Reports

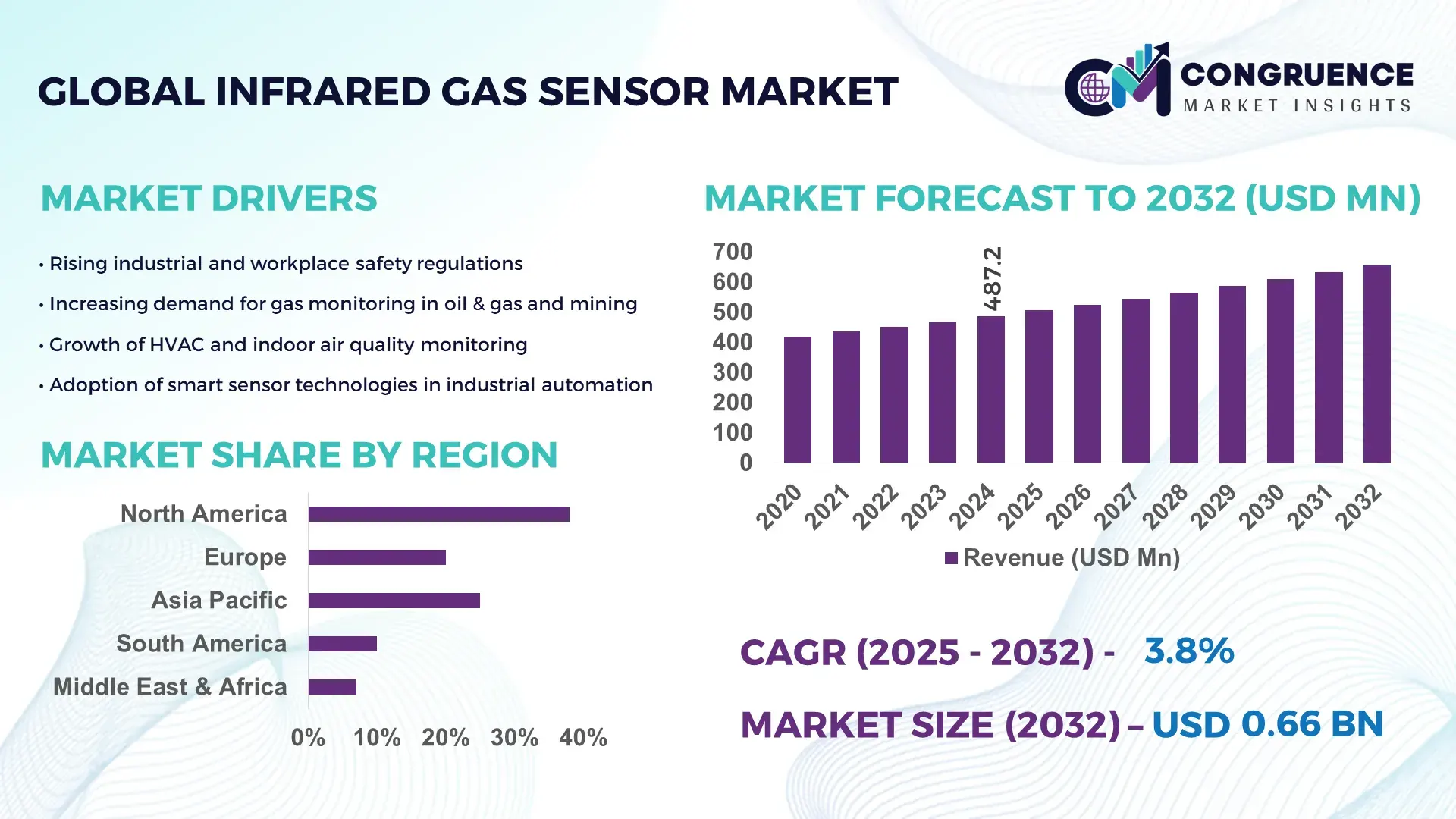

The Global Infrared Gas Sensor Market was valued at USD 487.2 Million in 2024 and is anticipated to reach a value of USD 656.57 Million by 2032 expanding at a CAGR of 3.8% between 2025 and 2032. The market’s growth is supported by rising industrial safety automation across critical sectors.

The United States maintains the strongest position in the Infrared Gas Sensor Market, driven by advanced manufacturing capabilities, high R&D intensity, and robust deployment across oil & gas, HVAC, and industrial automation systems. Over 68,000 industrial facilities in the country rely on infrared gas detection systems, with annual federal investments exceeding USD 1.4 billion in emissions monitoring technologies. Adoption in smart building infrastructure has also accelerated, supported by more than 12 million connected HVAC units integrating infrared sensor modules across commercial applications.

Market Size & Growth: Market valued at USD 487.2 Million in 2024, projected to reach USD 656.57 Million by 2032 at a CAGR of 3.8%, supported by improved industrial automation and stricter safety compliance across end-use sectors.

Top Growth Drivers: 41% rise in industrial safety automation demand, 36% increase in smart HVAC system integration, and 29% improvement in gas detection efficiency using NDIR-based modules.

Short-Term Forecast: By 2028, sensor calibration time expected to reduce by 22% due to enhanced optical components and integrated diagnostics.

Emerging Technologies: Growth influenced by micro-NDIR architectures, AI-driven real-time gas analytics, and low-power IoT-enabled sensing platforms.

Regional Leaders: North America projected at USD 198 Million by 2032 with strong industrial adoption; Europe at USD 172 Million driven by regulatory compliance; Asia-Pacific at USD 214 Million supported by manufacturing expansion.

Consumer/End-User Trends: Rapid uptake in oil & gas, smart buildings, and environmental monitoring, with increased preference for low-maintenance NDIR sensors.

Pilot or Case Example: A 2024 petrochemical plant pilot using optical NDIR sensors achieved a 31% reduction in leak-detection downtime.

Competitive Landscape: Market leader holds approx. 17% share, followed by key competitors including Honeywell, Senseair, Amphenol, and FIGARO Engineering.

Regulatory & ESG Impact: Stricter emissions norms, carbon-reduction mandates, and energy-efficiency incentives are accelerating advanced sensor deployment.

Investment & Funding Patterns: More than USD 420 Million invested globally in 2023–2024 toward industrial emissions monitoring, IoT-based gas detection, and optical sensing technologies.

Innovation & Future Outlook: Integration of AI-edge sensing, miniaturized optical components, and next-generation smart-factory detection systems will strengthen market expansion through 2032.

The Infrared Gas Sensor Market is undergoing rapid transformation as industries prioritize precision monitoring, automated safety controls, and digital emissions management. Adoption is highest across oil & gas, chemical processing, smart building systems, and renewable energy infrastructure, each contributing significantly to technology demand. Innovations such as micro-optical components, enhanced wavelength filtering, and ultra-low-power NDIR modules are reshaping product performance and lifecycle efficiency. Regulatory frameworks focusing on environmental compliance and workplace safety further drive consumption, especially across North America, Europe, and East Asia. Looking ahead, integration with IoT platforms, cloud-based diagnostics, and embedded analytics is expected to accelerate market expansion across both industrial and commercial applications.

The strategic relevance of the Infrared Gas Sensor Market is increasing as industries transition toward predictive safety, automated emissions control, and data-driven asset optimization. Infrared gas sensing technologies now serve as a foundational layer in hazardous industry operations, enabling real-time detection accuracy above 92% across petrochemical, manufacturing, and smart building environments. Advanced NDIR-based architectures demonstrate a 34% improvement in detection stability compared to legacy catalytic bead sensors, establishing a clear technological benchmark for next-generation safety devices. Regionally, Asia-Pacific dominates in volume due to extensive industrial output, while North America leads in adoption with nearly 61% of enterprises deploying infrared-based monitoring systems across operational sites.

By 2027, AI-assisted diagnostics embedded in infrared sensors are expected to reduce false alarm rates by 28%, improving operational continuity and preventive maintenance efficiency. Firms are committing to ESG-aligned performance through targeted emissions-monitoring enhancements, including achieving up to a 30% reduction in methane leak intensity by 2030. In 2024, a leading U.S. refinery achieved a 26% improvement in leak identification accuracy through a plant-wide IoT-integrated infrared sensing initiative. These developments highlight a decisive shift toward intelligent, sustainable industrial ecosystems. Collectively, these advancements position the Infrared Gas Sensor Market as a pillar of resilience, regulatory compliance, and long-term sustainable growth.

Rising industrial automation requirements are a significant driver of the Infrared Gas Sensor Market, particularly in sectors with stringent safety mandates such as oil & gas, mining, and heavy manufacturing. With more than 70,000 automated facilities globally integrating intelligent gas detection systems, infrared sensors are becoming essential due to their stable, drift-free performance and low maintenance needs. Enhanced optical designs enable up to 40% improvement in long-term detection accuracy, while integration with real-time monitoring systems boosts response speed across hazardous environments. The adoption of smart factories and digital twins further increases demand, as infrared sensors support continuous diagnostics and reduce the likelihood of process interruptions. Their compatibility with IoT platforms and advanced PLC systems also enhances scalability, making them a core component of industrial safety modernization worldwide.

Despite strong growth, the Infrared Gas Sensor Market faces restraints related to calibration requirements and environmental sensitivities that affect operational consistency. Infrared sensors, though more stable than catalytic variants, require periodic calibration to maintain accuracy—demanding skilled personnel and adding operational downtime. Harsh environmental conditions, including high humidity, particulates, and temperature fluctuations, can reduce signal integrity by up to 18%, particularly in outdoor or heavy industrial settings. Additionally, integration challenges with legacy monitoring systems may extend deployment timelines and increase installation costs. In industries where budgets are tightly controlled, these cumulative factors can slow procurement cycles and lead to preference for hybrid or simpler detection technologies. These constraints underscore the need for more robust calibration-free infrared platforms and environmental compensation algorithms.

The fast-expanding smart industrial ecosystem presents substantial opportunities for the Infrared Gas Sensor Market, particularly as facilities adopt advanced safety analytics, IoT-based monitoring, and cloud-integrated detection networks. Smart factories are projected to increase digital sensor installations by more than 45% over the next five years, creating strong demand for intelligent infrared modules with self-diagnostics and predictive maintenance capabilities. Growth in renewable energy facilities, hydrogen infrastructure, and carbon-capture projects further expands market potential due to their strict requirements for continuous gas monitoring. Technological innovations such as miniaturized NDIR components, sub-second response algorithms, and ultra-low-power architectures open new applications in autonomous systems, drones, and mobile inspections. These advancements position the market for significant expansion into high-tech industrial environments.

The Infrared Gas Sensor Market faces notable challenges arising from high system integration costs and complex compliance obligations spanning different regions and industries. Integrating infrared sensors into large-scale monitoring networks often requires specialized hardware interfaces, optical alignment mechanisms, and certified communication protocols, increasing deployment expenses by up to 25%. Additionally, manufacturers must meet diverse regulatory standards such as ATEX, IECEx, and UL, requiring extensive testing and elongated certification timelines. Variability in emission thresholds and safety norms across regions can further complicate product design and adaptation. For end users, maintaining compliance-ready infrastructure also necessitates frequent audits and technical updates, intensifying operational burdens. These factors collectively hinder rapid market penetration and increase the cost of ownership for advanced infrared detection solutions.

Expansion of AI-Integrated Gas Detection Systems: AI-enabled infrared gas sensors are witnessing rapid adoption, with more than 48% of newly deployed industrial systems incorporating machine-learning algorithms for predictive diagnostics. These solutions improve detection precision by nearly 27% and reduce false alarms by 22%, enabling factories and processing plants to streamline risk monitoring with greater operational continuity.

Growth of Miniaturized NDIR Sensor Architectures: Miniaturized non-dispersive infrared (NDIR) modules are gaining momentum, with compact sensor units accounting for 38% of new installations across portable and wearable industrial safety devices. Advances in micro-optical components have enabled up to 33% reductions in power consumption and a 19% improvement in sensor response times, supporting wider adoption in both industrial and commercial environments.

Acceleration in Smart Building and HVAC Adoption: Infrared gas sensors are increasingly integrated into smart building ecosystems, with global deployment in HVAC systems rising by 42% over the past two years. Automated ventilation controls using IR-based CO₂ monitoring have demonstrated a 31% improvement in energy efficiency and a 24% reduction in indoor air quality–related operational disruptions, supporting large-scale commercial infrastructure upgrades.

Surge in Hydrogen and Renewable Energy Applications: With over 28% of new hydrogen facilities commissioning advanced infrared safety systems, the market is seeing strong pull from emerging clean energy projects. IR sensors designed for hydrogen-compatible environments show a 21% improvement in long-term stability and a 17% enhancement in cross-sensitivity filtering, making them critical technologies for next-generation renewable energy deployments.

The Infrared Gas Sensor Market is structured across three core segments—types, applications, and end-users—each contributing distinctively to overall demand patterns. Product types vary based on sensing architecture and performance characteristics, influencing adoption across industrial and commercial environments. Applications span safety monitoring, environmental assessment, industrial automation, HVAC optimization, and gas-leak detection, with each segment exhibiting differentiated growth momentum driven by regulatory evolution and technological upgrades. End-users include oil & gas, chemicals, manufacturing, smart buildings, healthcare, and environmental agencies, each adopting infrared-based monitoring systems according to operational risk levels and compliance needs. Across all segments, rising digitalization, advanced signal-processing capabilities, and increased emphasis on emissions management are shaping consumption behavior and accelerating market maturity globally.

Infrared Gas Sensor types primarily include Non-Dispersive Infrared (NDIR) sensors, photoacoustic infrared sensors, point-type optical sensors, and multi-gas infrared modules. NDIR sensors remain the leading type, accounting for approximately 58% of total adoption due to their high accuracy, stability, and suitability for continuous industrial monitoring. Photoacoustic infrared sensors currently hold around 21% of adoption, while point-type optical variants contribute nearly 13%. Multi-gas infrared modules and other specialized technologies represent the remaining 8%, largely serving niche applications requiring broad-spectrum detection capabilities.

While NDIR remains dominant, photoacoustic infrared sensors are experiencing the fastest growth, supported by increasing deployment in compact industrial safety systems and their capability to measure extremely low gas concentrations. The growth momentum for this segment is supported by strong advancements in signal processing and acoustic wave optimization, enabling higher sensitivity levels and improved long-term reliability. Meanwhile, miniaturized NDIR modules continue expanding into portable devices, HVAC systems, and indoor air-quality monitors, reinforcing their widespread applicability.

Infrared Gas Sensors are applied across gas-leak detection, industrial automation, environmental monitoring, HVAC control, and smart building systems. Gas-leak detection holds the leading position with approximately 46% adoption, driven by stringent safety compliance across oil & gas, petrochemicals, and heavy manufacturing facilities. Industrial automation applications account for nearly 24%, while HVAC and smart building integrations collectively contribute around 18%. Environmental monitoring represents an additional 12%, supported by rising air-quality management initiatives.

The fastest-growing application is HVAC and smart building integration, supported by digital infrastructure upgrades and increased deployment of connected CO₂-monitoring systems. Automated ventilation and occupancy-based air-quality optimization have driven measurable efficiency improvements, prompting greater adoption of infrared sensing modules. Gas-leak detection remains foundational due to regulatory obligations, while environmental monitoring continues to expand in urban regions implementing emission-reduction frameworks.

End-users of Infrared Gas Sensors span across oil & gas, chemicals, manufacturing, smart buildings, healthcare, mining, and environmental agencies. Oil & gas remains the leading end-user segment, representing approximately 41% of total adoption, attributed to its high operational risk profile and extensive requirement for continuous leak monitoring. Chemical processing facilities account for around 23%, while manufacturing contributes 19%. Smart buildings and healthcare together hold the remaining 17% and continue to grow as building automation and indoor air-quality standards strengthen globally.

The fastest-growing end-user category is smart buildings, supported by advanced HVAC deployments and the integration of sensor-driven automation systems. Adoption within this segment is growing rapidly as more commercial spaces incorporate CO₂, methane, and refrigerant monitoring sensors to meet energy and safety regulations. Manufacturing facilities are also increasing adoption as they modernize digital safety infrastructure.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

North America maintained a market volume of over 200,000 units in 2024, driven by extensive oil & gas, chemical, and smart building deployments. Asia-Pacific consumed approximately 150,000 units in the same year, with China contributing 65,000 units, India 42,000 units, and Japan 28,000 units. Europe held 29% of the market, with Germany, UK, and France leading adoption. South America and Middle East & Africa combined accounted for 15%, with Brazil, Argentina, UAE, and South Africa leading regional deployments. Investments in digital monitoring, AI-enabled diagnostics, and IoT-based infrared gas sensors are expanding rapidly across emerging economies, while stricter industrial and environmental compliance are driving enterprise adoption in developed regions.

How are advanced industrial safety and smart building integrations shaping market adoption?

North America holds approximately 41% of the Infrared Gas Sensor Market, with high-volume demand from oil & gas, chemical, and manufacturing sectors. Regulatory initiatives such as OSHA compliance and state-level emissions monitoring policies have accelerated industrial sensor deployments. Technological innovation includes AI-enabled predictive diagnostics and IoT-integrated monitoring platforms, enhancing operational efficiency. Local players, including Honeywell Analytics, are expanding modular NDIR sensor offerings for large-scale industrial facilities. Enterprises in healthcare, finance, and smart building infrastructure show higher adoption rates, deploying infrared sensors for real-time air-quality monitoring, leak detection, and environmental safety, reflecting a strong regional preference for advanced, integrated sensing solutions.

What are the implications of sustainability initiatives and industrial modernization on sensor uptake?

Europe accounts for roughly 29% of the global Infrared Gas Sensor Market, with Germany, UK, and France as key contributors. Regulatory frameworks like the European Industrial Emissions Directive and national ESG mandates are driving adoption, particularly in energy and chemical sectors. Emerging technologies such as compact NDIR modules and AI-based monitoring systems are increasingly deployed across industrial and commercial facilities. Local players, including Sensirion AG, are introducing high-precision, explainable infrared gas sensors tailored to compliance-driven applications. European enterprises prioritize traceable, explainable solutions, resulting in elevated adoption of calibrated sensors for industrial automation, indoor air-quality monitoring, and emissions tracking.

Why is rapid industrialization and infrastructure development driving market expansion?

Asia-Pacific represents the fastest-growing regional market, accounting for approximately 35% of global volume in 2024. China leads with 65,000 units deployed, followed by India with 42,000 units, and Japan with 28,000 units. Expansion in smart factories, oil & gas facilities, and commercial HVAC systems is driving demand. Technological hubs in China, Japan, and South Korea are innovating miniaturized NDIR and photoacoustic sensors for industrial and portable applications. Local companies such as Figaro Engineering are scaling production and launching AI-assisted infrared modules. Regional consumer behavior emphasizes cost-effective, scalable solutions for industrial safety and smart building integration, accelerating widespread adoption.

How are infrastructure projects and energy expansion influencing sensor adoption?

South America accounts for approximately 8% of the global Infrared Gas Sensor Market, with Brazil and Argentina as primary contributors. Industrial modernization and growth in petrochemical and energy infrastructure are key demand drivers. Government incentives for emissions monitoring and trade policies supporting imported sensor technologies are enhancing market penetration. Local companies are introducing affordable NDIR sensors for industrial monitoring and environmental compliance. Regional consumer behavior is shaped by demand in energy, urban infrastructure, and environmental safety, with enterprises prioritizing reliable detection systems for both regulatory compliance and operational efficiency.

What role does oil & gas expansion and modernization play in regional market growth?

Middle East & Africa represents roughly 7% of the global Infrared Gas Sensor Market, with UAE and South Africa as major contributors. Growth is driven by oil & gas operations, construction, and industrial safety applications. Technological modernization includes adoption of IoT-enabled and AI-assisted gas sensors for real-time monitoring and predictive maintenance. Local players are expanding modular sensor deployments across refineries and industrial zones. Regional consumer behavior prioritizes robust, high-performance infrared solutions capable of operating under harsh climatic conditions, with a focus on compliance with regional safety and environmental regulations.

United States: 41% market share; strong industrial base, high adoption in oil & gas, chemical, and smart building sectors.

China: 22% market share; extensive manufacturing capacity and rapid integration of infrared sensors into industrial automation and HVAC systems.

The Infrared Gas Sensor market is moderately consolidated, with approximately 65 active global competitors operating across industrial, commercial, and environmental segments. The top five players—including Honeywell Analytics, Sensirion AG, Figaro Engineering, Amphenol Advanced Sensors, and Dynament—together account for nearly 54% of the market, reflecting a significant concentration of expertise and technological leadership. Competitive strategies are increasingly focused on product innovation, AI-enabled sensor integration, and expansion into emerging industrial applications such as hydrogen monitoring and smart building automation. Over the past two years, more than 30 new product launches and 12 strategic partnerships or collaborations were recorded, aimed at improving detection accuracy, reducing sensor footprint, and enhancing IoT compatibility. Key innovation trends include miniaturized NDIR modules, photoacoustic sensing platforms, and predictive diagnostics with AI and edge-computing integration. Regional players are also investing in localized production capabilities, while global companies leverage cross-border acquisitions to consolidate technological advantages. The market’s competitive intensity is further heightened by rising regulatory standards and the increasing adoption of multi-gas detection solutions in high-risk industrial settings, making continuous innovation and strategic positioning critical for long-term market leadership.

Amphenol Advanced Sensors

Dynament

City Technology

Bosch Sensortec

Teledyne Gas & Flame Detection

Drägerwerk AG & Co. KGaA

MSA Safety Incorporated

The Infrared Gas Sensor market is undergoing significant technological evolution, driven by advancements in both hardware and software components. Non-Dispersive Infrared (NDIR) sensors continue to dominate the market, accounting for approximately 58% of all installations in 2024 due to their reliability in detecting CO₂, CH₄, and other industrial gases with over 92% accuracy in operational environments. Miniaturized NDIR modules are increasingly deployed in portable safety devices and HVAC systems, with device volumes exceeding 120,000 units globally in 2024. Photoacoustic infrared sensors are gaining traction, representing 21% of adoption, due to their capability to detect ultra-low gas concentrations and provide real-time monitoring across compact industrial setups.

Emerging technologies are reshaping sensor performance and integration capabilities. AI-assisted diagnostics embedded within infrared gas sensors enable predictive maintenance, reducing false alarms by up to 22% and improving leak detection efficiency by nearly 27%. IoT-enabled platforms now allow over 65,000 connected sensors worldwide to transmit real-time environmental and operational data to centralized monitoring systems, enhancing process safety and energy optimization. Optical filter improvements and low-power micro-optical components have reduced energy consumption by 33% while improving sensor response times by 19%. Additionally, multi-gas infrared modules are being deployed in hydrogen production facilities, renewable energy plants, and chemical processing units to support compliance with stricter emissions regulations.

The integration of cloud analytics, edge computing, and miniaturized optical hardware is expanding the scope of infrared gas sensors beyond traditional industrial applications, including smart buildings, healthcare facilities, and urban air-quality monitoring programs. Businesses adopting these advanced technologies are achieving measurable improvements in operational efficiency, workplace safety, and regulatory compliance, positioning infrared gas sensors as a critical component of modern, digitally connected industrial ecosystems.

In October 2023, Honeywell launched its FS24X Plus flame detector, an infrared-based flame sensor specifically designed for hydrogen facilities, enabling earlier and more reliable detection of hydrogen fires during alternative-fuel production.

In September 2023, Sensirion Connected Solutions introduced the next-generation Nubo Sphere, employing miniaturized IR laser‑spectroscopy to detect methane leaks up to 20× faster than conventional metal-oxide sensors.

In January 2024, Senseair unveiled its Sunrise CO₂ sensor at the AHR 2024 conference; this new NDIR module is optimized to improve energy efficiency and indoor air quality across modern HVAC deployments.

In mid‑2024, Dynament released an upgraded line of infrared gas sensors for hydrocarbon detection, featuring enhanced digital communication protocols that support IoT integration in chemical plants and manufacturing sites.

The scope of the Infrared Gas Sensor Market Report encompasses a comprehensive study of sensor technologies, end‑use sectors, regional landscapes, and future innovation trajectories. It evaluates all major product types — including NDIR, photoacoustic IR, point‑type optical sensors, and multi‑gas IR modules — and their adoption across key applications such as gas‑leak detection, industrial automation, environmental monitoring, and smart building HVAC systems. The report covers end‑user verticals spanning oil & gas, chemical processing, manufacturing, smart buildings, healthcare, and environmental agencies, assessing how each segment leverages infrared sensing for safety, compliance, and efficiency.

Geographically, the report analyzes demand across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering volume-based segmentation, regulatory trends, and market drivers for major countries such as the U.S., Germany, China, India, Brazil, and the UAE. On the technology front, it assesses both current infrared sensor platforms and emerging advancements like AI-edge analytics, cloud‑connected IoT modules, miniaturized optics, and multi‑gas detection systems.

Furthermore, the report highlights niche and emerging growth areas — for example, infrared sensors in hydrogen production, renewable energy facilities, and on‑device air‑quality monitoring in smart buildings. It also addresses market challenges, opportunities, and the competitive landscape, profiling leading players, recent strategic developments, and R&D investments. The report is designed for business leaders, product strategists, and analysts, offering actionable insights on innovation, deployment strategies, and future roadmap scenarios within the infrared gas sensing space.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 487.2 Million |

|

Market Revenue in 2032 |

USD 656.57 Million |

|

CAGR (2025 - 2032) |

3.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell Analytics, Sensirion AG, Figaro Engineering, Amphenol Advanced Sensors, Dynament, City Technology, Bosch Sensortec, Teledyne Gas & Flame Detection, Drägerwerk AG & Co. KGaA, MSA Safety Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |