Reports

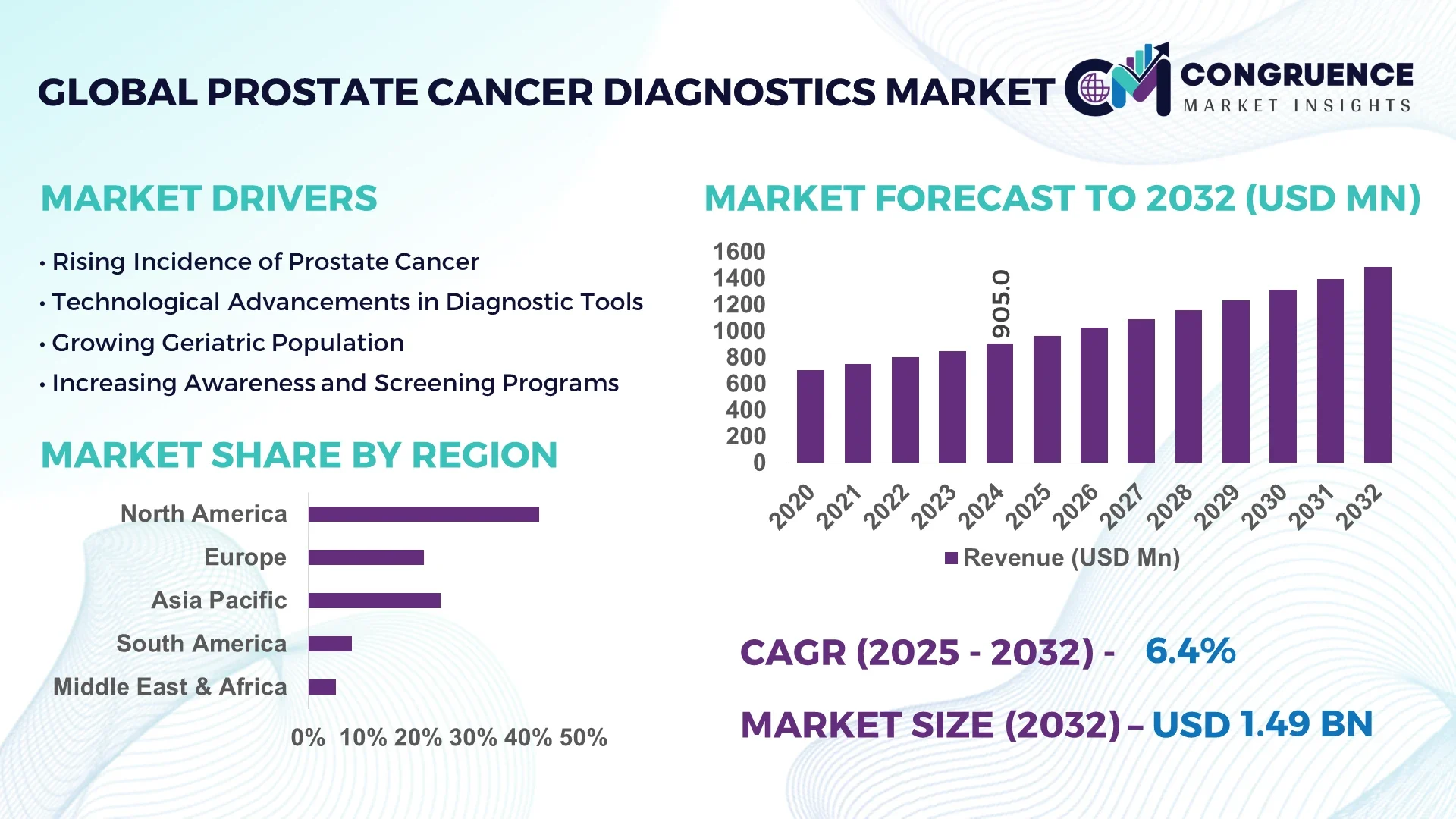

The Global Prostate Cancer Diagnostics Market was valued at USD 905.0 Million in 2024 and is anticipated to reach a value of USD 1,486.6 Million by 2032 expanding at a CAGR of 6.4% between 2025 and 2032.

The United States dominates the prostate cancer diagnostics market, driven by its extensive healthcare infrastructure, high incidence rate of prostate cancer, and widespread adoption of advanced diagnostic technologies. The growing focus on early detection and increasing awareness campaigns have led to higher screening rates, supporting market expansion in the region.

Prostate cancer diagnostics encompass a range of technologies including biomarker testing, imaging techniques, and biopsy methods. Continuous innovation in diagnostic tools is improving early detection accuracy and patient outcomes. Rising investments in research and development are fueling the introduction of non-invasive diagnostic tests, personalized diagnostics, and integration of molecular profiling. The market is also witnessing enhanced collaborations between diagnostic firms and healthcare providers, further driving product accessibility and adoption worldwide.

Artificial Intelligence (AI) is revolutionizing the prostate cancer diagnostics market by enhancing the precision, speed, and efficiency of diagnostic processes. AI-powered algorithms are now capable of analyzing large datasets from imaging and pathology slides, facilitating early detection and reducing human error. For instance, AI-assisted MRI interpretation enables radiologists to identify suspicious lesions with higher accuracy compared to conventional methods, streamlining the diagnosis process. Additionally, AI-driven pattern recognition in histopathology helps pathologists distinguish between benign and malignant prostate tissues more reliably.

Machine learning models are also improving the predictive power of biomarker tests by correlating genetic and clinical data to better stratify patients based on risk profiles. This personalized approach supports tailored treatment planning and monitoring, reducing overtreatment and enhancing patient quality of life. AI is increasingly being integrated into digital pathology platforms, enabling remote diagnostics and collaboration among specialists globally.

Furthermore, AI applications in natural language processing facilitate the extraction of relevant clinical information from electronic health records, improving patient stratification and clinical trial recruitment. The use of AI in prostate cancer diagnostics not only accelerates workflows but also supports continuous learning by refining models based on new data inputs.

“In 2024, a notable development occurred when an AI-based diagnostic system received regulatory approval for its enhanced ability to interpret multiparametric MRI scans of the prostate, demonstrating diagnostic accuracy improvements of up to 15% over traditional radiologist assessments.”

The increasing incidence of prostate cancer worldwide is a critical driver for market growth. Governments and healthcare organizations are promoting screening programs, particularly for high-risk groups, which boost demand for advanced diagnostic tests. Enhanced screening efforts improve early detection rates, thereby increasing patient eligibility for less invasive treatment options and better prognosis. This driver is supported by rising awareness campaigns and funding for prostate health, which collectively stimulate the market.

Despite technological advancements, the high cost associated with state-of-the-art prostate cancer diagnostic tools restricts widespread adoption, especially in developing regions. Expensive imaging equipment, biomarker testing kits, and biopsy procedures can limit accessibility for patients lacking adequate insurance coverage or financial resources. Additionally, healthcare providers may face budget constraints in upgrading diagnostic infrastructure, slowing market growth in cost-sensitive markets.

The increasing focus on personalized medicine presents substantial opportunities in the prostate cancer diagnostics market. Diagnostic tools that offer risk stratification and treatment monitoring enable tailored therapeutic interventions, improving patient outcomes. Innovations in genomics and biomarker discovery are driving the development of next-generation diagnostics that predict individual disease behavior. This trend is expected to open new avenues for market players in both developed and emerging markets.

Navigating complex regulatory frameworks poses a significant challenge for market participants, particularly for AI-based diagnostic tools requiring validation and approval. Additionally, integrating patient data for AI analytics raises concerns regarding data privacy and security. Ensuring compliance with stringent regulations while fostering innovation demands significant investment and expertise. These challenges could delay product launches and limit market penetration.

Rise of Multiparametric MRI (mpMRI) Usage: The adoption of mpMRI as a standard non-invasive imaging tool is improving prostate cancer detection accuracy. MpMRI reduces unnecessary biopsies by providing detailed visualization of suspicious areas, leading to better patient outcomes and reduced healthcare costs.

Growth of Liquid Biopsy Techniques: Liquid biopsy is gaining traction due to its minimally invasive nature and ability to provide real-time monitoring of tumor dynamics. This method helps in early detection, treatment response evaluation, and relapse monitoring, making it a preferred alternative to traditional tissue biopsies.

Advancements in Biomarker Discovery: Novel biomarkers, including PSA derivatives and genetic markers, are enhancing the precision of prostate cancer risk assessment and diagnosis. These biomarkers help differentiate aggressive cancer from benign conditions, supporting more personalized treatment strategies.

Integration of Artificial Intelligence and Machine Learning: AI-powered diagnostic tools are streamlining image analysis and pathology workflows. Machine learning algorithms improve accuracy in detecting clinically significant prostate cancer and predicting disease progression, enabling more tailored patient management.

Expansion of Telehealth and Remote Diagnostics: Telemedicine platforms are increasingly incorporating diagnostic services, providing remote consultation and second opinions. This expansion improves access to prostate cancer diagnostics, especially in underserved or rural regions, and supports timely clinical decision-making.

Collaborative Diagnostic Solutions: There is a growing trend of partnerships between diagnostic companies and healthcare providers to develop integrated solutions combining imaging, biomarker testing, and AI analytics. These holistic approaches aim to enhance diagnostic accuracy and optimize patient outcomes.

The prostate cancer diagnostics market is segmented based on type, application, and end-user to provide a comprehensive understanding of market dynamics. By type, the market includes biomarker testing, imaging, and biopsy, each serving distinct diagnostic purposes. Applications range from screening and early detection to monitoring and treatment guidance. End-users primarily consist of hospitals, diagnostic laboratories, and research institutes, reflecting the varied settings where prostate cancer diagnostics are utilized. Understanding these segments helps identify key growth areas and tailor innovations to meet specific clinical needs effectively.

The prostate cancer diagnostics market by type includes biomarker testing, imaging, and biopsy techniques. Among these, biomarker testing currently leads the market due to its non-invasive nature and ability to provide early indications of cancer presence through blood and urine tests. Biomarkers such as PSA, PCA3, and emerging genetic markers are increasingly relied upon for initial screening and risk assessment.

Imaging techniques, including multiparametric MRI and ultrasound, are the fastest growing segment. The growing adoption of advanced imaging technologies is driven by their ability to provide detailed anatomical and functional information, aiding in precise tumor localization and staging. Multiparametric MRI, in particular, has gained prominence for guiding biopsies and treatment decisions.

Biopsy methods, while traditional and essential for confirming diagnosis, are witnessing slower growth due to the shift towards less invasive options. However, advancements such as MRI-guided biopsies are enhancing accuracy and reducing patient discomfort, maintaining biopsy’s relevance in the market.

The applications in the prostate cancer diagnostics market include screening, early detection, treatment monitoring, and prognosis. Screening and early detection dominate the market due to the emphasis on identifying prostate cancer in asymptomatic stages to improve treatment outcomes. Public health initiatives and growing awareness campaigns have increased routine prostate cancer screening rates globally.

Treatment monitoring is the fastest growing application segment. Continuous advancements in diagnostic technologies are enabling real-time monitoring of disease progression and therapeutic response, facilitating personalized treatment adjustments. Technologies such as liquid biopsies and imaging are pivotal in this space, allowing less invasive, repeated assessments.

Prognosis, while crucial for long-term patient management, holds a smaller market share but is expected to gain traction as molecular diagnostics and AI-based predictive models enhance prognostic accuracy and individualized care plans.

End-users of prostate cancer diagnostics include hospitals, diagnostic laboratories, and research institutes. Hospitals represent the largest segment due to their comprehensive service offerings, including patient screening, diagnosis, and treatment planning. The presence of multidisciplinary teams and advanced diagnostic equipment makes hospitals a primary point of care for prostate cancer patients.

Diagnostic laboratories are the fastest growing end-user segment. The rising demand for specialized and high-throughput testing, including biomarker analysis and genetic profiling, has fueled the growth of independent and reference laboratories. These labs offer quick turnaround times and cost-effective testing solutions, supporting decentralized diagnostic services.

Research institutes contribute to market growth through continuous development and validation of new diagnostic technologies. Their role is critical in translating scientific discoveries into clinically applicable diagnostic tools, thereby supporting innovation and market expansion.

North America accounted for the largest market share at 42% in 2024; however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

The dominance of North America is attributed to its well-established healthcare infrastructure, high prostate cancer prevalence, and widespread adoption of advanced diagnostic technologies. Asia-Pacific's rapid growth is driven by increasing healthcare investments, growing awareness, and expanding screening programs in countries such as China and India. Europe follows closely with strong market presence supported by technological advancements and government initiatives for early cancer detection.

Technological Leadership and Adoption in the US and Canada

The North American market is characterized by extensive use of advanced diagnostic modalities like multiparametric MRI and biomarker-based liquid biopsies. The United States leads in the integration of AI-powered diagnostic tools, with over 60% of diagnostic centers employing such technologies. Canada has seen increased government funding to enhance prostate cancer screening coverage. The prevalence of prostate cancer remains high, with an estimated 1 in 8 men diagnosed during their lifetime, fueling demand for improved diagnostics. Collaborations between biotech firms and healthcare providers are accelerating innovative product launches.

Growing Focus on Precision Medicine and Public Screening Programs

Europe’s prostate cancer diagnostics market benefits from robust public health policies promoting early detection. Countries like Germany, France, and the UK have implemented national screening programs leading to increased testing volumes. Biomarker testing accounts for nearly 45% of diagnostics performed, supported by widespread insurance coverage. The rise of digital pathology and telemedicine has improved diagnostic access in rural areas. The European population’s aging demographic further underscores the need for effective diagnostics, with incidence rates climbing steadily over the past decade.

Rapid Market Expansion Fueled by Healthcare Infrastructure Development

Asia-Pacific is witnessing significant growth with China and India emerging as key markets. Increasing government healthcare expenditure and private sector investments have expanded diagnostic facilities by 30% over recent years. There is growing adoption of non-invasive diagnostic techniques due to patient preference and awareness campaigns. Urban centers are rapidly implementing advanced imaging and biomarker diagnostics, while rural areas are catching up through mobile health initiatives. The rising incidence of prostate cancer, estimated to affect over 1 million men in the region annually, is driving demand for cost-effective and accessible diagnostics.

Improved Healthcare Accessibility Driving Diagnostic Uptake

South America’s prostate cancer diagnostics market is evolving, with Brazil and Argentina leading regional adoption. Enhanced healthcare access and increased awareness have resulted in a 25% rise in screening rates over the past five years. Investments in modern diagnostic equipment, including ultrasound and PSA testing kits, have expanded capacity. Despite economic constraints, public-private partnerships are supporting broader diagnostic reach. Urban hospitals are the primary end-users, with increasing interest in integrating AI for image analysis.

Emerging Market Potential with Focus on Early Diagnosis

The Middle East and Africa region is gradually strengthening its prostate cancer diagnostics capabilities. Saudi Arabia and South Africa are the front-runners, with growing investments in healthcare infrastructure. Screening programs are in early stages but expanding rapidly, with awareness campaigns improving patient engagement. The region faces challenges such as limited specialized diagnostic centers and workforce shortages, but mobile diagnostics and telehealth are helping bridge gaps. The adoption of biomarker testing is increasing steadily, supported by government initiatives focused on non-communicable diseases.

United States: Holds the highest market share at approximately USD 380 million in 2024, driven by advanced diagnostic technologies, extensive screening programs, and a high prevalence of prostate cancer.

China: The second largest market valued around USD 120 million in 2024, supported by rapid healthcare infrastructure expansion, growing awareness, and increased adoption of innovative prostate cancer diagnostics.

The global prostate cancer diagnostics market is highly competitive, with numerous key players investing heavily in research and development to introduce innovative diagnostic solutions. Market leaders focus on enhancing the accuracy, speed, and patient comfort of diagnostic procedures. Companies are expanding their portfolios by incorporating advanced biomarker testing, imaging technologies, and AI-driven analytics. Strategic collaborations, mergers, and acquisitions are common as firms seek to strengthen their market presence and access emerging markets. Additionally, emphasis on regulatory approvals and clinical validations is shaping product launches and adoption rates. The market is also witnessing increased competition from startups specializing in AI and molecular diagnostics, challenging traditional players to innovate continuously. Leading companies allocate significant resources to clinical trials, ensuring their products meet stringent quality and efficacy standards, which influences purchasing decisions by healthcare providers.

Abbott Laboratories

F. Hoffmann-La Roche Ltd.

Becton, Dickinson and Company (BD)

Siemens Healthineers

Hologic, Inc.

Bio-Techne Corporation

PerkinElmer, Inc.

Myriad Genetics, Inc.

QIAGEN N.V.

Invitae Corporation

Technological advancements are driving the prostate cancer diagnostics market forward, focusing on non-invasive and highly accurate diagnostic methods. Biomarker testing, particularly using PSA and emerging genetic markers like PCA3 and SelectMDx, allows early detection through simple blood or urine tests. Imaging technologies such as multiparametric MRI (mpMRI) and advanced ultrasound techniques provide detailed visualization of prostate abnormalities, significantly improving biopsy targeting and tumor localization.

Artificial intelligence and machine learning are increasingly integrated into diagnostic platforms, enabling automated image analysis and predictive modeling. AI algorithms help radiologists detect suspicious lesions with higher precision and reduce inter-observer variability. Digital pathology, combined with AI, is revolutionizing tissue analysis by enabling remote diagnostics and improving workflow efficiency.

Additionally, liquid biopsy technology is gaining prominence, offering a minimally invasive way to detect circulating tumor cells and DNA, aiding in monitoring disease progression and treatment response. Innovations in molecular diagnostics are also enabling personalized risk assessments and tailored treatment strategies. Together, these technologies are transforming prostate cancer diagnostics toward earlier, more precise, and patient-friendly approaches.

In February 2024, Myriad Genetics launched a next-generation sequencing panel that enhances detection of prostate cancer-related genetic mutations, providing more comprehensive risk profiling for patients.

In October 2023, Siemens Healthineers introduced an AI-powered prostate MRI analysis tool that reduces reading time by up to 30% while improving lesion detection accuracy.

In August 2023, QIAGEN expanded its portfolio by releasing a new liquid biopsy assay designed to detect circulating tumor DNA specific to prostate cancer, enabling less invasive monitoring.

In January 2024, Hologic, Inc. received regulatory approval for its advanced biomarker test that combines urine-based genetic markers with clinical parameters to improve early detection sensitivity.

The prostate cancer diagnostics market report provides an in-depth analysis of market trends, technological advancements, competitive landscape, and growth drivers across key regions. It covers segmentation by type, application, and end-user, offering insights into leading and emerging segments. The report evaluates the impact of AI and molecular diagnostics on market evolution and highlights ongoing innovations in imaging and biomarker testing. Regional market dynamics are detailed, showcasing growth opportunities in established and emerging economies.

Furthermore, the report addresses challenges such as regulatory hurdles, cost factors, and variability in diagnostic accuracy, helping stakeholders navigate market complexities. Key player profiles, recent developments, and strategic initiatives are also included to present a comprehensive industry overview. Overall, the scope enables healthcare providers, investors, and manufacturers to make informed decisions based on current and forecasted market conditions.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Prostate Cancer Diagnostics Market |

| Market Revenue (2024) | USD 905.0 Million |

| Market Revenue (2032) | USD 1,486.6 Million |

| CAGR (2025–2032) | 6.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Abbott Laboratories, F. Hoffmann-La Roche Ltd., Becton, Dickinson and Company (BD), Siemens Healthineers, Hologic, Inc., Bio-Techne Corporation, PerkinElmer, Inc., Myriad Genetics, Inc., QIAGEN N.V., Invitae Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |