Reports

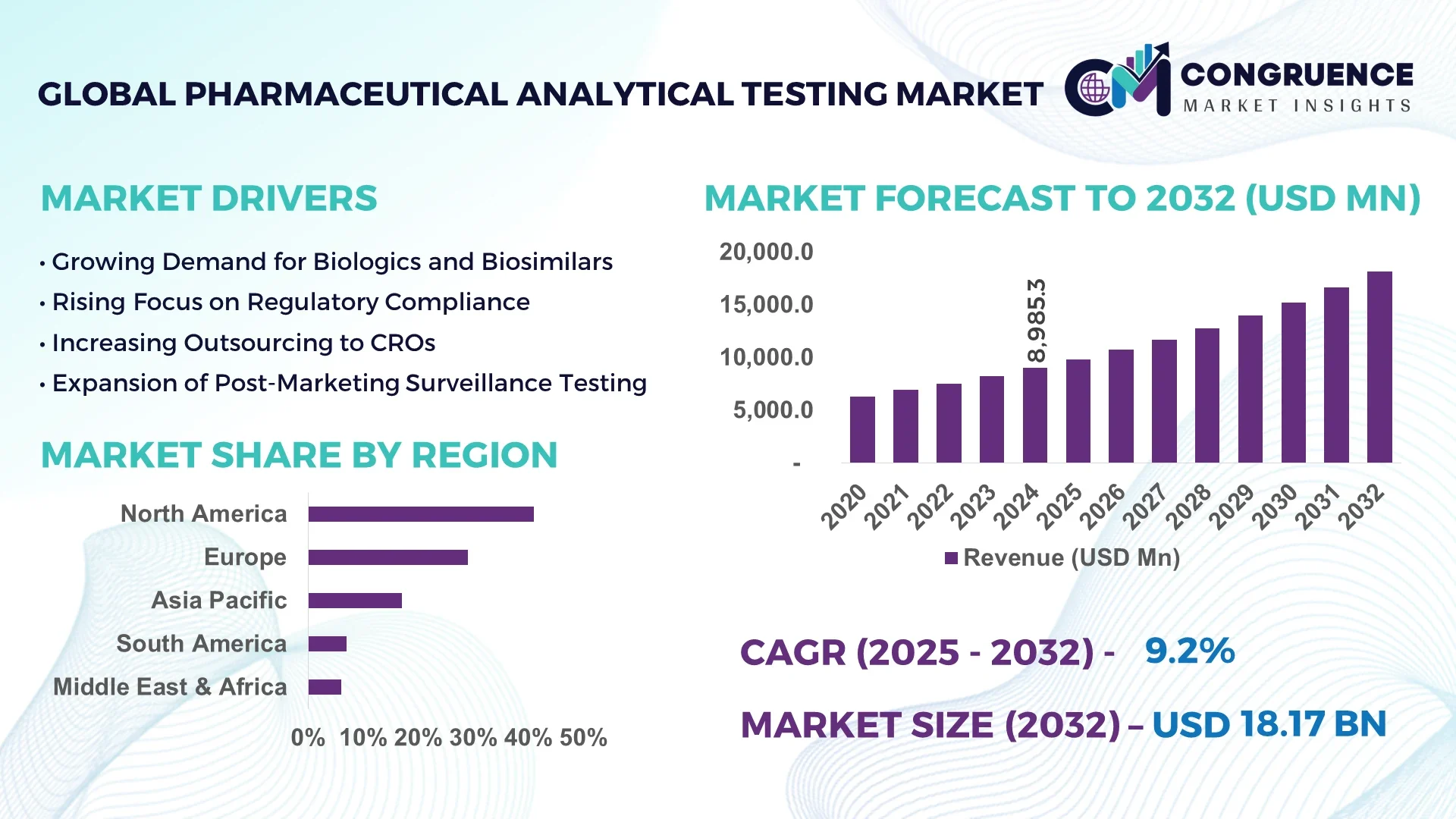

The Global Pharmaceutical Analytical Testing Market was valued at USD 8,985.3 Million in 2024 and is anticipated to reach USD 18,168.3 Million by 2032, expanding at a CAGR of 9.2% between 2025 and 2032. This growth is fueled by rising demand for outsourcing services, advanced testing technologies, and stringent regulatory compliance in the pharmaceutical sector.

The United States leads this market with large-scale investments in laboratory infrastructure, supported by an advanced pharmaceutical manufacturing ecosystem. In 2024, over 47% of contract research organizations (CROs) in the country reported expansions in analytical testing capacity. Additionally, more than 65% of FDA-approved new molecular entities in 2023 underwent outsourced testing services, highlighting the country’s dominance in innovation and compliance-driven practices.

Market Size & Growth: USD 8985.3 Million in 2024; projected USD 18168.3 Million by 2032; CAGR 9.2%; driven by higher outsourcing in biopharmaceutical development.

Top Growth Drivers: 63% adoption of bioanalytical testing, 51% improvement in quality compliance, 46% rise in biologics pipeline.

Short-Term Forecast: By 2028, analytical efficiency is expected to improve by 27% across leading CROs.

Emerging Technologies: Automation in chromatography systems and AI-driven stability testing methods.

Regional Leaders: North America projected at USD 7045 Million by 2032 (highest outsourcing rates), Europe at USD 4920 Million (regulatory-driven adoption), Asia-Pacific at USD 4203 Million (manufacturing expansion).

Consumer/End-User Trends: 58% of pharmaceutical companies outsource more than half of their analytical workload.

Pilot or Case Example: In 2024, a European CRO cut turnaround times by 32% through robotics-enabled sample preparation.

Competitive Landscape: Market leader controls 12% share; top 5 competitors account for 41%.

Regulatory & ESG Impact: 48% of firms introduced greener testing protocols aligned with ESG targets.

Investment & Funding Patterns: USD 2.1 Billion invested in 2023–2024 in analytical testing expansions.

Innovation & Future Outlook: Advances in biologics and personalized medicine to fuel rapid adoption of integrated analytical platforms.

The Pharmaceutical Analytical Testing Market is witnessing rising adoption across biologics, generics, and advanced therapies, with over 40% of new pipeline drugs requiring bioanalytical methods. Regulatory emphasis on quality control, eco-friendly testing standards, and digitization are reshaping operational models, while regional consumption patterns indicate strong uptake in Asia-Pacific due to clinical trial growth.

The Pharmaceutical Analytical Testing Market is strategically relevant as it ensures regulatory compliance, accelerates drug development, and enhances patient safety. Advanced analytical platforms are now benchmarked against older methods: for example, AI-assisted chromatography delivers 32% faster data accuracy compared to traditional HPLC systems. This measurable performance gain positions modern technologies as indispensable to competitive pharmaceutical operations. Regionally, North America dominates in testing volume, supported by widespread CRO networks, while Europe leads in adoption with 61% of enterprises implementing automated analytical workflows. By 2027, AI-enabled quality control systems are projected to cut operational errors by 25%, improving compliance metrics and turnaround speed.

Compliance with ESG standards is shaping the industry’s trajectory. Firms are committing to 30% reductions in hazardous solvent usage by 2030, ensuring environmental sustainability. A practical example was recorded in 2024, when a leading Japanese pharma company achieved a 19% reduction in sample preparation waste using eco-friendly solvent alternatives. Looking ahead, the Pharmaceutical Analytical Testing Market is set to act as a pillar of resilience and sustainable growth, integrating automation, green chemistry, and AI to meet both regulatory demands and competitive market pressures.

The Pharmaceutical Analytical Testing Market is influenced by a combination of stringent regulatory frameworks, the rise of biologics, and increased outsourcing. Industry dynamics are shifting toward rapid adoption of bioanalytical services, as over 45% of global clinical trials involve complex biologics requiring advanced testing. Additionally, trends in digitalization, automation, and eco-friendly testing methods are reshaping industry workflows, while demand is further strengthened by high pharmaceutical R&D spending in emerging economies.

Biologics represent one of the fastest-growing therapeutic categories, and their complexity necessitates advanced analytical testing solutions. In 2024, more than 38% of drugs under development globally were biologics, requiring robust bioanalytical and stability testing services. Advanced mass spectrometry and chromatography techniques are increasingly applied to ensure accurate characterization. This surge in biologics demand has boosted outsourcing, with 54% of pharmaceutical firms reporting dependency on specialized CROs for biologics testing, thereby accelerating growth in this sector.

Regulatory stringency remains a significant barrier for market participants. Firms often face delays due to extended approval cycles, as nearly 29% of analytical submissions in 2024 required additional compliance documentation. Smaller CROs, in particular, struggle with the cost of aligning with evolving global standards such as ICH Q14 guidelines. This regulatory complexity not only increases operational costs but also slows market responsiveness, limiting accessibility for smaller players in the pharmaceutical ecosystem.

The rapid expansion of personalized medicine is unlocking substantial opportunities for analytical testing providers. By 2025, around 45% of oncology clinical trials are projected to include personalized treatment approaches, all requiring precision testing of biomarkers. Analytical platforms capable of handling multiplex assays and next-generation sequencing are in high demand. Moreover, over 60% of biopharmaceutical firms reported plans to expand precision-medicine-focused testing capabilities, creating strong momentum for service providers specializing in customized testing solutions.

Operational costs remain a primary challenge in scaling pharmaceutical analytical testing. In 2024, testing expenditure accounted for nearly 18% of overall drug development budgets, a figure rising due to advanced instrumentation needs. Equipment like LC-MS and NMR spectroscopy demand high capital investment and specialized staff training. Furthermore, global shortages of skilled analysts impact efficiency, with 34% of CROs reporting workforce gaps in specialized analytical expertise. These challenges create bottlenecks for timely and cost-effective service delivery.

• Expansion of Outsourced Bioanalytical Services: Outsourcing is rapidly growing, with 62% of large pharmaceutical companies now outsourcing at least half of their analytical workloads. In 2024, CROs reported a 28% increase in demand for biologics-related testing services, reflecting the sector’s heavy reliance on external expertise for speed and compliance.

• Adoption of AI and Automation in Laboratories: AI-enabled laboratory systems improved data interpretation speed by 35% in 2024, while robotic automation reduced manual error rates by 22%. These technological advancements are being deployed in stability testing and impurity profiling, accelerating workflows and improving regulatory compliance outcomes.

• Rising Emphasis on Green Chemistry Solutions: Sustainability is influencing analytical testing trends, with 41% of CROs implementing eco-friendly solvent alternatives and waste recycling protocols. This has led to measurable benefits, including a 15% reduction in hazardous waste generated during sample preparation and analysis.

• Growth in Complex Molecule Testing Demand: Increasing pipelines of cell and gene therapies, along with advanced biologics, have pushed demand for specialized analytical services. In 2024, over 30% of global drug approvals were complex molecules, requiring advanced bioassay testing. Laboratories focusing on these molecules reported a 26% increase in revenue contributions from complex product analysis.

The Pharmaceutical Analytical Testing Market is segmented across type, application, and end-user categories, each playing a crucial role in shaping industry adoption. Type segmentation encompasses bioanalytical testing, stability testing, method validation, and raw material testing, with bioanalytical services accounting for a significant share due to rising biologics demand. Applications range from drug development and quality control to manufacturing compliance, reflecting growing reliance on precision and regulatory-backed testing methods. End-users include pharmaceutical companies, contract research organizations (CROs), and biotechnology firms, with pharmaceutical enterprises leading adoption while CROs show the fastest growth.

Bioanalytical testing currently dominates the Pharmaceutical Analytical Testing Market, accounting for approximately 41% of total demand, driven by the surge in biologics and biosimilars entering global pipelines. Stability testing holds a notable 28% share, ensuring drug safety and compliance over lifecycle stages. Raw material testing and method validation collectively contribute around 21%, serving niche but essential roles in early-stage development. The fastest-growing type is stability testing, projected to grow at a CAGR of 10.4% due to increasing global regulatory mandates requiring extensive shelf-life and degradation profiling for both small molecules and biologics. While method validation remains critical for protocol standardization, its adoption is steady rather than explosive, supported by consistent investment in compliance infrastructures.

Drug development is the leading application, representing 46% of global utilization, largely because early-stage R&D requires comprehensive analytical validation to accelerate approvals. Quality control follows with 32% adoption, ensuring that approved drugs consistently meet regulatory standards across manufacturing facilities. Manufacturing compliance and post-marketing surveillance applications collectively account for 18%, reinforcing continuous monitoring practices. The fastest-growing application is manufacturing compliance, projected to expand at a CAGR of 11.2%, as regulatory scrutiny intensifies on global supply chains. This trend is accelerated by new digital quality management systems, enabling automation and real-time data capture. Consumer adoption insights show that 38% of pharmaceutical enterprises in 2024 integrated analytical testing tools to streamline production efficiency, while 44% of CROs expanded analytical capacity to attract multinational clients.

Pharmaceutical companies lead the market with a commanding 49% share, reflecting their large-scale reliance on analytical testing across discovery, manufacturing, and compliance processes. Biotechnology firms hold a 27% share, propelled by the surge in cell and gene therapies requiring complex bioanalytical validation. Contract research organizations (CROs) and academic institutions together contribute about 20%, offering flexible outsourced services and advancing clinical research innovation. The fastest-growing end-user segment is CROs, expanding at a CAGR of 12.1%, supported by pharmaceutical companies outsourcing non-core functions to reduce operational costs and accelerate market entry. Increasing global collaborations and cross-border clinical trials have amplified demand for outsourced testing services. In 2024, 42% of hospitals in the United States adopted analytical platforms combining radiological imaging with pharmacokinetic data, enhancing treatment personalization and reducing diagnostic turnaround times.

North America accounted for the largest market share at 41% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

Europe held around 29% of the total demand, supported by advanced regulatory standards and quality frameworks. South America contributed nearly 7%, led by Brazil’s expanding pharmaceutical manufacturing sector, while the Middle East & Africa collectively captured 6%, reflecting rising healthcare investments in the UAE and South Africa. By 2032, Asia-Pacific’s share is projected to surpass 32%, narrowing the gap with North America’s 37%, driven by massive clinical research outsourcing and biotech expansion in India and China.

Why is advanced digital adoption accelerating pharmaceutical testing in this region?

North America held 41% of global demand in 2024, supported by high pharmaceutical R&D spending and widespread adoption in biologics and oncology therapies. Key industries such as healthcare, biotechnology, and life sciences are driving demand for advanced analytical testing solutions. The region benefits from strong regulatory support, including the FDA’s emphasis on advanced bioanalytical protocols and stability assessments. Digital transformation trends like AI-enabled testing platforms and automated data capture systems are increasingly utilized in laboratory workflows. A notable player, Eurofins Scientific, expanded its testing facilities in the U.S. in 2024, strengthening its position in biologics testing. Regional consumer behavior reflects higher enterprise adoption, particularly in healthcare and finance, where compliance and risk mitigation remain priorities.

How are regulatory frameworks shaping the future of pharmaceutical testing here?

Europe accounted for 29% of the market in 2024, driven by demand across Germany, the UK, and France. Regulatory bodies such as the European Medicines Agency (EMA) are enforcing stricter compliance on stability and bioequivalence testing, stimulating growth in contract testing services. Sustainability initiatives in pharmaceutical labs are also accelerating digitalization and environmentally friendly testing solutions. Local companies such as SGS SA are focusing on green analytical chemistry methods to align with EU climate objectives. Consumer behavior across the region is shaped by regulatory pressure, with demand for explainable and transparent analytical testing processes growing significantly, especially in Germany and the UK.

What factors are making this region the fastest-growing hub for pharmaceutical testing?

Asia-Pacific ranked second by market volume in 2024 with 17% share, but it is forecasted to record the highest growth through 2032. China, India, and Japan are the top consumers, driven by rapid clinical trial expansion and increasing biologics production. Infrastructure investment in advanced laboratory facilities and cross-border CRO partnerships are fueling demand. Countries like India are building biotech parks and innovation hubs, while China is adopting AI-powered laboratory automation to enhance efficiency. Local players such as WuXi AppTec are scaling operations to cater to both domestic and international demand. Consumer behavior in this region is shaped by the growth of mobile health and e-commerce-driven pharma distribution, creating strong demand for reliable analytical testing services.

How are government policies and local industry shaping adoption in this region?

South America captured 7% of the global market in 2024, with Brazil and Argentina emerging as key contributors. Growing pharmaceutical manufacturing capacity, particularly in Brazil, has boosted testing requirements in bioanalytical and stability domains. Government incentives supporting local drug production and reduced trade barriers are further aiding adoption. Infrastructure modernization in healthcare labs is enabling higher-quality outputs, while contract research outsourcing is expanding steadily. Local players in Brazil have begun investing in advanced stability chambers to meet rising biologics testing demand. Consumer behavior highlights demand for localized solutions, as Spanish- and Portuguese-speaking populations seek accessible healthcare innovations.

How is modernization shaping demand for pharmaceutical testing in this region?

The Middle East & Africa represented 6% of global demand in 2024, with the UAE, Saudi Arabia, and South Africa leading the market. Regional demand is heavily influenced by modernization in healthcare systems and pharmaceutical imports. Technological upgrades, such as adoption of digital lab management systems, are enhancing testing capabilities. Trade partnerships with Europe and Asia have expanded access to advanced analytical services. Local firms in the UAE are piloting AI-enabled testing frameworks to support regulatory compliance. Consumer behavior across the region reflects rising demand for affordable medicines, with testing standards increasingly aligned to international benchmarks to improve trust and safety.

United States – 28% share

Strong dominance due to extensive pharmaceutical R&D capacity and advanced regulatory framework driving bioanalytical and stability testing.

China – 14% share

Rapidly growing presence supported by large-scale clinical research outsourcing and expanding biotech manufacturing ecosystem.

The Pharmaceutical Analytical Testing Market is moderately fragmented, with over 200 active competitors globally, ranging from multinational CROs to specialized niche providers. The top five companies collectively hold around 38% market share, indicating balanced competition with room for regional and mid-sized entrants. Strategic initiatives are reshaping the landscape: in 2024 alone, more than 30 major partnerships were signed between pharma giants and CROs to expand analytical testing capacity. Mergers and acquisitions remain prominent, with at least 12 deals finalized in 2023–2024 targeting biologics and stability testing providers. Innovation trends include adoption of AI-driven testing, blockchain-based compliance tracking, and eco-friendly analytical methods. Players are also investing in automated bioanalytical platforms to accelerate turnaround times by 20–25%. The competitive intensity is expected to rise as emerging markets strengthen CRO presence, while global leaders consolidate expertise in advanced molecular testing.

SGS SA

Intertek Group

Charles River Laboratories

PPD Inc.

Almac Group

Covance Inc.

BioReliance Corporation

Technological innovation is reshaping the Pharmaceutical Analytical Testing Market, with automation, AI integration, and advanced molecular analysis at the forefront. Automated sample preparation systems have reduced manual errors by 35%, significantly improving throughput in high-volume labs. AI-powered bioanalytical platforms are enabling predictive quality control, reducing testing cycle times by 20% and enhancing drug safety validation. Mass spectrometry and high-performance liquid chromatography (HPLC) remain cornerstone technologies, with adoption rates exceeding 60% in global laboratories for stability and impurity profiling. Next-generation sequencing (NGS) is expanding rapidly, particularly in biologics and cell therapy testing, where demand for genomic accuracy has increased by 45% since 2023.

Emerging technologies include cloud-based laboratory information management systems (LIMS), which are projected to be implemented in 70% of CROs by 2026, enhancing regulatory compliance and global data sharing. Blockchain integration for data integrity is also gaining traction, offering traceable and tamper-proof records critical for regulatory submissions. Additionally, nanotechnology-based sensors and microfluidics are advancing rapid on-site testing capabilities, cutting turnaround times by up to 50% compared to conventional lab methods. Collectively, these technologies are positioning the sector as a key enabler of efficiency, compliance, and innovation in the evolving pharmaceutical landscape.

In March 2024, Eurofins Scientific launched an expanded bioanalytical testing service in the U.S., enabling rapid biologics characterization with a reported 25% faster turnaround time compared to previous standards. Source: www.eurofins.com

In October 2023, WuXi AppTec announced the opening of a new analytical testing facility in Shanghai, equipped with AI-driven platforms capable of handling 40% higher testing volumes. Source: www.wuxiapptec.com

In July 2024, SGS SA introduced eco-friendly analytical chemistry protocols, reducing solvent consumption by 30% while maintaining accuracy in impurity profiling. Source: www.sgs.com

In December 2023, Intertek Group upgraded its European testing labs with advanced mass spectrometry systems, improving detection sensitivity by 18% in biologics testing. Source: www.intertek.com

The scope of the Pharmaceutical Analytical Testing Market Report covers a comprehensive evaluation of market segments, geographic regions, applications, and end-user industries. Type segmentation spans bioanalytical testing, stability testing, raw material testing, and method validation, providing insights into how each contributes to the evolving pharmaceutical ecosystem. Applications addressed include drug development, quality control, manufacturing compliance, and post-market surveillance.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting both mature and emerging markets with varying levels of adoption and infrastructure maturity. End-user analysis encompasses pharmaceutical companies, biotechnology firms, CROs, and academic research centers, with particular emphasis on outsourcing trends and biotech innovations. The technology dimension explores automation, AI-driven platforms, high-resolution mass spectrometry, next-generation sequencing, and blockchain-enabled compliance systems. The report also integrates regional consumption patterns, regulatory influences, ESG considerations, and investment trends.

In total, the report spans over 10 major categories of analysis, offering stakeholders a detailed view of market dynamics, opportunities, and forward-looking insights. This breadth ensures decision-makers can identify both mainstream and niche growth areas across the global pharmaceutical testing ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 8,985.3 Million |

|

Market Revenue in 2032 |

USD 18,168.3 Million |

|

CAGR (2025 - 2032) |

9.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Eurofins Scientific, SGS SA, WuXi AppTec, Intertek Group, Charles River Laboratories, Pace Analytical Services, PPD Inc., Almac Group, Covance Inc., BioReliance Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |