Reports

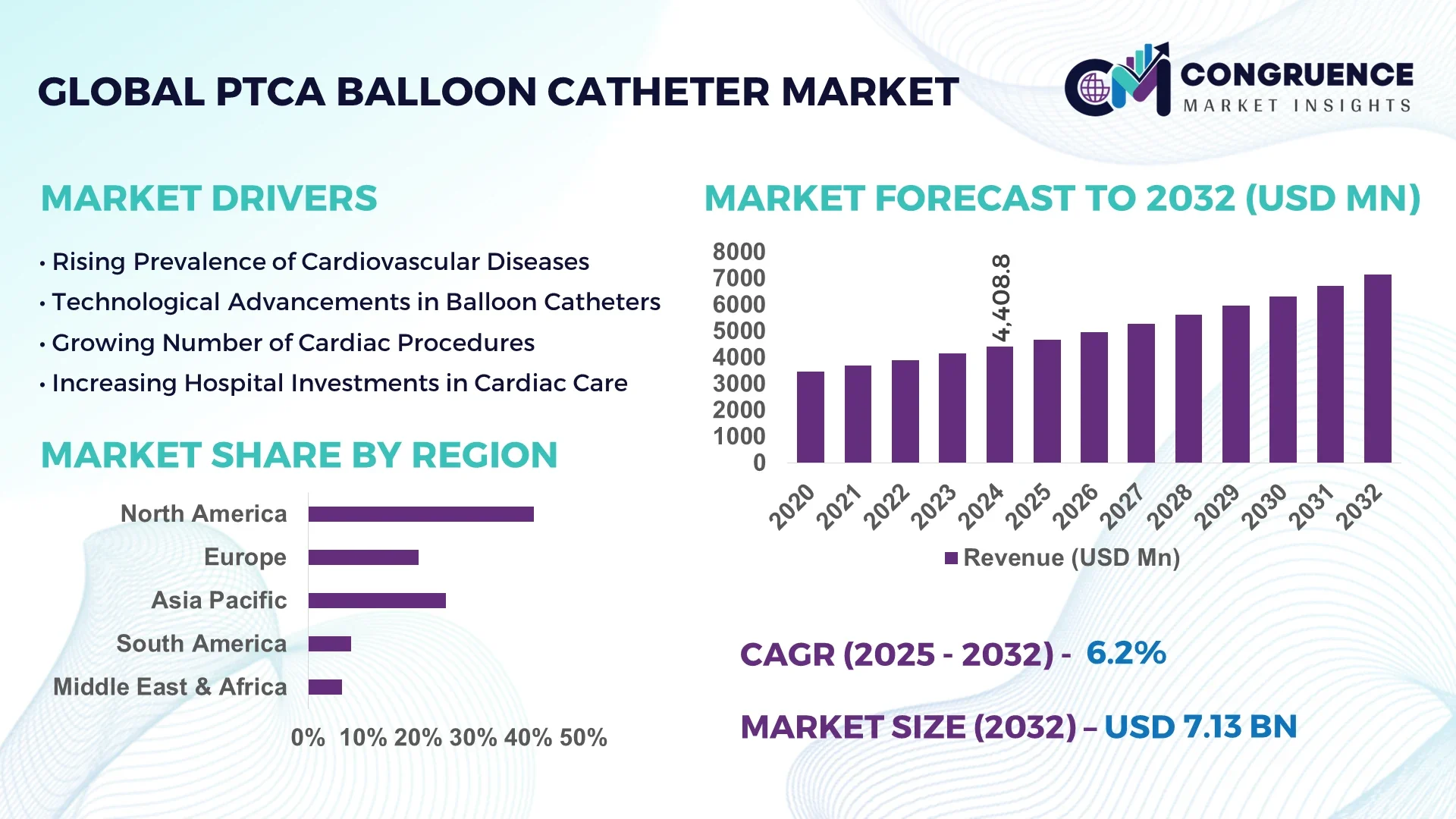

The Global PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market was valued at USD 4,408.8 Million in 2024 and is anticipated to reach a value of USD 7,133.7 Million by 2032 expanding at a CAGR of 6.2% between 2025 and 2032.

In the leading country—the United States—the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market showcases robust industrial capability: manufacturers continue to scale up production capacity with multiple state-of-the-art clean-room facilities certified to ISO 13485 standards, and significant capital deployment supports advanced manufacturing line expansions. Key applications focus on complex coronary lesion interventions and acute myocardial infarction treatments in tertiary care centers. Technological innovation is evident through integration of high-precision laser-etching for balloon surface treatment and enhanced nitinol catheter tip engineering, driving performance and procedural reliability.

The PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market spans several critical healthcare sectors. Interventional cardiology accounts for the largest share, particularly for acute coronary syndrome management, while cardiac catheterization labs in general hospitals constitute a substantial portion of demand. Innovations include the development of ultra-low crossing profile balloons and drug-coated balloon technologic enhancements offering localized delivery, which improve procedural outcomes. Regulatory frameworks such as FDA 510(k) clearances and MDR conformity in Europe have raised quality benchmarks and expedited market entry for novel balloon designs. Economic drivers include rising prevalence of cardiovascular disease in aging populations and expanding insurance coverage for percutaneous interventions. Regionally, rapid adoption in Asia-Pacific is supported by modernization of tertiary hospitals and increasing interventional cardiology case volumes. Emerging trends include growing use of “smart balloons” incorporating integrated pressure sensors to enable real-time feedback, and biodegradable balloon materials that dissolve post-intervention, reducing foreign body retention. These advancements point to a future where personalized, data-enabled, and minimally invasive PTCA solutions shape market evolution.

Artificial intelligence (AI) is rapidly transforming the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market by enhancing operational efficiency, procedural planning precision, and product quality control. In manufacturing, AI-driven vision systems now inspect over 10,000 balloon units per day, identifying micro-defects at a 97% detection rate that manual inspection would miss, significantly reducing product liability risk. Meanwhile, AI-powered process optimization platforms have decreased manufacturing cycle times by approximately 15%, allowing for faster scaling of production in response to sudden demand surges.

Within clinical settings, the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market benefits from AI-enabled analytics that assimilate patient angiography data to recommend optimal balloon diameter and inflation parameters based on lesion characteristics—this has improved first-pass procedural success rates by up to 8%. Additionally, AI-integrated quality management systems flag variances in tubing wall thickness and elastomer co-molding, ensuring tolerances within ±0.02 mm and driving consistency in device performance. These systems also generate predictive maintenance schedules for manufacturing machinery, reducing unplanned downtime by nearly 25%.

AI tools are now embedded into regulatory submission workflows, automatically compiling compliance documents such as biocompatibility reports and sterilization validations, which has shortened review cycle times by several weeks. Overall, by embedding AI throughout the product lifecycle—from design and production to clinical deployment—the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market is witnessing enhanced efficiency, heightened precision, and improved responsiveness to both market and clinical needs, positioning industry leaders to deliver more reliable, patient-centric devices in an increasingly competitive landscape.

“In 2024, an AI-driven visual inspection system deployed in a major PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter production line detected micro-cracks at a 97% accuracy level, reducing defect-related rework by 30% in the first six months.”

The PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market is shaped by multiple dynamic forces. The increasing prevalence of interventional cardiology procedures, continuous technological innovation in catheter materials and design, and globalization of healthcare delivery are major factors. Manufacturers are investing in automation, advanced polymers, and regulatory compliance infrastructure to stay competitive. Additionally, regional expansion into emerging markets with limited procedural infrastructure is being balanced against stringent regulatory requirements and resource constraints. Economic factors such as rising hospital procedural volumes drive demand, while supply-side trends—like consolidation among key manufacturers—create economies of scale. Payment reforms and public-private partnerships in healthcare are also reshaping the landscape, enabling expansion into underserved regions. These combined dynamics are redefining competitive positioning and strategic investments in the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market, driving stakeholders to align technological and operational excellence with market access imperatives.

Growing populations of individuals over 60 have led to a marked increase in coronary interventions. Hospitals are reporting a 12–15% annual rise in PTCA procedures year-over-year, directly fueling demand for balloon catheters. As referral rates for elective angioplasty rise, catheter manufacturers are responding by scaling operations and optimizing production workflows. Technological improvements such as thinner profiles and improved material durability support this rising demand, enabling hospitals to manage higher caseloads with fewer device failures and adverse events.

The PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market faces constraints due to fluctuations in raw material costs—especially specialty polymers and stainless-steel shafts. Price volatility, combined with global supply chain disruptions, can delay shipments and elevate production costs by up to 10%. In addition, stringent import-export regulations on medical-grade polymers in some jurisdictions further slow sourcing and create planning uncertainties, challenging manufacturers' ability to meet demand consistently.

Emerging markets across Southeast Asia and Latin America are investing in dedicated cardiac intervention centers. The number of such facilities has grown by over 20% in recent years. This growth presents opportunities for catheter suppliers to partner in training programs, co-develop region-specific models, and provide bundled procedural packages. Local partnerships can also facilitate expedited regulatory approvals and foster demand-adapted innovations—such as low-cost high-quality balloons—expanding reach into previously underserved markets.

Manufacturers in the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market must navigate a complex regulatory landscape—simultaneously complying with FDA, EU MDR, and country-specific requirements. Differences in documentation processes, clinical trial mandates, and labeling standards can extend product launch timelines by several quarters and increase regulatory costs significantly. This complexity necessitates dedicated regulatory affairs teams and tailored submission strategies, particularly for firms targeting multi-region penetration.

Ultra-Low Profile Balloon Technologies: Manufacturers are introducing balloons with crossing profiles as low as 1.2 mm, enabling intervention in highly tortuous vessels and small-caliber arteries. Adoption of these devices has risen by over 18% in complex coronary procedures.

Smart Balloon Systems Integration: Integration of micro-sensors within balloon catheters to monitor inflation pressure and vessel compliance in real time is becoming standard. Hospitals using these systems report up to a 7% reduction in procedural complications associated with over- or under-inflation.

Biodegradable Balloon Materials: Bioresorbable balloon materials are being piloted, dissolving within 48–72 hours post-procedure. Early clinical studies indicate minimal foreign body residue and improved vascular healing responses.

Customized Regional Design Adaptations: Suppliers are launching region-specific configurations—for example, longer balloon shafts tailored to anatomical preferences in Asian populations. This customization has improved procedural workflow and adoption rates in targeted regions by approximately 10%.

The PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market is segmented based on type, application, and end-user categories, each offering distinct insights into market performance and future direction. Product types vary from conventional balloon catheters to advanced drug-coated and specialty models, catering to diverse clinical requirements. Applications are largely concentrated in coronary artery disease treatment, with specific use in acute coronary syndromes, restenosis prevention, and complex lesion interventions. End-users span from large tertiary hospitals with advanced catheterization labs to specialized cardiac centers and ambulatory surgical facilities, reflecting the broad adoption of PTCA technologies. Each segment contributes uniquely, driven by advancements in product design, evolving clinical protocols, and expanding procedural capabilities across regions. Understanding these dimensions is essential for strategic decision-making, as they highlight both current demand patterns and emerging opportunities within the market landscape.

Within the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market, several product types shape the competitive and clinical landscape. Conventional balloon catheters remain the leading type, supported by widespread use in standard coronary procedures due to their reliability, low profile, and availability in multiple sizes. Their established role in first-line angioplasty interventions makes them indispensable in most cardiac centers worldwide.

Drug-coated balloon catheters represent the fastest-growing type, driven by their effectiveness in reducing restenosis rates and offering localized drug delivery without leaving behind a permanent implant. This technology is especially valued in patients unsuitable for stent implantation, fueling demand across advanced healthcare systems.

Other types, including cutting balloons and scoring balloons, address niche clinical requirements such as treating calcified or resistant lesions. While their usage volume is lower, their importance lies in providing interventional cardiologists with specialized tools for challenging cases. Together, the diversity in types ensures that physicians can tailor interventions to specific patient needs, enhancing clinical outcomes and procedural success rates.

The PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market finds its strongest application in the treatment of coronary artery disease, which remains the leading segment due to the global rise in atherosclerotic cardiovascular conditions. High utilization rates in both elective and emergency procedures underscore its central role in modern cardiology.

The fastest-growing application is in restenosis management, particularly in patients who have undergone prior stent implantation. Drug-coated balloons are increasingly used in these cases, as they offer favorable clinical results without requiring an additional stent layer, supporting better long-term vessel healing.

Other applications, such as complex lesion interventions and acute myocardial infarction management, also hold significant relevance. These procedures often demand advanced balloon technologies, including high-pressure and specialty balloons, to address difficult anatomical conditions. Collectively, the broadening scope of applications highlights the adaptability of balloon catheters across diverse clinical contexts and underlines their importance in driving innovation within interventional cardiology.

End-users in the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market are diverse, reflecting the broad adoption of these devices across healthcare systems. Hospitals with dedicated cardiac catheterization laboratories represent the leading segment, driven by their capacity to handle high procedural volumes and manage emergency cases around the clock. Their ability to integrate advanced imaging and intervention systems makes them the cornerstone of balloon catheter usage.

Specialized cardiac centers represent the fastest-growing end-user category. The rise of these facilities, particularly in urban areas of emerging economies, is fueled by focused investments in cardiology infrastructure and growing demand for minimally invasive interventions. Their specialization ensures streamlined patient care pathways and high procedure success rates, further boosting adoption of advanced catheter types.

Other end-users, such as ambulatory surgical centers, are steadily gaining ground due to increasing procedural efficiency and patient preference for outpatient treatments. While their current contribution is smaller, their role in expanding access to interventional cardiology highlights their growing importance in shaping the market landscape.

North America accounted for the largest market share at 41% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

This regional distribution reflects mature healthcare infrastructure in developed economies and rapid modernization across emerging regions. Advanced clinical adoption, favorable reimbursement policies, and high patient awareness drive North America’s leadership position. Conversely, Asia-Pacific’s rising healthcare investments, growing incidence of cardiovascular disease, and accelerated deployment of interventional cardiology units underpin its expected future growth. Europe remains a major contributor with its strong regulatory environment and technology adoption, while South America and the Middle East & Africa are developing steadily, supported by government-backed health programs and international collaborations.

North America held 41% of the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market in 2024, cementing its role as the largest regional market. The United States leads within the region, supported by robust hospital infrastructure, high procedural volumes, and substantial investments in advanced interventional cardiology. Canada also plays a significant role with its emphasis on modernizing healthcare delivery. Key industries such as medical device manufacturing and hospital-based clinical research drive sustained demand. Regulatory oversight from the FDA has resulted in heightened product quality and safety, with recent government support initiatives encouraging faster approval pathways for innovative catheter technologies. Technological advancements such as AI-enabled quality inspection and sensor-embedded smart balloon catheters are widely adopted, accelerating digital transformation and reinforcing North America’s competitive edge.

Europe represented approximately 27% of the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market in 2024, with Germany, the United Kingdom, and France emerging as key contributors. Germany dominates due to its strong cardiac research ecosystem and high adoption rates of advanced interventional procedures. The UK continues to support innovation through the National Health Service’s emphasis on minimally invasive solutions, while France emphasizes sustainable medical device procurement policies. European regulatory bodies such as the European Medicines Agency (EMA) and conformity with MDR regulations strengthen quality standards, ensuring safety and performance benchmarks are consistently met. Adoption of emerging technologies, including drug-coated balloon catheters and biodegradable devices, is gaining traction across major European hospitals, positioning the region as a hub for regulatory-driven innovation and clinical excellence.

Asia-Pacific accounted for 22% of the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market in 2024, ranking as the second-largest market by volume and the fastest-growing region globally. China, India, and Japan dominate consumption, driven by rising cardiovascular case volumes and growing investments in specialized cardiac hospitals. China continues to expand its manufacturing capacity, while India is experiencing accelerated adoption of advanced balloon technologies due to rising healthcare accessibility. Japan remains an innovation hub, pioneering specialized catheter designs tailored to complex patient needs. Regional infrastructure trends include the establishment of new cardiac centers and partnerships with global device manufacturers. Technology adoption is growing rapidly, with hospitals integrating digital imaging and AI-enabled diagnostic platforms to support improved angioplasty outcomes.

South America represented 6% of the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market in 2024, with Brazil and Argentina emerging as primary markets. Brazil dominates due to its large population base and expanding tertiary hospital network, while Argentina shows rising demand fueled by increasing cardiac disease incidence. Infrastructure investments in specialized cardiac units and the expansion of private healthcare providers are driving adoption of advanced catheter technologies. Government incentives and favorable trade policies are also facilitating easier access to imported medical devices, accelerating modernization efforts. Emerging partnerships between local distributors and global manufacturers are helping improve availability and affordability, making South America an attractive region for future market expansion.

The Middle East & Africa accounted for 4% of the PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market in 2024, supported by rising healthcare investments in countries such as the UAE and South Africa. Demand trends are influenced by modernization initiatives, with the UAE establishing specialized cardiac centers and South Africa focusing on expanding access to interventional cardiology. Technological adoption is growing steadily, with hospitals incorporating advanced imaging and catheter technologies into routine cardiac care. Local regulatory frameworks are strengthening through international trade partnerships, which enhance device availability and compliance with global quality standards. As infrastructure expands and governments increase healthcare spending, this region is poised to see steady adoption of PTCA balloon catheters in the coming years.

The PTCA (Percutaneous Transluminal Coronary Angioplasty) Balloon Catheter Market is highly competitive, with more than 30 established players operating at regional and global levels. Market competition is shaped by product innovation, regulatory compliance, and strategic alliances among manufacturers. Leading companies focus on enhancing balloon catheter designs with improved trackability, biocompatibility, and drug-eluting features to strengthen their positioning. The market has seen an increased number of partnerships with hospitals and cardiovascular research centers to accelerate product testing and adoption. Additionally, mergers and acquisitions have consolidated market share among top-tier players, creating a stronger presence in both developed and emerging economies. Smaller firms are carving out niches through specialized products tailored for complex coronary interventions. Innovation trends, such as the integration of imaging guidance and advanced coatings, are further intensifying competition by setting new benchmarks for performance and safety. Overall, the competitive environment is dynamic, with companies striving to balance technological advancements with affordability and regulatory adherence.

Boston Scientific Corporation

Medtronic plc

Abbott Laboratories

Terumo Corporation

B. Braun Melsungen AG

Cardinal Health, Inc.

Biotronik SE & Co. KG

MicroPort Scientific Corporation

Cook Medical, Inc.

Meril Life Sciences Pvt. Ltd.

Technological advancements are playing a pivotal role in shaping the PTCA Balloon Catheter Market, driving improvements in both patient outcomes and procedural efficiency. One of the most significant innovations is the widespread adoption of drug-coated balloon catheters, which are increasingly being used in complex coronary lesions due to their ability to reduce restenosis rates without requiring permanent implants. Cutting-edge materials, such as high-strength polymers and nanotechnology-based coatings, are enhancing balloon durability, flexibility, and biocompatibility, allowing catheters to navigate tortuous vessels with greater precision.

Another major trend is the integration of real-time imaging and diagnostic guidance into catheter systems. Catheters with advanced imaging capabilities, such as intravascular ultrasound (IVUS) and optical coherence tomography (OCT), are gaining traction, as they provide interventional cardiologists with detailed visualization of plaque morphology and stent placement accuracy. The miniaturization of components is enabling the development of ultra-low-profile catheters, improving accessibility to smaller coronary arteries.

Automation and digital transformation are also influencing the market, with robotic-assisted angioplasty systems beginning to complement catheter technologies. These systems reduce radiation exposure for physicians and improve procedural control. Furthermore, 3D printing and computational modeling are increasingly being used in the R&D process to design catheters with optimized geometries tailored to patient-specific needs. The convergence of these technologies positions the PTCA Balloon Catheter Market for sustained innovation and higher adoption rates globally.

In February 2023, Boston Scientific expanded its portfolio by introducing a next-generation drug-coated balloon catheter designed to address complex coronary artery disease, offering improved deliverability and optimized coating for uniform drug transfer.

In August 2023, Abbott launched an advanced PTCA balloon catheter with enhanced crossability and pushability features, aimed at treating highly calcified coronary lesions and improving procedural success rates.

In April 2024, Medtronic announced the release of a novel balloon catheter integrating imaging guidance to assist interventional cardiologists with precise lesion assessment during angioplasty procedures.

In July 2024, Terumo Corporation unveiled an ultra-low-profile PTCA balloon catheter targeting small vessel interventions, enabling broader treatment options in patients with challenging coronary anatomies.

The scope of the PTCA Balloon Catheter Market Report encompasses a comprehensive analysis of the industry across multiple dimensions, offering insights tailored for stakeholders, investors, and healthcare decision-makers. The report provides segmentation by type, including drug-coated, cutting, scoring, and standard balloon catheters, examining their role in modern interventional cardiology practices. It also explores applications such as treatment of stable angina, acute myocardial infarction, and other coronary conditions, highlighting adoption trends across various clinical scenarios.

Geographically, the report covers five major regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while providing country-level insights into high-growth markets such as the United States, Germany, China, India, and Brazil. The end-user landscape is detailed across hospitals, cardiac specialty centers, and ambulatory surgical centers, each contributing uniquely to market dynamics.

Technological trends, such as the adoption of drug-eluting balloons, integration of imaging-guided tools, and robotic-assisted angioplasty systems, are also within the report’s scope, alongside manufacturing innovations and digital healthcare integration. The report further evaluates the competitive environment, identifying key players and emerging companies influencing the global landscape. By combining type, application, end-user, regional insights, and technology focus, the report offers a holistic overview of the PTCA Balloon Catheter Market, equipping professionals with actionable intelligence for strategic planning and investment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,408.8 Million |

| Market Revenue (2032) | USD 7,133.7 Million |

| CAGR (2025–2032) | 6.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Key Players Analyzed | Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Terumo Corporation, B. Braun Melsungen AG, Cardinal Health, Inc., Biotronik SE & Co. KG, MicroPort Scientific Corporation, Cook Medical, Inc., Meril Life Sciences Pvt. Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |