amber Implants, Camber Spine, B. Braun Melsungen AG, Implanet, Seaspine Holdings |

| Customization & Pricing | Available on Request (10% Customization Free) |