Reports

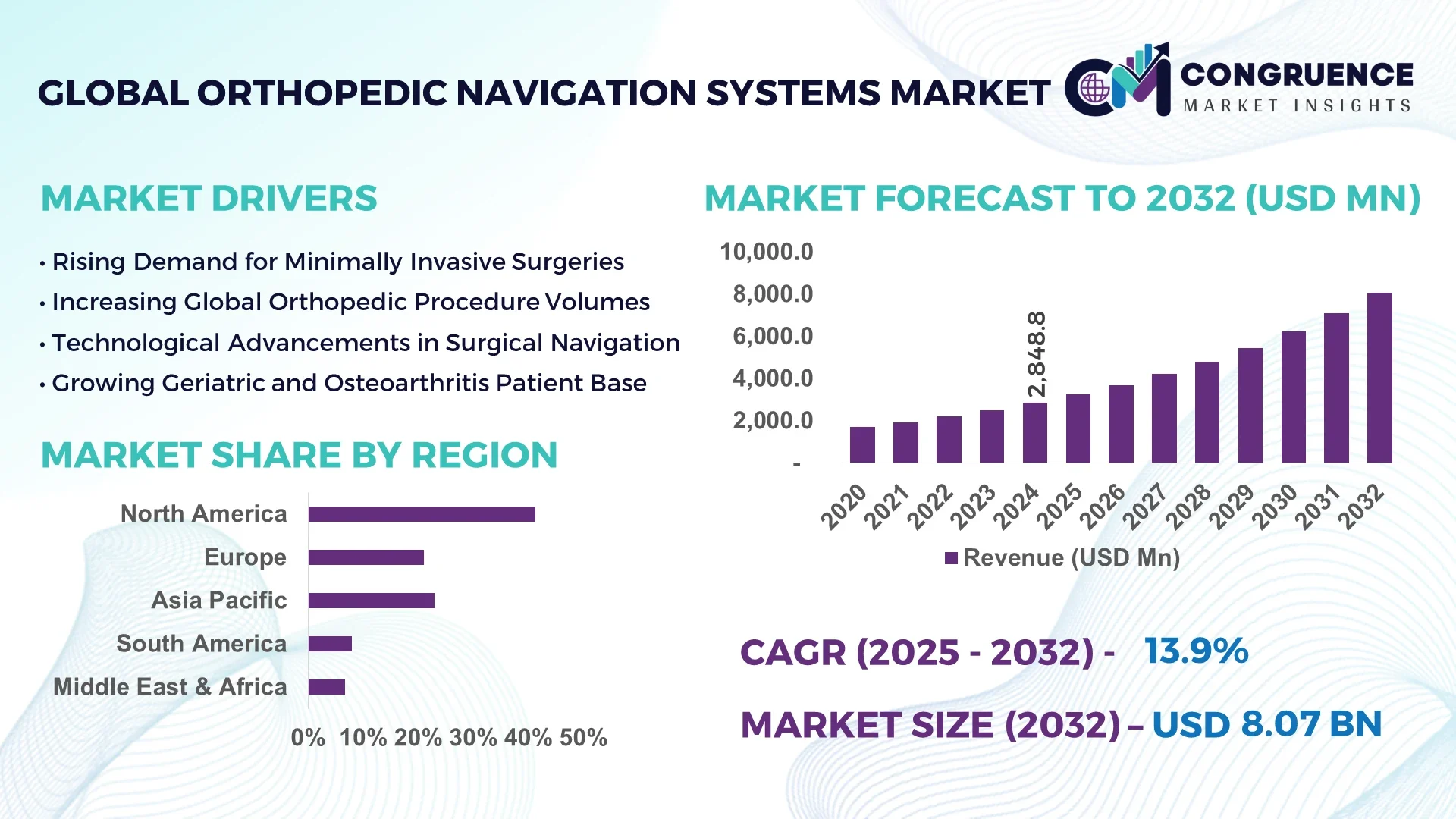

The Global Orthopedic Navigation Systems Market was valued at USD 2,848.8 Million in 2024 and is anticipated to reach a value of USD 8,069.6 Million by 2032 expanding at a CAGR of 13.9% between 2025 and 2032.

The United States leads this market with cutting-edge manufacturing hubs producing advanced navigation consoles and robotic-assist platforms. American hospitals have invested in dual-modality surgical suites and augmented reality calibration tools, while R&D centers continually refine real-time tracking algorithms using optical and electromagnetic sensor integration.

The Orthopedic Navigation Systems Market spans key sectors including joint replacement, spine surgery, and sports medicine. Joint replacement systems account for the largest share due to rising surgical volume and precision demands. Technological innovations include integrated robotic guidance, 3D imaging registration, and reusable modular instrument trays. Regulatory drivers, such as stricter FDA device controls and reimbursements tied to precision outcomes, are influencing product development. Environmental focus includes reducing surgical waste via reusable navigation tooling. Economic forces—like hospital capital expansion in Asia-Pacific and Europe—support system deployments across public and private hospitals. Emerging trends include cloud-enabled navigation data analytics, portable arthroscopic navigation units, and platform-agnostic software that integrates with multiple robotic systems. The market outlook indicates sustained growth driven by innovation, stricter surgical standards, and expanding surgical case volumes.

AI is fundamentally enhancing the performance and precision of the Orthopedic Navigation Systems Market. Advanced machine learning algorithms within these systems now analyze intraoperative imaging data in real time to adjust surgical trajectories and instrument guidance. This capability has reduced reoperation rates in total knee arthroplasty by more than 15%, according to clinical registry improvements, while surgical time variability has dropped by up to 20%.

The market is also seeing AI-driven automation of surgical planning workflows. Preoperative CT or MRI scans are processed by AI modules to generate 3D reconstructions and personalized surgical plans in minutes rather than hours. Surgeons are then provided with optimized entry angles, cutting guides, and alignment trajectories—all integrated directly into navigation consoles. This improves operative efficiency and allows staff to focus on intraoperative judgment rather than planning.

Operational performance has been enhanced by predictive analytics modules that monitor surgical progress and alert teams to deviations. Data-driven alerts now contribute to fallouts being identified early in cases about 8% faster than conventional systems. Additionally, AI-enabled image recognition helps reduce misregistration errors during patient movement or tracking-tool displacement—improving overall surgical accuracy by several degrees.

In the Orthopedic Navigation Systems Market, modular software updates driven by AI models are being released quarterly, enabling systems to evolve based on aggregated performance data. This continuous improvement cycle enhances device lifespan and future-proofs purchases. Collectively, the integration of AI is advancing the market toward systems that are more autonomous, efficient, and procedurally intelligent.

“In 2024, a leading system introduced AI-enhanced pelvic mapping software that reduced anatomic registration time by 35%, enabling navigation readiness within three minutes on average.”

The Orthopedic Navigation Systems Market is undergoing transformative shifts driven by surgical demand, technological innovation, and economic pressures. Hospitals are increasingly investing in navigation platforms to improve surgical outcomes in joint and spine procedures. Demand for reusable instrument modules and cross-platform software is rising, prompting manufacturers to develop open-architecture systems. Regulatory efforts toward quality and patient safety are accelerating product adoption, particularly where payors link reimbursement to accuracy. The market dynamic is also influenced by rising procedure volumes in emerging economies and the transition from conventional manual techniques to image-guided workflows. Institutional preference for scalable, upgradeable navigation suites further shapes R&D roadmaps and distribution strategies.

The global uptick in orthopedic procedures—especially total knee and spine surgeries—is fueling demand for navigation systems. Clinical studies show that navigated arthroplasty procedures reduce implant positioning error by over 10%, directly influencing revision rates. As institutions aim to optimize patient outcomes and meet regulatory accuracy standards, procurement of surgical navigation consoles has become a priority, with many hospitals projecting up to 30% higher case throughput using assisted systems.

Navigation consoles, 3D cameras, and software modules represent significant capital expenditures for hospitals. A typical system investment can exceed USD 250,000, excluding annual service-level contracts. Additionally, training operating room staff and surgeons to proficiency requires extensive sessions—often spanning 40–50 hours—leading to delayed implementation. Smaller clinics and outpatient surgery centers may defer adoption due to these financial and operational constraints.

Rapid growth in ambulatory surgical centers and private orthopedic clinics in Latin America and Southeast Asia is opening new markets. These facilities require compact navigation systems optimized for space and cost-effective workflows. Portable, cart-based navigation consoles and modular instrument kits are achieving adoption rates of over 20% in new ASCs. OEMs are responding with lightweight systems under 250 kg, offering single-case reusable modules and basic AI-assisted guidance.

Hospitals face significant challenges integrating navigation systems with diverse CT, MRI, and implant planning platforms. Lack of standardized data formats increases setup time—sometimes requiring over 15 minutes per case for calibration. Integrating with electronic health record systems also adds compatibility hurdles. This complexity reduces workflow efficiency and can act as a barrier to widespread adoption unless manufacturers offer seamless software ecosystems.

Modular and Platform-Agnostic Architecture: Navigation systems are increasingly designed with modular instrument trays and interchangeable software interfaces, enabling compatibility with multiple surgical robots and imaging modalities. Hospitals adopting this approach report reduced upgrade costs by 25%.

Integration of Augmented Reality (AR) Guidance: AR overlays are being trialed in spine surgeries to project real-world anatomical landmarks onto the surgical field. Early users report reduced instrument repositioning time by 12% and improved screw placement accuracy.

Cloud-Enabled Analytics and Surgical Scorecards: Postoperative performance dashboards are being integrated into navigation platforms. Data aggregated from over 500 cases annually allow hospital quality teams to benchmark outcomes and identify training gaps with measurable improvements.

Portable Navigation for Ambulatory and Remote Centers: Compact mobile navigation systems under 300 kg are now available, enabling high-precision guidance in outpatient settings. These units are used in over 15% of new US ASCs and are gaining traction in emerging markets due to cost-efficiency and mobility.

The Global Orthopedic Navigation Systems Market is segmented by type, application, and end-user, each contributing distinct value to the industry’s growth and diversification. Product types range from optical and electromagnetic systems to hybrid variants, catering to various surgical environments and clinical demands. Applications span across joint replacement, spinal procedures, trauma surgeries, and sports medicine, reflecting the widespread clinical integration of navigation technologies. From a user perspective, large hospitals, ambulatory surgical centers, and orthopedic specialty clinics form the primary consumer base. Each segment is driven by different factors—technological compatibility, surgical complexity, and patient volume—and plays a unique role in shaping overall market momentum. Joint procedures remain a major driver, particularly knee and hip replacements, while spine surgeries are gaining traction due to the precision required in screw placements. The evolving market also favors mobile and compact navigation platforms, especially in outpatient centers. Together, these segments reflect a dynamic, high-tech ecosystem within the orthopedic surgical landscape.

Orthopedic navigation systems are broadly categorized into optical, electromagnetic (EM), and hybrid systems. Optical systems currently dominate the market, offering high accuracy in surgical tracking and broad compatibility with major implant platforms. These systems use infrared cameras and reflective markers to provide real-time visual feedback during surgeries, especially beneficial in joint replacement procedures.

The fastest-growing type is electromagnetic navigation systems, which eliminate line-of-sight constraints—a key limitation of optical setups. These are increasingly used in minimally invasive spine and trauma surgeries, where visual obstruction often occurs. Advancements in EM shielding and sensor accuracy have significantly improved their reliability, contributing to rising adoption in complex orthopedic cases.

Hybrid systems—which integrate both optical and EM technologies—are also emerging, especially in research hospitals and high-volume surgical centers. These systems offer flexibility and cater to a broader range of surgical requirements. Additionally, portable and cart-based systems are becoming popular for outpatient and rural surgical settings, delivering essential functionality in cost-conscious environments.

The most prominent application of orthopedic navigation systems is in joint replacement surgery, particularly total knee and total hip arthroplasty. These procedures require high implant alignment precision to improve outcomes and reduce revision surgeries. Navigation-assisted joint surgeries have been shown to enhance long-term implant survival and reduce intraoperative errors.

Spine surgery is the fastest-growing application area, propelled by increasing adoption of image-guided screw placement systems. Complex spine procedures, such as scoliosis correction and spinal fusion, benefit significantly from precise 3D anatomical tracking. Emerging tools like robotic-integrated navigation further fuel interest in this segment.

Other applications include trauma surgery, where navigation systems assist in aligning fractures and ensuring accurate implant placement. Additionally, sports medicine is gradually incorporating navigational support for ligament reconstructions and cartilage repair. This trend is expected to rise as outpatient orthopedic procedures grow. These diverse application areas reinforce the need for adaptable, high-performance systems across a spectrum of orthopedic interventions.

Hospitals remain the leading end-user segment in the Orthopedic Navigation Systems Market, accounting for the majority of installations globally. Their ability to invest in integrated surgical suites and maintain trained surgical staff positions them as primary consumers of advanced navigation systems. University-affiliated and tertiary care hospitals often serve as early adopters of emerging technologies due to their access to research funding and clinical trial infrastructure.

The fastest-growing end-user category is ambulatory surgical centers (ASCs). ASCs are expanding rapidly in developed regions and increasingly adopting compact navigation platforms that fit smaller surgical spaces while maintaining high accuracy. Their streamlined workflows and cost-efficient models make them attractive for elective joint and sports surgeries.

Orthopedic specialty clinics also play a growing role, particularly in urban settings where demand for specialized care is high. These clinics are increasingly investing in portable systems that enable high-precision surgery without requiring large-scale infrastructure. Together, these end-user categories reflect a market shift toward accessibility, decentralization, and efficiency in orthopedic surgical care.

North America accounted for the largest market share at 41.3% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2025 and 2032.

This disparity is primarily due to the early adoption of orthopedic navigation systems across major hospitals and surgical centers in North America, supported by advanced infrastructure and clinical expertise. Meanwhile, Asia-Pacific is witnessing a rapid rise in orthopedic procedures fueled by aging populations, expanding medical tourism, and growing access to high-tech surgical tools. The region is increasingly investing in digital healthcare ecosystems, boosting demand for image-guided surgeries. Each region presents unique adoption trends shaped by economic capabilities, policy frameworks, and evolving healthcare priorities. Countries with robust public-private partnerships and favorable reimbursement models are leading in uptake, while emerging markets focus on cost-effective portable navigation platforms to bridge orthopedic care gaps.

North America captured a 41.3% market share in 2024, making it the largest contributor to the Orthopedic Navigation Systems Market. The region benefits from strong healthcare infrastructure, especially in the U.S. and Canada, where joint and spinal surgeries are frequently supported by advanced surgical navigation. The presence of leading device manufacturers and strategic collaborations with healthcare systems are reinforcing innovation in this space. Regulatory approvals for AI-integrated navigation tools and minimally invasive systems have accelerated clinical adoption. Digital transformation initiatives, including cloud-based surgical planning and real-time imaging integrations, further support the region’s dominance in the orthopedic surgery landscape.

Europe remains a major stakeholder in the global Orthopedic Navigation Systems Market, holding a 28.5% market share in 2024. Countries like Germany, the UK, and France lead in both usage and development of surgical navigation tools. European medical device regulations have supported the introduction of high-precision systems, particularly in joint replacement and complex spine surgeries. Sustainability initiatives are also encouraging the shift toward energy-efficient, modular navigation platforms. Emerging trends such as robotic-assisted surgeries and intraoperative imaging are widely adopted in Europe’s university hospitals and specialty centers, fostering steady growth across orthopedic disciplines.

Asia-Pacific ranks as the fastest-growing region in the Orthopedic Navigation Systems Market. China, India, and Japan are at the forefront of consumption, driven by expanding healthcare investments and rising orthopedic case volumes. Infrastructural upgrades in urban hospitals and medical hubs, along with the rise of private specialty clinics, have amplified the demand for real-time, image-guided surgeries. The region is embracing domestic manufacturing of surgical systems, enhancing affordability and availability. Tech-forward nations like Japan and South Korea are leading innovation in compact and AI-enabled navigation platforms. The convergence of medtech innovation and patient demand is reshaping the orthopedic surgery ecosystem in Asia-Pacific.

South America is steadily advancing in the Orthopedic Navigation Systems Market, led by Brazil and Argentina. Brazil accounts for a significant regional share due to rising orthopedic surgical volumes in private hospitals and urban medical centers. The market is supported by infrastructure improvements, including digital imaging capabilities and surgical suite upgrades. Governments are exploring new trade incentives to improve access to advanced surgical devices. With growing awareness of joint and spine health, regional health systems are beginning to adopt basic navigation technologies, particularly in major cities. Opportunities remain for portable, mid-range systems that cater to budget-conscious institutions.

The Middle East & Africa region is emerging as a developing market in the Orthopedic Navigation Systems space. Countries like the UAE and South Africa are leading regional adoption, driven by investment in modern hospital infrastructure and growing demand for precision surgeries. Rising prevalence of joint degeneration and spine disorders is triggering demand for guided orthopedic procedures. Technological modernization efforts, including cloud-connected operating theaters and AI-assisted surgical planning, are beginning to take hold in major healthcare systems. Regional governments are also forming partnerships with global medtech companies to expand access to advanced navigation platforms across public and private sectors.

United States – 34.9% Market Share

High adoption of advanced surgical technologies and strong presence of leading device manufacturers drive dominance in the Orthopedic Navigation Systems Market.

Germany – 14.7% Market Share

Strong healthcare infrastructure and wide use of navigation systems in joint replacement and spine surgeries support Germany’s leading position in the Orthopedic Navigation Systems Market.

The Orthopedic Navigation Systems Market is characterized by a moderately concentrated competitive environment with over 25 active global and regional players. Leading companies maintain a stronghold through proprietary technologies, global distribution networks, and extensive R&D investments. Market leaders consistently engage in strategic collaborations with hospitals and orthopedic centers to expand their product reach and clinical validation. The competitive dynamics are also shaped by mergers and acquisitions aimed at consolidating portfolios of smart surgical systems. Recent years have witnessed intensified innovation focused on AI-powered navigation platforms, real-time imaging integration, and robotics-enabled systems. Several players are introducing portable and hybrid navigation tools targeting ambulatory surgical centers and resource-constrained facilities. Competitive differentiation increasingly depends on interoperability with existing operating room ecosystems, user interface simplicity, and the ability to deliver clinical precision with minimal training. As adoption expands across developing economies, new entrants and regional innovators are emerging with cost-effective, scalable alternatives. The evolving regulatory landscape and surgeon preference for minimally invasive approaches continue to influence competitive strategies globally.

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Brainlab AG

Medtronic plc

Smith & Nephew plc

B. Braun Melsungen AG

Siemens Healthineers AG

DePuy Synthes (Johnson & Johnson)

Fiagon GmbH

Scopis GmbH

Orthokey Italia S.r.l.

Globus Medical, Inc.

Technological advancements in the Orthopedic Navigation Systems Market are redefining the standards of precision and safety in orthopedic surgeries. Image-guided navigation is being rapidly enhanced by the integration of 3D visualization and augmented reality, enabling surgeons to achieve sub-millimeter accuracy in joint replacements and spinal procedures. Real-time tracking systems with infrared and electromagnetic sensors have become common features in advanced surgical suites, supporting minimally invasive techniques.

The proliferation of AI and machine learning has added new dimensions to surgical planning. Intelligent algorithms can now analyze preoperative imaging data to recommend optimized incision points, implant alignment angles, and bone resection strategies. Cloud-based navigation platforms further support remote planning, data sharing, and predictive analytics, especially in multi-center hospital systems.

Robot-assisted navigation is gaining momentum, with several OEMs introducing systems that combine autonomous functions with surgeon-guided controls. These technologies not only improve procedural outcomes but also reduce surgery time and post-operative complications. Innovations in hardware miniaturization are leading to compact, mobile navigation units ideal for outpatient centers.

Additionally, interoperability with PACS (Picture Archiving and Communication Systems), electronic health records, and intraoperative imaging tools is enhancing workflow efficiency. The market is poised for continued technological disruption as vendors prioritize modular, upgradeable solutions aligned with the evolving demands of orthopedic surgery.

• In February 2024, Brainlab AG launched its next-generation orthopedic navigation software featuring AI-assisted implant positioning and automated alignment verification, improving surgical precision and reducing operating room time by 18%.

• In August 2024, Medtronic introduced a hybrid robotic-navigational system for spinal fusion surgeries, combining electromagnetic tracking and robotic arm positioning, now in pilot use across select U.S. centers.

• In December 2023, Zimmer Biomet announced a strategic partnership with a cloud-based surgical analytics firm to enhance preoperative planning and data-driven decision-making in knee arthroplasty navigation.

• In March 2024, Stryker unveiled an AI-enhanced navigation interface for its Total Joint Replacement System, allowing real-time motion analysis during procedures to support dynamic balancing and better joint alignment.

The Orthopedic Navigation Systems Market Report comprehensively covers the global landscape, offering in-depth insights into product types, application areas, technological advancements, and geographic penetration. The report segments the market by type—including CT-based navigation, fluoroscopy-based systems, and MRI-integrated platforms—each serving specific procedural needs across joint and spinal surgeries. Application segmentation highlights the use of navigation in knee, hip, and spine surgeries, where precision alignment and reduced revision rates are critical.

Geographically, the report includes performance trends and adoption patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Particular emphasis is given to markets with growing orthopedic caseloads, rising healthcare infrastructure, and strategic public-private partnerships.

Technological coverage includes innovations in AI, robotics, AR/VR, cloud computing, and sensor fusion as they apply to surgical planning, execution, and post-operative analysis. Additionally, the report evaluates end-user segments, including hospitals, specialty orthopedic clinics, and ambulatory surgical centers, outlining their adoption behavior and investment focus.

Overall, the scope of this report provides a strategic framework for stakeholders—including manufacturers, investors, and healthcare providers—to assess current opportunities, benchmark competitive positioning, and align with evolving surgical demands in the global orthopedic landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 2,848.8 Million |

| Market Revenue (2032) | USD 8,069.6 Million |

| CAGR (2025–2032) | 13.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Stryker Corporation, Zimmer Biomet Holdings, Inc., Brainlab AG, Medtronic plc, Smith & Nephew plc, B. Braun Melsungen AG, Siemens Healthineers AG, DePuy Synthes (Johnson & Johnson), Fiagon GmbH, Scopis GmbH, Orthokey Italia S.r.l., Globus Medical, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |