Reports

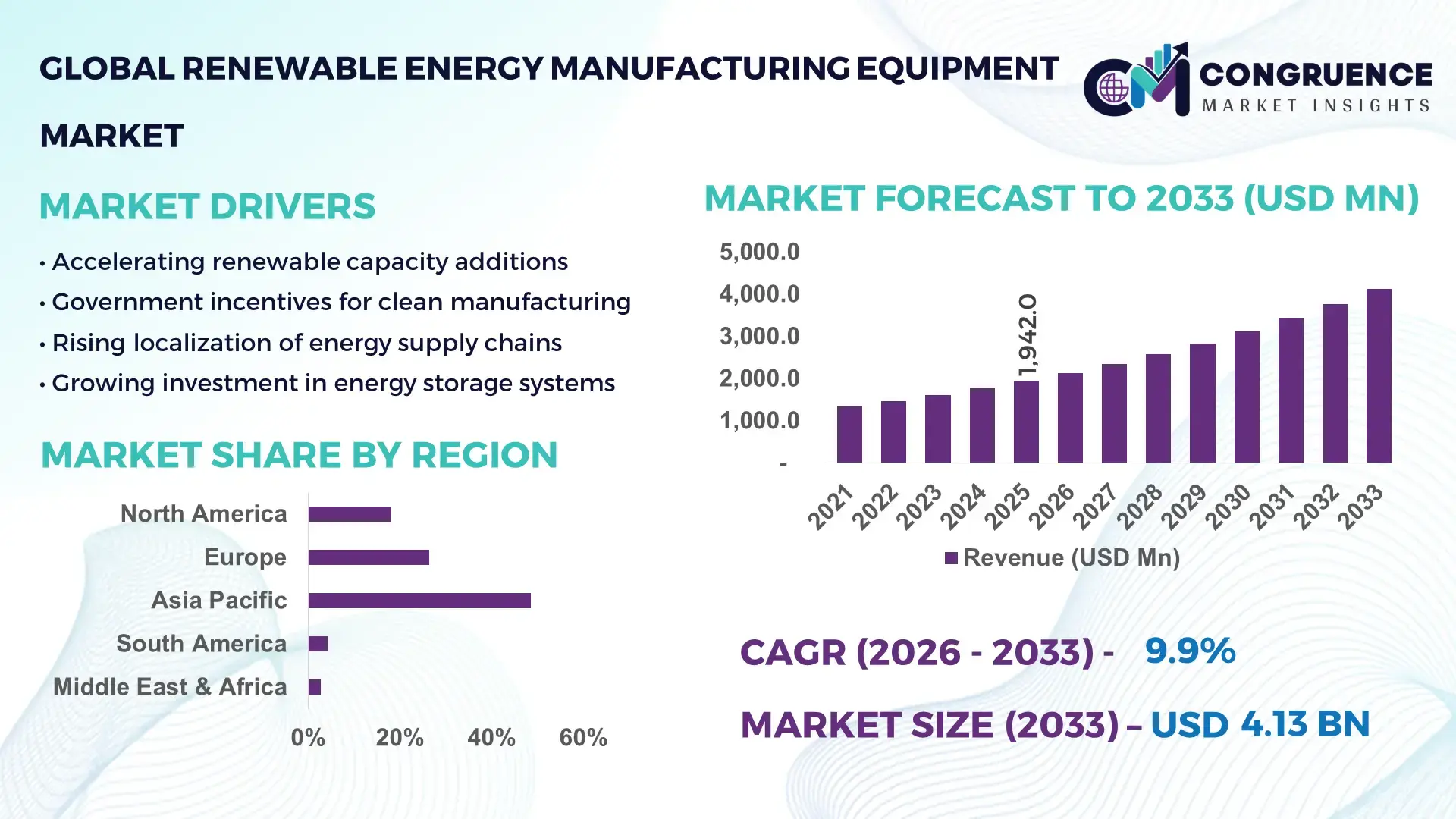

The Global Renewable Energy Manufacturing Equipment Market was valued at USD 1,942.0 Million in 2025 and is anticipated to reach a value of USD 4,132.7 Million by 2033 expanding at a CAGR of 9.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by accelerated renewable capacity additions, localization of clean-energy supply chains, and sustained capital investment in advanced manufacturing infrastructure.

China represents the most extensive production base for renewable energy manufacturing equipment globally, supported by large-scale industrial clusters across Jiangsu, Zhejiang, Guangdong, and Hebei provinces. The country’s annual solar module manufacturing capacity exceeded 500 GW in 2024, while wind turbine nacelle production surpassed 80 GW annually. Capital expenditure in renewable manufacturing equipment crossed USD 90 billion between 2022 and 2024, driven by automation upgrades, high-throughput deposition tools, and AI-enabled quality control systems. Advanced equipment adoption supports applications across utility-scale solar, offshore wind, grid-scale energy storage, and green hydrogen electrolyzer manufacturing.

Market Size & Growth: USD 1,942.0 Million in 2025, projected to reach USD 4,132.7 Million by 2033, expanding at a CAGR of 9.9% driven by accelerated renewable manufacturing localization.

Top Growth Drivers: Solar manufacturing capacity expansion (42%), wind turbine scaling (31%), energy storage equipment adoption (27%).

Short-Term Forecast: By 2028, automated production lines are expected to reduce unit manufacturing costs by 18%.

Emerging Technologies: AI-enabled production control systems, advanced power electronics manufacturing tools, and digital twin-based equipment calibration.

Regional Leaders: Asia Pacific (USD 1,850.0 Million by 2033) driven by scale manufacturing; Europe (USD 1,120.0 Million) led by precision engineering adoption; North America (USD 960.0 Million) focused on domestic capacity rebuilding.

Consumer/End-User Trends: Utility-scale renewable manufacturers account for over 55% of equipment demand, followed by independent power producers.

Pilot or Case Example: In 2024, a gigafactory automation pilot reduced production downtime by 22%.

Competitive Landscape: Market leader holds approximately 18% share, followed by 5–7 players each holding 6–10%.

Regulatory & ESG Impact: Net-zero manufacturing mandates and clean-energy tax credits accelerating equipment upgrades.

Investment & Funding Patterns: Over USD 140 billion allocated globally to renewable manufacturing infrastructure expansion.

Innovation & Future Outlook: Integration of AI-driven quality inspection and low-waste manufacturing lines shaping next-generation facilities.

The Renewable Energy Manufacturing Equipment Market supports solar PV, wind turbine, battery, and power electronics sectors, with solar equipment contributing approximately 48% of total demand. Recent advances in automation, high-efficiency cell manufacturing tools, and smart factory platforms are reshaping production economics. Regulatory decarbonization mandates, regional supply-chain security initiatives, and rising clean-energy consumption in Asia Pacific and Europe are driving equipment upgrades, while digitalized and modular manufacturing lines represent the next growth frontier.

The Renewable Energy Manufacturing Equipment Market holds strategic relevance as nations transition from energy import dependence to domestic clean-energy manufacturing resilience. Governments and enterprises increasingly view manufacturing equipment as a strategic lever to secure supply chains, reduce carbon exposure, and enhance long-term energy affordability. Advanced automation platforms now enable consistent output quality while reducing labor intensity, positioning equipment suppliers as critical partners in energy transition strategies.

Technological benchmarking highlights measurable gains. AI-enabled manufacturing execution systems deliver up to 28% throughput improvement compared to conventional PLC-based controls. Asia Pacific dominates in production volume, while Europe leads in advanced equipment adoption, with nearly 52% of renewable manufacturers deploying Industry 4.0-enabled production lines. By 2028, predictive maintenance powered by machine learning is expected to cut unplanned equipment downtime by 25%.

ESG alignment is accelerating capital deployment. Firms are committing to manufacturing sustainability metrics such as 30% energy intensity reduction and 40% material recycling rates by 2030. In 2024, Germany-based renewable equipment manufacturers achieved a 21% reduction in production scrap through AI-assisted process optimization. Looking forward, the Renewable Energy Manufacturing Equipment Market is positioned as a foundational pillar for industrial resilience, regulatory compliance, and scalable, sustainable economic growth.

The Renewable Energy Manufacturing Equipment Market Dynamics reflect rapid industrial transformation aligned with global decarbonization priorities. Equipment demand is shaped by capacity expansions in solar, wind, and energy storage manufacturing, coupled with technological shifts toward automation and digital manufacturing platforms. Policy-backed domestic manufacturing initiatives, regional trade realignments, and rising efficiency benchmarks are influencing procurement strategies. Manufacturers increasingly prioritize flexible, modular equipment capable of supporting multi-technology production lines, while cost optimization and yield improvement remain central decision factors across the Renewable Energy Manufacturing Equipment Market.

Global renewable capacity additions exceeded 500 GW annually, creating sustained demand for manufacturing-scale equipment. Solar PV alone requires high-precision wafering, cell processing, and module assembly tools, with automated lines improving yield rates by over 20%. Wind turbine scaling demands advanced casting, machining, and blade fabrication equipment capable of handling larger component sizes. Government-backed localization initiatives further amplify equipment procurement as manufacturers establish regional plants to meet policy compliance and logistics efficiency targets.

Manufacturing equipment for renewable energy systems requires substantial upfront investment, with fully automated solar cell production lines costing upwards of USD 150 million per facility. Smaller manufacturers face financing constraints, limiting adoption of advanced tools. Long equipment payback cycles, complex installation requirements, and the need for skilled operators further slow adoption, particularly in emerging economies with limited industrial infrastructure maturity.

Smart factory integration unlocks significant efficiency and cost optimization potential. Digital twins enable real-time equipment simulation, reducing commissioning times by nearly 30%. AI-driven quality inspection systems cut defect rates by up to 25%, while energy-efficient machinery lowers operational power consumption. These advancements create opportunities for equipment suppliers offering integrated hardware-software ecosystems tailored to renewable manufacturing environments.

Supply chain volatility affects access to precision components such as power electronics, sensors, and specialty alloys. Lead times for critical subcomponents have extended by 20–35% in recent years, delaying equipment delivery schedules. Additionally, evolving technical standards across regions increase customization complexity, raising engineering costs and extending deployment timelines for equipment manufacturers.

Expansion of Fully Automated Production Lines: Over 48% of new renewable manufacturing facilities now deploy end-to-end automated equipment, achieving productivity gains of 22% and defect reduction of 19%. Robotics density in solar module assembly has crossed 140 units per 10,000 workers, significantly improving consistency and throughput.

Integration of AI-Driven Quality Control: AI-based visual inspection systems are now embedded in 37% of new equipment installations, reducing rework rates by 24%. Machine learning algorithms analyze over 1.5 million data points per production cycle, enabling real-time defect detection and process correction.

Shift Toward Energy-Efficient Manufacturing Equipment: Next-generation equipment designs lower energy consumption per unit output by 18–26%. Manufacturers adopting high-efficiency furnaces and smart power management systems report annual energy savings exceeding 20%, aligning production with ESG mandates.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Renewable Energy Manufacturing Equipment Market. Research suggests that 55% of new projects achieved cost benefits through modular practices. Pre-bent and cut components fabricated off-site using automated machines reduced labor requirements by 30% and shortened project timelines by 25%, particularly across Europe and North America.

The Renewable Energy Manufacturing Equipment Market is segmented based on type, application, and end-user, reflecting the structural complexity of renewable energy supply chains. Equipment types range from solar and wind manufacturing machinery to battery and power electronics production systems, each aligned with different stages of clean energy infrastructure development. Application-wise, equipment demand is driven by solar PV module manufacturing, wind turbine assembly, energy storage system production, and balance-of-system component fabrication. End-user adoption spans utility-scale renewable developers, independent power producers, OEM manufacturers, and contract manufacturing firms. Decision-makers increasingly prioritize equipment flexibility, automation readiness, and energy efficiency, as manufacturers seek to optimize yield, reduce operational downtime, and comply with sustainability mandates across diverse renewable technology pathways.

The market by type is led by solar photovoltaic manufacturing equipment, which currently accounts for approximately 46% of overall equipment adoption. This leadership is supported by the global scale-up of wafer, cell, and module production lines, where high-throughput and precision equipment is critical to meeting rising solar deployment targets. Wind turbine manufacturing equipment follows with nearly 28% adoption, driven by demand for advanced blade molding, nacelle assembly, and large-scale machining systems.

However, energy storage manufacturing equipment represents the fastest-growing type, expanding at an estimated 12.4% CAGR, supported by rapid growth in lithium-ion and next-generation battery factories. Automation intensity in battery equipment lines has increased by over 35% in recent installations, accelerating throughput and consistency. Other equipment types, including power electronics manufacturing tools and hydrogen electrolyzer production systems, collectively account for around 26% of adoption, serving niche but strategically important applications in grid stability and emerging energy vectors.

In 2025, a large-scale battery manufacturing facility implemented next-generation electrode coating equipment, achieving a 20% reduction in material waste and improving production yield across multiple gigawatt-hours of annual capacity.

By application, solar PV manufacturing remains the dominant segment, representing nearly 44% of total equipment utilization, supported by sustained global additions of solar capacity and ongoing upgrades to high-efficiency cell technologies. Wind energy manufacturing accounts for about 27%, reflecting demand for larger turbines and offshore-capable components.

The fastest-growing application is energy storage system manufacturing, expanding at an estimated 13.1% CAGR, fueled by grid-scale storage deployment and electric mobility integration. Advanced battery equipment adoption is rising as manufacturers target faster charge cycles and higher energy density. Other applications—including power electronics, inverters, and balance-of-system components—collectively contribute roughly 29% of market activity.

In terms of adoption trends, over 41% of renewable manufacturing enterprises globally reported piloting automated quality inspection systems in 2025, while nearly 35% of large utilities prefer suppliers with digitally enabled manufacturing capabilities to ensure reliability and scalability.

In 2024, automated solar module inspection systems were deployed across multiple manufacturing plants, enabling defect detection accuracy improvements exceeding 30% and reducing field failure rates.

From an end-user perspective, utility-scale renewable manufacturers represent the leading segment, accounting for approximately 48% of total equipment demand, driven by large-capacity project pipelines and standardized production requirements. OEM manufacturers follow with around 26% adoption, leveraging advanced equipment to differentiate through performance and reliability.

The fastest-growing end-user group is contract and toll manufacturers, expanding at an estimated 11.8% CAGR, as outsourcing of renewable component production increases to optimize capital efficiency and speed-to-market. Other end-users, including research institutions and pilot-scale technology developers, collectively contribute about 26% of equipment utilization.

Adoption indicators show that over 39% of renewable OEMs integrated AI-enabled process control systems in 2025, while more than 33% of contract manufacturers reported higher equipment utilization rates through multi-technology production lines.

In 2025, a consortium of renewable OEMs deployed smart manufacturing equipment across shared facilities, achieving a 17% increase in asset utilization and faster transition between product lines.

Asia-Pacific accounted for the largest market share at 48.6% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

Asia-Pacific’s dominance is supported by large-scale manufacturing ecosystems, with over 65% of global solar module and wind component manufacturing capacity concentrated in the region. Europe held approximately 26.4% share in 2025, driven by advanced engineering standards and sustainability-led equipment upgrades, while North America accounted for around 18.1%, supported by reshoring initiatives and clean energy incentives. South America and the Middle East & Africa collectively represented about 6.9%, reflecting emerging manufacturing bases and infrastructure-driven adoption. Across regions, equipment automation rates now exceed 40% in advanced markets, while emerging regions report year-on-year installation volume growth above 20%, indicating strong long-term convergence in manufacturing sophistication.

The region accounted for approximately 18.1% of the global Renewable Energy Manufacturing Equipment Market in 2025, supported by strong domestic manufacturing policies and industrial modernization. Demand is primarily driven by solar PV equipment, battery manufacturing systems, and power electronics production tools, with energy storage-related equipment adoption exceeding 34% of regional installations. Government support includes long-term tax credits, local-content incentives, and grants supporting over 120 new clean manufacturing facilities. Digital transformation is evident, with nearly 46% of manufacturers deploying AI-enabled process control and predictive maintenance platforms. A leading local equipment supplier expanded automated inverter production lines in 2024, increasing output efficiency by 21%. Regional adoption behavior shows higher enterprise-level uptake, with more than 40% of large energy manufacturers prioritizing fully automated, data-driven production environments.

Europe held an estimated 26.4% share in 2025, anchored by Germany, the UK, and France, which together represent over 62% of regional equipment demand. Strict sustainability and industrial efficiency regulations are driving rapid upgrades to low-emission and energy-efficient manufacturing equipment. Advanced robotics penetration in renewable manufacturing plants has crossed 44%, particularly in solar cell processing and wind turbine blade fabrication. Emerging technologies such as digital twins and closed-loop material recovery systems are increasingly integrated into equipment design. A major regional equipment manufacturer introduced high-efficiency cell manufacturing tools that reduced process energy consumption by 19%. Consumer behavior across the region reflects compliance-driven procurement, with over 50% of manufacturers prioritizing traceable, explainable, and regulation-aligned production systems.

Asia-Pacific ranked first globally by volume, contributing nearly 48.6% of total market activity in 2025. China, India, and Japan are the largest consuming countries, collectively accounting for over 70% of regional equipment installations. The region leads in giga-scale factories, with more than 90 solar and battery megafactories operating or under construction. Manufacturing trends emphasize high-throughput automation, with equipment utilization rates exceeding 85% in leading plants. Innovation hubs across East Asia report over 35% adoption of AI-based quality inspection systems. A major regional player expanded fully automated module assembly lines in 2025, cutting defect rates by 24%. Regional behavior is characterized by scale-first adoption, with manufacturers favoring rapid deployment and cost-optimized equipment platforms.

South America represented approximately 4.2% of global market share in 2025, led by Brazil and Argentina. Renewable manufacturing equipment demand is closely tied to grid expansion and utility-scale solar and wind projects, with solar-related equipment accounting for nearly 52% of regional installations. Government incentives include import duty reductions and preferential financing for clean manufacturing assets. Infrastructure upgrades have driven a 28% increase in equipment installations over recent years. A regional equipment integrator supported localized wind component manufacturing, reducing logistics dependency by 18%. Consumer adoption patterns show demand linked to localized production and language-adapted digital interfaces for manufacturing systems.

The region accounted for roughly 2.7% of global demand in 2025, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Renewable manufacturing equipment adoption is driven by diversification away from fossil fuels, with solar equipment representing over 58% of regional demand. Large-scale industrial zones and cross-border trade partnerships are accelerating technology transfer. Equipment modernization initiatives report 31% improvements in production efficiency across newly commissioned plants. A regional manufacturer deployed automated solar module lines in 2024, doubling output capacity within 18 months. Consumer behavior reflects project-led adoption, with equipment purchases aligned closely to utility-scale development timelines.

China – 34.8% Market Share: High-volume production capacity and deeply integrated renewable manufacturing supply chains.

United States – 15.6% Market Share: Strong regulatory push for domestic manufacturing and rapid adoption of advanced automated equipment.

The competitive environment in the Renewable Energy Manufacturing Equipment Market is complex and moderately consolidated, with a large number of active competitors vying for technological leadership and regional expansion. There are 100+ active competitors globally, including diversified industrial machinery suppliers, specialized renewable equipment manufacturers, and automation technology firms. The combined share of the top 5 companies is around 38%, indicating that while major players hold significant influence, a long tail of smaller specialized firms contributes substantially to market diversity. Key players are investing heavily in strategic partnerships, capacity expansions, and product launches to maintain competitive relevance. For example, several equipment manufacturers have introduced AI-enabled quality inspection systems and digital twin production solutions, increasing automation adoption by more than 40% across new facilities.

Innovation trends show a rise in fully automated production lines, robotics integration, and advanced power electronics manufacturing tools, which are becoming baseline requirements for competitiveness. Strategic initiatives such as joint ventures between module line specialists and automation technology firms are expanding capability portfolios. The competitive landscape also includes regional suppliers focusing on local content and compliance with domestic manufacturing mandates, particularly in China, India, and the EU. This dynamic mix of global scale players and nimble regional specialists fuels continuous innovation and competitive pressure in the Renewable Energy Manufacturing Equipment Market, making strategic positioning, technological differentiation, and supply-chain resilience critical for sustained leadership.

Vestas Wind Systems A/S

Meyer Burger Technology AG

DN Solutions

Trumpf Group

First Solar, Inc.

JinkoSolar Holding Co., Ltd.

Hanwha Solutions (Qcells)

Goldwind Science & Technology Co., Ltd.

Nordex SE

Enercon GmbH

Mitsubishi Heavy Industries, Ltd.

Schuler Group

Manz AG

SANY Heavy Industry Co., Ltd.

The Renewable Energy Manufacturing Equipment Market is being reshaped by a wave of technological advancements that improve production efficiency, precision, and flexibility. Automation and robotics are among the most transformative technologies, with over 45% of new manufacturing lines incorporating advanced robotics for tasks such as module assembly, precision machining, and handling of large components. These systems reduce cycle times and labor requirements while improving consistency and quality. AI-driven quality inspection systems have seen rapid adoption, detecting manufacturing defects in real time and reducing rework rates by over 20% compared with traditional visual inspection methods.

Digital twin technology is emerging as a critical capability, enabling manufacturers to simulate production workflows, optimize processes before physical deployment, and conduct continuous equipment calibration without interrupting live operations. This has resulted in measurable improvements in throughput and predictive maintenance scheduling. The integration of IoT sensors and edge computing allows real-time monitoring of equipment health, enabling condition-based maintenance and minimizing unplanned downtime.

Another key technological trend is the adoption of advanced power electronics manufacturing tools, necessary for producing next-generation inverters and converters that support high-efficiency renewable energy systems. In solar PV manufacturing, heterojunction (HJT) and TOPCon equipment are shifting production toward higher efficiency cell types, while in wind manufacturing, large-scale blade molding and precision machining systems accommodate increasingly larger turbine designs.

Emerging additive manufacturing (3D printing) is also gaining traction, particularly for producing complex parts, reducing material waste, and supporting rapid prototyping. These technologies together are enabling a transition toward smart, flexible, and reconfigurable production lines, which are essential for meeting evolving demand profiles in the renewable energy sector.

• In June 2025, HVR Solar Pvt Ltd inaugurated a 2GW annual PV module manufacturing facility in Sonipat, Haryana, enhancing production of advanced N-Type Topcon bifacial modules with up to 715Wp output for utility and commercial applications. Source: www.economictimes.com

• In June 2025, Avaada Electro launched production of India’s first 720Wp TOPcon solar modules at its Butibori plant near Nagpur, with initial capacity of 1.5GW and plans to scale to 7GW of annual output by July 2025. Source: www.timesofindia.indiatimes.com

• In October 2025, Senvion India announced plans to expand blade manufacturing capacity from 1.5GW to 2GW annually with a new facility in Rajkot, targeting a 20–25% share of the Indian wind installation market and export opportunities. Source: www.timesofindia.indiatimes.com

• In December 2025, the U.S. extended solar manufacturing tariff exclusions on key equipment through November 2026, supporting continued imports of solar manufacturing machinery and reducing cost barriers for domestic facility expansions. Source: pv-magazine-usa.com

The Renewable Energy Manufacturing Equipment Market Report covers a comprehensive spectrum of segments, technologies, and regional landscapes shaping the industry’s evolution. The report’s segmentation analyzes equipment by type, including solar PV manufacturing systems, wind turbine production tools, battery and energy storage manufacturing equipment, and power electronics and balance-of-system assembly machinery. Each type is evaluated in terms of functionality, production workflows, and integration with automation and digital controls.

The application dimension explores how equipment serves diverse production pathways, from mono- and bifacial solar modules to large-scale wind blades and advanced battery cells, including niche areas such as hydrogen electrolyzer and power converter manufacturing. End-user insights delve into demand profiles across utility-scale developers, OEMs, contract manufacturers, and R&D entities, highlighting adoption trends such as digital quality control systems and flexible manufacturing lines.

Geographically, the report examines regional landscapes across Asia-Pacific, North America, Europe, South America, and Middle East & Africa, detailing infrastructure capacities, local policy environments, manufacturing ecosystems, and innovation hubs. Technology focus areas include AI-enabled inspection, robotics and automation, digital twins, IoT-based predictive maintenance, additive manufacturing, and advanced power electronics tooling. The market report also identifies emerging niches—such as manufacturing for next-generation thin-film PV and integrated battery systems—offering decision-makers a strategic view of market breadth, technological evolution, and competitive forces shaping the renewable energy manufacturing equipment landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,942.0 Million |

| Market Revenue (2033) | USD 4,132.7 Million |

| CAGR (2026–2033) | 9.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Siemens AG, ABB Ltd., GE Vernova, Vestas Wind Systems A/S, Meyer Burger Technology AG, DN Solutions, Trumpf Group, First Solar, Inc., JinkoSolar Holding Co., Ltd., Hanwha Solutions (Qcells), Goldwind Science & Technology Co., Ltd., Nordex SE, Enercon GmbH, Mitsubishi Heavy Industries, Ltd., Schuler Group, Manz AG, SANY Heavy Industry Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |