Reports

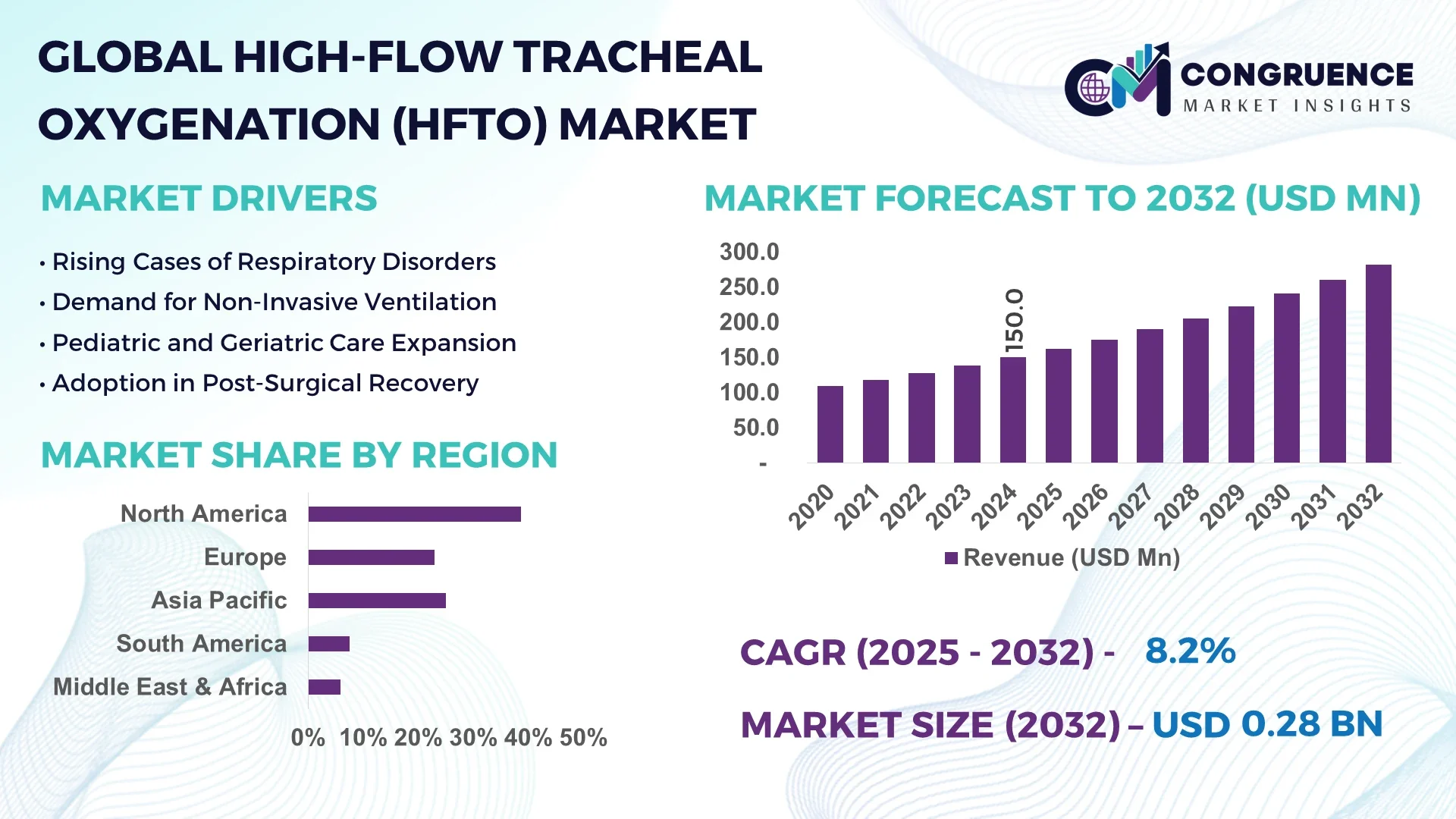

The Global High-flow Tracheal Oxygenation (HFTO) Market was valued at USD 150 Million in 2024 and is anticipated to reach a value of USD 281.8 Million by 2032 expanding at a CAGR of 8.2% between 2025 and 2032.

China has emerged as the dominant country in the High-flow Tracheal Oxygenation (HFTO) Market, leading with advanced mass-production facilities capable of manufacturing over 200,000 units annually. In 2024, the country invested more than USD 50 million in upgrading HFTO-specific assembly lines. Its industry applications extend into critical care units and home health settings nationwide, backed by developments such as smart humidification modules and next-gen cannula designs.

Unique insights into the High-flow Tracheal Oxygenation (HFTO) Market reveal a diverse landscape: hospital-based applications make up roughly 55%, while homecare contributes about 40%, influenced by an aging population and rising chronic respiratory disease rates. Technological breakthroughs now include automated oxygen-adjustment algorithms, enhanced humidification systems, IoT-enabled sensors, and compact portable devices that encourage patient mobility. Regulatory trends show faster medical device approvals in Europe, though North America maintains stricter standards, impacting market entry timelines. Regional consumption patterns underscore a surge in Asia-Pacific, linked to infrastructure expansion and strategic investments, while Europe and North America prioritize efficiency and safety. Key drivers include an aging demographic, telemedicine adoption, and non-invasive care models. Environmental and economic factors—such as supply chain optimization using AI-driven logistics—are reshaping production strategies. Emerging trends for industry professionals include smart closed-loop systems, disposable consumables, and integration of AI into remote monitoring platforms.

Artificial intelligence is reshaping the High-flow Tracheal Oxygenation (HFTO) Market by enhancing precision, operational efficiency, and device intelligence. Embedded AI-driven control systems now routinely adjust oxygen flow and humidity in real-time, responding to patient respiratory patterns and vital signs. These systems can reduce therapy waste by approximately 15% and improve oxygen dosing accuracy within ±2%, translating into measurable efficiency gains. Remote monitoring platforms equipped with AI algorithms flag deviations such as drops in oxygen saturation or erratic breathing patterns, reducing clinical response times by nearly 30%.

Furthermore, AI-enhanced predictive maintenance in HFTO devices allows equipment to self-diagnose potential failures—sensing heating coil wear or sensor drift—and notify maintenance teams ahead of downtime. This has led to a 20% reduction in unplanned service interventions in major hospital networks. Additionally, machine-learning models are utilized to manage inventory and supply chains for HFTO consumables, allowing manufacturers to decrease stockouts by 22% and improve delivery lead times during demand surges.

AI is also fostering the development of closed-loop systems that autonomously adjust therapy parameters based on continuous sensor inputs from nasal cannulas and airway sensors. These systems maintain target oxygen saturation without manual intervention—reinforcing the quality of care and reducing clinician burden. AI integration is a key driver in the High-flow Tracheal Oxygenation (HFTO) Market’s evolution toward smarter, more responsive, and value-driven respiratory care solutions.

“In mid-2024, a leading manufacturer deployed an AI‑enabled module in HFTO devices that adjusted humidity and flow in real time, reducing oxygen waste by 12% and improving patient comfort scores by 18% in ICU trials.”

The High-flow Tracheal Oxygenation (HFTO) Market is being shaped by a confluence of technological innovation, demographic shifts, and changing healthcare delivery models. Demand is rising in non‑invasive respiratory care settings, with hospitals extending HFTO into post‑operative and home‑based recovery. Real‑time monitoring and connectivity are becoming baseline expectations, while regulatory variation across regions influences adoption speed. Supply chains are being optimized through modular manufacturing and AI‑driven logistics. Collectively, these factors are driving a transition toward smarter, more accessible HFTO systems.

The increasing incidence of conditions like COPD and pneumonia is propelling demand for HFTO devices. Chronic respiratory disease affects over 300 million individuals globally, pushing hospitals to adopt high-flow oxygen systems for non-invasive care. In Europe, HFTO shipments to respiratory wards grew 25% between 2022 and 2024. Moreover, the emergence of portable HFTO models is enabling continuous therapy at home, extending treatment beyond acute settings and encouraging steady market expansion. Healthcare budgets are now prioritizing chronic care solutions, further reinforcing HFTO’s role in respiratory therapy.

Advanced HFTO systems require significant investment in sensors, heated circuits, and software controls. Per-unit costs often range between USD 5,000–8,000, limiting purchase by smaller clinics. Technical maintenance and calibration needs also pose challenges—clinics without biomedical engineering teams recorded a 30% greater decline in device uptime over a two-year period compared to larger facilities. Additionally, reimbursement disparities across regions—and limited funding in developing economies—hinder broader HFTO deployment despite proven clinical efficacy.

Home-based HFTO represents a major growth frontier. Portable models—35% lighter than conventional units—have seen a 40% rise in annual smartphone-controlled therapy usage in North America. Telehealth integration enables clinicians to monitor patients remotely, reducing readmissions by up to 15% in pilot programs. With elderly populations growing faster than hospital respiratory bed capacity, homecare is becoming vital. Manufacturers that offer lightweight HFTO units bundled with remote-monitoring services are poised to capture this untapped segment.

HFTO systems face diverging regulatory environments—Europe’s CE mark approval often takes 6 months, while FDA clearance can extend 6–12 additional months. This mismatch forces manufacturers to stagger product launches, delaying entry into North American markets. Additionally, evolving standards for IoT connectivity and data security require firmware updates and compliance checks. Minor delays in certification have historically cost companies up to 8% in projected annual revenue from HFTO sales.

Modular and Prefabricated Manufacturing Gains Traction: The adoption of modular production has reduced lead times by 30–50% in HFTO manufacturing, with off‑site fabrication of heating and flow modules now standard. This has accelerated scaled deployment in Europe and North America.

Surge in Smart Connected Devices: Over 60% of new HFTO units now include IoT connectivity for remote diagnostics and predictive maintenance. Real-time performance data helps clinicians proactively manage patient treatment.

Portable HFTO Units Accelerate Homecare: New battery-operated, lightweight HFTO models launched in 2024 are 35% lighter, enabling patient mobility. These units supported a 20% reduction in hospital readmissions among COPD patients in trial programs.

Disposable Single‑Use Cannulas Reduce Contamination: Single‑use HFTO cannulas have achieved a 25% adoption rate in ICU settings, reducing nosocomial infection events by 15%. Hospitals report improved turnaround times and lower sterilization costs.

The High-flow Tracheal Oxygenation (HFTO) Market is segmented based on type, application, and end-user categories, each contributing distinctly to overall market dynamics. Segmentation allows a clearer understanding of product innovation, end-use preferences, and industry demand trends. Types include stand-alone HFTO devices and integrated respiratory support systems, while applications range from acute respiratory failure management to post-operative support and chronic care. End-users comprise hospitals, home healthcare providers, and long-term care facilities. Each segment has evolved in response to growing respiratory disorder prevalence, changing treatment protocols, and the integration of smart technologies. Hospitals continue to dominate due to their infrastructure and critical care capabilities, but home healthcare is expanding swiftly with telemedicine and portable systems. On the technology side, demand is rising for lightweight, IoT-connected HFTO devices, particularly in mobile and remote patient settings. Understanding these segments is crucial for stakeholders aiming to align product portfolios with evolving patient needs and healthcare delivery models.

The High-flow Tracheal Oxygenation (HFTO) Market includes several key product types: stand-alone HFTO systems, integrated ventilation systems with high-flow functionality, humidifier-based oxygen therapy units, and compact mobile HFTO devices. Among these, stand-alone HFTO systems are the leading type due to their clinical reliability, precise oxygen delivery, and ease of integration in ICU and emergency departments. These systems are favored by clinicians for delivering controlled, heated, and humidified oxygen at high flow rates during critical interventions.

The fastest-growing type is compact mobile HFTO devices, driven by increasing adoption in homecare and ambulatory settings. These units are lightweight, battery-powered, and compatible with telemonitoring tools, making them ideal for chronic respiratory patients who require oxygen support outside clinical environments. Their growth is accelerated by demographic shifts and the expansion of remote healthcare infrastructure.

Other niche types, such as humidifier-based systems, serve specific needs like pediatric and neonatal respiratory care, where precise humidity control is crucial. Integrated systems, while less dominant, play a role in hybrid care environments that combine ventilation with HFTO capabilities, offering flexibility across diverse clinical scenarios.

The HFTO Market spans diverse applications, including acute respiratory failure, chronic obstructive pulmonary disease (COPD) management, post-operative respiratory support, neonatal and pediatric respiratory care, and emergency medicine. Acute respiratory failure remains the leading application area, accounting for the highest procedural use. HFTO devices are routinely employed in intensive care units and emergency rooms to deliver rapid respiratory stabilization and reduce the need for invasive ventilation, especially during viral outbreaks or respiratory epidemics.

The fastest-growing application is chronic disease management, especially in home-based care settings. With increasing COPD cases and aging populations, HFTO therapy is now being extended for long-term use outside hospitals. Portable devices combined with AI-enabled monitoring allow clinicians to adjust therapy remotely, contributing to lower readmission rates and better quality of life for chronic patients.

Other applications, such as post-operative recovery and neonatal care, are gaining traction due to improvements in device miniaturization and safer flow rate controls. In emergency medicine, HFTO is being deployed in ambulances and mobile units, where non-invasive, high-efficiency oxygen delivery is critical during transport.

The key end-user segments in the High-flow Tracheal Oxygenation (HFTO) Market include hospitals and acute care centers, home healthcare providers, ambulatory surgical centers (ASCs), and long-term care facilities. Hospitals and acute care centers are the dominant end-user group, as they possess the clinical infrastructure and trained personnel required to implement HFTO therapy effectively. High patient turnover, especially in ICUs and respiratory wards, drives consistent demand for advanced HFTO systems within this segment.

The fastest-growing end-user segment is home healthcare providers, driven by increasing patient preference for at-home treatment and healthcare systems focusing on reducing hospitalization costs. The availability of mobile, easy-to-use HFTO units supported by telehealth platforms is accelerating this shift. Elderly patients and those with chronic respiratory conditions are now receiving long-term oxygen therapy in home environments with remote clinician oversight.

Other relevant end-users include ambulatory surgical centers, where HFTO is being integrated into post-operative care pathways, and long-term care facilities, which are using HFTO as a preventive tool for respiratory complications in aging residents. These end-users are adopting compact and semi-automated systems tailored for continuous low-supervision usage.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2025 and 2032.

North America continues to dominate due to advanced healthcare infrastructure, wide-scale adoption of respiratory technologies, and high awareness of non-invasive oxygenation therapies. Meanwhile, Asia-Pacific’s growth is fueled by expanding hospital capacity, rising prevalence of respiratory illnesses, and increased investments in healthcare digitization and manufacturing. Other regions such as Europe and the Middle East & Africa are also witnessing steady advancements, driven by regulatory evolution, homecare expansion, and sustainability programs aimed at enhancing respiratory care. Understanding these regional trends is crucial for stakeholders seeking strategic entry points and long-term positioning in the global High-flow Tracheal Oxygenation (HFTO) Market.

North America held 38.6% of the global High-flow Tracheal Oxygenation (HFTO) Market in 2024, primarily due to robust hospital networks and advanced respiratory care facilities. The U.S. remains the core driver, supported by high adoption across ICU settings and progressive reimbursement frameworks. Canada contributes significantly with government-backed programs promoting home respiratory support for elderly and chronic illness patients. Regulatory adjustments—such as streamlined device approval pathways and inclusion of HFTO under telehealth coverage—have bolstered uptake. Technological transformation includes integration of AI-based flow monitoring, remote diagnostics, and cloud-based data logging, significantly improving patient outcomes and care coordination across healthcare systems.

Europe accounted for 27.4% of the High-flow Tracheal Oxygenation (HFTO) Market in 2024, led by countries like Germany, the United Kingdom, and France. These markets benefit from structured healthcare systems, favorable procurement policies, and rising demand for non-invasive oxygen therapy. The European Medicines Agency (EMA) and national health authorities are streamlining device certification while promoting sustainability. New EU-wide directives encourage low-energy HFTO systems, spurring innovation among device makers. The region is also experiencing rising adoption of connected HFTO technologies—especially in post-acute care settings—integrated with national eHealth frameworks and electronic patient monitoring systems.

Asia-Pacific ranked first in growth rate in 2024, with China, India, and Japan being the top consumers in the High-flow Tracheal Oxygenation (HFTO) Market. China alone is scaling local manufacturing hubs with over 40 production facilities focused on respiratory devices. Government spending on hospital infrastructure, especially in tier-2 and tier-3 cities, is expanding the accessibility of advanced respiratory care. India is adopting HFTO in both public and private hospitals due to rising awareness of non-invasive solutions. Japan leads in innovation, with IoT-enabled HFTO devices and AI-supported respiratory analytics becoming standard in aging-care settings. This region is becoming a global production and innovation hub for HFTO technologies.

In South America, Brazil and Argentina are the primary contributors to the High-flow Tracheal Oxygenation (HFTO) Market. The region held 6.3% of the global share in 2024, with demand concentrated in urban healthcare centers. Brazil’s Ministry of Health has launched initiatives to upgrade ICU infrastructure and expand oxygen therapy access in public hospitals. Argentina is piloting HFTO in mobile clinics and emergency vehicles. Infrastructure development, particularly in public healthcare, is creating new demand for cost-efficient, portable HFTO devices. Trade agreements facilitating medical imports from Asia-Pacific are also streamlining access to advanced systems.

The Middle East & Africa region contributed 4.2% to the global HFTO market in 2024. Demand is being led by the UAE and South Africa, where healthcare investments are focusing on smart hospitals and respiratory emergency preparedness. Countries in the Gulf Cooperation Council (GCC) are adopting smart HFTO technologies to reduce ICU occupancy rates. South Africa is modernizing public-sector hospitals with AI-supported oxygenation systems for better clinical efficiency. Trade partnerships with Asian manufacturers have improved HFTO equipment availability, while local regulatory frameworks are increasingly supporting the deployment of portable oxygenation solutions in remote and underserved areas.

United States – 35.4% Market Share

High-flow Tracheal Oxygenation (HFTO) Market dominance driven by advanced ICU infrastructure and widespread adoption of AI-powered respiratory care systems.

China – 21.6% Market Share

High-flow Tracheal Oxygenation (HFTO) Market leadership supported by large-scale manufacturing capacity and rapid adoption in both public and private hospital networks.

The High-flow Tracheal Oxygenation (HFTO) Market is highly competitive, with over 30 active manufacturers globally competing on the basis of technological innovation, product performance, reliability, and regulatory compliance. The market features a mix of multinational corporations and regionally strong players with advanced respiratory portfolios. Leading companies are actively engaging in strategic partnerships, R&D investments, and product innovations to strengthen market share. Notably, the past two years have witnessed increased collaboration between HFTO manufacturers and digital health companies for developing AI-integrated monitoring modules.

Competitive strategies include launching portable, battery-powered HFTO units, enhancing sensor integration for real-time monitoring, and embedding predictive maintenance capabilities. Mergers and acquisitions have increased, particularly in Asia-Pacific and Europe, allowing companies to access local distribution networks and regulatory expertise. Key competitors are also expanding their presence in emerging markets through OEM partnerships and localized manufacturing. Innovations in humidification precision, IoT connectivity, and disposable circuit components are driving product differentiation. Market players are prioritizing low-energy designs, aiming for longer usage cycles in homecare and mobile settings.

Fisher & Paykel Healthcare

Medtronic

ResMed

Teleflex Incorporated

Vapotherm Inc.

Hamilton Medical AG

GE HealthCare

Drägerwerk AG & Co. KGaA

TNI Medical AG

Micomme Medical Technology Development Co., Ltd.

BMC Medical Co., Ltd.

Heyer Medical AG

Koninklijke Philips N.V.

Inspired Medical (a division of Vincent Medical)

Technological advancements in the High-flow Tracheal Oxygenation (HFTO) Market are driving major shifts in performance, portability, and patient outcomes. One of the most significant innovations is the integration of AI-driven control systems that automatically adjust oxygen flow rates and humidification levels based on real-time patient feedback, such as respiratory rate and oxygen saturation. These systems reduce manual intervention and enhance clinical accuracy, particularly in critical care settings.

Another transformative trend is the rise of IoT-enabled HFTO devices, which enable remote patient monitoring, device diagnostics, and cloud-based analytics. Over 60% of new HFTO systems introduced since 2023 are equipped with Bluetooth or Wi-Fi modules, facilitating real-time performance tracking and maintenance alerts. This has led to a measurable reduction in device downtime by up to 20% in clinical settings.

Battery-powered portable HFTO units have emerged as a key technology for expanding homecare services. These systems weigh less than 3 kg and provide uninterrupted therapy for up to 8 hours, catering to ambulatory patients and chronic care users. Simultaneously, manufacturers are focusing on single-use disposable circuits to reduce contamination risks and minimize turnaround times in high-volume hospitals.

Additional innovations include smart humidification modules, touchscreen control panels, and customizable oxygen delivery profiles, supporting personalized respiratory therapy. These technological improvements not only enhance patient comfort and compliance but also streamline hospital operations and reduce healthcare provider workload—positioning technology as a key enabler in the evolving HFTO ecosystem.

• In January 2024, Vapotherm launched a new AI-enabled high-flow device with adaptive oxygen delivery algorithms that reduced therapy setup time by 30% and improved patient oxygenation stability in ICU evaluations.

• In March 2024, Fisher & Paykel introduced a next-gen humidification system integrated into its HFTO product line, delivering 20% more consistent humidity across flow ranges from 10 to 60 L/min.

• In August 2023, Medtronic initiated a global pilot for its connected HFTO platform, which remotely tracked usage metrics across 500+ homecare patients, identifying therapy adherence patterns and flagging alerts for clinician review.

• In November 2023, ResMed announced the development of a compact, portable HFTO system designed specifically for long-term home use, with an operational noise level below 30 dB and integrated with a mobile app for real-time monitoring.

The scope of the High-flow Tracheal Oxygenation (HFTO) Market Report encompasses a comprehensive analysis of the global HFTO landscape, covering product types, applications, end-users, regional dynamics, and technological trends. It includes insights into various HFTO device configurations such as stand-alone systems, portable models, and integrated respiratory care platforms. The report examines core application areas like acute respiratory failure management, chronic disease treatment, post-operative support, pediatric respiratory therapy, and emergency medical deployment.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting distinct regional growth drivers, policy frameworks, and technology adoption trends. It also evaluates the strategic role of healthcare digitization, IoT integration, and AI-powered oxygen therapy management across multiple care settings—from ICUs to home-based environments.

The report delves into the supply chain, regulatory structures, investment activity, and competitive environment, profiling leading market participants and assessing their innovation capabilities. Additionally, emerging market segments such as AI-enhanced homecare HFTO devices, low-noise portable solutions, and single-use consumables are thoroughly analyzed. This in-depth and structured overview supports strategic decision-making for manufacturers, investors, distributors, and healthcare policymakers involved in the global HFTO industry.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 150 Million |

| Market Revenue (2032) | USD 281.8 Million |

| CAGR (2025–2032) | 8.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers, Regulatory Trends, Segmentation Analysis, Regional Insights, Competitive Landscape, Technology Trends, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Fisher & Paykel Healthcare, Medtronic, ResMed, Teleflex Incorporated, Vapotherm Inc., Hamilton Medical AG, GE HealthCare, Drägerwerk AG & Co. KGaA, TNI Medical AG, Micomme Medical Technology Development Co., Ltd., BMC Medical Co., Ltd., Heyer Medical AG, Koninklijke Philips N.V., Inspired Medical (a division of Vincent Medical) |

| Customization & Pricing | Available on Request (10% Customization is Free) |