Reports

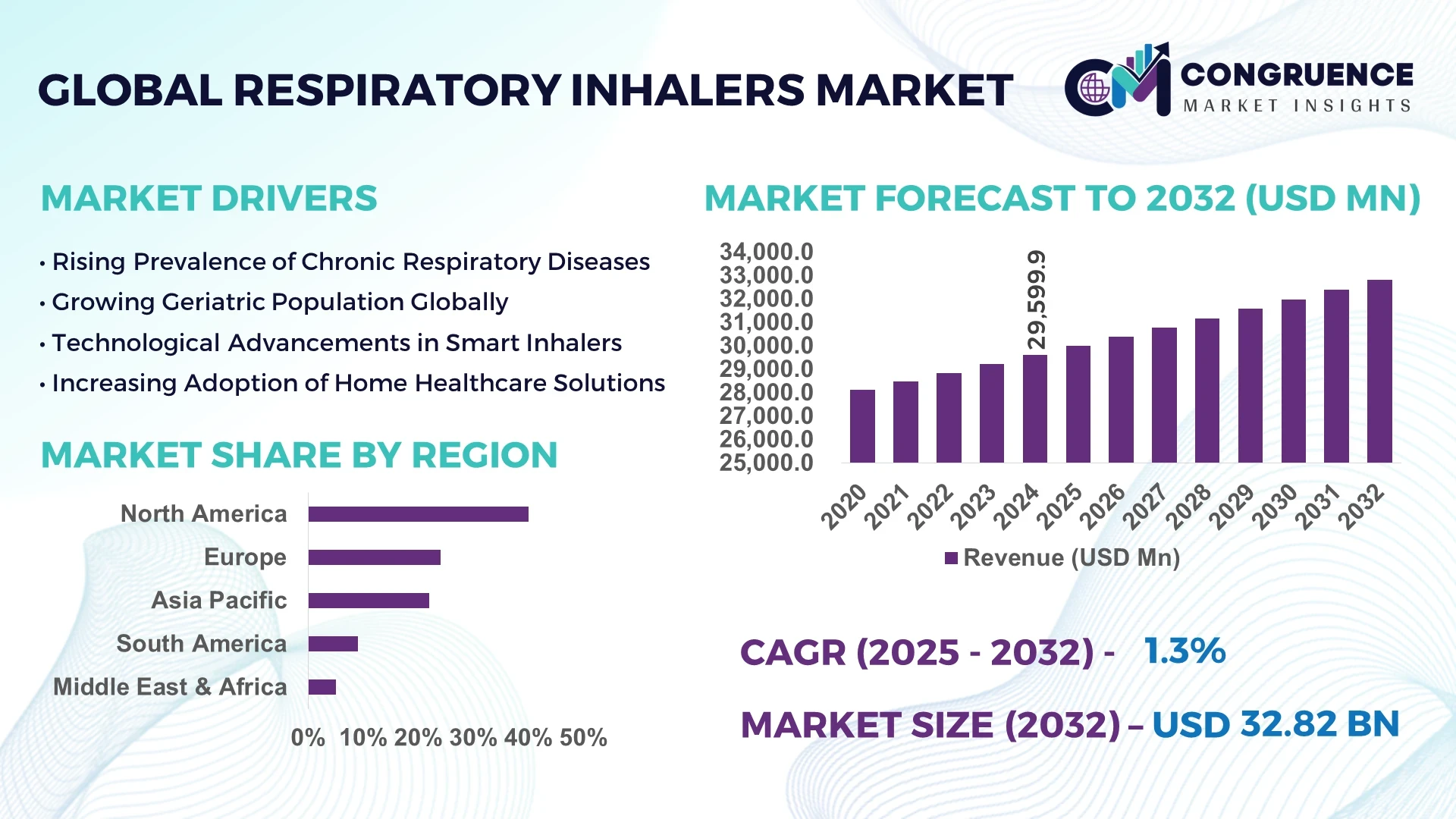

The Global Respiratory Inhalers Market was valued at USD 29,599.86 million in 2024 and is anticipated to reach USD 32,822.01 million by 2032, expanding at a CAGR of 1.3% between 2025 and 2032.

The respiratory inhalers market is undergoing significant growth due to the rising global burden of chronic respiratory diseases such as asthma, COPD, and cystic fibrosis. These conditions are becoming more prevalent due to urban pollution, tobacco use, and aging populations. Respiratory inhalers have become essential therapeutic tools, offering effective drug delivery directly to the lungs. The market is further fueled by innovations in device design, such as breath-actuated inhalers, digital smart inhalers, and user-friendly portable nebulizers. With increasing healthcare expenditure and improved patient awareness, especially in emerging economies, the demand for efficient, precise, and affordable inhalation therapy is at an all-time high. Pharmaceutical companies are investing in inhalable biologics and combination inhaler therapies, improving adherence and outcomes for patients suffering from respiratory ailments. As the trend shifts toward homecare respiratory solutions, the global respiratory inhalers market continues to witness expansion across both developed and developing regions.

Artificial Intelligence (AI) is revolutionizing the respiratory inhalers market by enhancing diagnosis, treatment personalization, and medication adherence. AI-enabled inhalers are capable of monitoring usage patterns, detecting inhalation technique errors, and transmitting real-time data to healthcare professionals for continuous treatment optimization. Smart inhalers, integrated with Bluetooth and cloud-based platforms, help patients manage their asthma or COPD by tracking dosage frequency and environmental triggers. In a clinical trial, smart inhalers integrated with AI improved medication adherence by over 60% and reduced emergency hospital visits by nearly 30%. AI-based predictive analytics are also being deployed to identify patients at risk of exacerbations, enabling early interventions and proactive care strategies.

Digital health platforms are increasingly used to personalize inhaler-based therapies based on patient lifestyle and behavior. This allows for dynamic dosage adjustments, reducing side effects and improving quality of life. AI's role in identifying patterns across vast datasets is proving critical for pharmaceutical companies conducting respiratory drug research. Additionally, remote patient monitoring through AI is becoming a standard feature in chronic care management programs. As regulatory approvals for AI-integrated devices become more streamlined, these smart inhalers are poised to reshape the future of respiratory care by combining precision, personalization, and preventive health management.

"In February 2025, Diag-Nose.io, a biotech company based in Victoria, Australia, announced the development of RhinoMAP, an AI-driven technology designed to personalize treatment for patients with chronic respiratory conditions, including asthma and COPD. RhinoMAP utilizes data from nasal liquid biopsy samples to match patients with the most effective medication based on their unique biological profiles."

The dynamics of the respiratory inhalers market are shaped by rapid technological advancements, increasing prevalence of respiratory disorders, and growing focus on self-administered drug delivery systems. As respiratory health becomes a key global concern, the demand for compact, efficient, and digitally enhanced inhalation devices is rising. Regulatory agencies are supporting innovation by fast-tracking approvals for smart inhalers and biologic therapies. Moreover, partnerships between medtech companies and pharmaceutical giants are driving product innovation and expanding market reach. With growing awareness and diagnosis rates, especially in rural and underserved regions, the respiratory inhalers market is witnessing a shift from hospital-based care to portable, home-use solutions.

Surge in Respiratory Disease Prevalence Globally

The rise in asthma and COPD cases is one of the biggest drivers in the respiratory inhalers market. According to the Global Burden of Disease Report, over 260 million people globally suffer from asthma, and COPD is the third leading cause of death worldwide. Environmental pollution, tobacco smoking, and occupational hazards are significantly contributing to this increase. In urban India and China, the prevalence of respiratory conditions has grown by more than 20% in the past five years. As these diseases require long-term medication through inhalation devices, the demand for both maintenance and rescue inhalers continues to surge. Inhalers are preferred due to their rapid action, targeted drug delivery, and patient convenience. Pharmaceutical manufacturers are responding by developing triple therapy inhalers and fixed-dose combinations, increasing their usage among chronic respiratory patients.

High Cost of Advanced Inhalers and Limited Access in Low-Income Regions

Despite their medical benefits, the high cost of advanced inhalers remains a key barrier. Smart inhalers with AI integration or digital trackers often cost significantly more than traditional MDIs or DPIs, limiting accessibility for patients in low-income regions. For example, in sub-Saharan Africa and parts of Southeast Asia, less than 15% of patients with chronic respiratory diseases can afford long-term inhalation therapy. Furthermore, the lack of healthcare infrastructure and professional training in rural areas results in incorrect inhaler use and low treatment adherence. Health systems in developing countries often prioritize acute care over chronic disease management, leading to underdiagnosis and undertreatment. Additionally, the limited presence of cold-chain logistics and retail pharmacies in remote areas affects the availability of certain inhalers, especially biologic-based ones that require specific storage conditions.

Rise in Home-Based Respiratory Treatment and Telemedicine Integration

The growing popularity of homecare respiratory solutions is creating new opportunities for inhaler manufacturers. As chronic respiratory patients increasingly seek convenience and independence, the demand for easy-to-use, portable inhalers has soared. Over 70% of COPD patients now prefer inhalers that support home use, particularly during recovery or long-term disease management. Integration of inhalers with telemedicine platforms is another major opportunity, especially in post-pandemic healthcare settings. With remote consultations becoming a norm, connected inhalers that transmit real-time data to doctors ensure continuous monitoring and timely intervention. Pharmaceutical companies are also exploring partnerships with digital health platforms to provide remote inhalation training and personalized medication reminders. This convergence of smart tech, eHealth platforms, and self-management tools is expected to unlock new growth avenues, especially in aging populations with limited mobility.

Device Misuse and Poor Adherence Rates

A major challenge in the respiratory inhalers market is poor inhaler technique and low medication adherence. Studies show that nearly 45% of asthma patients and over 60% of COPD patients use their inhalers incorrectly, compromising treatment efficacy. This leads to avoidable exacerbations, hospitalizations, and increased healthcare costs. The lack of standard inhaler training programs and limited patient education is particularly concerning in emerging economies and rural regions. Moreover, patients often skip doses due to side effects, forgetfulness, or device complexity, particularly with multi-step DPIs and SMIs. Even in developed countries, inconsistent usage and unreported errors hinder treatment outcomes. While smart inhalers attempt to solve this issue through reminders and usage tracking, their adoption remains low due to affordability issues. Addressing patient behavior, simplifying device design, and increasing awareness remain critical challenges for market growth.

The respiratory inhalers market is undergoing a major transformation driven by digital health integration, personalized medicine, and innovation in inhalation technology. One of the leading trends is the adoption of smart inhalers, which combine sensors, mobile apps, and cloud connectivity to optimize drug adherence and monitor patient outcomes. The global smart inhaler user base is expected to surpass 10 million by 2026. Breath-actuated and dose-controlled inhalers are also gaining popularity due to improved drug delivery precision and reduced wastage. Pharmaceutical companies are focusing on developing combination inhalers that include corticosteroids, bronchodilators, and anticholinergics to simplify therapy for COPD and asthma patients.

Sustainability is becoming another focus area, with manufacturers shifting from traditional propellants to eco-friendly alternatives. For example, hydrofluoroalkane-free MDIs are now being promoted to reduce the environmental impact of inhalers. There is also growing interest in dry powder inhalers due to their portability and longer shelf life, especially in humid climates. Additionally, AI-enabled inhalers and wearable respiratory monitors are being developed to offer predictive care, flagging early signs of exacerbation. These technology-driven trends are reshaping how patients and clinicians manage respiratory conditions, paving the way for a smarter, more connected future in inhalation therapy.

The respiratory inhalers market is broadly segmented by product type, application, and end-user insights, each reflecting critical dimensions of growth and innovation across the industry. In terms of type, the market features Metered Dose Inhalers (MDIs), Dry Powder Inhalers (DPIs), Soft Mist Inhalers (SMIs), Nebulizers (Jet, Ultrasonic, and Mesh), and next-generation Smart Inhalers. Each device type is tailored for different patient profiles, medication delivery preferences, and treatment durations. Application-wise, respiratory inhalers are primarily used for managing Chronic Obstructive Pulmonary Disease (COPD), Asthma, and Cystic Fibrosis. These conditions represent a substantial portion of global respiratory illness burdens, requiring long-term inhalation therapy. End-user insights reveal that hospitals and clinics dominate the current market share due to institutional purchasing power and emergency needs. However, the demand from homecare settings, retail pharmacies, and online channels is rising sharply, driven by the push toward patient-centric, digital-first, and home-based care models. This structured segmentation provides stakeholders with actionable insights to target key growth pockets, launch application-specific products, and expand geographically in the respiratory inhalers industry.

Metered Dose Inhalers (MDIs): Metered Dose Inhalers (MDIs) are among the most commonly used inhaler types globally, accounting for over 40% of market share as of 2024. These inhalers utilize chemical propellants to deliver aerosolized medication and are often used in rescue therapies for asthma and mild COPD. MDIs are favored for their affordability, portability, and fast-acting drug delivery. However, proper hand-breath coordination is essential for optimal performance, which can be challenging for children and elderly patients. In countries like India and Brazil, MDIs are heavily prescribed due to cost-effectiveness and widespread availability. Pharmaceutical companies are developing MDIs with built-in spacers and dose counters to improve compliance and usability.

Dry Powder Inhalers (DPIs): Dry Powder Inhalers (DPIs) deliver medication in powder form and are activated by the patient's own breath, making them environmentally safer by eliminating propellants. As of 2024, DPIs constitute approximately 30% of the global respiratory inhalers market. These devices are typically used for maintenance therapy in COPD and persistent asthma. Popular among adults and the elderly, DPIs are also ideal for regions with regulations discouraging propellant use. They are easy to handle and offer high lung deposition. Devices like Turbuhaler and Diskus are widely known in this segment. Despite their convenience, DPIs require sufficient inspiratory flow, limiting their use in patients with advanced respiratory compromise.

Soft Mist Inhalers (SMIs): Soft Mist Inhalers (SMIs) generate a fine, slow-moving mist without using propellants, offering superior lung deposition and reduced oropharyngeal drug loss. These inhalers are particularly suitable for elderly patients or those with low inspiratory capacity. SMIs make up roughly 10–12% of the total market. In 2024, usage rose notably in Europe and North America due to patient preference for smoother inhalation. The Respimat inhaler from Boehringer Ingelheim is a leading product in this category. SMIs are considered more efficient than MDIs and DPIs in drug absorption, though they are generally priced higher and less widely available in lower-income regions.

Nebulizers (Jet, Ultrasonic, Mesh): Nebulizers transform liquid medication into mist and are commonly used for severe respiratory cases and pediatric care. Jet nebulizers dominate the segment, though ultrasonic and mesh types are gaining traction due to portability and quieter operation. In 2024, nebulizers held a 15% global market share, with increased adoption in hospitals and homecare settings. Mesh nebulizers are becoming popular for their compact design and efficient drug delivery. These devices are vital in ICUs and emergency rooms for patients unable to operate handheld inhalers. Nebulizers are also being integrated into telemedicine kits for remote care of chronic respiratory patients.

Smart Inhalers (AI-integrated, Connected Devices): Smart inhalers represent the fastest-growing segment, driven by increasing demand for digital health solutions and patient monitoring. These devices use sensors, Bluetooth, and AI to track usage patterns, provide reminders, and share data with healthcare providers. In 2024, smart inhalers accounted for just under 5% of the market but are projected to double in the next 3–5 years. Companies like Propeller Health and Teva are at the forefront of development. Smart inhalers improve adherence by up to 60% and reduce hospital visits by more than 25%. Their integration into remote patient management platforms is transforming chronic disease care in asthma and COPD.

Chronic Obstructive Pulmonary Disease (COPD): COPD remains one of the primary drivers of inhaler demand worldwide, accounting for more than 50% of all inhaler prescriptions. In 2024, over 200 million people were estimated to suffer from COPD globally, with high prevalence in China, India, and the U.S. Patients often require a combination of bronchodilators and corticosteroids, delivered via MDIs, DPIs, or nebulizers. Long-acting maintenance therapies are the cornerstone of COPD treatment. The market has witnessed a growing preference for triple therapy combination inhalers, which enhance patient adherence and clinical outcomes. Inhalers for COPD must be intuitive and effective across different disease stages and physical capacities.

Asthma: Asthma affects over 260 million people globally and remains a leading cause of respiratory-related hospitalizations, especially among children and adolescents. Inhalers are the most effective method for delivering both controller and rescue medications in asthma management. MDIs and DPIs dominate asthma therapy, with smart inhalers gaining ground in pediatric and adolescent care for real-time monitoring. Inhaled corticosteroids and combination therapy are commonly used for chronic asthma, while short-acting beta-agonists provide rapid relief during attacks. In 2024, demand for inhalers tailored for pediatric use, including low-dose and ergonomic models, has risen sharply, reflecting a shift toward patient-specific inhalation design.

Cystic Fibrosis: Cystic Fibrosis is a rare yet life-threatening condition requiring consistent respiratory support. Inhalers, particularly nebulizers and mesh devices, are essential for delivering mucolytics and antibiotics directly to the lungs. As of 2024, there were over 100,000 diagnosed cases globally, with high concentration in North America and Europe. Nebulized treatments form a critical part of daily therapy for CF patients to prevent mucus buildup and reduce lung infections. The market is seeing innovation in portable nebulizers and aerosolized gene therapies. As life expectancy for CF patients increases due to advanced therapeutics, the demand for specialized inhalation devices continues to grow steadily.

Hospitals & Clinics: Hospitals and clinics remain the largest end-users in the respiratory inhalers market, accounting for over 45% of global sales in 2024. These institutions prioritize high-throughput devices like MDIs and nebulizers for acute care and emergency cases. In ICUs and outpatient departments, rapid medication delivery and ease of administration are critical, making conventional inhalers indispensable. Hospitals also often serve as the first point of diagnosis and prescription initiation. The demand is highest in tertiary care hospitals and urban centers where access to respiratory specialists is more prevalent. The growing hospitalization rates for respiratory infections and COPD are sustaining high inhaler procurement.

Homecare Settings: The rising trend of at-home respiratory management is significantly boosting inhaler demand in homecare settings. With the increasing burden of chronic respiratory illnesses, particularly among aging populations, home-use inhalers like DPIs, SMIs, and mesh nebulizers are becoming mainstream. In 2024, homecare contributed to nearly 25% of inhaler use globally. Patients prefer devices that are compact, reusable, and easy to operate. The shift toward telehealth and remote monitoring further supports this growth, with smart inhalers being deployed for continuous therapy without in-person visits. Manufacturers are also focusing on training modules and instructional packaging tailored for at-home patients.

Retail Pharmacies & Drug Store: Retail pharmacies play a pivotal role in over-the-counter and prescription-based inhaler distribution. In 2024, they accounted for 20% of all inhaler sales, particularly in urban and suburban regions. Pharmacist-guided device selection, medication counseling, and accessibility make these channels convenient for chronic patients. Pharmacies often stock a wide variety of brands and inhaler types, enabling consumer choice based on affordability and preferences. In developing countries, retail outlets are critical for dispensing essential asthma and COPD medication due to the limited reach of hospital infrastructure. Their role is further expanding through in-store clinics and pharmacist-driven patient education.

Online Pharmacies: Online pharmacies are rapidly emerging as a vital channel, particularly post-COVID, when digital health adoption surged. In 2024, online inhaler sales accounted for nearly 10% of the total market but are expected to grow at a double-digit rate. These platforms offer doorstep delivery, subscription-based refill models, and bundled inhaler packages. AI-based e-commerce algorithms assist patients in choosing the correct device based on prescription and historical behavior. Smart inhalers, in particular, are frequently purchased online due to their tech-savvy target audience. Online pharmacies also serve as critical access points in remote regions, helping bridge the gap between patients and essential respiratory care products.

North America accounted for the largest market share at 40% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

The North American market remains dominant, fueled by advanced healthcare infrastructure and a high prevalence of respiratory diseases such as asthma and COPD. Europe holds a significant market share, driven by an aging population and increasing healthcare access. Meanwhile, the Asia-Pacific region is anticipated to experience rapid growth due to rising healthcare investments and growing awareness. The Middle East and Africa are also expected to see growth, albeit at a slower pace.

Dominance of the U.S. Market and Growing Demand for Innovative Solutions

North America has consistently been the largest market for respiratory inhalers, owing to the high demand driven by the prevalence of asthma, COPD, and other respiratory conditions. The U.S. holds the majority of the market share, with millions of individuals affected by these conditions. Additionally, government initiatives to improve healthcare access, the availability of innovative inhaler technologies, and a strong regulatory framework supporting respiratory products all contribute to the region's dominance. The market benefits from extensive research and development in the healthcare sector, especially in the development of smart inhalers that track patient usage and provide more efficient delivery of medication.

Rising Awareness and Integration of Smart Technology

Europe’s respiratory inhalers market continues to grow steadily, driven by rising awareness about respiratory diseases, including asthma and chronic obstructive pulmonary disease (COPD). The market is significantly driven by healthcare systems in countries like Germany, the UK, and France, which offer easy access to medical devices and treatments. The rise in smoking-related diseases, urbanization, and increasing levels of air pollution in major cities have also contributed to the growth of this market. Furthermore, the integration of digital technology in respiratory inhalers, including smart inhalers with connectivity features, is gaining popularity across European nations. The regulatory environment in Europe is also supportive of advancements in medical devices, ensuring continued market expansion.

Rapid Growth in China, India, and Japan due to Increased Awareness

The Asia-Pacific region is poised to be a key growth area for the respiratory inhalers market, with countries like China, India, and Japan driving the demand. China has the largest share in the region, with its rapidly expanding healthcare system and increasing focus on managing respiratory diseases. India’s market is expanding due to high pollution levels and a growing patient base suffering from respiratory ailments. In Japan, the market is supported by an aging population and high healthcare spending. Additionally, with increased healthcare access and awareness programs, the demand for inhalers is expected to surge in developing countries in the region. The rising number of smokers and environmental factors are anticipated to further drive market growth.

Growing Healthcare Access Amidst Rising Air Pollution

The Middle East & Africa respiratory inhalers market is witnessing steady growth, primarily driven by increasing cases of respiratory diseases in both developed and developing regions. Countries like Saudi Arabia, the UAE, and South Africa are seeing higher adoption rates due to rising pollution levels and greater healthcare awareness. The demand for respiratory inhalers is particularly high among urban populations in the Middle East, where high levels of air pollution and sedentary lifestyles contribute to asthma and other respiratory conditions. In Africa, while healthcare infrastructure may vary, growing access to treatment and the awareness of respiratory conditions are gradually improving, contributing to a rise in inhaler usage.

The respiratory inhalers market is highly competitive, with several key players dominating the market landscape. Companies such as GlaxoSmithKline, AstraZeneca, and Boehringer Ingelheim are major contributors, offering a wide range of inhaler products for both asthma and COPD management. These companies focus on continuous innovation, with advancements in inhaler technology, including the development of dry powder inhalers (DPIs), metered-dose inhalers (MDIs), and smart inhalers that track medication use. The market is also influenced by generic inhaler products, as pharmaceutical companies look to capture a larger share of the growing demand from emerging markets. With regulatory approvals and partnerships between key stakeholders in the healthcare and pharmaceutical sectors, the competition is expected to intensify as new technologies and products emerge.

GlaxoSmithKline

AstraZeneca

Novartis

Boehringer Ingelheim

Merck

Pfizer

Cipla

Teva Pharmaceuticals

Mylan

Sun Pharmaceutical Industries

The technology behind respiratory inhalers has evolved significantly in recent years, with a strong focus on improving drug delivery systems and patient adherence. Innovations in inhaler technology include the development of dry powder inhalers (DPIs), which provide a more efficient delivery of medication, and metered-dose inhalers (MDIs) with enhanced ease of use. The integration of smart inhalers, which feature sensors to track usage and provide feedback to healthcare providers, is one of the key technological advancements in the market. These devices help ensure better patient compliance, particularly for those with chronic conditions. Additionally, digital platforms that sync with smart inhalers are enhancing patient management by allowing real-time monitoring of inhaler use, offering personalized insights, and promoting more precise drug delivery. With advancements in inhaler design, the industry is expected to focus more on minimizing the environmental impact of inhalers, such as reducing propellant-based inhalers that contribute to greenhouse gas emissions. These technological strides are making respiratory treatments more effective, personalized, and environmentally friendly.

In March 2024, GlaxoSmithKline (GSK) announced it would cap out-of-pocket costs for its asthma and chronic obstructive pulmonary disease (COPD) inhalers at $35 per month for eligible U.S. patients starting in January 2025. This move is designed to improve medication affordability and accessibility for U.S. patients.

In June 2024, Boehringer Ingelheim launched an initiative to reduce the out-of-pocket costs for its inhalers to $35 per month for eligible patients. This comes after rising concerns about the affordability of inhalers in the U.S.

In August 2023, AstraZeneca unveiled its plan to invest an additional $250 million in its asthma inhaler manufacturing plant in Qingdao, China. This investment aims to increase production capacity to meet growing demand in the Asia-Pacific region, particularly in China and India.

In February 2023, Aptar Pharma launched HeroTracker® Sense, a digital health solution that transforms metered-dose inhalers (pMDIs) into smart connected devices. This innovation aims to enhance medication adherence by offering real-time tracking and reminders.

In January 2023, the U.S. FDA approved Airsupra, a new combination inhaler by AstraZeneca. Airsupra is designed for asthma patients and combines albuterol and budesonide in a single rescue medication. This is the first such inhaler to be approved in this category.

The Respiratory Inhalers Market Report provides a comprehensive analysis of the market, focusing on various aspects such as product types, applications, end-users, and geographical regions. The report examines trends and dynamics influencing the market, including the growing adoption of smart inhalers, which integrate technology to improve patient adherence to prescribed therapies. In terms of products, metered-dose inhalers (MDIs) and dry powder inhalers (DPIs) remain prominent, with innovation in digital health tools driving new product developments. The report also covers the increasing prevalence of respiratory diseases like asthma and COPD, contributing to the rising demand for inhalers. The market is segmented by product type, including MDIs, DPIs, and nebulizers, each serving different patient needs. It also explores the competitive landscape, highlighting key players such as GlaxoSmithKline, Boehringer Ingelheim, and AstraZeneca, among others. Regulatory and reimbursement policies are also evaluated, as they impact market penetration, particularly in emerging markets. The geographical analysis includes North America, Europe, Asia-Pacific, and the Middle East & Africa, showcasing regional market trends, with North America leading the market due to high demand in the U.S. and Canada. Emerging markets in Asia-Pacific and Africa are expected to see significant growth as healthcare systems improve and awareness of respiratory diseases rises.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 29599.86 Million |

|

Market Revenue in 2032 |

USD 32822.01 Million |

|

CAGR (2025 - 2032) |

1.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GlaxoSmithKline, AstraZeneca, Novartis, Boehringer Ingelheim, Merck, Pfizer, Cipla, Teva Pharmaceuticals, Mylan, Sun Pharmaceutical Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |