Reports

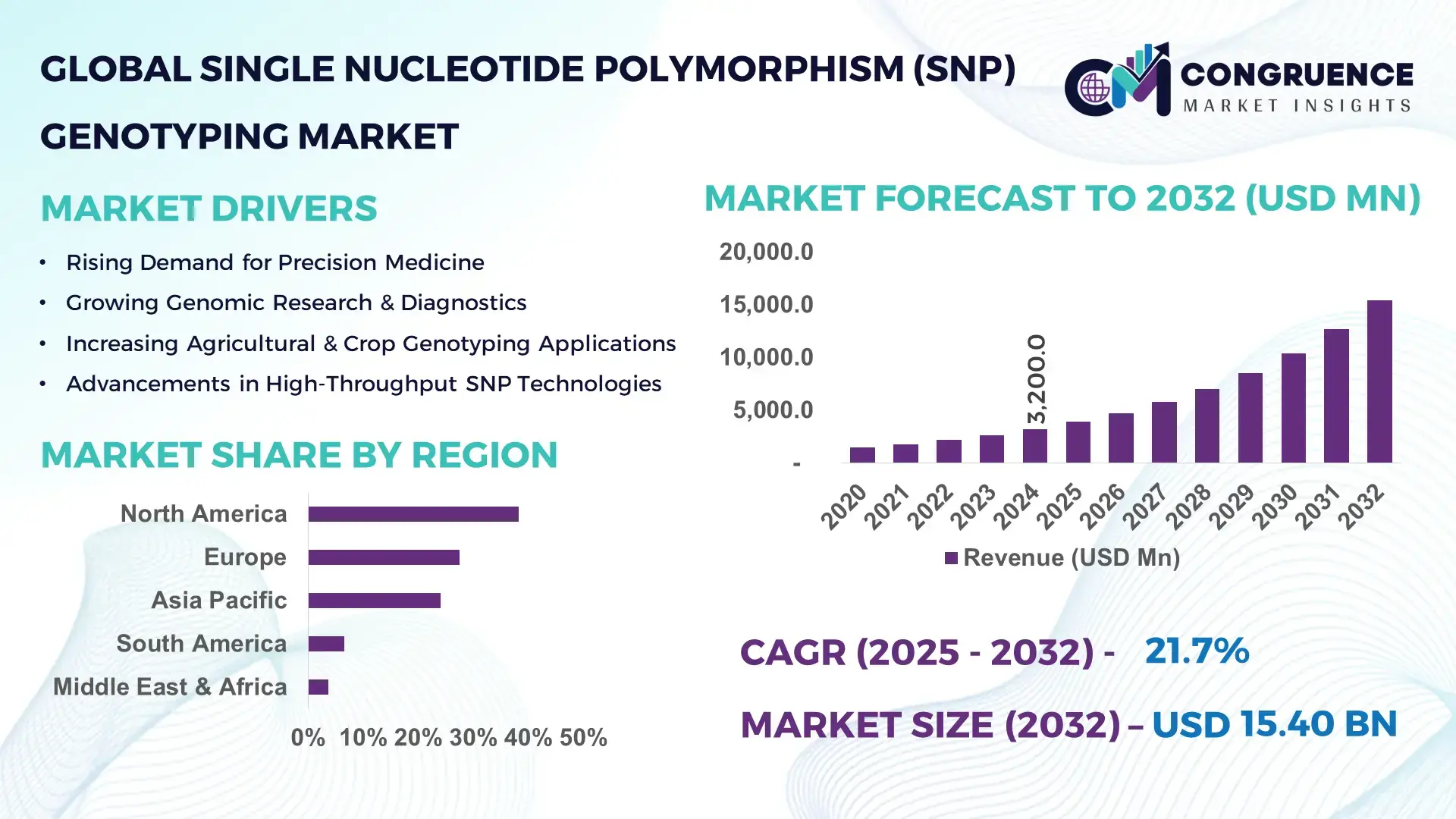

The Global Single Nucleotide Polymorphism (SNP) Genotyping Market was valued at USD 3,200.0 Million in 2024 and is anticipated to reach USD 15,398.4 Million by 2032, expanding at a CAGR of 21.7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This accelerated growth is driven by rapid advancements in high-throughput sequencing platforms and increasing clinical applications of precision diagnostics.

The United States maintains the strongest industry foundation, supported by more than 1,250 active genomics research laboratories, USD 48.3 billion in annual biotechnology R&D expenditure, and extensive integration of SNP-based assays in oncology, pharmacogenomics, and agricultural biotechnology pipelines. The country also hosts over 40% of global sequencing installations, enabling large-scale biobank initiatives and accelerating commercialization of advanced genotyping tools.

Market Size & Growth: Valued at USD 3.2 Billion in 2024, projected to reach USD 15.39 Billion by 2032, expanding at a CAGR of 21.7%; growth supported by rising adoption of precision medicine.

Top Growth Drivers: Increased clinical adoption (38%), platform efficiency improvements (27%), and wider agricultural genomics applications (22%).

Short-Term Forecast: By 2028, workflow automation is expected to reduce per-sample processing time by 32%.

Emerging Technologies: AI-enabled variant calling, microfluidic-based SNP arrays, and hybrid sequencing–genotyping platforms.

Regional Leaders: North America projected to reach USD 6.8 Billion by 2032; Europe to reach USD 4.2 Billion with strong clinical adoption; Asia–Pacific to reach USD 3.6 Billion driven by population-scale genomics programs.

Consumer/End-User Trends: Diagnostics laboratories and research institutes lead adoption as genotyping turnaround times drop by 28%.

Pilot or Case Example: In 2024, a national oncology program achieved a 41% improvement in mutation-detection efficiency using SNP-guided assay integration.

Competitive Landscape: Market leader holds ~18% share; key competitors include Thermo Fisher Scientific, Illumina, Agena Bioscience, LGC Biosearch, and Qiagen.

Regulatory & ESG Impact: Strengthening genomic data compliance frameworks and sustainability-focused R&D incentives influence technology adoption.

Investment & Funding Patterns: Over USD 2.1 Billion invested recently in genotyping infrastructure, precision medicine projects, and bioinformatics innovation.

Innovation & Future Outlook: Advanced multiplex platforms, AI-driven interpretation engines, and population genomics programs are expected to reshape long-term market evolution.

The market is witnessing rapid evolution across diagnostics, agriculture, and drug development, supported by growing adoption of integrated genotyping workflows, new AI-enabled interpretation tools, expanding population-scale genomic efforts, and strengthening regulatory frameworks guiding ethical data utilization.

The Single Nucleotide Polymorphism (SNP) Genotyping Market is becoming strategically vital as global healthcare, agriculture, and pharmaceutical ecosystems increasingly depend on high-resolution genetic insights. Its relevance is amplified by precision therapy demand, where targeted drug responses improve clinical accuracy by more than 35%, compared to older broad-spectrum therapeutic standards. In diagnostics, modern microfluidic genotyping systems deliver 40% faster processing than earlier plate-based methods, strengthening their role in large-volume testing programs.

Regional growth dynamics further reinforce the market’s strategic significance. North America dominates in volume, supported by extensive genomic infrastructure and large-scale clinical adoption, while Asia–Pacific leads in user adoption, with over 46% of research institutions integrating SNP-based tools into disease surveillance and agricultural improvement programs. This geographic interplay underlines the market’s diverse investment and capability expansion patterns.

Short-term projections show strong momentum. By 2027, AI-driven variant interpretation engines are expected to cut analysis time by up to 50%, significantly improving laboratory throughput and reducing operational burdens. Meanwhile, ESG commitments are shaping procurement and operational strategies, with biotechnology firms aiming for 30% reductions in consumable waste by 2030, aligned with environmentally responsible genomics practices.

Practical advancements illustrate measurable outcomes. In 2024, a European genomics consortium achieved a 33% reduction in sequencing error rates through the integration of machine-learning quality filters within SNP genotyping workflows. Such innovations enhance data integrity and support broader deployment of genomics in clinical and agricultural settings.

Going forward, the SNP Genotyping Market will remain a pillar of resilience, compliance, and sustainable technological advancement, reinforced by next-generation sequencing convergence, regulatory modernization, and global-scale genomics initiatives driving precision decision-making across sectors.

The Single Nucleotide Polymorphism (SNP) Genotyping Market is undergoing rapid transformation, driven by the increasing role of precision medicine, agricultural genomics, and advanced drug discovery workflows. Technological improvements in high-throughput sequencing, microarrays, and digital PCR systems continue to enhance accuracy, throughput, and operational efficiency. Rising investment in genomics research, expanding biobank infrastructures, and greater integration of AI in variant detection workflows further stimulate market evolution. Additionally, global initiatives focusing on population-scale genomic mapping and the adoption of standardized laboratory automation practices are creating robust demand for next-generation genotyping solutions. These dynamics collectively support continuous innovation, accelerated adoption across industries, and expansion of genotyping capabilities worldwide.

Growing emphasis on precision medicine is substantially boosting the adoption of SNP genotyping technologies. Healthcare systems are increasingly utilizing genotype-to-phenotype correlations to personalize drug therapies, resulting in improved clinical outcomes and reduced adverse reactions. Over 120 countries have launched national genomics missions incorporating SNP-based diagnostics. Clinical programs integrating pharmacogenomic profiling report up to 45% improvement in treatment-response accuracy, driving widespread adoption. Furthermore, hospitals are implementing SNP-driven predictive models to guide cancer therapy selection and cardiovascular risk assessment, strengthening demand for advanced genotyping platforms. As medical institutions transition toward evidence-based precision protocols, the deployment of SNP assays for risk stratification, early disease detection, and therapeutic optimization continues to expand.

Despite strong adoption, the SNP Genotyping Market faces limitations due to the massive data volumes generated by high-throughput sequencing and large-scale population genomics programs. Many institutions lack sufficient bioinformatics infrastructure, leading to data backlogs and longer interpretation timelines. Genotyping workflows often require computational loads exceeding 40 terabytes per large sequencing project, emphasizing the need for advanced analytics resources. Integration challenges between legacy electronic health record systems and modern genomic data platforms further restrict seamless implementation. Additionally, maintaining compliance with privacy regulations, such as GDPR and HIPAA, increases operational complexity for laboratories handling sensitive genetic datasets. These constraints collectively slow down process scalability and limit the broader impact of genotyping technologies.

The rapid growth of agricultural genomics offers substantial opportunities for the SNP Genotyping Market. Global food-security initiatives increasingly emphasize genomic selection, with SNP-based techniques enabling up to 30% faster breeding cycles and improved trait predictability. Major agricultural economies are deploying genotyping tools to enhance drought tolerance, pest resistance, and crop nutritional quality. More than 280 large-scale crop improvement projects now incorporate SNP arrays to optimize germplasm evaluation and hybrid development. Livestock breeding programs also utilize SNP markers for superior lineage tracking and productivity enhancement. As agricultural biotechnology expands, demand for cost-efficient, high-throughput SNP platforms is expected to rise across both developed and emerging markets.

The SNP Genotyping Market faces notable challenges arising from specialized skill requirements and rising operational burdens. Laboratories require highly trained personnel to manage sequencing workflows, data quality checks, and variant interpretation processes, but global shortages persist—particularly in regions where genomic infrastructure is still developing. Training costs have increased by over 22% in the last five years, impacting scalability. Additionally, maintenance of advanced sequencing equipment demands high technical expertise and strict environmental controls, adding to operational complexity. Smaller laboratories often struggle with the financial and technical demands associated with maintaining high-throughput genotyping systems, limiting wide-scale deployment across resource-constrained environments.

AI-Enhanced Genotyping Pipelines: AI-driven variant classification tools are reshaping genotyping workflows, with algorithms improving interpretation accuracy by up to 28% and reducing analysis time by 35%. Laboratories integrating AI-assisted quality filtering report significantly enhanced throughput while processing more than 2 million SNP calls per batch, accelerating clinical and research applications.

Multi-Omics Integration Driving Workflow Expansion: SNP genotyping is increasingly combined with transcriptomics and epigenomics, enabling deeper biological insights. Multi-omics workflows have grown by 42% in institutional adoption, allowing researchers to analyze up to 3× more biological parameters per sample. This trend supports broader use in oncology, immunology, and agricultural biotechnology.

Automation and High-Throughput Platforms Accelerating Output: Automated SNP genotyping platforms now deliver 50–60% reductions in labor time and achieve throughput exceeding 10,000 samples per run, supporting large biobank projects. Automated liquid-handling systems have expanded adoption in Europe and Asia, where efficiency-driven genomics programs are scaling rapidly.

Expansion of Population-Scale Genomics Initiatives: More than 35 national genome programs now integrate SNP genotyping to map disease susceptibility and population diversity. Participation rates have grown by 25% annually, enabling datasets exceeding 20 million SNP profiles. These initiatives support drug discovery, heritage mapping, and public-health surveillance.

The Single Nucleotide Polymorphism (SNP) Genotyping Market is segmented across type, application, and end-user categories, reflecting the broad integration of genotyping technologies in healthcare, agriculture, biotechnology, and research domains. Type-based segmentation is driven by the adoption of high-throughput platforms and demand for rapid, cost-efficient variant identification across diverse samples. Application segmentation is shaped by rising utilization in diagnostics, pharmacogenomics, and crop improvement programs, supported by expanding institutional uptake. End-user analysis highlights robust adoption among research institutes, clinical laboratories, and agricultural genomics centers as they increasingly rely on automated workflows, AI-enabled variant calling, and scalable microarray and sequencing systems. Together, these segmentation layers demonstrate a market that is technologically intensive, application-diverse, and aligned with global investments in genetic science and precision-driven research initiatives.

The SNP genotyping landscape comprises several major technology categories, each fulfilling distinct analytical and operational needs across clinical, research, and agricultural workflows. Microarray-based SNP genotyping currently leads the market with nearly 41% adoption, supported by its cost efficiency and ability to analyze hundreds of thousands of variants simultaneously. Sequencing-based genotyping accounts for approximately 33%, though its adoption rate is accelerating rapidly due to growing demand for high-accuracy variant detection and scalable automation capabilities. Digital PCR platforms are the fastest-growing type, expanding at an estimated 14–16% annual growth rate, driven by their exceptionally high sensitivity for detecting low-frequency alleles and their increasing use in oncology, infectious disease monitoring, and crop trait validation. Additional types—such as mass spectrometry–based genotyping, TaqMan assays, and single-tube chemistry methods—collectively represent 26% of the market, serving niche applications where specificity, rapid turnaround, or targeted variant analysis are essential.

SNP genotyping serves a wide spectrum of applications, with diagnostics and clinical genomics representing the leading segment at about 44% of total adoption, driven by increased reliance on genotype-guided therapy selection and early disease detection. Agricultural biotechnology accounts for nearly 27%, while drug discovery and development contributes around 18%. However, pharmacogenomics is the fastest-growing application, expanding at an estimated 15–18% annual growth rate, supported by advancements in personalized medicine, increased payer acceptance of genomic testing, and the proliferation of large-scale population genomics programs. Remaining applications—including microbial typing, ancestry analysis, and biomarker validation—collectively account for 11% of the market and continue to gain traction among research and commercial entities. In 2024, more than 39% of healthcare enterprises globally reported piloting SNP-integrated diagnostic systems to enhance clinical decision-making. Additionally, over 52% of plant-genetics laboratories adopted SNP-based workflows to accelerate hybrid development programs.

Research institutions constitute the largest end-user segment, accounting for approximately 46% of total market adoption, supported by extensive academic funding, population-scale genomic programs, and demand for high-throughput variant analysis platforms. Clinical and diagnostic laboratories follow with a 32% share, while agriculture and livestock genomics centers maintain around 16% adoption. Pharmaceutical and biotechnology companies represent the fastest-growing end-user group, expanding at an estimated 13–15% growth rate, as SNP genotyping becomes integral to drug target validation, clinical trial optimization, and biomarker-driven therapeutic design. The remaining end-users—including forensic laboratories, contract research organizations (CROs), and personalized wellness companies—collectively hold 6% of the market, contributing to specialized applications such as ancestry mapping, trait analysis, and molecular verification. Industry adoption trends reinforce this momentum: In 2024, more than 41% of global research universities integrated automated SNP platforms to accelerate genetics-based curricula and research outputs. Additionally, over 34% of clinical laboratories in the US adopted hybrid sequencing-SNP workflows to improve diagnostic concordance and testing turnaround.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21.7% between 2025 and 2032.

The market distribution reflects strong demand dynamics across high-income healthcare systems, rapidly digitalizing emerging economies, and regions prioritizing precision medicine adoption. Europe captured around 27.5% share in 2024, driven by genomics research funding exceeding USD 4.3 billion. Asia-Pacific held approximately 24.1% share, supported by rapidly expanding genomic sequencing hubs in China, India, and Japan, which collectively processed over 18 million genotype samples in 2024. South America maintained a 6.5% share, while the Middle East & Africa accounted for 3.7%, reflecting early-stage adoption but rising investment in clinical genomics infrastructure. These regional variations highlight differences in healthcare expenditure, R&D capacity, regulatory maturity, and national genome programs, shaping the overall trajectory of the global Single Nucleotide Polymorphism (SNP) Genotyping Market.

North America accounted for approximately 38.2% of the global SNP genotyping market in 2024, supported by high adoption in healthcare, pharmaceuticals, biotechnology, and agriculture. The region benefits from strong regulatory frameworks, including updated FDA guidelines on genomic diagnostic validation and increased NIH funding crossing USD 51 billion in 2024. Advancements such as ultra-high-throughput sequencing, AI-assisted variant calling, and integrated bioinformatics platforms enhance regional market depth. Local players such as Thermo Fisher Scientific expanded sample-processing capacity to over 12 million genotyping assays, strengthening market penetration. Consumer behavior is shaped by high enterprise adoption in healthcare and finance sectors, where genomic data integration and personalized medicine are significantly more mainstream compared to other regions.

Europe held around 27.5% market share in 2024, led by major economies such as Germany, the UK, and France. The region benefits from strong regulatory oversight through the EMA and initiatives promoting standardized genomic workflows under the European Health Data Space (EHDS). Sustainability-driven digital infrastructure and precision medicine funding exceeding USD 4.3 billion contribute to rising adoption. The region is witnessing rapid integration of cloud-based genotyping analytics and AI-enabled variant interpretation. Local players, such as Qiagen in Germany, continue to expand mid-throughput assay portfolios to support hospital-based genetic testing. Consumer behavior emphasizes regulatory compliance and demand for explainable genomic insights, enhancing trust-driven adoption in clinical and research settings.

Asia-Pacific represented approximately 24.1% of global volume in 2024 and ranked as the fastest-growing region, led by China, India, and Japan. The region’s rapid growth is supported by large-scale genome sequencing programs, expanding biobanks, and increased manufacturing of microarray and sequencing reagents. China processed over 10 million genotyping samples in 2024 alone, while India surpassed 3 million due to expanding diagnostic networks. Japan continues to drive innovation through advanced medical imaging and AI-driven genomic analytics. Local players, such as BGI, are scaling high-throughput sequencing capabilities across regional hubs. Consumer behavior is heavily influenced by mobile-first digital adoption, e-commerce-driven diagnostics ordering, and strong interest in AI-integrated health platforms.

South America accounted for 6.5% of the global market in 2024, with Brazil and Argentina leading overall demand. The region is witnessing improvements in laboratory infrastructure, increased biotechnology investments, and adoption of genotyping in agricultural genomics and infectious disease surveillance. Government programs promoting bioeconomy development and reduced tariffs on genomic equipment are further supporting growth. Local diagnostic firms in Brazil have increased regional testing volumes to over 450,000 samples per year, contributing to market expansion. Consumer behavior shows increasing demand tied to media and language localization efforts, along with growing awareness of personalized medicine among urban populations.

The Middle East & Africa accounted for 3.7% of the global SNP genotyping market in 2024, led by the UAE, Saudi Arabia, and South Africa. Regional growth is driven by diversification from traditional oil and gas sectors into healthcare modernization, genetic disease research, and population-scale genome initiatives. Investments in genomic medicine centers and trade partnerships encouraging the import of high-throughput sequencing platforms are contributing to expanding adoption. Local players in the UAE have begun deploying AI-based bioinformatics tools capable of processing over 50,000 variant profiles annually. Consumer behavior trends show increasing acceptance of preventive genomics, influenced by rising chronic disease awareness and national health digitalization programs.

United States – 34.5% Market Share: Dominance supported by advanced R&D infrastructure and high adoption of precision medicine.

China – 18.9% Market Share: Leadership driven by large-scale genome sequencing capacity and expanding biotechnology manufacturing.

The Single Nucleotide Polymorphism (SNP) Genotyping market is moderately consolidated yet highly competitive, with 10–15 major active global competitors operating in instruments, consumables, and bioinformatics. The top 5 companies—Illumina, Thermo Fisher Scientific, QIAGEN, Bio-Rad Laboratories, and Agilent Technologies—together command around 50–55% of the market. These players leverage extensive R&D, diversified product lines, and broad global reach to maintain leadership.

Strategic initiatives are driving innovation and competitive differentiation. For example, Thermo Fisher continues to expand its genotyping assay portfolio through launches of high-multiplex TaqMan assays. Illumina is pushing deeper into high-throughput sequencing with cloud-connected analysis platforms. QIAGEN is growing its clinical genomics footprint via laboratory services acquisitions and data-analysis toolkits. Bio-Rad introduced a droplet digital PCR system tailored for SNP detection in liquid biopsy and single-cell contexts, enhancing sensitivity and enabling new use cases. Agilent is forming partnerships to integrate its genotyping hardware with cloud analytics infrastructure.

Beyond the top players, several specialized companies and startups are innovating around automation, microfluidics, bioinformatics, and AI-assisted variant calling. The presence of these firms, combined with the market share of the top five, reflects a moderately consolidated landscape: dominant players are defending their core platforms, while challengers push differentiation through niche innovation, lower-cost workflows, and integrated service models.

Illumina, Inc.

Agilent Technologies, Inc.

Roche Diagnostics

10x Genomics, Inc.

LGC Limited

Current and emerging technologies are reshaping the SNP genotyping market by addressing trade-offs between throughput, sensitivity, cost, and scalability. Microarray platforms remain a workhorse for high-density genotyping, enabling the simultaneous interrogation of hundreds of thousands of SNPs. These arrays are especially prevalent in genome-wide association studies (GWAS), population genetics, and agricultural breeding programs. Their integration with automated liquid handlers and robust bioinformatics pipelines significantly boosts throughput and operational efficiency.

Next-generation sequencing (NGS)–based genotyping is gaining ground because of its scalability and accuracy. Sequencing-based SNP detection supports discovery of rare or novel variants that microarrays may miss. Technological advancements—including benchtop sequencers, library-prep automation, and improved flow cells—are driving broader adoption, especially in research institutions and large biobanks. Real-time PCR (e.g., TaqMan) assays remain widely used for targeted SNP genotyping due to their simplicity, speed, and compatibility with existing laboratory infrastructure. These assays are especially favored in clinical diagnostics and pharmacogenomics, where specific SNPs guide therapeutic decisions. Digital PCR is emerging as a powerful tool for high-precision variant detection, particularly for low-frequency alleles, somatic mutations, and copy-number variants. Digital PCR platforms such as droplet-based systems provide high sensitivity and reproducibility, enabling clinical labs to push the boundaries of minimal residual disease monitoring and single-cell genotyping.

Other specialized technologies are also contributing to innovation. Mass spectrometry–based assays (e.g., MALDI-TOF) support medium- to high-throughput multiplexed genotyping, suitable for validation studies and custom panels. KASP (Kompetitive Allele-Specific PCR) is another flexible, cost-effective method with low error rates, making it attractive for crop breeding and research-focused genotyping. Emerging techniques like nanopore sequencing and CRISPR-based assays offer potential for rapid, portable, and amplification-free SNP detection, appealing for field diagnostics and decentralized testing. In parallel, the genomics space is seeing strong integration with cloud analytics, AI, and machine-learning algorithms, which accelerate variant calling, improve quality control, and streamline data workflows. Service providers are increasingly offering turnkey bioinformatics solutions, reducing the burden on labs with limited computational infrastructure. This technological convergence is enabling faster, more accurate, and scalable genotyping—making it viable for clinical, research, and agricultural applications.

In October 2024, Illumina launched two compact MiSeq i100 benchtop sequencers — an entry model priced at USD 49,000 and a higher-capacity i100 Plus at USD 109,000 — designed for faster in-house sequencing with 18 preconfigured programs and room-temperature reagent storage. Source: www.illumina.com

At AGBT 2024 (Feb 2024), 10x Genomics announced major product advancements across its three platforms (Chromium, Visium, Xenium), introducing upgrades that expand single-cell and spatial multi-omics throughput and enable higher-resolution analyses for drug discovery and translational research programs. Source: www.10xgenomics.com

On 31 October 2024, LGC Biosearch Technologies launched Amp-Seq One, a one-step targeted genotyping-by-sequencing workflow built for commercial breeding and applied genomics; the solution emphasizes reduced hands-on steps and faster turnaround for high-sample throughput breeding programs. Source: www.biosearchtech.com

On 31 July 2024, Thermo Fisher announced integration of its Axiom™ Human Genotyping Arrays with Allelica’s polygenic risk-score software, creating an end-to-end genotyping-to-PRS reporting workflow aimed at translating research genotyping into clinically actionable risk reports. Source: www.thermofisher.com

This SNP Genotyping Market Report provides a comprehensive, strategic analysis covering product types (instruments, reagents, consumables, software), technologies (microarray, NGS sequencing, digital PCR, mass spectrometry, KASP), applications (diagnostics, pharmacogenomics, agricultural genomics, research, microbial and ancestry testing), and end users (academic/research institutes, clinical labs, biotech/pharma companies, agricultural organizations, CROs, forensics). Geographically, the report spans major markets: North America, Europe, Asia-Pacific, South America, and Middle East & Africa—highlighting regional infrastructure maturity, regulatory environments, and genomics program adoption.

It also delves into innovation vectors such as AI-driven variant calling, cloud-native bioinformatics platforms, high-throughput automation, and portable sequencing systems. Emerging or niche segments are explored, including decentralized testing, field-deployable genotyping (e.g., nanopore-based), CRISPR-assay integration, and single-cell SNP analysis. The report examines competitive dynamics, profiling global industry leaders, smaller challengers, and their strategic initiatives—partnerships, product launches, M&A, and R&D direction.

Furthermore, the scope covers funding and investment trends in SNP genotyping infrastructure, reagent development, and bioinformatics, as well as the impact of national genome projects and public-private partnerships. It offers insights tailored to decision-makers in biotech, diagnostics, pharmaceuticals, agriculture, and genomics service provision, helping them understand where value is emerging, where risks lie, and how to align strategy with technological and market evolution.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,200.0 Million |

| Market Revenue (2032) | USD 15,398.4 Million |

| CAGR (2025–2032) | 21.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Thermo Fisher Scientific, QIAGEN, Bio‑Rad Laboratories, Illumina, Agilent Technologies, Roche Diagnostics, 10x Genomics, LGC Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |