Reports

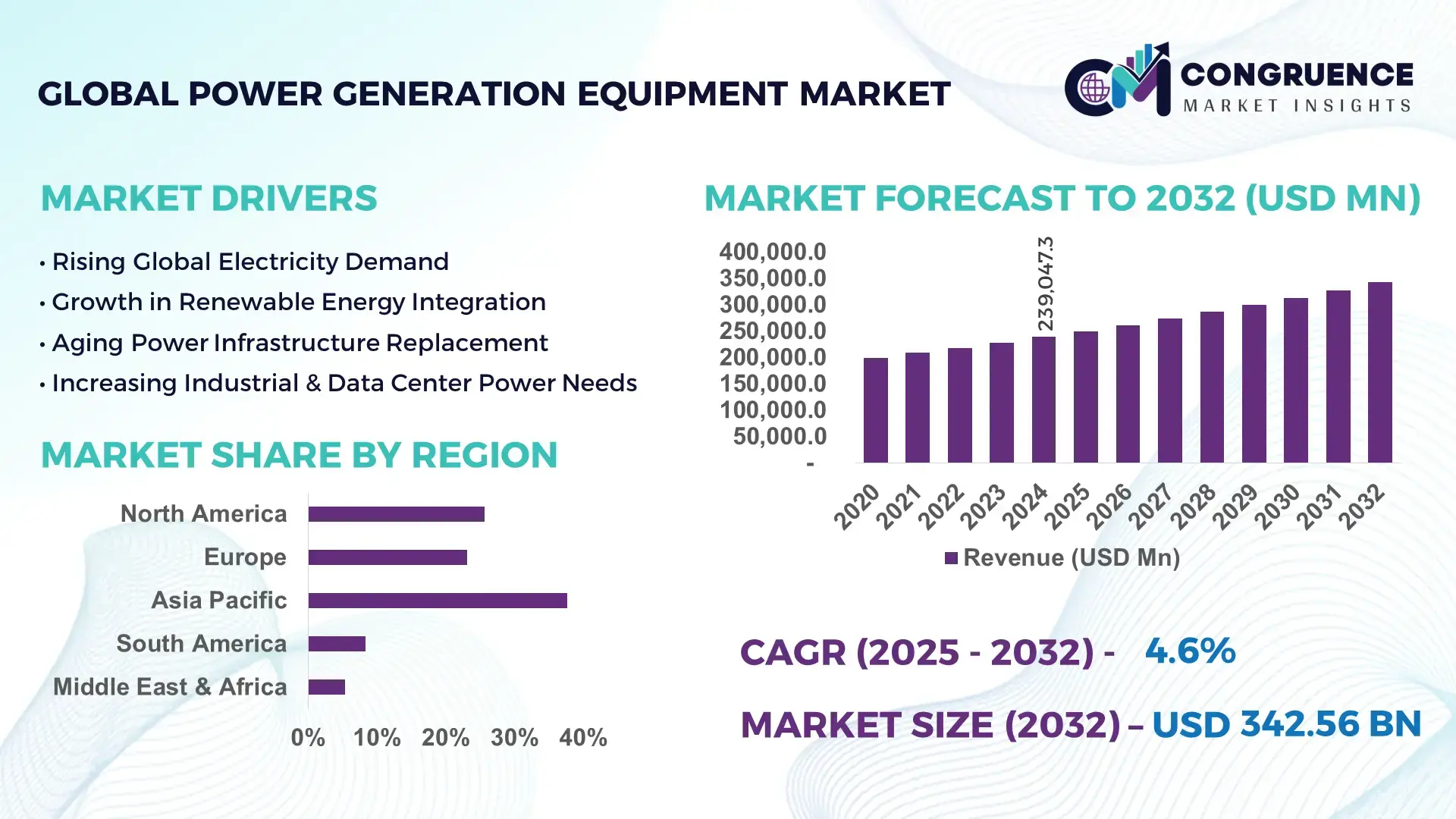

The Global Power Generation Equipment Market was valued at USD 239,047.3 Million in 2024 and is anticipated to reach a value of USD 342,560.5 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032.

In 2025, China continues to play a central role in the Power Generation Equipment Market, boasting the world’s largest installed power generation infrastructure. The country has significantly ramped up investments in high-capacity thermal and renewable power plants. Its domestic manufacturers have expanded production capacities to meet both local and export demand, while major advancements in turbine and generator efficiency—driven by government-supported R&D—have further solidified China’s position as a leader in technology deployment.

The Power Generation Equipment Market is closely interlinked with industries such as utilities, oil & gas, manufacturing, and infrastructure, which account for the bulk of end-user demand globally. Utilities remain the largest contributors, driven by upgrades to aging grids and rising energy consumption. Technological innovations—such as next-generation gas turbines, digital twin-enabled systems, and hybrid energy storage integrations—are significantly improving system efficiency and lifecycle performance. Regulatory pressures related to carbon emissions and energy transition policies in Europe and North America are compelling utilities to modernize and decarbonize generation fleets. Economically, government stimulus packages across regions have supported new infrastructure development, particularly renewable power installations, influencing regional consumption patterns. Asia-Pacific is seeing increased adoption of solar and wind-powered generation equipment, while North America and Europe are investing in hydrogen-based systems and microgrids. Future outlook points toward increased automation, grid-interactive solutions, and further convergence of traditional and renewable technologies, reshaping how and where power generation equipment is deployed worldwide.

Artificial Intelligence (AI) is profoundly reshaping the Power Generation Equipment Market by enhancing operational performance, optimizing asset management, and streamlining maintenance cycles. Through predictive analytics, AI algorithms can anticipate component failures in turbines and generators with over 90% accuracy, significantly reducing unplanned downtime and extending equipment lifespan. Power plant operators are leveraging machine learning models to fine-tune fuel mix optimization, resulting in up to 12% improvement in thermal efficiency across combined cycle plants. Additionally, AI-powered digital twins allow real-time simulation of operational conditions, enabling faster decision-making and risk mitigation.

Grid-connected power generation systems increasingly rely on AI for dynamic load forecasting and grid-balancing operations, which are vital in integrating variable renewable sources. AI systems are also automating diagnostics in wind and solar installations, improving output predictability and minimizing manual inspection costs. The Power Generation Equipment Market is witnessing a steady migration toward AI-based autonomous control systems, especially in remote or off-grid installations. These advancements help utilities and independent power producers (IPPs) reduce operational costs and improve return on investment, while also meeting stricter environmental compliance standards through optimized energy output and emissions control.

“In early 2025, a major U.S.-based energy technology firm successfully deployed an AI-driven predictive maintenance platform across 80 natural gas turbine installations, resulting in a 28% reduction in unscheduled outages and a 15% increase in mean time between failures (MTBF), thereby extending overall equipment reliability and reducing annual maintenance costs by over USD 4 million.”

The Power Generation Equipment Market is undergoing a transformative phase driven by increasing global demand for energy reliability, modernization of legacy systems, and the integration of renewable sources. The sector is evolving with the shift toward digital infrastructure, decarbonization, and distributed energy resources. Rapid industrialization in emerging economies is amplifying the need for scalable, efficient, and low-emission power generation systems. Meanwhile, developed regions are emphasizing retrofitting of existing plants with smart systems and emission control upgrades. Regulatory compliance, cost-effectiveness, and technological flexibility are defining strategic priorities in the procurement and deployment of power generation equipment globally.

The growing deployment of hybrid power systems, combining renewable sources with conventional backup equipment, is a key driver of the Power Generation Equipment Market. These systems require highly adaptive equipment capable of managing variable loads and storage interfaces. In 2024 alone, over 3.5 GW of hybrid energy capacity was installed globally, utilizing AI-enabled generators and advanced energy management systems. Decentralized microgrids, especially in remote and industrial zones, are pushing demand for modular and containerized power solutions. Governments and corporations are investing in such infrastructure for better energy independence, reliability, and sustainability. These developments require next-gen equipment designed to operate autonomously with minimal maintenance.

One of the major restraints impacting the Power Generation Equipment Market is the growing frequency of global supply chain disruptions, particularly in sourcing high-performance materials like specialty alloys, electronic controllers, and semiconductors. In 2024, lead times for critical generator and turbine components increased by over 35% due to geopolitical tensions and logistical bottlenecks. This has resulted in project delays and increased overall capital expenditure. OEMs are also facing shortages of skilled labor, further impacting production timelines. Such challenges are compelling manufacturers and buyers to reconsider sourcing strategies and develop contingency plans, thus increasing operational complexity and cost.

The global shift toward cleaner energy has opened substantial opportunities for hydrogen-based power generation technologies, driving innovation in the Power Generation Equipment Market. By 2025, over 40 pilot hydrogen projects are operational globally, creating demand for new types of combustion turbines and electrolyzers. Equipment manufacturers are developing turbines that can operate on blends of natural gas and hydrogen, while power electronics systems are being redesigned for compatibility with hydrogen production facilities. Nations like Japan and Germany are investing heavily in green hydrogen infrastructure, opening new markets for specialized equipment. The push for zero-emission power generation is expected to accelerate the adoption of hydrogen-compatible machinery.

Compliance with increasingly stringent emission norms is a growing challenge in the Power Generation Equipment Market. Equipment must now meet advanced regulatory standards, particularly regarding nitrogen oxide (NOx) and particulate emissions, leading to increased R&D and manufacturing costs. In the European Union, recent updates to the Industrial Emissions Directive mandate the integration of continuous emissions monitoring systems (CEMS) in most thermal plants. These upgrades require specialized retrofitting, software integration, and maintenance, significantly impacting the overall cost structure. Smaller utilities and IPPs face budgetary constraints in adopting such solutions, delaying modernization efforts and reducing competitiveness in tender-based procurements.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Power Generation Equipment Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Digital Twin Technology: Power plants are increasingly incorporating digital twin solutions into their operational ecosystems. By simulating physical assets and replicating performance in virtual environments, these systems enhance predictive maintenance and optimize output. In 2024, digital twin adoption improved fuel efficiency by 7% and reduced operational costs in over 120 combined-cycle power plants.

Surge in Demand for Grid-Interactive Equipment: Equipment capable of two-way interaction with smart grids is gaining traction, particularly in regions with high renewable penetration. These systems offer voltage regulation, frequency stabilization, and real-time feedback. Manufacturers are investing in inverter-based technologies that support dynamic grid participation, enabling more flexible energy flow management.

Increased Focus on Noise and Emission Reduction: Environmental concerns are driving innovation in low-noise, low-emission generation equipment. In 2025, over 60% of new gas turbines introduced noise-dampening and selective catalytic reduction (SCR) features as standard. These improvements align with urban deployment needs and stricter zoning laws, especially in Asia-Pacific and European cities.

The Power Generation Equipment Market is segmented based on type, application, and end-user, each playing a pivotal role in defining market dynamics and investment strategies. The type segment encompasses a variety of technologies ranging from gas turbines to generators and boilers, each tailored to specific operational needs. Application-wise, the market caters to sectors such as industrial power supply, grid support, and backup power solutions, reflecting varying demand across use cases. In terms of end-users, utilities dominate the landscape, followed by manufacturing, oil & gas, and commercial facilities. Regional deployment patterns also influence segment performance, with Asia-Pacific prioritizing grid expansion and North America investing heavily in grid resilience and renewable integration. Understanding these segmentation layers is crucial for stakeholders aiming to align product development, procurement strategies, and capacity planning with emerging demand trends and evolving regulatory conditions.

The Power Generation Equipment Market encompasses several key product types including gas turbines, steam turbines, generators, boilers, and engines. Among these, gas turbines currently lead the market due to their operational flexibility, high thermal efficiency, and widespread usage in both peaking and base-load plants. Their ability to quickly respond to grid demands makes them ideal for balancing renewable fluctuations.

Generators, particularly those integrated with digital monitoring and control systems, represent the fastest-growing segment, driven by the growing need for grid reliability, distributed generation, and energy resilience in both urban and remote areas. Innovations in generator designs, such as high-speed alternators and brushless excitation systems, are also contributing to their rising adoption across various power configurations.

Steam turbines continue to play a significant role, particularly in coal and nuclear-powered plants, though their growth is moderate due to the energy transition away from fossil fuels. Boilers and engines, though niche in certain geographies, remain essential for captive and industrial power applications, maintaining a steady demand in localized sectors.

The Power Generation Equipment Market serves a diverse array of applications, with grid-based power generation emerging as the dominant application segment. This is largely attributed to the growing emphasis on reliable and uninterrupted energy supply, grid modernization projects, and renewable integration initiatives in developed economies.

The fastest-growing application is in renewable energy integration, where advanced generation equipment supports hybrid systems, microgrids, and variable power sources such as solar and wind. As global renewable capacity continues to expand, power generation equipment that supports voltage and frequency stabilization is increasingly in demand.

Industrial applications remain a key focus, particularly in energy-intensive sectors such as cement, steel, and chemical manufacturing, which require high-capacity, continuous power solutions. Backup power systems, while typically smaller in scale, are gaining traction across hospitals, data centers, and telecommunications facilities due to rising concerns over energy reliability and disaster preparedness. Each of these application areas is evolving rapidly in line with global energy trends and infrastructure resilience requirements.

In the Power Generation Equipment Market, utility companies represent the largest end-user segment. These entities require high-capacity equipment for centralized power plants and national grids, often investing in long-life, high-efficiency systems with integrated emissions controls. The transition toward cleaner energy sources and the growing emphasis on grid stability continue to drive significant procurement in this sector.

Independent Power Producers (IPPs) are the fastest-growing end-user group, supported by deregulated energy markets and public-private partnership models. IPPs are increasingly active in renewable and hybrid project development, often requiring flexible, modular equipment capable of integrating with solar, wind, and storage systems.

Other notable end-users include industrial manufacturers, who deploy on-site generation equipment to ensure power reliability and control energy costs, particularly in regions with unstable grid access. The commercial sector, including large-scale retail complexes, hospitality, and data centers, is also contributing to market growth through steady investments in backup and co-generation equipment tailored for operational continuity and energy optimization.

Asia-Pacific accounted for the largest market share at 42.7% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific’s dominance stems from its extensive infrastructure development, growing energy demand, and robust investments in renewable and hybrid power generation systems. The region's industrial expansion and urbanization across China, India, and Southeast Asia continue to create high-volume demand for scalable and modular generation equipment. Meanwhile, North America’s growth is fueled by rapid digital transformation of power systems, aggressive decarbonization policies, and increasing reliance on distributed energy and microgrid solutions. Additionally, policy-driven incentives and modernization of aging power infrastructure are encouraging public and private investments in cutting-edge equipment such as AI-integrated turbines and grid-interactive systems. These trends are reshaping regional strategies for equipment deployment and long-term sustainability.

North America held a market share of 24.3% in 2024, positioning itself as a critical region in the Power Generation Equipment Market. The demand is largely driven by sectors such as utilities, oil & gas, data centers, and industrial manufacturing. Federal and state-level programs promoting grid modernization, along with incentives for clean energy deployment, are catalyzing equipment upgrades across the U.S. and Canada. For instance, the transition from conventional to smart grids has increased the need for advanced turbines, generators, and hybrid systems that are digitally optimized. Moreover, digital transformation initiatives, including predictive maintenance using AI and the integration of IoT platforms, are enhancing operational efficiency and lifecycle management of installed equipment. These technological enhancements, combined with stricter emissions and safety regulations, are encouraging widespread replacement of aging systems with environmentally compliant, high-performance alternatives.

Europe accounted for 21.5% of the global Power Generation Equipment Market in 2024, with Germany, the UK, and France leading regional consumption. The market is heavily influenced by the European Union’s Green Deal, Net-Zero targets, and stringent industrial emissions standards. These policies are pushing power providers to adopt next-gen, low-emission turbines and renewable-compatible equipment. Germany’s shift away from nuclear and coal has intensified investment in decentralized generation and hydrogen-based systems. France and the UK are rapidly modernizing their national grid networks with advanced digital controls and energy storage integration. Technological adoption is strong across the region, with smart monitoring systems, hybrid plants, and carbon capture-ready generation equipment becoming common. Public funding and compliance-driven investments are expected to sustain demand for power generation equipment tailored for efficiency, flexibility, and environmental responsibility.

Asia-Pacific continues to lead in total volume, with 42.7% market share in 2024, driven by high energy demand across China, India, Japan, and Southeast Asia. China remains the largest single-country consumer, supported by massive investments in utility-scale solar, wind, and thermal plants. India is rapidly scaling its power infrastructure with a strong focus on electrifying rural areas and integrating renewables into its national grid. Japan, meanwhile, emphasizes fuel efficiency and resilient backup systems in its generation strategy. Across the region, manufacturing growth, export-oriented industrial zones, and rising urbanization are intensifying the need for robust and scalable power generation equipment. Regional innovation hubs are also contributing to the development of compact, high-efficiency, and renewable-integrated systems tailored for varied environmental and regulatory conditions. These factors collectively make Asia-Pacific the largest and most strategically vital region in the global Power Generation Equipment Market.

South America contributed approximately 5.6% to the global Power Generation Equipment Market in 2024, with Brazil and Argentina leading regional deployments. Brazil's national energy strategy emphasizes hydro, biomass, and increasingly solar and wind projects, which are stimulating demand for compatible generation equipment. Argentina is expanding natural gas-based generation, requiring flexible gas turbines and hybrid systems. Infrastructure challenges, especially in rural and high-altitude areas, are encouraging localized power generation solutions. Moreover, regional governments are offering incentives for sustainable energy technologies, import tax reductions for clean equipment, and streamlined permitting processes. While the market is smaller compared to other continents, its growth trajectory is supported by rising electricity demand, expanding industrial bases, and government-backed modernization efforts, creating opportunities for both domestic and international equipment manufacturers.

The Middle East & Africa accounted for 5.9% of the Power Generation Equipment Market in 2024, with countries like the UAE, Saudi Arabia, and South Africa driving most of the demand. The region’s requirements are closely tied to oil & gas sector activities, infrastructure development, and expanding commercial construction. The UAE and Saudi Arabia are actively diversifying their energy portfolios through clean energy initiatives, resulting in increased deployment of solar-compatible and hybrid generation systems. South Africa continues to invest in energy security measures, including off-grid and modular power solutions. Technological modernization is gaining momentum through digital platforms for performance monitoring, AI-enhanced maintenance, and mobile power units for temporary and emergency installations. Local trade policies and regional partnerships are also fostering competitive procurement and investment in modern, low-emission equipment across both public and private sectors.

China – 30.8% Market Share

High production capacity and large-scale deployment of both traditional and renewable generation systems.

United States – 19.5% Market Share

Strong end-user demand driven by utility modernization, advanced infrastructure, and digital innovation in energy management.

The Power Generation Equipment Market is characterized by a highly competitive environment involving over 120 active global and regional manufacturers. These players operate across various product segments including turbines, generators, boilers, and engines, serving diverse end-user industries. Leading companies are consistently focused on strengthening their market position through strategic product launches, regional expansion efforts, and technological innovations. A rising trend involves partnerships with digital solution providers to develop AI-integrated systems and predictive maintenance platforms.

Mergers and acquisitions are also shaping the landscape, enabling companies to diversify product portfolios and expand their geographical footprint. Competitive differentiation is increasingly driven by energy efficiency, modular design adaptability, and grid compatibility features. Companies are also investing in R&D to develop equipment capable of supporting hybrid power generation systems and meeting evolving emissions standards. The shift toward decentralized and renewable energy sources has encouraged innovation in low-noise, lightweight, and portable generation units, intensifying the competitive pressure in both industrial and commercial sectors.

Siemens Energy

General Electric (GE)

Mitsubishi Power

Caterpillar Inc.

Wärtsilä Corporation

Cummins Inc.

MAN Energy Solutions

Doosan Enerbility

Rolls-Royce Power Systems

Ansaldo Energia

Kohler Power

MTU Friedrichshafen

Hyundai Heavy Industries

ABB Ltd.

Hitachi Energy

Technological innovation is rapidly reshaping the Power Generation Equipment Market with a strong focus on efficiency, flexibility, and environmental compliance. One of the most transformative technologies is the deployment of digital twin systems, which simulate real-time operational conditions to enable predictive maintenance and improve asset lifecycle performance. Plants utilizing digital twin models have reported up to 20% improvement in operational efficiency and 30% reduction in downtime.

AI and machine learning algorithms are being integrated into generation units to monitor system health, optimize fuel usage, and enable autonomous operations. For example, smart turbines now incorporate sensors that analyze vibration, temperature, and load data to predict potential failures. This helps reduce maintenance costs and ensures uninterrupted operation.

Another key innovation is the development of hydrogen-compatible turbines and combustion systems that can handle fuel blends, addressing the rising demand for clean energy. Modular and skid-mounted systems are gaining traction for their ease of installation, scalability, and adaptability across temporary and remote sites. Emerging markets are also seeing growth in microgrid-ready equipment, which supports decentralized power solutions.

Furthermore, low-emission boilers, high-speed alternators, and variable frequency generators are being engineered to meet increasingly strict global standards for efficiency and environmental impact. These advancements position the industry to respond to the dual demands of energy reliability and sustainability.

• In March 2024, Siemens Energy launched its HL-class gas turbine in India, designed for high-efficiency, flexible operations. The turbine supports hydrogen blending up to 30%, making it suitable for low-carbon power generation.

• In October 2023, Mitsubishi Power installed the world’s first ammonia-fed combustion turbine in Japan. The unit successfully produced electricity while maintaining NOx emissions within regulated limits, advancing alternative fuel integration.

• In January 2024, Cummins Inc. unveiled a new range of hydrogen-fueled generator sets for industrial and commercial sectors. These generators offer a 100% carbon-free power alternative for backup and peak demand usage.

• In July 2023, Wärtsilä completed the deployment of a 100 MW flexible engine-based power plant in the Philippines. The project utilizes seven gas engines with ultra-fast start-up capabilities to stabilize intermittent renewable output.

The Power Generation Equipment Market Report provides a comprehensive analysis of global industry trends, product categories, technology developments, and regional performance. It includes in-depth segmentation by type (gas turbines, steam turbines, generators, boilers, engines), application (grid-based generation, backup power, industrial usage, renewable integration), and end-users (utilities, independent power producers, industrial sectors, and commercial entities).

Geographically, the report covers key regions including Asia-Pacific, North America, Europe, South America, and Middle East & Africa, offering insights into country-specific dynamics, growth opportunities, and regulatory influences.

The scope further extends to evaluating emerging technologies such as AI-integrated control systems, hydrogen-compatible turbines, digital twins, and microgrid-ready solutions. Attention is also given to modular, portable, and low-emission designs, which are gaining momentum in off-grid and developing markets.

The report targets decision-makers across OEMs, utilities, IPPs, EPC contractors, and investors by presenting actionable intelligence on procurement trends, innovation focus areas, and long-term infrastructure planning. It highlights both mature and niche segments, enabling a detailed understanding of the competitive and technological forces shaping the future of global power generation equipment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 239,047.3 Million |

| Market Revenue (2032) | USD 342,560.5 Million |

| CAGR (2025–2032) | 4.6 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Siemens Energy, General Electric (GE), Mitsubishi Power, Caterpillar Inc., Wärtsilä Corporation, Cummins Inc., MAN Energy Solutions, Doosan Enerbility, Rolls-Royce Power Systems, Ansaldo Energia, Kohler Power, MTU Friedrichshafen, Hyundai Heavy Industries, ABB Ltd., Hitachi Energy |

| Customization & Pricing | Available on Request (10 % Customization is Free) |