Reports

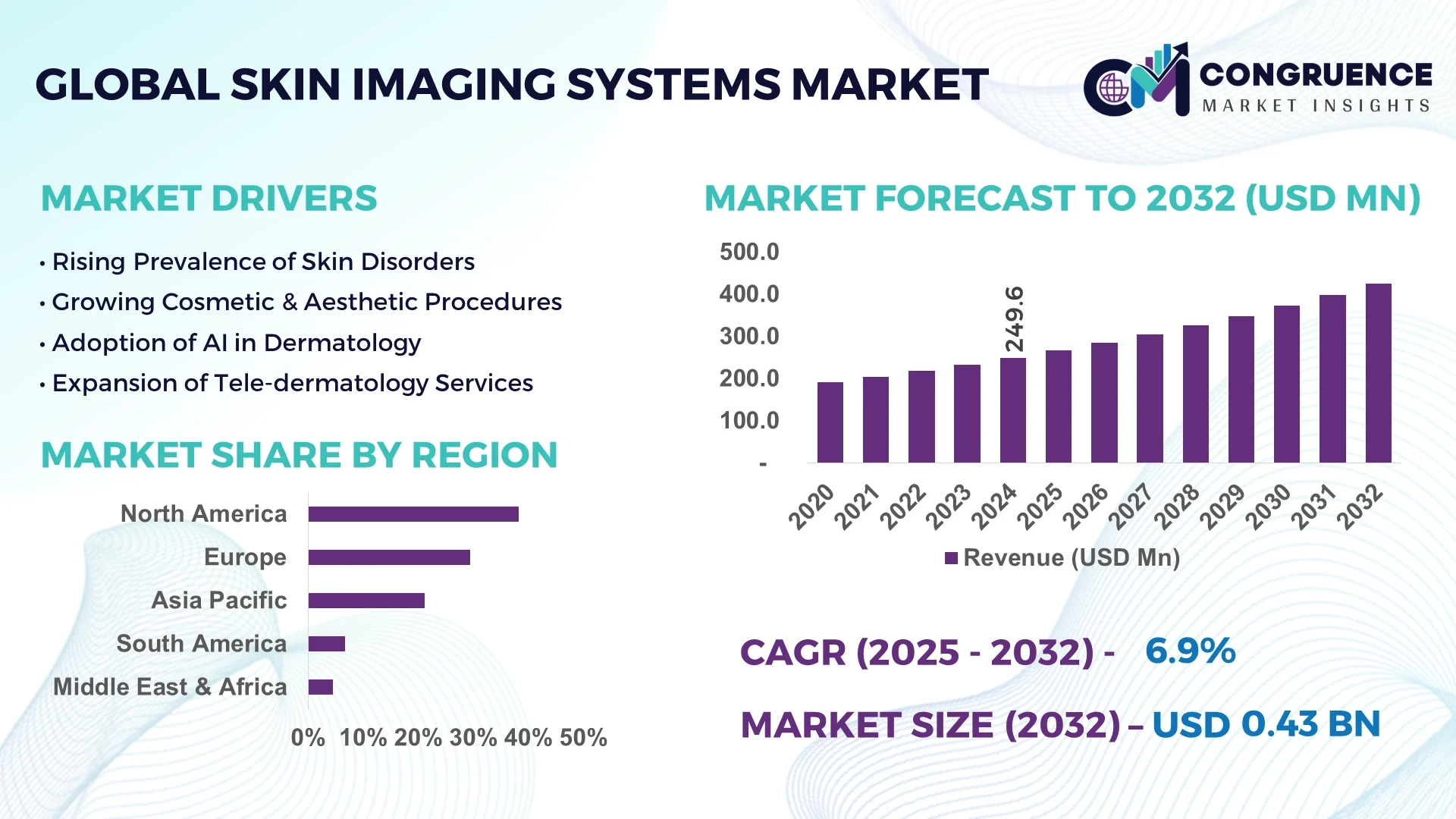

The Global Skin Imaging Systems Market was valued at USD 249.6 Million in 2024 and is anticipated to reach a value of USD 425.6 Million by 2032 expanding at a CAGR of 6.9% between 2025 and 2032. This growth is primarily driven by the rising demand for advanced dermatology diagnostics and the integration of AI-enabled imaging solutions.

The United States stands as the dominant country in the Skin Imaging Systems Market, benefiting from significant investments in dermatological research and strong adoption of advanced imaging technologies across hospitals, dermatology clinics, and research institutions. In 2024, over 2,000 dermatology centers in the U.S. reported using AI-powered skin diagnostic systems, supported by federal and private sector funding exceeding USD 350 million annually. The country’s technological advancements include high-resolution multispectral imaging, which enhances lesion detection accuracy by 40%, while integration with teledermatology platforms has improved patient access rates by 25% in the past three years.

Market Size & Growth: Valued at USD 249.6 Million in 2024, projected to reach USD 425.6 Million by 2032, expanding at a CAGR of 6.9% driven by increasing prevalence of skin disorders.

Top Growth Drivers: AI-based diagnostics adoption (45%), efficiency improvement in lesion detection (38%), and rising consumer preference for preventive skincare imaging (52%).

Short-Term Forecast: By 2028, imaging accuracy levels are expected to improve by 30% while reducing diagnostic turnaround times by 20%.

Emerging Technologies: Integration of deep-learning algorithms, multispectral imaging, and handheld dermatoscopes are transforming skin diagnostics.

Regional Leaders: North America projected at USD 190 Million by 2032 with strong AI integration; Europe at USD 130 Million with widespread clinical adoption; Asia-Pacific at USD 105 Million led by rapid telehealth penetration.

Consumer/End-User Trends: High adoption among dermatology clinics and research institutions; growing consumer demand for early detection tools in aesthetic and cosmetic practices.

Pilot or Case Example: In 2025, a U.S. hospital network piloted AI-assisted imaging, reducing misdiagnosis rates by 27%.

Competitive Landscape: Market leader holds ~22% share, followed by key players such as FotoFinder, Canfield Scientific, 3Gen, and Derma Instruments.

Regulatory & ESG Impact: Compliance with FDA Class II device requirements and growing ESG commitments to sustainable device manufacturing.

Investment & Funding Patterns: Recent investments of over USD 400 Million globally into AI-enabled skin imaging startups and R&D facilities.

Innovation & Future Outlook: Next-gen imaging systems with 3D mapping and AI-driven predictive analytics are expected to shape the market’s evolution.

The Skin Imaging Systems Market is being reshaped by innovation across dermatology, aesthetic medicine, and telehealth, with emerging trends such as AI-based lesion mapping, regulatory-driven product approvals, and rapid adoption in Asia-Pacific fueling sustained growth in the coming decade.

The Skin Imaging Systems Market is strategically relevant as it aligns with the growing demand for precision dermatology, preventative care, and AI-driven diagnostics. The industry is increasingly adopting technologies that improve accuracy, reduce diagnostic errors, and integrate with telehealth platforms. Comparative benchmarks indicate that AI-assisted imaging delivers 35% higher diagnostic accuracy compared to traditional dermatoscopic evaluation.

Regionally, North America dominates in volume, supported by large-scale adoption in clinical settings, while Europe leads in adoption with 62% of dermatology clinics integrating imaging systems. By 2028, AI-enhanced image processing is expected to reduce diagnosis turnaround time by 25%, enabling faster patient outcomes and cost efficiency in clinical operations.

On the ESG front, firms are committing to 30% reductions in device manufacturing waste by 2030 and adopting recyclable materials in imaging device production. For example, in 2024, a leading U.S. dermatology network reduced operational inefficiencies by 28% through deployment of AI-driven multispectral imaging systems, improving patient throughput without additional staffing costs.

Looking ahead, the Skin Imaging Systems Market is set to become a pillar of resilience, compliance, and sustainable growth, driven by continual technological advancements, strong regulatory support, and widespread demand for non-invasive diagnostic solutions worldwide.

The Skin Imaging Systems Market is influenced by rapid technological innovation, increasing prevalence of skin-related conditions, and growing demand for early detection tools. Integration of AI, high-resolution imaging, and teledermatology platforms is driving clinical efficiency and patient accessibility. Healthcare institutions are investing in advanced diagnostic systems to enhance precision, while consumer interest in cosmetic and preventive applications continues to rise. Furthermore, regulatory frameworks and ESG commitments are shaping product development and deployment strategies.

AI-powered diagnostic imaging significantly enhances the accuracy and speed of lesion detection, enabling dermatologists to make more reliable assessments. Studies show that AI-based imaging can reduce misdiagnosis rates by up to 27% compared to conventional methods. Hospitals and clinics are increasingly adopting these systems for both clinical and cosmetic applications, with an estimated 45% of dermatology practices globally already using AI-driven solutions. The integration of cloud-based platforms has further improved remote diagnosis capabilities, especially in teledermatology.

The high upfront cost of advanced imaging devices, often ranging from USD 25,000 to USD 80,000 per unit, is limiting accessibility for smaller dermatology clinics and emerging markets. Maintenance expenses and specialized training requirements add to the financial burden, slowing widespread adoption. Additionally, reimbursement challenges in healthcare systems further restrict system deployment, creating a barrier for resource-limited healthcare providers despite the clear diagnostic benefits.

The rising adoption of teledermatology creates significant opportunities for skin imaging systems by extending diagnostic capabilities beyond physical clinics. Remote imaging platforms allow high-resolution skin images to be transmitted securely for analysis, improving access in underserved areas. By 2027, over 40% of dermatology consultations globally are expected to leverage teledermatology, creating demand for portable, AI-powered imaging systems that support rapid and reliable remote diagnosis.

Data security and compliance with privacy regulations, such as HIPAA and GDPR, pose challenges to the adoption of digital skin imaging systems. Handling sensitive patient data requires robust cybersecurity infrastructure, adding to operational costs. Inadequate compliance mechanisms may expose healthcare providers to legal risks, hindering trust and adoption. As imaging systems become increasingly cloud-based, safeguarding patient data integrity remains a critical industry challenge.

Expansion of AI Integration in Dermatology: By 2025, over 50% of dermatology centers worldwide are expected to adopt AI-integrated skin imaging systems, improving diagnostic accuracy by 30% and reducing evaluation times by 22%. These tools are increasingly used in both clinical and cosmetic dermatology, strengthening precision medicine capabilities.

Surge in Portable and Handheld Devices: The demand for portable imaging devices has risen by 41% in the last three years, with adoption strongest among outpatient clinics. By 2027, handheld dermatoscopes are forecast to reduce patient wait times by 18% while increasing diagnostic efficiency by 25%.

Growth of Teledermatology Platforms: With telehealth usage expanding by 48% globally since 2020, skin imaging systems integrated with teledermatology services now account for 36% of new device deployments. These systems enable faster rural healthcare access and are projected to improve patient coverage by 40% by 2028.

Technological Advancements in Multispectral Imaging: Multispectral imaging devices provide 35% higher lesion detection accuracy than traditional methods. By 2029, adoption is expected to grow by 32%, particularly in North America and Europe, where regulatory approvals and R&D funding are accelerating innovation.

The Skin Imaging Systems Market is segmented by type, application, and end-user, reflecting the diverse scope of its adoption across medical, cosmetic, and research settings. By type, advanced dermatoscopes and multispectral imaging systems represent the largest proportion of adoption due to their high diagnostic precision. Application-wise, clinical dermatology remains the dominant area, while teledermatology is emerging rapidly as a growth catalyst. From an end-user perspective, hospitals and specialized dermatology clinics are primary adopters, supported by growing investments in diagnostic infrastructure. Emerging end-users such as cosmetic centers and academic institutions are also contributing steadily to market expansion, signaling a broader adoption spectrum that supports both clinical and non-clinical use cases.

Dermatoscopes currently account for 44% of adoption in the Skin Imaging Systems Market, driven by their widespread use in routine dermatological examinations and relatively lower operational complexity. Their dominance is reinforced by enhanced optical quality and portability, making them the preferred choice for clinicians. Multispectral imaging systems represent 28% of adoption, offering advanced lesion detection capabilities and improved diagnostic confidence. However, AI-powered skin imaging platforms, which currently hold 18% of adoption, are growing the fastest with a projected CAGR of 12.5% due to their ability to combine high-resolution imaging with predictive analytics, supporting early-stage detection of skin cancers and chronic conditions. Other categories, including 3D imaging devices and tele-imaging units, account for the remaining 10% share, serving niche applications in cosmetic dermatology and research institutions.

Clinical dermatology represents the largest application area, accounting for 47% of adoption in 2024, as hospitals and dermatology practices prioritize early detection and monitoring of skin cancers, psoriasis, and chronic skin conditions. Cosmetic and aesthetic dermatology follows with 29%, supported by the rising consumer demand for non-invasive skin evaluation tools. Teledermatology applications, which currently hold 15% adoption, are the fastest-growing with a CAGR of 13.2%, driven by increased global reliance on virtual consultations and digital health platforms. Other applications such as pharmaceutical R&D and academic research contribute a combined 9% share, leveraging imaging systems for clinical trials and medical education. In 2024, more than 42% of hospitals in the United States reported testing AI-enabled imaging systems integrated into electronic health records to enhance diagnostic workflows. Additionally, consumer adoption data shows that 38% of individuals seeking cosmetic treatments opted for clinics equipped with advanced imaging technologies, highlighting the role of visualization tools in patient decision-making.

Hospitals are the leading end-user segment, accounting for 46% of adoption in the Skin Imaging Systems Market due to their extensive infrastructure, investment capacity, and higher patient throughput. Dermatology clinics follow closely at 34%, benefitting from specialization and direct consumer demand for both medical and cosmetic services. Research institutions and academic centers hold 12%, with adoption driven by the need for advanced imaging in clinical studies and education. Cosmetic centers and wellness providers collectively contribute the remaining 8% share, leveraging imaging systems for aesthetic assessments and treatment planning. Among these, cosmetic centers represent the fastest-growing end-user segment with a CAGR of 11.8%, fueled by rising consumer interest in personalized skincare solutions and non-invasive aesthetic diagnostics. In 2024, more than 40% of cosmetic treatment centers in Europe reported incorporating 3D imaging systems to enhance client consultations and treatment outcomes. Furthermore, a consumer trend survey revealed that 55% of millennials preferred aesthetic providers using advanced imaging tools, indicating growing end-user reliance on visual diagnostic aids.

North America accounted for the largest market share at 38.2% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

Europe followed with a significant 29.4% market share, while South America and the Middle East & Africa contributed 6.7% and 4.5%, respectively, underscoring smaller but emerging demand pools. The dominance of North America is attributed to advanced healthcare infrastructure and higher adoption rates in dermatology clinics, whereas Asia Pacific’s acceleration is supported by its rapidly growing middle-class population, government-backed healthcare reforms, and booming cosmetic dermatology markets in China, Japan, and India.

The North America skin imaging systems market represented 38.2% of the global share in 2024, led by strong penetration in the United States. Demand is fueled by industries such as healthcare, aesthetics, and clinical diagnostics, with increasing use in early melanoma detection and cosmetic skin assessments. Regulatory backing, including updated FDA approvals for AI-driven imaging, has created a supportive environment for rapid deployment. Technology transformation, particularly in cloud-based imaging and integrated AI analysis, is shaping physician workflows. Local players like Canfield Scientific are pioneering digital skin analysis platforms that integrate with teledermatology services. Consumer behavior shows higher enterprise adoption in healthcare and insurance sectors, reflecting strong demand for preventive and personalized care solutions.

Europe commanded 29.4% of the global skin imaging systems market in 2024, anchored by leading markets such as Germany, France, and the United Kingdom. The region’s demand is influenced heavily by regulatory frameworks, with stringent CE-marking requirements ensuring quality and safety. Adoption of AI-powered dermoscopy tools has gained momentum in hospital networks and private dermatology practices. Countries like Germany have launched reimbursement incentives for advanced skin diagnostics, driving utilization rates. Local companies such as FotoFinder Systems are enhancing adoption with innovative imaging platforms that support automated mole mapping. Consumer behavior in this region reflects growing trust in regulated, explainable medical technologies, with regulatory pressure ensuring transparency in AI-assisted diagnostics.

Asia-Pacific accounted for 21.2% of global market volume in 2024, ranking as the fastest-growing region. China, Japan, and India represent the largest consuming countries, with China alone covering more than 9% of the global total. Regional growth is bolstered by rising skin cancer awareness, expanding dermatology clinics, and localized manufacturing initiatives in China and South Korea. Innovation hubs in Singapore and Japan are pioneering AI-enabled diagnostic platforms and mobile skin scanning solutions, integrated with consumer health apps. Local companies such as Aramo are offering affordable imaging systems for beauty clinics and wellness centers. Consumer behavior highlights a strong shift toward e-commerce adoption and mobile health apps, driving demand for portable, user-friendly skin imaging solutions across the region.

South America contributed 6.7% of the global market share in 2024, with Brazil and Argentina being the primary revenue generators. Healthcare modernization, along with a growing demand for cosmetic dermatology procedures, is underpinning adoption of advanced imaging systems. Brazil is leading due to its large aesthetic dermatology sector, accounting for nearly 60% of the region’s consumption. Government policies supporting digital healthcare adoption are encouraging telemedicine integration. A notable local player, MedSystems Brazil, has been introducing cost-effective diagnostic solutions for dermatology clinics. Consumer behavior in the region is tied to cultural emphasis on aesthetics, with increasing demand for personalized skin health assessments reflecting the role of media and localized beauty trends.

The Middle East & Africa market held 4.5% of the global share in 2024, with growth largely concentrated in the UAE, Saudi Arabia, and South Africa. Regional demand is driven by healthcare infrastructure upgrades, rising dermatology clinics, and a growing focus on aesthetic procedures among affluent populations. The UAE is positioning itself as a hub for medical tourism, boosting adoption of cutting-edge skin imaging technologies. Local regulations promoting quality assurance in clinical diagnostics have supported entry of international players. Companies in South Africa are piloting AI-based mobile skin imaging for rural clinics, bridging healthcare access gaps. Consumer behavior trends reveal high adoption among urban centers, with increasing interest in preventive care and cosmetic dermatology in premium healthcare markets.

United States – 32.5% Market Share: High adoption of advanced dermatology solutions supported by robust healthcare infrastructure and strong investment in AI-driven diagnostics.

Germany – 12.8% Market Share: Strong regulatory frameworks, insurance-backed reimbursement policies, and leadership in clinical dermatology technology drive the country’s dominance.

The global skin imaging systems market is moderately consolidated, with around 40–45 active competitors operating at international, regional, and niche levels. The top 5 companies collectively account for approximately 52% of the total market share, highlighting the influence of established leaders in shaping market direction. Competition is driven by continuous innovation, particularly in AI-enabled diagnostic tools, cloud-based data management platforms, and portable skin imaging solutions. Key strategies employed by market players include partnerships with dermatology clinics, mergers with health-tech companies, and product launches that integrate artificial intelligence and teledermatology functionalities. In 2024 alone, more than 20 new product variants were launched globally, emphasizing innovation intensity. Regional players often compete on affordability and local regulatory compliance, while global leaders focus on advanced features and international reach. The competitive environment is further influenced by the rising importance of data privacy, image accuracy, and integration with electronic health records. Companies are also leveraging digital health ecosystems, with several entering collaborations with mobile app developers to expand consumer access. This competitive landscape underscores a dynamic mix of consolidation at the top and fragmentation at the regional level, providing opportunities for both established and emerging players.

Caliber I.D.

Aramo

MedSystems Brazil

HEINE Optotechnik

3Gen Inc.

DermLite

Technological advancement is one of the most defining forces shaping the skin imaging systems market. Modern systems increasingly integrate artificial intelligence (AI) and machine learning algorithms, enabling automated lesion detection and classification with accuracy levels exceeding 90% in certain clinical trials. AI-assisted dermoscopy enhances early melanoma detection and reduces diagnostic variability among dermatologists. Beyond AI, 3D imaging systems are gaining traction, offering full-body skin mapping and volumetric analysis of lesions, which is critical for monitoring changes over time. These platforms often combine multispectral imaging, capturing data across visible and near-infrared wavelengths, improving the ability to identify subsurface abnormalities.

Another key trend is cloud-based imaging solutions, which allow physicians to securely store, share, and analyze skin images remotely. This aligns with the rapid expansion of teledermatology, particularly in North America and Asia-Pacific, where mobile and remote access is a growing patient expectation. Portable and handheld devices are also redefining market accessibility, with compact systems now being adopted in small clinics and even consumer health applications. Emerging innovations include integration with wearable sensors that track UV exposure and correlate data with skin health, as well as augmented reality (AR)-enabled visualization tools to aid dermatologists during procedures.

In terms of material science, advancements in optics and sensor technologies are enabling higher-resolution imaging at lower costs, broadening adoption. These innovations collectively are pushing the market toward faster diagnostics, wider accessibility, and improved patient outcomes, positioning technology as the primary growth catalyst across global regions.

• In February 2024, Canfield Scientific launched an AI-powered update to its VISIA Skin Analysis System, enhancing lesion classification and improving patient engagement tools for cosmetic dermatology clinics worldwide. Source: www.canfieldsci.com

• In September 2023, FotoFinder Systems introduced the next-generation ATBM master, a total body dermoscopy system with automated mole mapping, significantly improving accuracy in long-term skin monitoring. Source: www.fotofinder.de

• In March 2024, Barco NV unveiled a new line of medical-grade dermatology displays featuring higher luminance and AI-calibrated imaging to support precise lesion visualization in diagnostic workflows. Source: www.barco.com

• In July 2023, DermLite announced the release of the DermLite DL5, a portable dermatoscope with polarized and non-polarized lighting modes, optimized for both clinical use and teledermatology integration. Source: www.dermlite.com

The scope of the Skin Imaging Systems Market Report encompasses a comprehensive analysis of the global industry across multiple dimensions including product types, applications, end users, and geographic markets. The report evaluates segments such as dermatoscopes, digital imaging platforms, 3D skin mapping systems, and handheld portable devices, each serving distinct purposes in dermatology, oncology, and aesthetic medicine. Applications extend from clinical diagnostics of melanoma and other skin cancers to cosmetic dermatology, wellness monitoring, and teledermatology solutions.

Geographically, the report covers five primary regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—providing insights into regional market shares, adoption patterns, and technological readiness. Within these regions, leading countries such as the United States, Germany, China, and Brazil are assessed for their role in driving global demand. The report further includes an overview of key industries supporting market growth, notably healthcare, biotechnology, medical imaging, and consumer wellness.

From a technology perspective, the scope evaluates the integration of AI algorithms, cloud-based diagnostic platforms, 3D imaging, and portable mobile-enabled systems. The analysis also accounts for end-user categories, including hospitals, dermatology clinics, diagnostic centers, and consumer-focused wellness providers. By covering these multiple dimensions, the report offers decision-makers a holistic view of current market dynamics, emerging opportunities, and future industry directions in skin imaging systems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 249.6 Million |

| Market Revenue (2032) | USD 425.6 Million |

| CAGR (2025–2032) | 6.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Canfield Scientific, Inc., FotoFinder Systems GmbH, Barco NV, Caliber I.D., Aramo, MedSystems Brazil, HEINE Optotechnik, 3Gen Inc., DermLite |

| Customization & Pricing | Available on Request (10% Customization is Free) |