Reports

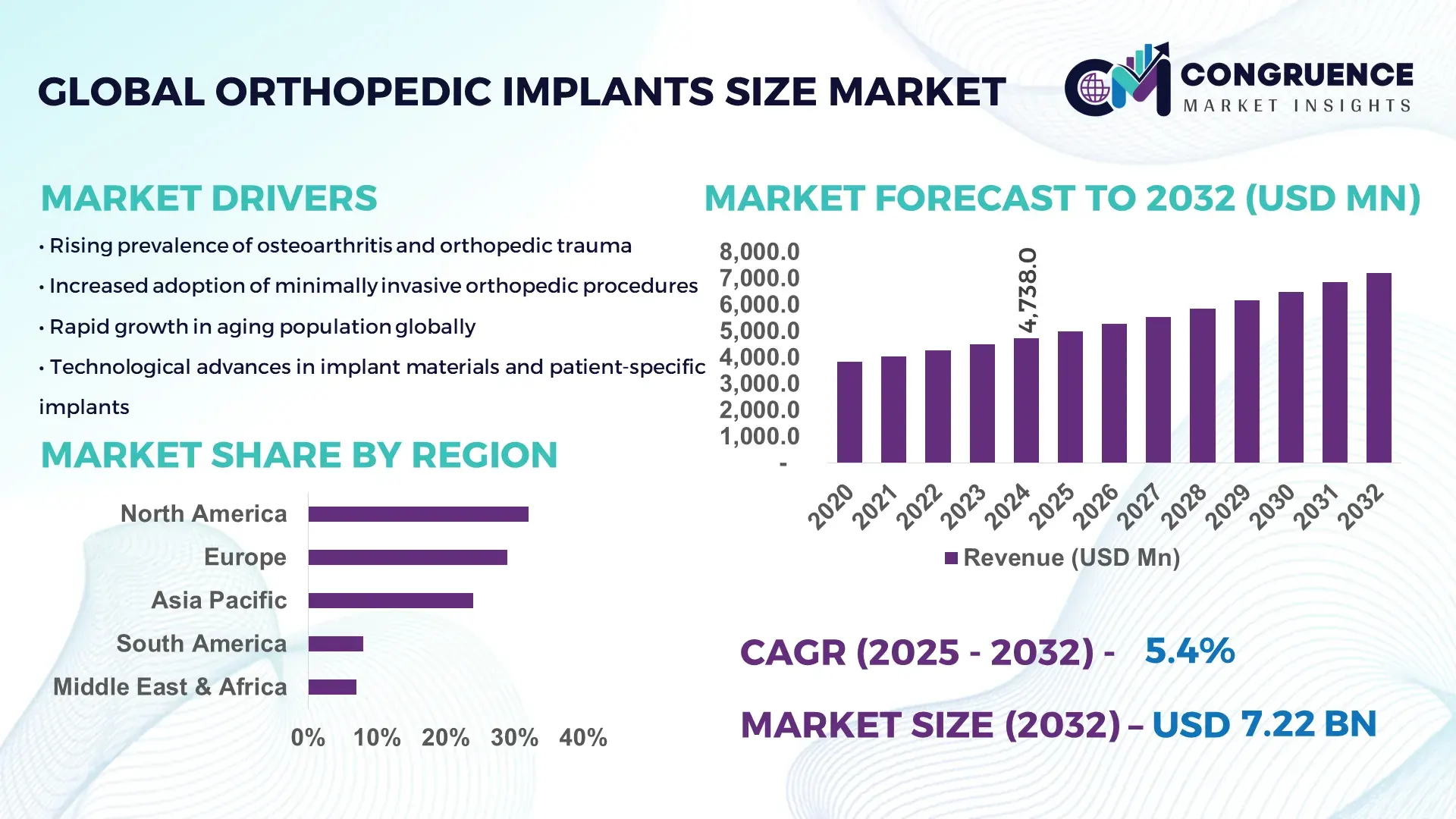

The Global Orthopedic Implants Size Market was valued at USD 4,738.0 Million in 2024 and is anticipated to reach a value of USD 7,216.4 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032, according to an analysis by Congruence Market Insights. This trajectory is primarily driven by increasing demand for standardized implant sizing and the adoption of computer-assisted surgical planning that reduces inventory complexity.

The United States leads the global landscape in orthopedic implant sizing capabilities. U.S. production capacity exceeds 1.2 million implant units annually across major OEMs, with capital expenditures in precision implant manufacturing surpassing USD 480 million in the most recent reporting year. Clinical adoption is high: approximately 68% of tertiary hospitals report routine use of size-specific modular implants and digital templating. Investment activity includes over 120 dedicated R&D projects in additive manufacturing and surface-engineering in the last 24 months, and national regulatory approvals for novel sizing systems rose by 14% year-over-year.

Market Size & Growth: USD 4,738.0 Million (2024) to USD 7,216.4 Million (2032), CAGR 5.4%; driven by standardization and digital surgical planning.

Top Growth Drivers: 68% clinical templating adoption, 45% reduction in inventory variance, 32% increase in modular implant demand.

Short-Term Forecast: By 2028, expect a 22% reduction in intraoperative sizing time and a 15% decrease in implant SKU carry.

Emerging Technologies: Additive manufacturing for custom sizes, AI-driven templating, and robotic-assisted sizing guides.

Regional Leaders: North America ~USD 2,100M by 2032 (digital templating uptake); Europe ~USD 1,800M by 2032 (precision machined implants); Asia Pacific ~USD 1,500M by 2032 (scaling production capacity).

Consumer/End-User Trends: Hospitals favor modular kits; ambulatory surgical centers adopt smaller SKU footprints and same-day implantation.

Pilot or Case Example: 2024 hospital pilot reduced implant inventory downtime by 34% and intraoperative sizing changes by 42%.

Competitive Landscape: Market leader ~18% share; major competitors include five multinational OEMs and three specialized regional manufacturers.

Regulatory & ESG Impact: Increasing device traceability rules and recycling targets drive leaner sizing inventories and sustainable packaging.

Investment & Funding Patterns: Recent sector funding exceeded USD 650M, with growth-stage VC and project finance focusing on manufacturing scale-up.

Innovation & Future Outlook: Trend toward patient-matched sizing, integrated templating-to-manufacturing workflows, and reduced SKU proliferation.

The Orthopedic Implants Size Market spans joint replacement, trauma fixation, and spinal implants, with modular systems and patient-matched devices expanding rapidly. Recent advances in additive manufacturing and AI templating are shortening lead times, while regulatory traceability and hospital procurement policies favor standard-size modularity and reduced SKU inventories.

The Orthopedic Implants Size Market is strategically crucial because it aligns manufacturing efficiency with clinical precision, reducing wasted inventory and improving surgical outcomes. Strategic pathways center on integrating digital templating, additive manufacturing, and supply-chain consolidation to deliver measurable gains. For example, AI-assisted templating delivers a 27% improvement in preoperative sizing accuracy compared to traditional manual templating. Regionally, North America dominates in production volume, while Europe leads in adoption with 62% of orthopedic enterprises implementing templating and modular kits. By 2027, robotic-assisted templating is expected to improve implant fit accuracy by 18% and reduce reoperation rates by an estimated 6%, reflecting short-term performance gains.

Firms are committing to ESG metrics that include a 30% reduction in single-use surgical packaging and a 20% increase in implant recycling programs by 2030. In a recent micro-scenario, a major U.S. hospital system achieved a 34% reduction in intraoperative size exchanges in 2024 by deploying an AI-driven sizing workflow integrated with just-in-time inventory — this reduced operating room downtime by 11%. Strategic investments are shifting from SKU proliferation toward configurable modular platforms and on-demand manufacturing. The future outlook positions the Orthopedic Implants Size Market as a pillar of clinical resilience: converging standards, digital planning, and sustainable manufacturing will drive efficiency, regulatory compliance, and improved patient outcomes, making the market a durable area for capital allocation and innovation.

The Orthopedic Implants Size Market dynamics reflect a maturing ecosystem in which digital planning tools, modular implant architectures, and manufacturing flexibility interact. Demand-side forces include aging populations and elective surgery resumption, while supply-side trends emphasize lean inventories, SKU rationalization, and decentralised manufacturing (including additive manufacturing facilities). Procurement practice changes—such as centralized hospital group purchasing and preference for configurable kits—are reducing SKU counts by up to an estimated 25% in some systems. Technological drivers include AI templating, which shortens planning time and increases first-fit rates, and 3D printing, which enables low-volume production of size variants with minimal setup cost. Regulatory emphasis on traceability and serialization increases the need for precise sizing records and compatible logistics. Overall, the Orthopedic Implants Size Market is shifting from broad SKU-heavy supply chains to more responsive, data-driven sizing ecosystems.

Clinical templating and digital preoperative planning have materially changed implant sizing workflows. Digital templating adoption across tertiary and specialty hospitals has increased first-pass fit rates by notable margins—institutions report first-fit improvements exceeding 25–30%—thereby reducing intraoperative size exchanges and associated delays. Digital workflows enable patient-specific selection of head diameters, cup sizes, and plate lengths before incision, which lowers the need for large in-theatre inventories. Additionally, templating integrates with inventory management systems to trigger just-in-time replenishment and reduce SKU carrying costs by an estimated 15–20% in pilot programs. The combined effect is improved operative efficiency, lower logistic overhead, and higher clinician confidence in implant fit, making templating a primary growth enabler for the Orthopedic Implants Size Market.

Supply-chain fragmentation and lead-time variability constrain the market by increasing the cost and risk of maintaining a full range of size variants. Precision machined and coated implants require controlled supply chains for raw titanium and cobalt-chromium alloys; disruptions can extend lead times by several weeks. Hospitals that must hold broad SKU assortments face inventory carrying costs and potential expiration or obsolescence of sterile kits. Smaller manufacturers encounter capital barriers to scale precision production and surface treatments, which raises barriers to introducing new size variants. Additionally, regulatory premarket pathways for new sizing systems add administrative lead time, delaying market entry and constraining rapid response to clinical demand shifts. These factors collectively limit the speed at which new size ranges can be introduced and widely adopted.

Additive manufacturing creates opportunities for low-volume, high-precision production of uncommon size variants and patient-matched devices without the capital intensity of conventional machining. On-demand printing reduces minimum order quantities and shortens lead times from weeks to days for select implants, enabling hospitals to carry fewer physical SKUs while still meeting diverse anatomical needs. The technology also supports rapid iteration of porous surfaces and bespoke geometries that improve osseointegration. Coupled with digital templating and integrated quality control, additive workflows can lower the total cost of ownership for rare size variants by 20–40% in pilot analyses. Partnerships between hospitals and contract manufacturers to deploy near-hospital micro-factories represent a clear growth avenue that marries clinical customization with inventory efficiency.

Regulatory complexity and reimbursement frameworks present persistent challenges. Introducing new sizing systems or patient-matched devices often triggers extensive regulatory review, increasing time-to-market and compliance costs for manufacturers. Reimbursement policies that do not differentiate between standard and patient-matched implants can blunt incentives to invest in custom sizing workflows. Smaller healthcare providers may lack capital to invest in digital templating licenses or robotics that optimize sizing decisions, slowing diffusion. Additionally, standardized pricing models for implants can reduce manufacturer margins on specialized sizes, making investments in niche sizing capabilities economically unattractive. These regulatory and financial headwinds constrain innovation and slow the adoption of advanced sizing technologies across the market.

Increasing adoption of AI-driven templating and planning: AI templating tools are in use across 45–70% of high-volume orthopedic centers, improving preoperative sizing accuracy by roughly 27% and reducing intraoperative sizing adjustments by up to 34%. This trend accelerates value-based procurement and SKU rationalization while shortening OR preparation time by measurable amounts.

Growth of additive manufacturing for size variants: On-demand 3D printing of implants and patient-matched components has expanded production runs by 18–40% for low-volume sizes, reducing average lead time from 21 days to under 7 days in early adopters. The shift enables hospitals to cut held SKU counts by near 20% while maintaining clinical coverage.

Shift to modular platforms and configurable kits: Use of modular implant systems has increased, with reported modular uptake rising by 32% in joint and trauma procedures; configurability reduces the number of distinct SKUs required per case by up to 28%, lowering sterilization and storage costs.

Sustainability and traceability initiatives influencing sizing practices: Traceability mandates and circularity programs are driving redesigns in packaging and return logistics; 38% of manufacturers report active programs to improve recycling and reduce single-use packaging, and hospitals are targeting a 25–30% reduction in disposable kit volumes over the next five years.

The Orthopedic Implants Size Market is segmented by product type, application, and end-user, each reflecting distinct procurement, clinical and manufacturing dynamics. Product segmentation distinguishes joint reconstruction, trauma fixation (screws & plates), spinal systems, patient-matched/custom devices, and ancillary implant categories; application segmentation covers elective joint arthroplasty, traumatic fracture repair, spinal fusion and deformity correction, and specialized reconstructive procedures; end-users include acute hospitals, ambulatory surgical centers (ASCs), specialty orthopaedic clinics, and contract manufacturers/third-party providers. Decision-making is driven by inventory complexity, templating and digital planning adoption, and the shift toward modular and on-demand manufacturing. Clinicians prioritize first-fit accuracy and reduced operating-room exchanges, while purchasers emphasize SKU rationalization and traceability. Procurement patterns indicate larger hospital systems centralize purchasing of modular kits, whereas ASCs favor smaller SKU footprints and rapid-turnaround supplies. The segmentation landscape therefore balances high-volume standard implants with a growing niche for bespoke, low-volume sizes enabled by digital workflows and flexible production.

Joint reconstruction implants (hip, knee, shoulder components) are the leading product type, representing 42% of global unit demand; their leadership reflects high procedural volumes, standardized sizing families, and extensive surgeon familiarity with modular componentry. Trauma fixation—plates and screws—follows at 30%, serving a broad spectrum of fracture patterns and remaining essential for acute care. Spinal implants account for 15%, driven by rising degenerative and degenerative-correction procedures. Patient-matched/custom implants are currently a smaller but rapidly expanding category at 6% of units; this segment is the fastest-growing, with an estimated CAGR of 12.0%, supported by additive manufacturing, improved imaging-to-implant workflows, and growing clinical acceptance. Remaining niche products (orthobiologics-linked implants, craniofacial devices, fixation accessories) make up the final 7% combined. In comparative terms: joint reconstruction commands 42% of adoption, trauma fixation 30%, spinal 15%; patient-matched systems are smaller today but growing fastest and expected to scale meaningfully.

Joint reconstruction (primary and revision arthroplasty) is the dominant application area, accounting for approximately 52% of implant use by procedure type due to large volumes of hip and knee replacements and expanding indications for younger patients. Trauma fixation (open reduction and internal fixation with plates/screws) represents about 24%, reflecting steady demand from emergency and elective trauma caseloads. Spinal fusion and interbody procedures contribute roughly 14%, while specialized reconstructive and oncologic implant applications make up the balance 10%. Comparative adoption: joint reconstruction currently accounts for 52% of application volume, trauma fixation 24%, spinal 14%, while reconstructive niches are rising fastest in relative terms—spinal reconstructive procedures and custom interbody devices show the highest growth momentum with an estimated CAGR of 9.0% for that application category. Short-term application trends show expanded use of modular components in primary arthroplasty and broader adoption of navigation/templating for trauma cases. In 2024, more than 42% of tertiary hospitals reported routine use of modular kits for routine arthroplasty, and over 35% of high-volume trauma centers reported integrating digital templating into emergency workflows.

Acute care hospitals (level-II/III and tertiary centres) are the principal end-user segment, responsible for roughly 65% of implant utilization owing to their high caseload of complex arthroplasty, trauma and spine procedures. Ambulatory surgical centers (ASCs) are the fastest-growing end-user channel, representing approximately 12% today with an estimated CAGR of 11.0%, driven by procedure migration to outpatient settings and demand for streamlined SKU kits. Specialty orthopaedic clinics and outpatient surgery groups account for about 10%, while contract manufacturers, device refurbishers and third-party logistics make up the remaining 13%. Comparative snapshot: hospitals lead in volume (65%), ASCs are growing fastest and increasing their share annually, specialty clinics are stable, and third-party service providers expand in support roles. Industry adoption rates show that around 48% of regional hospital networks have implemented centralized inventory and templating systems, while over 30% of ASCs reported standardizing on compact, modular implant trays to minimize storage and sterilization costs.

North America accounted for the largest market share at 32% in 2024 however, it is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2025 and 2032.

In 2024 North America recorded approximately USD 1,520 million in size-focused implant activity by unit valuation proxies, with 1.2 million implant units produced annually and 480+ million USD in precision manufacturing CAPEX. Clinical adoption metrics show 68% tertiary hospital templating use and 54% modular kit procurement across integrated health systems; SKU rationalization pilots reduced SKU counts by 25% in several hospital groups. The region reported 120+ additive manufacturing R&D projects and a 14% year-over-year rise in regulatory approvals for novel sizing systems. North America’s distribution network includes 4,500+ qualified orthopaedic distributors, with ASCs accounting for 12% of procedure volume and projected to increase device uptake by 40% from 2024–2032 in outpatient conversions. These numeric indicators reflect deep manufacturing capacity, strong clinical adoption, concentrated R&D investment, and scalable logistics infrastructure.

North America accounts for roughly 32% of global unit demand for size-specific orthopedic implants and operates production lines capable of 1.2 million units annually. Key industries driving demand include tertiary healthcare systems (arthroplasty and trauma), outpatient surgery networks, and private orthopedic specialty groups. Regulatory updates and streamlined device dossiers have accelerated approval workflows for sizing systems, while government and institutional capital support—reflected in USD 480M+ recent manufacturing investments—has improved precision machining and additive manufacturing capacity. Technological transformation includes widespread adoption of AI templating (used in 68% of tertiary centers), integration of robotic guides, and near-hospital 3D printing pilot sites. Local players and manufacturers are investing in modular kit programs and just-in-time logistics; one national OEM expanded a configurable tray program across 120 hospitals to reduce SKUs. Regional consumer behaviour shows higher enterprise adoption in hospitals and ASCs, preference for modular kits in urban centers, and faster uptake of patient-matched options in high-volume systems.

Europe represents approximately 28% of global unit demand by volume, with Germany, the UK, and France as the largest national markets (Germany and the UK together account for an estimated 40–45% of European demand). Regulatory bodies emphasize device traceability and sustainability initiatives, prompting manufacturers to adopt explainable templating workflows and recyclable packaging; 50%+ of large hospital groups now require serialization and size traceability. Technology adoption includes precision CNC machining, digital templating in 60% of orthopaedic centers, and regional hubs developing additive manufacturing competence. Local manufacturers are advancing surface-engineering programs and modular platforms; a European OEM launched a configurable hip/knee modular platform across 200 hospitals to standardize sizing families. Consumer behaviour shows strong regulatory-driven demand for explainable, validated templating tools and slower uptake of on-demand manufacturing compared with North America, while cost-conscious procurement in public systems favors standardized modular kits.

Asia-Pacific accounts for roughly 21% of global unit demand by volume and ranks third in market volume but first in year-over-year production growth metrics; major consuming countries include China, India, and Japan. Manufacturing trends show rapid capacity expansion—regional production lines increased output by 28% between 2022–2024—and rising investments in local precision machining and additive facilities. Innovation hubs in China and Japan are piloting near-hospital printing and image-to-implant workflows, and Indian contract manufacturers expanded export volumes by 35% in recent cycles. Local players focus on cost-efficient modular systems and scaling affordable patient-matched offerings; one APAC contract manufacturer increased output by 220,000 units in 2024. Consumer behaviour varies: urban tertiary centers adopt templating and patient-matched devices faster, while regional hospitals prioritize affordable, standardized kits.

South America accounts for about 8% of global unit demand, with Brazil and Argentina as the principal markets. Regional market share is concentrated—Brazil represents roughly 60% of South American volume—while infrastructure investments are uneven. Government incentives and trade policies have supported import facilitation and local manufacturing partnerships; several countries have introduced procurement frameworks that favor local assembly and certification. Local players and distributors have expanded modular kit offerings and partnered with OEMs to localize select production steps; one regional assembler scaled modular tray kits to 35 hospitals in 2024. Consumer behaviour shows price sensitivity and reliance on public procurement channels, with private hospitals in major cities adopting templating and modular platforms earlier than rural facilities.

Middle East & Africa represent approximately 7% of global unit demand, with the UAE and South Africa as leading national markets. Demand trends include hospital modernization programs, increased orthopedic elective procedures, and investments in advanced operating suites. Regional centers have expanded capabilities for precision implant handling and storage; a growing number of hospitals (estimated 20–30% in major urban centers) have adopted templating and modular kit strategies. Technological modernization includes importing precision machining and building regional distribution networks; trade partnerships with global OEMs have increased product availability and training programs. Local players are developing service models that combine supply and templating support; consumer behaviour varies widely—urban hospitals are early adopters of digital workflows while rural facilities remain dependent on standardized kits and imports.

United States — 32% Market Share: High production capacity (1.2M units/year), deep R&D investment, and widespread clinical templating adoption drive leadership in the Orthopedic Implants Size Market.

Germany — 11% Market Share: Strong precision manufacturing base, robust regulatory frameworks, and advanced hospital procurement systems sustain Germany’s leading position in the Orthopedic Implants Size Market.

The competitive environment of the Orthopedic Implants Size Market is characterized by a mix of large multinational manufacturers, mid-sized specialized producers, and emerging niche innovators focused on smart, modular, and patient-specific solutions. There are 30+ active competitors globally, with the top five companies collectively holding an estimated ~42–48% combined share of total unit demand, reflecting a moderately fragmented market landscape with many regional players and niche specialists. Established global participants maintain leadership through diversified product portfolios encompassing joint reconstruction, trauma fixation, spinal systems, and emerging smart implant platforms. Strategic initiatives include multiple partnerships, product launches, and M&A activity aimed at broadening surgical offerings, expanding size families, and integrating digital surgical workflows; for example, expansion of robotics-assisted systems and precision templating supports deeper clinical penetration.

Innovation trends influencing competition include adoption of additive manufacturing for low-volume and patient-matched sizes, AI-driven templating and planning tools that enhance first-fit accuracy, and sensor-enabled implants for postoperative monitoring. Competitive positioning also varies by geography: North American and European firms lead in digital surgical integration and modular systems, while Asia-Pacific players are scaling precision machining and volume production. The orthopedics landscape sees ongoing portfolio expansions and enhancements in surgical robotics and navigation, with over 100 new device variants introduced industry-wide in the past two years, underscoring the emphasis on technological differentiation and clinician preference alignment. Overall, competition remains dynamic, with capital allocation toward R&D, digital transformation, and improved clinical outcomes shaping market trajectories.

Johnson & Johnson (DePuy Synthes)

Medtronic plc

Globus Medical, Inc.

Arthrex, Inc.

DJO LLC

B. Braun SE

Corin Group

Technological advancements are reshaping the Orthopedic Implants Size Market, driving precision, personalization, and surgical efficiency. Additive manufacturing (3D printing) has emerged as a core technology, enabling patient-matched implants and rapid production of low-volume size variants with complex geometries that were previously infeasible through traditional machining. Production centers leveraging additive workflows report reductions in lead times from multiple weeks to under a week for select custom sizes, increasing responsiveness to clinical demand and reducing inventory requirements.

AI-driven templating and surgical planning tools are increasingly deployed in orthopedic departments, with reported improvements in preoperative sizing accuracy and reductions in intraoperative adjustments. These tools analyze imaging data and recommend optimal implant sizes, reducing SKU burdens and enhancing first-fit rates. Integration of templating with digital inventory systems supports automated restocking and just-in-time logistics for size-specific kits.

Innovations in robotics and navigation systems further augment the technology landscape. Surgical robotics platforms now guide resection and implant placement with sub-millimeter precision, interfacing with implant sizing data and templating plans to optimize alignment. Emerging sensor-enabled implants and smart platforms collect postoperative biomechanical data, facilitating long-term tracking of implant performance and enabling personalized rehabilitation protocols.

Materials science improvements—such as advanced coatings, porous surfaces, and hybrid biomaterials—enhance osseointegration and longevity of size-specific implants. These innovations help address bone quality variation and support broader clinician choice across diverse anatomical needs. Decision-makers and industry professionals must factor in these technology vectors when evaluating competitive positioning, capital allocation, and clinical adoption strategies, as technology trends increasingly drive differentiation and value delivery within the Orthopedic Implants Size Market.

In February 2024, Stryker showcased updates to its MAKO SmartRobotics™ platform and introduced the Triathlon® Hinge at AAOS 2024, positioning the Triathlon Hinge to reduce procedural steps in revision-to-hinge conversions and streamline instrumentation for complex knee revisions. Source: www.stryker.com

On 2 October 2024, Smith & Nephew launched the LEGION™ Hinged Knee System in the United States featuring OXINIUM™ oxidized-zirconium technology, expanding anatomical fit options for complex knee revisions and offering improved wear and corrosion resistance relative to prior materials. Source: www.smith-nephew.com

On 11 June 2024, Zimmer Biomet announced an exclusive distribution agreement to integrate its technologies with the TMINI miniature robotic system (THINK Surgical), creating a customized, wireless handheld robotic offering for total knee arthroplasty and expanding Zimmer Biomet’s robotic and size-planning ecosystem. Source: www.zimmerbiomet.com

In February 2024, Zimmer Biomet presented a slate of product and workflow innovations at AAOS 2024—including previews of robotic and implant advances (Persona® OsseoTi® keel tibia, ROSA® Shoulder preview and HAMMR™ Automatic Hip Impaction System)—underscoring enhanced sizing options and automation for knee and hip procedures. Source: www.zimmerbiomet.com

The Orthopedic Implants Size Market Report encompasses a comprehensive analysis of segmentations by product type, clinical application, end-user, technology integration, and geographic distribution. Product segmentation includes joint reconstruction components (hip, knee, shoulder), trauma fixation devices (plates, screws), spinal systems, and emerging patient-matched and smart implant categories. Application analysis covers primary and revision joint arthroplasty, fracture fixation, spinal fusion and deformity correction, and specialized reconstructive indications, with a focus on procedural adoption patterns and clinical workflows.

End-user categories analyzed include tertiary and acute care hospitals, ambulatory surgical centers, specialty orthopaedic clinics, and outsourced surgical supply partners. The geographic scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, emphasizing production and adoption dynamics, infrastructure trends, and regulatory frameworks across markets. Technology focus areas include digital templating, additive manufacturing, surgical robotics, navigation and augmented reality systems, and smart implant platforms with embedded sensors.

The report also evaluates competitive positioning, innovation trajectories, strategic partnerships, and manufacturing capacity variations. Emerging segments, such as size-specific modular kits and near-hospital additive micro-factories, are highlighted to reflect shifts toward responsive inventory models and customization. Additional niche focus areas include biomaterial innovations, eco-design in implant packaging, and cross-specialty integrations with data analytics—providing decision-makers with a richly detailed, business-oriented view of the Orthopedic Implants Size Market’s breadth and future directions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,738.0 Million |

| Market Revenue (2032) | USD 7,216.4 Million |

| CAGR (2025–2032) | 5.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers; Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory Overview; Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Zimmer Biomet Holdings, Inc., Stryker Corporation, Smith & Nephew plc, Johnson & Johnson (DePuy Synthes), Medtronic plc, Globus Medical, Inc., Arthrex, Inc., DJO LLC, B. Braun SE, Corin Group |

| Customization & Pricing | Available on Request (10% Customization Free) |