Reports

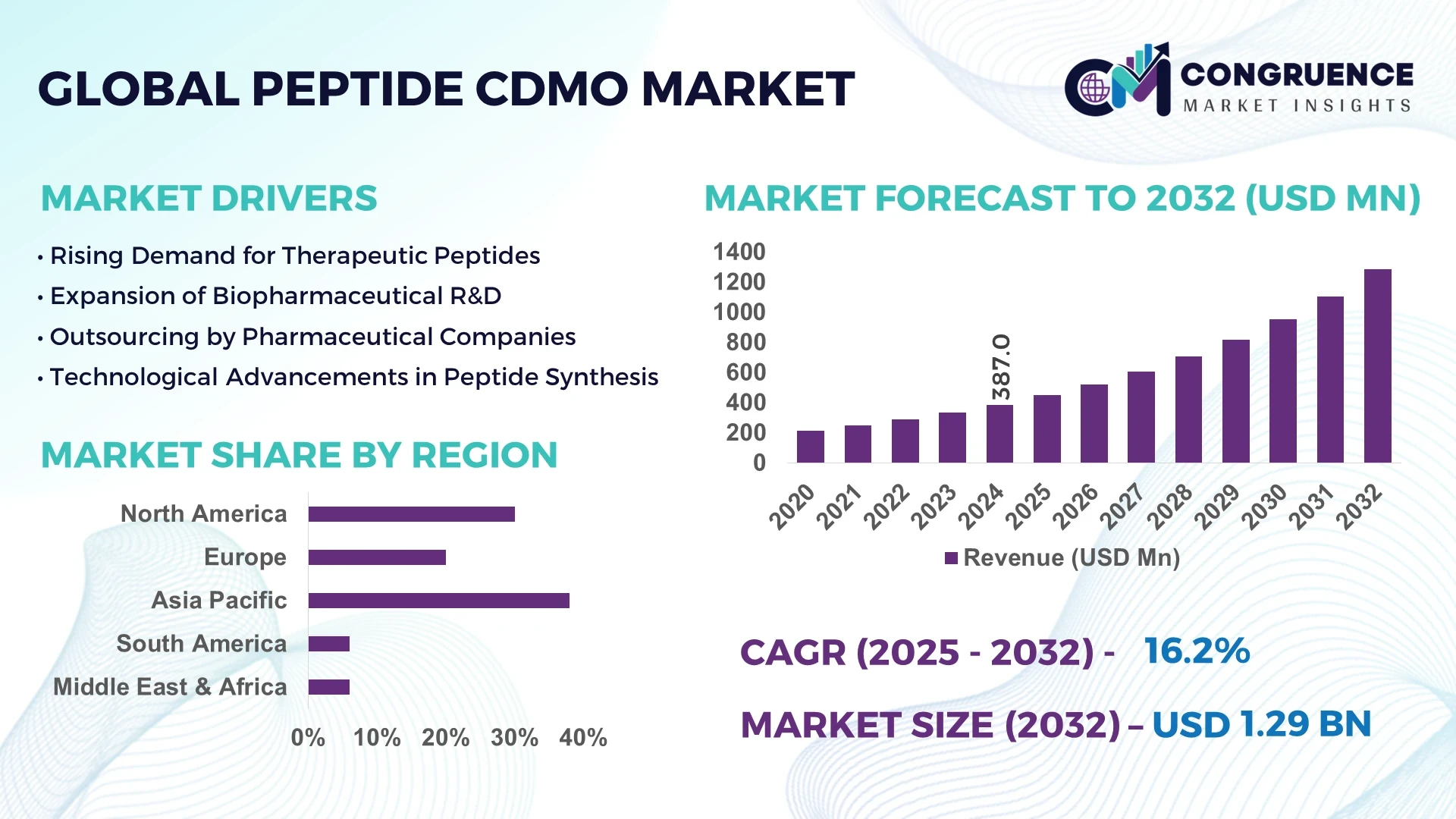

The Global Peptide CDMO Market was valued at USD 387.0 Million in 2024 and is anticipated to reach a value of USD 1,286.4 Million by 2032 expanding at a CAGR of 16.2% between 2025 and 2032.

India plays a leading role in this market, with key CDMO players such as Hyderabad-based Neuland Laboratories operating large-scale peptide API production facilities, hosting over 180 scientists and serving more than 500 global clients. These facilities are backed by substantial investment in analytical and manufacturing capacity, are highly compliant with international regulatory standards, and cater to applications across oncology, metabolic, and infectious disease peptide therapeutics.

The Peptide CDMO Market encompasses multiple industry sectors—primarily pharmaceutical therapeutics (e.g., oncology, metabolic disorders, infectious diseases), cosmetic peptides, and academic or research-oriented applications. Solid-phase and liquid-phase peptide synthesis technologies continue to evolve: innovations include high-throughput SPPS platforms, continuous-flow peptide synthesis, and automated purification systems that significantly shorten development timelines. Regulatory drivers—such as increasingly stringent GMP compliance and enhanced quality-by-design expectations—encourage CDMOs to invest in upgraded cleanroom environments, robust analytical validation, and green chemistry approaches that reduce waste. Economic motivations include outsourcing efficiencies, with regional patterns seeing strong demand in North America for advanced oncology peptides, while Asia-Pacific demonstrates accelerating growth fueled by manufacturing scalability and cost advantages. Emerging market trends include peptide–oligonucleotide conjugate CDMO services, which are gaining traction in precision medicine, and a shift toward integrated end-to-end CDMO capabilities spanning API, formulation, and analytical support—all aimed at accelerating time-to-clinic and reducing risk, which is especially appealing for biotech and mid-sized pharma decision-makers.

AI has begun to meaningfully influence the Peptide CDMO Market by enhancing efficiency, optimizing production workflows, and improving quality control in peptide synthesis operations. Machine learning algorithms are increasingly applied to real-time process analytical data—such as monitoring reaction kinetics during solid-phase peptide synthesis—to detect deviations early, enabling adaptive feedback that minimizes batch failures and reduces waste. Advanced AI models also support predictive maintenance of critical synthesis and purification equipment, reducing downtime and improving overall operational performance.

In peptide design and early development stages, deep learning frameworks—such as graph neural networks—accelerate target identification, enabling CDMOs to offer faster, more cost-effective lead generation services with improved predictability. AI-driven scheduling tools optimize facility utilization across multiple peptide projects, balancing resource allocation and demand to improve throughput, shorten turnaround times, and increase client satisfaction.

Moreover, AI-assisted analytical platforms streamline impurity profiling, using pattern recognition to flag potential contaminants in peptide batches—this enhances compliance and speeds up release cycles while maintaining high quality. With these innovations, the Peptide CDMO Market is becoming more agile and reliable, offering CDMO providers the ability to deliver faster, more scalable, and high-quality peptide synthesis services—critical for decision-makers pursuing speed-to-market and operational excellence.

"In 2024, a peptide CDMO pilot project implemented a machine learning model to predict optimal SPPS coupling times based on resin characteristics and reagent batch data, reducing average coupling failures by 35% and improving first-pass synthesis success rates by 22%."

The Peptide CDMO Market is rapidly shaped by evolving therapeutic demand, technological innovation, and outsourcing preferences. While pharmaceutical firms continue to expand peptide-based drug pipelines, CDMOs offer scalable, regulated manufacturing solutions essential for early to late-stage clinical programs. Technological advances—including automation, continuous-flow synthesis, and integrated analytics—are reducing cycle times and raising yield consistency. Simultaneously, a push for greener processes is prompting adoption of solvent-saving chemistries and waste-minimization strategies. Geographically, growth in Asia-Pacific, especially India and China, reflects cost-sensitive clients increasingly outsourcing to capable regional CDMOs. Meanwhile, regulatory expectations in developed markets drive investments in quality systems and infrastructure. Collectively, these trends compel CDMOs to differentiate via speed, compliance, technological leadership, and global footprint to meet evolving market demands.

The surge in peptide-targeted drug development—in oncology, metabolic disorders, and infectious diseases—is significantly boosting Peptide CDMO Market activity. Drug developers are increasingly outsourcing peptide synthesis to specialized CDMOs to leverage their capabilities in complex processes like SPPS and LPPS. This is translating into higher demand for custom peptide APIs and formulation services. CDMOs are investing in high-throughput automated synthesizers and purification platforms, with some reporting up to 40% faster turnaround times compared to conventional methods. This operational efficacy is a compelling value proposition for pharmaceutical clients focused on accelerating development timelines.

Despite growing demand, the Peptide CDMO Market faces constraints, particularly from high capital expenditures and infrastructure demands. Establishing SPPS-capable cleanroom facilities and acquiring regulatory certifications (e.g., GMP, FDA) requires substantial capital, which can exceed tens of millions of dollars. Smaller biotech firms may remain hesitant to enter the market or switch providers due to concerns over transition risks, quality consistency, and the inability to support large-scale runs, particularly when CDMOs face capacity constraints or scalability limitations. This dynamic can slow access to peptide CDMO services for emerging players.

The advent of peptide–oligonucleotide conjugate therapies presents a major opportunity for Peptide CDMO Market providers to expand service offerings. These conjugates require highly specialized synthesis protocols—peptide synthesis linked to oligonucleotide backbones—which few CDMOs currently offer. By investing in dual-capability platforms, CDMOs can capture this emerging segment, where demand is surging in precision medicine and targeted treatments. The ability to offer integrated conjugate synthesis positions CDMOs to become strategic partners in next-generation therapeutic development.

CDMOs in the peptide space face ongoing challenges in navigating complex, evolving regulations across jurisdictions. For example, new impurity control expectations demand advanced analytical methods like high-resolution mass spectrometry and peptide-specific impurity profiling, requiring CDMOs to continually invest in instrumentation and technical staff training. Additionally, aligning multi-country regulatory filings for global clients introduces complexity in managing batch documentation, validation protocols, and quality release criteria—particularly when different regions demand variant standards. The regulatory burden thus remains a significant operational challenge for Peptide CDMO Market providers.

Modular, scalable synthesis facilities: CDMOs are increasingly adopting modular, prefabricated cleanrooms and automated synthesis units. Prefabricated SPPS suites are built off-site and installed with precision, reducing construction and commissioning times. This modular approach—especially popular in North America and Europe—accelerates time-to-operation and enables rapid capacity scaling without compromising quality.

Real-time analytics and digital monitoring: Advanced process analytical technologies (PAT) such as in-line UV monitoring and near-infrared spectroscopy are being integrated into synthesis platforms. These enable real-time monitoring of reaction progress, with CDMOs reporting up to 30% reduction in batch reworks and improved consistency in peptide purity levels.

Sustainable chemistry protocols: To meet environmental and cost mandates, CDMOs now offer greener peptide synthesis—utilizing solvent recovery systems and minimizing toxic reagents. Some have achieved up to 40% reduction in hazardous waste generation per kilogram of peptide produced, strengthening their appeal to clients with ESG (Environmental, Social, Governance) commitments.

Flexible contract models and integrated services: CDMOs are expanding from standalone peptide synthesis to offering end-to-end solutions—spanning peptide design support, analytical testing, formulation, and even clinical batch production under a single contract. This “one-stop shop” model reduces coordination overhead and aligns with client demand for streamlined vendor management and faster development timelines.

The segmentation of the Peptide CDMO Market provides valuable insights into how this industry is structured and where opportunities are emerging. Segmentation can be broadly categorized into types, applications, and end-users, each reflecting distinct demand drivers and technological requirements. By type, the market encompasses solid-phase peptide synthesis (SPPS), liquid-phase peptide synthesis (LPPS), hybrid synthesis techniques, and custom peptide services. In terms of applications, the focus ranges from oncology and metabolic disorders to infectious diseases, vaccines, and cosmetic formulations. End-user categories include large pharmaceutical companies, biotechnology firms, academic and research institutes, and specialty healthcare providers. Each segment carries unique growth dynamics, shaped by evolving R&D pipelines, outsourcing strategies, and advancements in synthesis technologies. Understanding these distinctions helps decision-makers allocate resources effectively and anticipate competitive positioning within this rapidly expanding domain.

The Peptide CDMO Market by type is dominated by solid-phase peptide synthesis (SPPS), which remains the most widely used method due to its ability to produce complex, long-chain peptides with high purity. SPPS has become the industry standard, supported by automation and process innovations that allow CDMOs to scale production efficiently while maintaining quality control. The fastest-growing type is hybrid synthesis, which combines SPPS and liquid-phase peptide synthesis (LPPS). Hybrid techniques are gaining traction because they enable cost-effective production of long peptides while reducing the limitations inherent in each standalone process. LPPS, although less dominant than SPPS, continues to play an important role in producing simpler peptides and cyclic peptides that require solution-based chemistry. Custom peptide services, often project-specific, serve niche research, diagnostic, and therapeutic needs, contributing flexibility and value-added offerings for small- to mid-sized biotech clients. Collectively, these types create a diverse ecosystem that allows CDMOs to meet varied client demands across therapeutic and non-therapeutic applications.

Oncology applications currently lead the Peptide CDMO Market, driven by the growing demand for peptide-based cancer vaccines, targeted therapies, and immuno-oncology solutions. The need for highly specific, stable, and effective peptides in oncology has encouraged significant outsourcing to CDMOs with advanced synthesis and analytical capabilities. The fastest-growing application is in metabolic disorders, particularly diabetes management, where peptide-based drugs such as insulin analogs and GLP-1 receptor agonists are expanding their clinical and commercial use. Infectious disease applications also play a key role, with peptides increasingly incorporated into vaccine development and antiviral therapies. Cosmetic peptides, though smaller in scale compared to pharmaceuticals, contribute steadily to the market due to rising demand in skin care and anti-aging formulations. Other applications, including cardiovascular and neurological peptide therapeutics, add further diversity, reflecting the expanding potential of peptides in multiple therapeutic domains. This application landscape underscores the strategic role of CDMOs in enabling specialized, compliant, and scalable solutions across a wide range of health-related fields.

Large pharmaceutical companies represent the leading end-user segment in the Peptide CDMO Market, as their extensive pipelines and global reach require reliable, large-scale peptide manufacturing under stringent regulatory standards. These organizations often collaborate with CDMOs to ensure rapid scale-up from clinical to commercial production while maintaining compliance. The fastest-growing end-user group is biotechnology firms, which are increasingly outsourcing peptide synthesis due to limited in-house infrastructure and the need for specialized expertise. Biotechs are highly active in early-phase drug development, fueling demand for flexible and customized CDMO services. Academic and research institutions also contribute significantly by partnering with CDMOs for peptide supply in preclinical studies, experimental therapies, and diagnostic applications. Specialty healthcare providers, while representing a smaller share, rely on peptides for niche formulations, including advanced cosmetic and personalized medical applications. Together, these end-user groups shape a market characterized by collaboration, innovation, and growing reliance on outsourced expertise to accelerate peptide-focused development.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 18% between 2025 and 2032.

Asia-Pacific recorded the largest regional presence in the Peptide CDMO Market in 2024, driven by substantial manufacturing capacity and rising domestic demand. The region’s 38% share in 2024 reflects concentrated production hubs in China, India, and Japan, supported by active capacity expansions, workforce scaling, and investment in analytical and quality systems. North America held roughly 30% of the market in 2024, while Europe accounted for about 20%, with South America and Middle East & Africa sharing the remaining balance. Regional consumption patterns show North America focused on clinical-stage and high-value oncology peptides, whereas Asia-Pacific emphasizes large-volume commercial manufacturing and cost-efficient scale-up. Across regions, investment in automation, cleanroom expansions, and end-to-end CDMO offerings is reshaping competitive dynamics and enabling faster client onboarding and global supply reliability.

North America accounted for approximately 30% of the Peptide CDMO Market in 2024, remaining a leading destination for clinical development and high-complexity peptide projects. Key industries driving demand include large pharmaceutical companies, specialized biotech firms in oncology and immunology, and contract research organizations supporting early-stage development. Regulatory oversight and quality expectations—anchored by frequent interactions with authorities and rigorous GMP frameworks—have encouraged CDMOs to invest in advanced analytical systems, in-line process control, and digital batch documentation. Technological advancements in the region include adoption of continuous synthesis modules, high-throughput purification platforms, and AI-enabled process analytics that improve throughput and reduce batch variability. Government and institutional support for biotech innovation, coupled with strong clinical trial activity, sustains demand for integrated CDMO services across the United States and Canada.

Europe represented around 20% of the Peptide CDMO Market in 2024 and remains distinguished by strong regulatory oversight, robust quality culture, and a focus on sustainability in manufacturing. Key European markets such as Germany, the United Kingdom, and France are notable for their advanced biopharma ecosystems and skilled talent pools. Regulatory bodies across Europe emphasize rigorous impurity control and environmental compliance, prompting CDMOs to adopt solvent recovery systems, green chemistry protocols, and lifecycle management practices. Adoption of emerging technologies—such as PAT integration, automated formulation lines, and digital quality management systems—is increasing, particularly among mid-sized CDMOs aiming to serve European biotech clients. Sustainability initiatives and circular manufacturing practices are influencing capital planning and facility upgrades, reinforcing Europe’s reputation for quality-driven, environmentally conscious peptide manufacturing.

Asia-Pacific led regional volumes in the Peptide CDMO Market in 2024 and remains the largest market by production volume and capacity, supported by top consuming and producing countries including China, India, and Japan. Infrastructure trends show rapid expansion of GMP-compliant peptide production suites, modular cleanroom installations, and investment in downstream purification capacity. Manufacturing trends emphasize cost efficiency, scale-up expertise, and the ability to handle high-volume commercial runs for peptide APIs and intermediates. Regional tech trends include the emergence of innovation hubs in Bangalore, Hyderabad, Shanghai, and Suzhou that combine process development centers with pilot-scale manufacturing. Collaborative partnerships between local CDMOs and global biotech sponsors are increasing, as are investments in automation and high-throughput synthesis to meet both domestic and export demand.

South America accounted for approximately 6% of the Peptide CDMO Market in 2024, with Brazil and Argentina representing the most active national markets for peptide contract manufacturing and clinical supplies. The region is characterized by growing interest in local production capacities to reduce import dependencies and support regional clinical trials. Infrastructure development is uneven but improving, with investments in GMP facility upgrades and cold-chain logistics to support biologics and peptide handling. Energy and utility considerations influence site selection and operating costs, while several governments are introducing incentives and trade policies aimed at fostering pharmaceutical manufacturing and export orientation. As regional CDMOs expand capabilities, South America is becoming an increasingly relevant node for regional supply and early-stage clinical production.

Middle East & Africa held roughly 6% of the Peptide CDMO Market in 2024 and is showing nascent but accelerating demand driven by healthcare modernization and strategic investments in biotech infrastructure. Major growth countries include the United Arab Emirates and South Africa, where public-private partnerships and specialized medical clusters are supporting talent development and laboratory modernization. Technological modernization trends include establishment of quality control laboratories, adoption of digital record keeping, and selective automation to support local clinical manufacturing. Local regulations and trade partnerships are evolving to facilitate import of raw materials and export of finished products, while government initiatives seek to attract investment in life sciences manufacturing as part of broader economic diversification strategies.

India — 24% Market Share

India leads the Peptide CDMO Market with a 24% share, supported by extensive manufacturing capacity, a skilled peptide-focused workforce, and sustained capital investment in API and analytical facilities.

United States — 22% Market Share

United States holds a 22% share, driven by high demand from large pharmaceutical companies, advanced clinical development programs, and continual investment in process development and regulatory compliance.

The Peptide CDMO Market is characterized by a highly competitive and fragmented landscape, with over 60 active global competitors offering a range of specialized services. Leading players differentiate themselves through strategic investments in high-throughput peptide synthesis, automated purification systems, and advanced analytical platforms to ensure consistent quality and scalability. Several CDMOs have formed strategic partnerships with pharmaceutical and biotechnology companies to expand service portfolios and strengthen geographic presence. Mergers and acquisitions are also prevalent, enabling companies to integrate complementary capabilities, broaden product offerings, and accelerate time-to-clinic for clients. Innovation trends such as continuous-flow peptide synthesis, AI-assisted process optimization, and peptide–oligonucleotide conjugate production are driving differentiation, with firms investing heavily in process development and digital transformation. Market positioning varies from full-service end-to-end CDMOs to niche players specializing in specific therapeutic areas or peptide types. Operational efficiency, compliance with international regulatory standards, and technological leadership are key competitive factors shaping the strategic landscape and influencing client selection.

Lonza Group

WuXi AppTec

Polypeptide Group

Bachem AG

Jubilant Biosys

AmbioPharm Inc.

PeptiDream Inc.

Neuland Laboratories

CordenPharma

Bio-Synthesis Inc.

The Peptide CDMO Market is being transformed by both established and emerging technologies. Solid-phase peptide synthesis (SPPS) remains the dominant technology due to its ability to produce long-chain, high-purity peptides. Continuous-flow peptide synthesis is gaining adoption, enabling faster reaction cycles, reduced reagent consumption, and enhanced process control. Hybrid synthesis approaches combining SPPS and liquid-phase peptide synthesis (LPPS) are increasingly used for complex peptides, optimizing cost and efficiency. Automated purification technologies, including preparative HPLC and multi-column systems, are improving yield consistency and reducing manual labor. Analytical advancements, such as high-resolution mass spectrometry and in-line UV monitoring, enhance impurity profiling and real-time reaction monitoring. Digital transformation is another significant trend, with AI-driven process analytics and predictive maintenance tools optimizing throughput, minimizing batch failures, and improving operational efficiency. Peptide–oligonucleotide conjugate synthesis is an emerging technological focus, with CDMOs developing specialized platforms to meet the requirements of precision medicine. These technological developments collectively enhance scalability, reproducibility, and compliance in the Peptide CDMO Market.

In March 2023, Bachem AG inaugurated a new automated peptide synthesis facility in Switzerland, equipped with high-throughput SPPS modules and digital monitoring systems to accelerate complex peptide production.

In September 2023, Lonza Group partnered with a leading US biotechnology company to provide integrated peptide development and manufacturing services for oncology-focused therapeutics, enhancing capacity for clinical-stage peptides.

In February 2024, WuXi AppTec expanded its peptide purification capabilities with multi-column preparative HPLC systems at its China facility, enabling simultaneous processing of up to 12 peptide batches.

In May 2024, Neuland Laboratories launched a dedicated peptide–oligonucleotide conjugate synthesis unit in Hyderabad, India, integrating advanced analytical and automation technologies to support next-generation precision medicine projects.

The Peptide CDMO Market Report provides a comprehensive overview of the global peptide contract development and manufacturing landscape, covering production, technology, applications, and end-user sectors. The report analyzes key market segments, including SPPS, LPPS, hybrid synthesis, and custom peptide services, detailing their operational relevance and contribution to pharmaceutical, cosmetic, and research applications. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional production hubs, infrastructure trends, regulatory frameworks, and technological innovations. End-user analysis focuses on large pharmaceutical companies, biotechnology firms, academic and research institutions, and specialty healthcare providers. The report also examines technological drivers such as continuous-flow synthesis, automated purification, AI-enabled analytics, and peptide–oligonucleotide conjugate platforms. Additionally, strategic market insights include competitive positioning, partnerships, mergers, and R&D initiatives. Emerging trends and niche segments, such as precision medicine and cosmetic peptides, are explored to guide investment, operational planning, and strategic decision-making for industry professionals, executives, and stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 387.0 Million |

| Market Revenue (2032) | USD 1,286.4 Million |

| CAGR (2025–2032) | 16.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Lonza Group, WuXi AppTec, Polypeptide Group, Bachem AG, Jubilant Biosys, AmbioPharm Inc., PeptiDream Inc., Neuland Laboratories, CordenPharma, Bio-Synthesis Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |