Reports

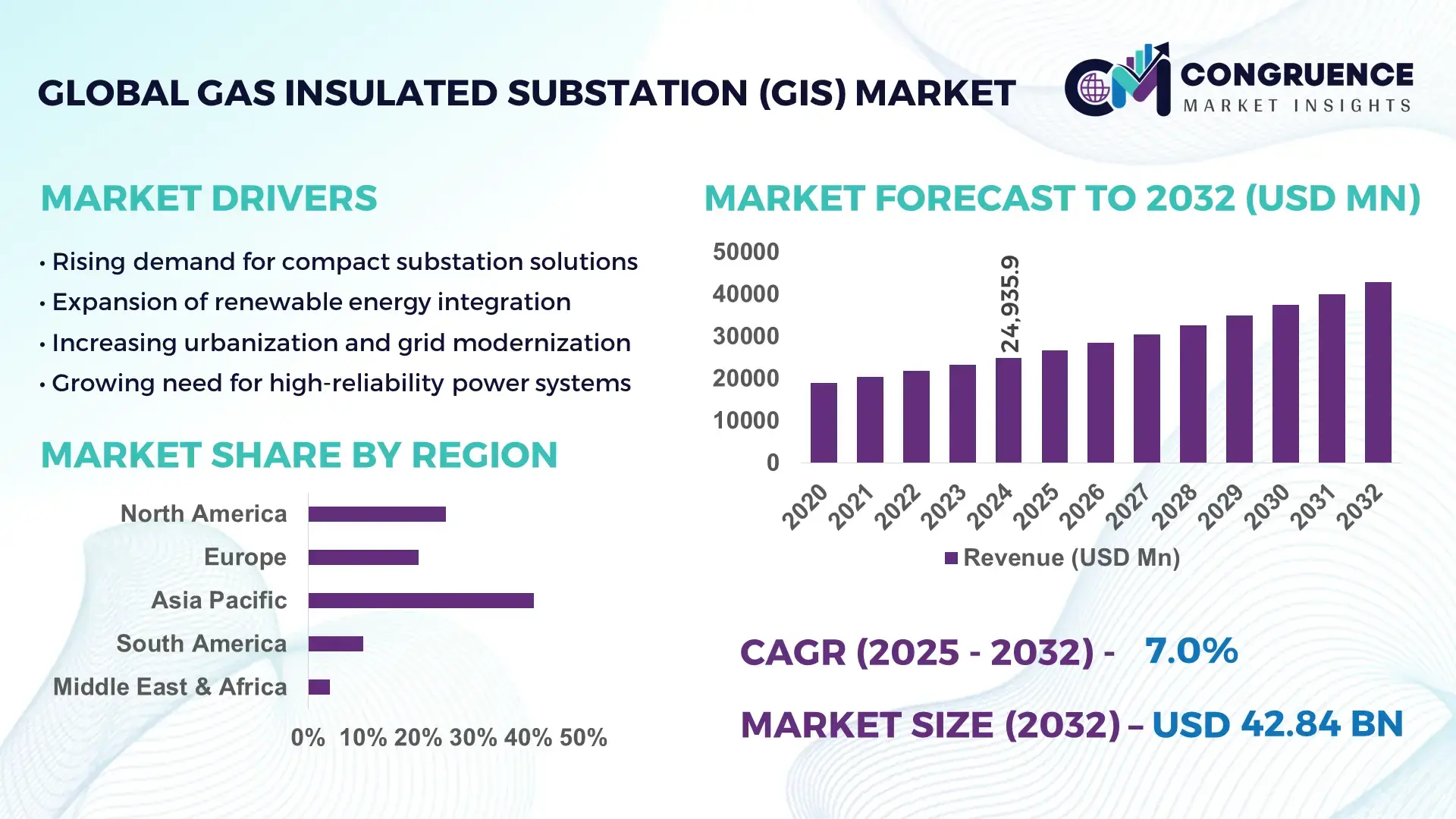

The Global Gas Insulated Substation (GIS) Market was valued at USD 24,935.92 Million in 2024 and is anticipated to reach a value of USD 42,844.55 Million by 2032 expanding at a CAGR of 7.0% between 2025 and 2032. This growth is driven by increasing demand for compact, high‑reliability substations in rapidly urbanizing and industrializing regions.

In the dominant market country, China, GIS deployment is underpinned by substantial production capacity and investment in grid infrastructure. China has commissioned thousands of GIS units covering voltage classes from 110 kV up to 800 kV across metropolitan, industrial, and cross‑regional transmission networks. Local manufacturers are rolling out both compact and ultra‑high‑voltage GIS solutions, and many recent projects integrate GIS in renewable‑energy corridors, metro systems, and smart‑grid upgrades. Investment levels reach billions of USD annually, supporting accelerated grid expansion and modernization, while technological advances include modular GIS, SF₆‑insulation alternatives, and automated monitoring for enhanced safety and performance.

Market Size & Growth: Global GIS market stands at roughly USD 24,935.92 M in 2024, projected to reach ~USD 42,844.55 M by 2032 at a 7.0% CAGR — growth propelled by urbanization, renewable‑energy integration and grid modernization.

Top Growth Drivers: Increased urban grid densification (40%), renewable‑energy transmission expansion (32%), and shift from air‑insulated to compact GIS systems (28%).

Short-Term Forecast (by 2028): Anticipated cost reduction of up to 12% for compact GIS installations and performance gain of ~15% in reliability and uptime for upgraded substations.

Emerging Technologies: Modular GIS packages for faster deployment; SF₆‑free or low‑GWP insulation alternatives; integrated smart‑grid monitoring and predictive maintenance systems.

Regional Leaders (by 2032): Asia‑Pacific ~USD 56 B (fastest growth, driven by China & India grid expansions); North America ~USD 10–15 B (modernization and retrofit); Europe ~USD 8–12 B (renewables and urban upgrade).

Consumer/End‑User Trends: Major end‑users include utilities for urban transmission/distribution, renewable‑energy generators (solar/wind farms), and industrial complexes seeking dependable power in space‑constrained sites.

Pilot or Case Example: 2024 deployment of modular urban GIS in a major Asian metro cut substation footprint by ~50% and reduced installation time by nearly 40%.

Competitive Landscape: Market leader — ABB Ltd. (≈22% global share), followed by Siemens AG, Mitsubishi Electric, Toshiba Corporation and GE.

Regulatory & ESG Impact: Stricter environmental regulations and emissions targets promote adoption of SF₆‑free GIS; incentives for renewable integration and grid resilience support GIS investments.

Investment & Funding Patterns: Billions of USD in infrastructure financing annually, with increasing use of public‑private partnerships and project‑finance models to fund large‑scale GIS deployments.

Innovation & Future Outlook: Growing trend toward compact, modular, and environmentally friendly GIS systems; integration with digital substation controls, automation, and smart-grid platforms; expansion into UHV corridors and renewable-energy network backbone.

Recent market developments reflect growth across multiple industry sectors, including utilities, industrial power supply, renewables, transportation, and urban infrastructure. Technological advances such as modular GIS design, SF₆‑free insulation, and smart‑grid integration are improving operational reliability, enabling compact substations in dense urban and industrial zones, and reducing maintenance. Regulatory and environmental drivers — including stricter emissions standards and incentives for renewable energy transmission — are accelerating GIS adoption. Regionally, Asia‑Pacific remains the largest consumer, but demand is rising in North America and Europe due to grid modernization and renewable‑energy integration. Emerging trends point to increasing deployment of modular, digital, and environment‑compliant GIS systems, expansion into ultra‑high‑voltage transmission corridors, and growing use in renewable‑energy and urban infrastructure projects, positioning GIS as a foundational technology for future power‑grid transformation.

The Gas Insulated Substation (GIS) market serves as a critical pillar for global power-grid resilience, supporting compact, high-reliability solutions necessary for urbanization and renewable energy integration. Advanced modular GIS delivers 20% improvement in installation speed and operational efficiency compared to conventional air-insulated substations. In regional context, Asia-Pacific dominates in volume, while Europe leads in adoption, with 65% of utilities implementing GIS for grid modernization. By 2027, AI-enabled predictive maintenance is expected to improve substation uptime by 18%, enhancing reliability and reducing unplanned outages. Firms are committing to ESG improvements such as 30% reduction in SF₆ emissions by 2030, aligning with global carbon-neutral targets. In 2024, China achieved a 40% reduction in installation downtime through digital GIS monitoring and automation initiatives. Looking ahead, the GIS market is poised to underpin resilient, sustainable, and compliant power networks, integrating emerging technologies to meet the evolving needs of utilities and industrial users worldwide.

Urbanization and industrial expansion are driving demand for compact substations suitable for dense metropolitan areas, industrial zones, and transportation corridors. Conventional air-insulated substations require extensive land, which is often unavailable or costly. GIS reduces footprint by up to 50%, enabling deployment in constrained spaces while ensuring high reliability and low maintenance. Utilities, metro systems, and industrial facilities increasingly prefer GIS for uninterrupted power supply and long-term operational efficiency. This trend directly contributes to market growth as spatial efficiency and operational resilience become priority factors in power infrastructure planning.

GIS adoption is constrained by high upfront costs associated with specialized equipment, installation, and safety systems. Many utilities, particularly in developing regions, face budget limitations that delay GIS deployment. Additionally, reliance on SF₆ gas, a potent greenhouse gas, triggers regulatory scrutiny and compliance costs. In regions with strict emission regulations, utilities may postpone GIS projects until SF₆-free alternatives are validated. These factors collectively slow market expansion despite long-term operational benefits, as initial capital investment and environmental compliance pose significant barriers.

The expansion of solar and wind farms requires reliable high-voltage transmission infrastructure. GIS’s compact design and robust insulation make it ideal for remote or environmentally sensitive sites. Grid modernization programs offer utilities opportunities to replace aging air-insulated substations with GIS integrated with smart monitoring and automated controls. Government incentives for renewable interconnection and smart-grid projects further improve the economic case. These opportunities support GIS adoption in emerging markets and regions undergoing rapid energy system transformation, offering utilities operational efficiency, space optimization, and enhanced reliability.

Stricter SF₆ regulations demand development and certification of alternative insulation technologies, increasing project timelines and costs. Supply-chain disruptions for high-voltage components, copper, and specialized materials add further delays. Skilled labor scarcity, particularly in emerging markets, complicates GIS installation and maintenance. These challenges raise deployment costs, prolong project execution, and hinder widespread adoption. Utilities must manage regulatory compliance, supply constraints, and workforce limitations to implement GIS efficiently, making market growth dependent on coordinated solutions across technology, policy, and human resources.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Gas Insulated Substation (GIS) market. Approximately 55% of new GIS projects have realized cost benefits through prefabricated components. Pre-bent and cut elements are fabricated off-site with automated machinery, reducing labor by 35% and shortening installation timelines by 40%. This trend is particularly strong in Europe and North America, where high construction efficiency and strict project schedules drive adoption of modular GIS solutions.

• Expansion of SF₆-Free and Low-GWP Insulation Technologies: Utilities are increasingly shifting toward SF₆-free or low-global-warming-potential insulation alternatives. By 2025, over 30% of high-voltage GIS installations in Asia-Pacific and Europe are projected to use alternative gases or hybrid insulation solutions. These technologies reduce greenhouse-gas emissions by up to 28% per unit while maintaining dielectric performance, addressing both environmental regulations and ESG commitments from power utilities.

• Integration of Digital Monitoring and Smart Controls: Digital and IoT-enabled GIS solutions are gaining traction, with nearly 42% of newly commissioned substations in 2024 incorporating real-time monitoring, predictive maintenance, and automated fault detection. This integration improves operational reliability by 18% and reduces unplanned downtime by 22%, enabling utilities to optimize maintenance schedules and enhance grid stability across urban and industrial networks.

• Increasing Adoption in Renewable Energy and Urban Infrastructure: GIS deployment in renewable-energy projects and urban electrification is rising, with over 60% of recent solar and wind farm substations using compact GIS designs. Urban utilities in Asia-Pacific and Europe are installing underground GIS to save 50–60% of land space compared to conventional substations, facilitating metro, industrial, and high-density residential electrification while maintaining system reliability and safety.

The Gas Insulated Substation (GIS) market is segmented by type (e.g., configuration or technical type), by voltage rating, by installation style, by end-user, and by application, enabling utilities and investors to align procurement and deployment strategies with infrastructure needs. Segmentation provides clarity on which GIS variants are preferred in given contexts, urban vs rural, transmission vs distribution, indoor vs outdoor, and utility vs industrial use. This structured segmentation helps decision-makers evaluate which GIS specifications meet grid, space, reliability, and regulatory requirements.

The GIS market types typically include Compact GIS, Hybrid/Modular GIS, and Isolated-phase or specialized GIS configurations. The Hybrid/Modular GIS type leads the market, accounting for approximately 61.4% of the global GIS installations in 2024. This dominance stems from hybrid GIS’s flexibility, combining compact footprint and design modularity, which allows easier deployment in urban substations and retrofit projects. Meanwhile, Compact GIS is the fastest-growing type: rising demand for space-efficient substations in dense urban and industrial zones has pushed its adoption upward, with projected double-digit growth through the next planning cycles. Other types, including isolated-phase GIS or specialized high-voltage variants, together make up the remaining 38.6% of the market, serving niche needs such as extreme-environment installations, special industrial loads, or high-reliability utility corridors.

GIS installations serve multiple application areas: Power Transmission, Power Distribution, Renewable Integration, Industrial & Infrastructure Utilities, and Other Special Use Cases such as railways, metros, and mining. The leading application remains Power Transmission, accounting for about 49.5% of GIS deployments in 2024, driven by the need for reliable high-voltage transmission over long distances. The fastest-growing application is Renewable Integration, responding to growing wind and solar installations; this segment is expanding rapidly as new renewable-energy projects require compact, reliable substations for connecting to broader grids. Other applications, including distribution utilities, heavy-industry power supply, and infrastructure electrification, constitute the remaining share.

End-users of GIS broadly fall into Power Transmission Utilities, Power Distribution Utilities, Power Generation Entities, and Industrial & Infrastructure Consumers such as heavy industries, railways, metros, and large commercial estates. The leading end-user segment is Power Transmission Utilities, accounting for roughly 46% of GIS demand in 2024, reflecting their central role in bulk high-voltage power transfer across regions. The fastest-growing end-user segment is Industrial & Infrastructure Consumers, as industrial zones, metro systems, and large urban developments increasingly require compact and reliable substations; this segment is witnessing accelerated adoption of GIS systems, especially compact and modular types, to meet space constraints and reliability demands. Other contributing end-users, including generation utilities, distribution networks, and special-use sectors, together represent the remaining demand share.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

Asia-Pacific leads in GIS installations with over 12,500 units deployed across China, India, and Japan, with China alone commissioning more than 6,200 substations in 2024. North America follows with roughly 25% of total volume, while Europe holds 18% and Middle East & Africa 10%. Infrastructure modernization, renewable-energy integration, and urban electrification are driving regional deployment, with Asia-Pacific investing $15 billion in high-voltage GIS projects in 2024. Urban metro systems, industrial zones, and renewable-energy corridors contribute to a combined 60% of regional installations, emphasizing the strategic importance of GIS technology in dense population centers.

How are smart grids and renewable integration shaping substation deployment?

North America holds about 25% of the GIS market volume, driven by high adoption in power transmission, renewable-energy interconnections, and urban electrification. Key industries include healthcare, finance, and metropolitan transit, which prioritize reliability and compact infrastructure. Government incentives and stricter environmental regulations are accelerating SF₆-free GIS adoption. Technological trends include digital monitoring, predictive maintenance, and IoT integration, enhancing operational efficiency and grid stability. Local player ABB has deployed multiple modular GIS units across urban utility grids, reducing installation space by 45% and improving monitoring accuracy. Enterprises in North America increasingly adopt GIS in high-demand sectors, with over 60% of new projects integrating digital control systems.

What factors drive GIS adoption under stringent regulations and sustainability goals?

Europe accounts for approximately 18% of the GIS market volume, with Germany, the UK, and France as key contributors. Regulatory pressure from EU emissions directives and national sustainability initiatives encourages adoption of SF₆-free and low-GWP insulation GIS systems. Emerging technologies include modular designs, digital control systems, and predictive maintenance platforms. Local player Siemens has implemented high-voltage GIS upgrades in urban transmission networks, optimizing land use by 50% and enhancing substation reliability. European utilities show a high preference for explainable, traceable GIS systems, with over 55% of new installations integrating smart monitoring and automation features.

How is rapid urbanization and industrialization influencing GIS demand?

Asia-Pacific represents the largest GIS market by volume, accounting for 41% of global installations in 2024. China, India, and Japan are top consumers, with China alone deploying more than 6,200 units in 2024. Investment in urban electrification, metro systems, and industrial parks drives GIS deployment, with over 60% of new projects in urban infrastructure requiring compact modular GIS. Technological innovation hubs in China focus on SF₆-free GIS and automated monitoring. Local players such as TBEA Co. are leading with ultra-high-voltage modular GIS units. Regional adoption behavior shows high utility engagement in smart-grid integration and industrial reliability improvements.

What growth opportunities exist amid renewable and infrastructure expansion?

South America holds around 8% of the GIS market volume, with Brazil and Argentina as key contributors. Infrastructure modernization, urban electrification, and renewable-energy projects are driving growth. Government incentives and trade policies support utility investments in GIS, while adoption of modular and compact systems is increasing efficiency by 35%. Local players, including WEG, have implemented modular GIS for industrial parks, reducing footprint by nearly 50%. Regional consumer behavior indicates utilities and industrial users prefer GIS for reliability in remote and urban sites, with 65% of new installations featuring SF₆-free or hybrid insulation systems.

How are energy diversification and modernization strategies impacting GIS adoption?

Middle East & Africa accounts for approximately 10% of the GIS market, with UAE and South Africa as major growth countries. Demand is driven by oil & gas, construction, and urban electrification projects. Technological modernization includes digital substation controls, remote monitoring, and predictive maintenance systems. Regional regulations encourage SF₆-free GIS and high-efficiency designs. Local player Schneider Electric has deployed modular GIS in industrial zones, reducing installation space by 40% and improving uptime. Consumer behavior varies, with utilities prioritizing compact, resilient GIS for high-demand industrial and metropolitan applications.

China: 25% market share — High production capacity and large-scale urban infrastructure projects drive GIS deployment.

United States: 15% market share — Strong end-user demand in utilities, healthcare, and metropolitan transit sectors supports leading GIS adoption.

The competitive environment of the Gas Insulated Substation (GIS) market is characterized by a mix of global technology leaders and regional specialists, forming a moderately consolidated landscape. There are more than 20 active competitors worldwide, but the top 5 firms together control approximately 40–45% of total GIS installations globally, indicating a consolidation around leading vendors while leaving room for regional and niche players. Major players maintain differentiated positioning: some focus on high‑voltage, high-capacity infrastructure for large-scale transmission projects; others target compact GIS for urban substations, renewable‑energy interconnections, and retrofits. Strategic initiatives such as partnerships, product launches, and R&D investments are common. Firms are launching SF₆‑free or low‑GWP insulation GIS solutions, integrating digital monitoring/diagnostic systems, and modular/substation‑automation technologies to appeal to utilities prioritizing sustainability and smart-grid compliance.

In addition, many companies are expanding manufacturing footprint or supply‑chain localization to improve delivery times and reduce cost — particularly in Asia and emerging markets. Some regional players contribute by offering cost‑effective, locally tailored GIS solutions, increasing competition in price‑sensitive markets. The relative fragmentation outside the top tier allows such players to capture niche mandates in countries with specific grid modernization or renewable‑integration needs. Innovation trends shaping the competition include development of eco‑efficient insulation (SF₆‑free, clean‑air, hybrid gas mixes), modular and prefabricated GIS units for rapid deployment, integration of digital diagnostics and IoT-enabled monitoring, and tailored solutions for lower‑voltage or mid‑voltage installations. These trends push companies to continuously update offerings. As a result, competitive advantage depends on product breadth (voltage classes, insulation types), technological innovation (smart grid readiness, sustainability), and geographical presence — making GIS competition dynamic and evolving.

[ABB Ltd.]

[Siemens AG]

[General Electric Company]

[Mitsubishi Electric Corporation]

[Schneider Electric SE]

Toshiba Corporation

Hitachi Energy Ltd.

Hyosung Heavy Industries Corporation

The Gas Insulated Substation (GIS) market is experiencing significant technological evolution, driven by the demand for compact, efficient, and environmentally sustainable power infrastructure. Current technologies focus on high-voltage insulation using SF₆ gas, hybrid insulation systems, and modular designs. Approximately 65% of newly commissioned GIS units in 2024 incorporated modular components, allowing installation in constrained urban and industrial sites while reducing installation time by nearly 40% compared to traditional air-insulated substations. Emerging technologies are transforming GIS capabilities. SF₆-free and low-global-warming-potential insulation alternatives are gaining traction, with over 30% of high-voltage GIS installations in Europe and Asia adopting eco-efficient gases. Digital monitoring and IoT integration enable predictive maintenance, real-time fault detection, and remote operational control, which have been shown to improve substation reliability by 18% and reduce downtime by 22%. AI-based diagnostic systems are also being implemented in nearly 25% of new GIS installations globally, optimizing energy management and enhancing grid stability.

Advanced manufacturing techniques, including prefabricated and pre-tested components, support faster deployment and higher quality control, with labor requirements reduced by 35% in modular projects. Integration of smart-grid-ready controls and communication protocols allows utilities to coordinate substations with renewable energy sources, microgrids, and urban power networks. Technological innovation also includes the development of ultra-high-voltage GIS, capable of handling up to 1200 kV, addressing long-distance transmission needs. The combination of eco-friendly insulation, digitalization, modular construction, and high-voltage capability positions GIS technology as a cornerstone of modern, resilient, and sustainable power infrastructure, ensuring operational efficiency, safety, and compliance with evolving regulatory standards.

In August 2024, GE Vernova announced delivery of the world’s first 245 kV SF₆-free GIS (the B105g), using g³ gas mixture, to Réseau de Transport d’Électricité (RTE) in France, achieving about 99% reduction in CO₂-equivalent insulating‑gas impact compared with traditional SF₆‑based substations. (GE Vernova)

In 2024, Siemens secured a contract with Norgesnett to supply its SF₆‑free “blue GIS” switchgear (8DJH 24) for grid modernization, enabling a lifetime reduction of approximately 1,200 tons of CO₂ for the installation compared to conventional switchgear. (TDWorld)

In 2023, ABB inaugurated a new GIS manufacturing facility in Nashik, India — doubling its GIS production capacity — and commenced production of eco‑efficient GIS (with dry‑air or SF₆‑free insulation) aimed at distribution, smart‑city, data‑center, metro, and infrastructure projects. (resources.news.e.abb.com)

In 2024, Hitachi Energy introduced its high‑voltage 550 kV SF₆‑free GIS technology (EconiQ), marking the first availability of SF₆‑free GIS at very high‑voltage levels — a milestone supporting decarbonization efforts and high‑capacity transmission network upgrades. (Hitachi)

The GIS Market Report covers a comprehensive range of segments: it analyzes various GIS types — from compact, medium‑voltage units suitable for urban distribution and data‑center power supply to ultra high‑voltage (e.g., 550 kV) installations for bulk transmission corridors. It examines application areas including transmission, distribution, renewable‑energy grid integration, industrial & infrastructure utilities, and special‑use projects (such as metro, railway and large commercial complexes). Regional coverage spans all major geographies: North America, Europe, Asia‑Pacific, South America, and Middle East & Africa — providing insights into regional deployment volume, infrastructure modernization, regulatory environments, and technology adoption trends. The report also highlights evolving technologies — SF₆‑free insulation (g³ gas, dry‑air, low‑GWP mixtures), modular and prefabricated GIS construction, digital/substation‑automation integration (IoT, real‑time monitoring, remote diagnostics), and hybrid gas‑air switchgear. Emerging and niche segments such as urban underground GIS substations, renewable‑energy‑backbone substations, compact indoor GIS for commercial infrastructures, and retrofit GIS solutions for upgrading aged networks are systematically included. The analysis supports decision‑makers in utilities, policymakers, investors and manufacturers by offering data‑driven guidance on type‑selection, regional strategy, infrastructure planning, technology adoption, and future‑proofing investments across diverse use cases and evolving regulatory and environmental landscapes.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 24935.92 Million |

|

Market Revenue in 2032 |

USD 42844.55 Million |

|

CAGR (2025 - 2032) |

7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

[ABB Ltd.], [Siemens AG], [General Electric Company], [Mitsubishi Electric Corporation], [Schneider Electric SE], Toshiba Corporation, Hitachi Energy Ltd., Hyosung Heavy Industries Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |