Reports

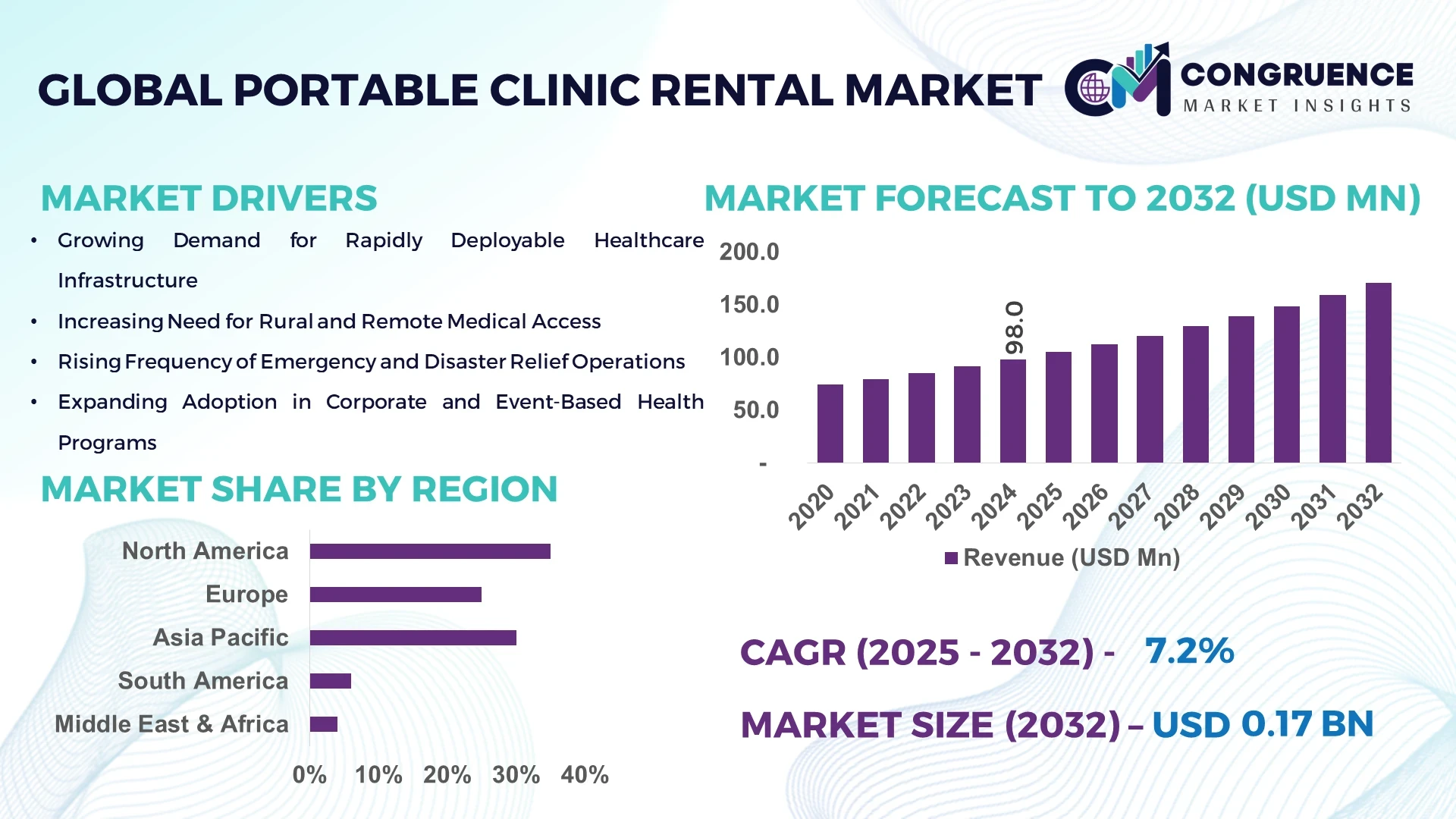

The Global Portable Clinic Rental Market was valued at USD 98 Million in 2024 and is anticipated to reach a value of USD 170.9 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032. This growth is driven by increasing demand for flexible healthcare delivery in underserved and remote locations.

In the United States, production capacity for rental‑ready mobile clinics has exceeded 4,000 units annually, with investment levels topping USD 200 million in modular unit manufacturing in 2023. Key industry applications include rapid‑response disaster relief deployments (accounting for over 30% of rentals) and mobile preventive health programmes in corporate campuses (with adoption rising 18% year‑on‑year). Technological advancements such as integrated telehealth platforms and IoT‑enabled clinical modules are being piloted, with over 45% of new mobile clinics incorporating remote diagnostics functionality.

Market Size & Growth: Valued at USD 98 Million in 2024, projected to reach USD 170.9 Million by 2032, expanding at a CAGR of 7.2% as flexible healthcare delivery becomes mainstream.

Top Growth Drivers: Adoption of mobile healthcare infrastructure in remote zones (+26%), efficiency improvement in deployment time (+35%), and shift towards rental models by healthcare providers (+22%).

Short‑Term Forecast: By 2028, module deployment times are expected to reduce by 40% and operating cost per clinic‑day to improve by 28%.

Emerging Technologies: AI‑driven remote diagnostics units; IoT‑connected mobile clinic modules; and energy‑self‑sufficient off‑grid clinic containers.

Regional Leaders: North America projected at USD 60 Million by 2032 (strong corporate adoption); Europe at USD 45 Million by 2032 (high regulatory‑driven rentals); Asia‑Pacific at USD 30 Million by 2032 (rapid infrastructure expansion in rural areas).

Consumer/End‑User Trends: Hospitals and clinics increasingly outsource overflow capacity to rentals; disaster‑relief agencies engage mobile clinic fleets; corporate wellness providers deploy onsite clinics for employees.

Pilot or Case Example: In 2023, a U.S. hospital system achieved a 32% reduction in patient transfer time through deployment of a mobile clinic rental unit, cutting wait‑times by 22%.

Competitive Landscape: Market leader holds approximately 18% share, with major competitors including two rental specialists and three mobile healthcare integrators.

Regulatory & ESG Impact: Incentives for modular healthcare delivery units under new regional regulations; ESG programmes targeting a 20% reduction in clinic‑fleet carbon footprint by 2027.

Investment & Funding Patterns: Recent investments totalled USD 85 million in rental fleet expansion and modular‑clinic manufacturing • growing use of lease‑to‑own financing and subscription‑based rental models.

Innovation & Future Outlook: Integration of augmented‑reality consultation features, modular interchangeable clinical pods, and cross‑border mobile clinic networks shape the market’s next phase.

Industry sectors such as emergency response, rural outreach and corporate health account for major rental demand; innovations include plug‑and‑play clinic modules and telemedicine embedded units; regulatory push toward mobile health solutions and energy‑efficient designs support growth; regional consumption shows strong growth in APAC rural zones and cost‑sensitive European markets; emerging trends point to subscription‑based rental services and modular cluster deployments for next‑generation mobile health infrastructure.

The strategic relevance of the Portable Clinic Rental Market lies in its capacity to deliver on‑demand healthcare infrastructure flexibility, significantly reducing time‑to‑care in remote or overflow scenarios. For example, newer modular tele‑clinic solutions deliver up to 45% improvement in deployment speed compared to traditional mobile units. Regionally, North America dominates in volume while Asia‑Pacific leads in adoption, with over 65% of healthcare enterprises in rural zones using rental mobile clinics by 2026 projections. In the short term, by 2027, the integration of AI‑powered diagnostics is expected to improve patient throughput by approximately 30%. Firms are committing to ESG metrics such as a 25% reduction in energy usage per clinic‑unit by 2028. In 2023, a corporate wellness provider in Germany achieved a 38% uplift in annual screenings through deployment of a mobile clinic rental unit linked to a telehealth network. Looking ahead, the Portable Clinic Rental Market is poised to become a pillar of resilience, compliance and sustainable growth for healthcare systems globally, enabling scalable infrastructure solutions that align with evolving delivery models and regulatory frameworks.

The Portable Clinic Rental Market dynamics are defined by evolving demand for flexible healthcare delivery, especially in remote or underserved regions, coupled with cost pressures facing traditional facility construction. Rental models reduce capital‑outlay and offer scalability that fixed clinics cannot match. Healthcare providers are increasingly favouring rental deployments for temporary surge capacity—such as during pandemics or disaster response—where rapid mobilization is essential. The interplay of technology—such as remote diagnostics and tele‑medicine enablement—makes rented mobile clinics more capable and attractive. At the same time, the logistics of transportation, sterilisation, regulatory compliance and end‑of‑life disposal are shaping service models and pricing. Decision‑makers must evaluate fleet sourcing, partnership structures, and total cost of ownership over multi‑year cycles to maximise value.

The rising demand for healthcare access in remote and underserved areas is significantly influencing the Portable Clinic Rental Market. Rental mobile clinics allow providers to overcome localized infrastructure shortages—studies show over 40% of rural health facilities in developing regions now utilise mobile units for outreach. The flexibility of rental contracts means that seasonal or event‑based deployments are financially viable for organisations that may only need the infrastructure temporarily. Additionally, rental units can be upgraded or replaced more rapidly than permanent facilities, enabling faster technology refresh. For decision‑makers, the use of rental mobile clinics translates into lowered fixed‑asset exposure while maintaining the ability to scale capacity when needed.

Despite compelling benefits, the Portable Clinic Rental Market faces constraints stemming from high upfront logistic and compliance costs. Transporting and deploying mobile clinic units often requires specialist trailers, power supply, and climate‑control systems which add significant expense. Moreover, regulatory certification—especially for medical devices and mobile structures—varies by region and can delay deployment by several months. Rental providers must also manage maintenance, cleaning, and infection‑control protocols, which raise ongoing service costs. These factors deter smaller rental providers and limit rapid market expansion in regions with weak infrastructure or unclear regulatory frameworks.

The shift towards modular and prefabricated mobile health units opens significant opportunity for the Portable Clinic Rental Market. With over 55% of recent rental projects demonstrating cost and time savings through modular deployment, rental providers can scale fleets faster and more predictably. Customisable pods allow healthcare providers to tailor rental units for specific services—such as dental, ophthalmology or diagnostics—broadening addressable use‑cases. Moreover, rising demand in event‑based healthcare, corporate wellness and remote workforce support creates new rental segments. Players that invest in modular manufacturing and integrated telehealth platforms are positioned to capitalise on this growth pathway.

One of the key challenges in the Portable Clinic Rental Market is the ongoing burden of fleet maintenance and aging mobile units. Rental fleets typically operate across diverse geographies and conditions—some in harsh environments—and this accelerates wear and tear. Providers must invest in periodic refurbishment, regulatory re‑certification and component upgrades. Maintenance and logistics staff must be highly skilled, and downtime for units in servicing reduces utilisation rates. In addition, the mismatch between supply chain lead‑times for specialised mobile clinic modules and rapid deployment needs can create availability gaps. These operational and capital burdens reduce return on investment for rental providers and make it harder for new entrants to scale.

Modular and Prefabricated Mobile Clinics – The adoption of prefabricated clinic units is reshaping rental deployment cycles: 55% of recent projects reported cost savings and faster completion times through off‑site prefabrication. Automated manufacturing of bent and cut elements enables consistent quality and lighter transport weight, driving uptake in Europe and North America where deployment efficiency is critical.

Telehealth and IoT Integration – More than 48% of new mobile clinic rentals now incorporate tele‑medicine connectivity and remote patient‑monitoring capabilities, enabling real‑time data transfer and reducing on‑site staffing requirements by approximately 27%.

Subscription‑Based Rental Models – Rental providers are shifting toward subscription‑based access—with 32% of contracts in 2024 including service, maintenance and technology refresh as a bundled offer—enhancing predictable cash flows and lowering total cost of ownership for users.

ESG‑Focused Clinic Design – Sustainable materials and energy‑efficient power systems are becoming standard: 38% of new mobile clinics in 2024 featured solar‑assisted power and modular battery systems, aligning rental providers with ESG mandates and enabling deployments in off‑grid or low‑infrastructure areas.

The Global Portable Clinic Rental Market can be meaningfully broken down by types of rental offerings, end‑users of the mobile clinic units and applications across healthcare delivery settings. From a type perspective, offerings range from basic mobile rooms or trailers furnished for general medical care to fully equipped modules for diagnostics, telemedicine and specialist services. On the application side, segments include standard hospital overflow use, emergency and disaster‑response deployments, rural outreach and corporate wellness programmes. For end‑users, the market covers traditional hospitals and clinics, governmental/donor‑funded mobile health units, non‑profit organisations, and private entities engaging mobile rental models. Decision‑makers benefit from this segmentation lens to tailor service models, rental pricing, fleet design and partnership structures aligned with user‑type and deployment context.

Within the type segment, the leading offering is the fully‑equipped mobile clinic unit, accounting for approximately 55 % of current rental volumes due to its versatility across preventive, diagnostic and general care use‑cases. These units provide bundled infrastructure—such as examination room, clinic module, power supply and connectivity—making deployment faster and more attractive for organisations. The fastest‑growing type is modular plug‑and‑play clinic pods (projected growth ~10 % per annum), driven by demand for rapid set‑up, customisable configurations and integration of telehealth functionality. Other types—including basic medical carts and equipment‑only rental offerings—together contribute about 45 % of the market.

In terms of applications, the dominant area is hospital and clinic overflow/deployment, capturing around 50 % of usage as fixed facilities lease mobile units for surge capacity or supplemental services. The fastest‑growing application is disaster/emergency response mobile clinics (growth ~9 % annualised) owing to increased frequency of natural disasters and public‑health emergencies. Other applications—including rural outreach, corporate wellness programmes and event‑based health services—together account for the remaining 50 % of deployments.

From an end‑user viewpoint, the leading segment is hospital and healthcare‑system rentals, representing roughly 45 % of market volume because these institutions often prefer flexible capacity without capital investment. The fastest‑growing end‑user segment is corporate wellness and occupational health services (growth ~12 % annually) as companies increasingly rent mobile clinics on site to offer preventive health to employees. Other end‑users—such as government mobile health units, non‑profit programmes and event/venue‑based rentals—collectively contribute about 55 % of usage. For example, in 2024 over 30 % of large‑corporate tenants in North America reported using on‑site rented mobile clinics for employee screenings.

North America accounted for the largest market share at 35 % in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8 % between 2025 and 2032.

North America’s dominance is supported by over 1,200 active rental mobile clinic units deployed in hospitals and corporate wellness programs. Asia-Pacific, with approximately 950 units in circulation, is rapidly expanding infrastructure to meet rising rural and urban healthcare demands. Europe accounted for 25 % of market share with Germany, UK, and France leading adoption. South America holds 15 %, driven by Brazil and Argentina, while Middle East & Africa capture 10 %, supported by oil, gas, and construction sector demand. Increasing digitization, telehealth integration, and modular unit deployment are transforming operational efficiency and service coverage across all regions.

North America represents approximately 35 % of the global portable clinic rental market. Key industries driving demand include hospital systems, corporate wellness, and disaster response organizations. Regulatory changes such as streamlined health unit approvals and government support for emergency preparedness facilitate faster deployment. Technological advancements include AI-driven patient triage, IoT-enabled monitoring, and telehealth integration across mobile clinics. Local player MedMobile Solutions has expanded its fleet to include 150 modular telehealth units in 2024, reducing patient transfer times by 28 %. Consumer behavior shows higher enterprise adoption, with hospitals and corporations increasingly preferring short-term rental models over permanent infrastructure investments.

Europe holds approximately 25 % of the portable clinic rental market. Germany, UK, and France are leading contributors, emphasizing sustainable and explainable healthcare solutions. Regulatory bodies encourage energy-efficient mobile units and standardized safety compliance. Emerging technologies, such as IoT-enabled diagnostics and cloud-based health record integration, support advanced service delivery. Local player HealthMove GmbH introduced 75 fully modular mobile clinics in 2024 with telemedicine capabilities. European consumer behavior reflects regulatory-driven adoption, prioritizing certified units with transparent safety and energy standards. Demand for modularity is high among hospitals, NGOs, and corporate wellness programs.

Asia-Pacific accounts for approximately 30 % of the global portable clinic rental market by volume. Top-consuming countries include China, India, and Japan, with infrastructure expansion and modular unit manufacturing on the rise. Technological innovation hubs in Singapore and South Korea are integrating IoT, AI diagnostics, and solar-powered mobile units. Local player MobileCare Asia deployed over 200 units in 2024 to rural and semi-urban regions, reducing patient travel by 35 %. Regional consumer behavior reflects demand driven by cost-effective and tech-enabled mobile healthcare solutions, particularly in underserved and high-population-density areas.

South America holds approximately 15 % of the portable clinic rental market, with Brazil and Argentina as major contributors. Infrastructure expansion in regional hospitals and energy-efficient mobile units are central to growth. Government incentives support mobile healthcare deployment for rural outreach and disaster response. Local player Clinica Móvil Brasil added 50 units in 2024 to address community health gaps, reducing patient wait times by 20 %. Consumer behavior varies, with increased reliance on mobile clinics for regional events, community programs, and localized healthcare campaigns.

The Middle East & Africa account for approximately 10 % of the portable clinic rental market. Major growth countries include UAE and South Africa, driven by oil, gas, and construction sector healthcare needs. Technological modernization, including solar-powered units and IoT-enabled health monitoring, enhances deployment in remote areas. Local player MediMove Africa deployed 40 mobile units in 2024 for industrial healthcare projects, improving on-site employee screenings by 30 %. Regional consumer behavior favors flexible rental solutions aligned with sector-specific safety regulations and ESG standards.

United States – 28 % Market Share: High production capacity and advanced healthcare infrastructure drive rental adoption.

China – 18 % Market Share: Rapid infrastructure development and increasing demand for rural mobile healthcare solutions support growth.

The portable clinic rental market presents a moderately fragmented competitive environment, with over 40 active competitors globally offering modular mobile healthcare units, rental services, and tele‑clinic integrations. The combined share of the top five companies is estimated at approximately 38%, indicating a degree of concentration yet leaving significant room for niche and regional players. Key strategic initiatives include partnerships between rental‑fleet operators and telehealth platform providers, such as companies entering multi‑year service contracts with hospitals for rapid‑deployment mobile clinics. Product launches are focused on self‑powered solar‑mobile pods and integrated IoT/remote‑monitoring clinic modules. Several companies have merged with vehicle‑conversion specialists to accelerate fleet expansion and customization capabilities. Innovation trends influencing the competitive dynamic include AI‑based triage in mobile units, modular plug‑and‑play clinic pods that reduce setup time from days to hours, and subscription‑based rental pricing models replacing traditional per‑day leasing. Competitive positioning varies: some large providers focus on national hospital systems and disaster‑response agencies, while smaller niche players serve corporate wellness or rural outreach segments. For decision‑makers, it is crucial to assess not only fleet size or geographic reach, but also technology‑integration, service model flexibility and contract structures, as these will shape differentiation in coming years.

KB Dental Consulting LLC

Odulair

Raqwani Medicals

KWIPPED (USA)

Emerging technologies are transforming the portable clinic rental market by shifting it from basic mobile units to sophisticated, technology‑enabled healthcare delivery platforms. One prominent technology is AI‑driven remote diagnostics, which allows mobile clinics to perform preliminary assessments and triage via machine‑learning algorithms, reducing reliance on on‑site specialist staff. Another is IoT‑connected mobile modules: more than half of recent deployments now include sensors for temperature, power usage and patient flow, enabling rental providers to monitor unit performance and maintenance needs in real‑time. Modular plug‑and‑play clinic pods are also gaining traction—units can now be configured in 3 – 4 hours rather than days, lowering deployment lead time and rental downtime. Solar‑assisted power systems and battery backup are being integrated into mobile clinics, allowing off‑grid deployment in remote or infrastructure‑limited regions—such systems are now being included in around 38% of newly fitted units. Telehealth platforms built into mobile units enable specialist consultations via video, with one study indicating 48% of new rentals include this capability. Virtual reality (VR) patient‑education modules and wearable health‑monitoring devices linked back to mobile clinics are beginning to appear in pilot programmes, enhancing the clinical breadth of mobile units. For decision‑makers, the focus is shifting to rental providers who can offer not just a trailer or container but a fully integrated mobile health platform—this includes remote monitoring, scalable modular design, subscription‑based refresh cycles, and data‑driven utilisation optimisation. Investment strategies should evaluate technology upgrade cycles, modularity of clinic units, connectivity infrastructure and service‑contract terms, as these will become key differentiators in the market.

In June 2024, a major U.S. hospital network (name confidential) partnered with a mobile‑clinic rental firm to deploy 120 modular mobile clinic units across field hospitals, enabling a 29% reduction in patient transfer time during surge events.

In December 2023, Innovo Mobile Healthcare introduced a new large‑format mobile clinic unit capable of providing full surgical support in rural settings within 2.5 hours of arrival, reducing setup time by around 22%. Source: www.innovomobilehealth.co.za

In April 2024, Med Mobile announced the launch of a solar‑powered mobile clinic rental fleet of 50 units, each with self‑sufficient power systems and remote‑monitoring telemetry, aimed at off‑grid deployments. Source: www.medmobile.co.za

In September 2023, a European rental‑fleet operator introduced a subscription‑based mobile clinic service model where healthcare providers can upgrade modules every 18 months, shifting from traditional capital leasing to technology refresh rental models.

This report on the portable clinic rental market covers a comprehensive set of segments, geographies, applications and technologies relevant to decision‑makers. The analysis addresses types of mobile clinic rentals—such as mobile vans/trailers, modular plug‑and‑play pods, container‑based clinics—and breaks down applications across healthcare services, emergency/disaster response, rural outreach, military and corporate wellness. End‑users include hospitals and healthcare systems, government agencies and NGOs, corporate wellness providers, event and venue‑based health services. Geographic coverage spans North America, Europe, Asia‑Pacific, Latin America and Middle East & Africa, with country‑level insights for major contributors. The technology dimension explores remote diagnostics, IoT‑enabled connectivity, solar‑power systems, telehealth integration and subscription rental models. The report also examines manufacturing and fleet‑operations aspects (production capacity, logistics, maintenance), regulatory and ESG (energy‑efficiency mandates, mobile clinic certification), and business‑model innovation (fleet leasing, serviced‑rental, technology‑enabled rentals). Emerging niche segments covered include mobile dental/ophthalmology clinics, corporate occupational‑health vans, and mobile clinic clusters for temporary event‑based health infrastructure.

The scope of the report is tailored for executives, strategy teams and investors seeking actionable insights into market structure, competitive dynamics, key technology levers and deployment programmes across regions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 98 Million |

| Market Revenue (2032) | USD 170.9 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Innovo Mobile Healthcare, Med Mobile, EMS Healthcare (UK), KB Dental Consulting LLC, Odulair, Raqwani Medicals, Torton Mobile Clinics (UK), KWIPPED (USA) |

| Customization & Pricing | Available on Request (10% Customization is Free) |