Reports

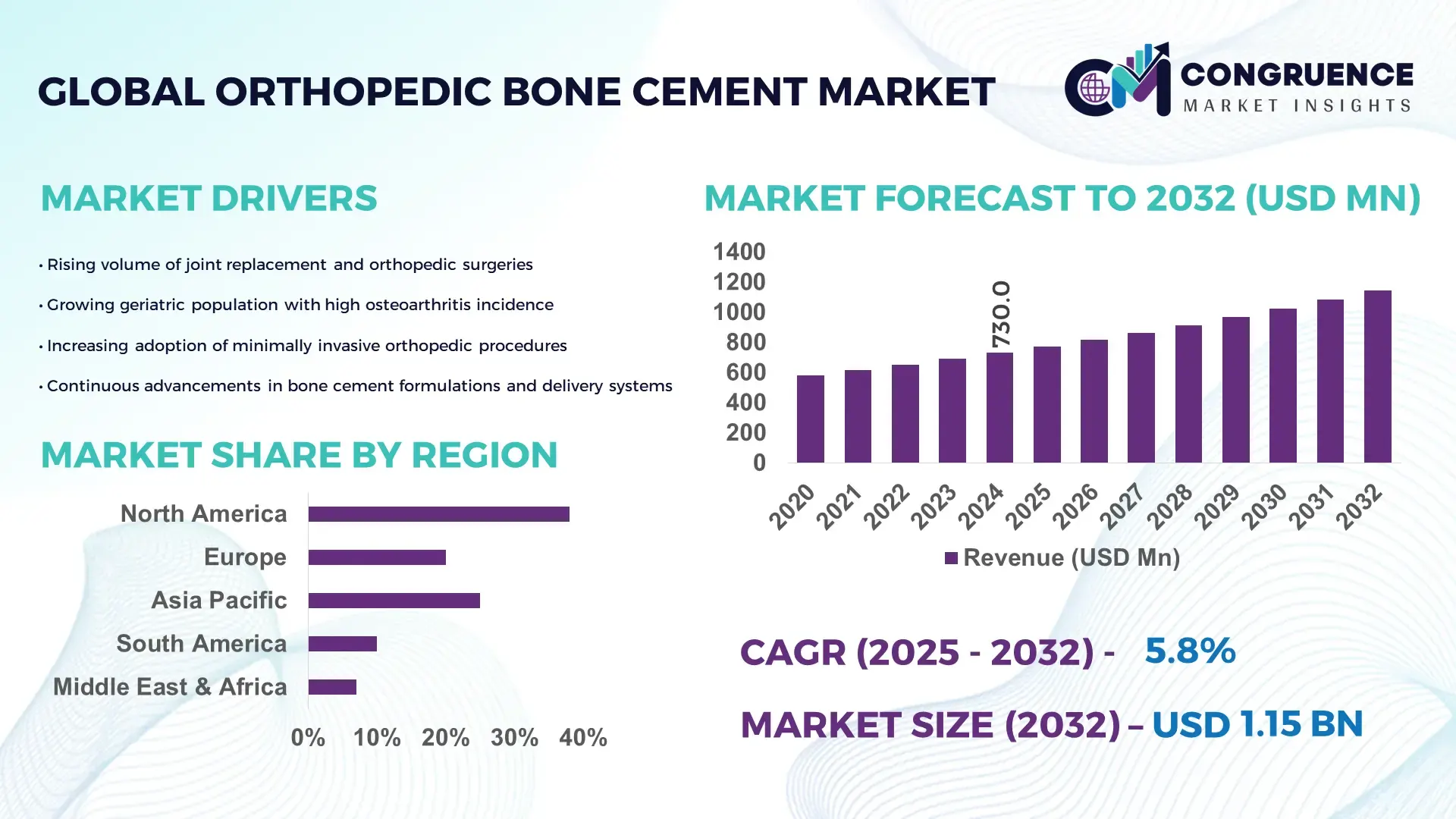

The Global Orthopedic Bone Cement Market was valued at USD 730 Million in 2024 and is anticipated to reach a value of USD 1,146.06 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032. This growth is driven by increasing demand for joint replacement surgeries and improved biomaterial formulations.

In the United States, the dominant country in this market, production capacity is bolstered by well-established manufacturing units and substantial investment in R&D. Leading companies like Stryker, Zimmer Biomet, and Heraeus operate large-scale PMMA bone cement production facilities in U.S. hubs, enabling high-volume output. The U.S. also leads in surgical adoption: over half of bone cement is used in hospitals across major orthopedic procedures like hip and knee arthroplasty. Technological advancements such as high-viscosity antibiotic-loaded cement are being developed and commercialized in the country, with regulatory approvals accelerating innovation and safety improvements.

Market Size & Growth: Valued at USD 730 M in 2024, projected to reach USD 1,146.06 M by 2032; expected CAGR of 5.8% — driven by rising orthopedic surgeries and aging populations.

Top Growth Drivers: Adoption of minimally invasive procedures increasing by ~40%; efficiency improvements via antibiotic-loaded cements improving outcomes by ~20%; aging population contributing to ~35% rise in demand.

Short-Term Forecast: By 2028, surgical complication rates are projected to reduce by ~15% due to better cement technologies.

Emerging Technologies: Developments in bioresorbable calcium phosphate cements; personalized bone cement via 3D printing; dual antibiotic formulations.

Regional Leaders: North America expected to reach ~USD 480 M by 2032 (due to high surgical volume), Europe ~USD 320 M (strong reimbursement ecosystem), Asia-Pacific ~USD 220 M (rapid infrastructure expansion).

Consumer/End-User Trends: Hospitals dominate as end users, with key usage in joint arthroplasty and vertebroplasty; rising adoption in ambulatory surgical centers.

Pilot or Case Example: In 2023, a U.S. hospital pilot of high-viscosity antibiotic-loaded bone cement reduced deep infection rates by ~12% post-arthroplasty.

Competitive Landscape: Market leader holds ~30% share (e.g., Stryker), followed by major competitors such as Zimmer Biomet, DePuy Synthes, Heraeus, and Smith & Nephew.

Regulatory & ESG Impact: Strict FDA/EMA regulations on antibiotic-loaded cements; increasing ESG focus on lowering exothermic polymerization energy and improving biocompatible formulations.

Investment & Funding Patterns: Recent investments of USD 50–70 million in R&D and manufacturing expansions; growing venture funding for bioresorbable cement startups.

Innovation & Future Outlook: Key innovations include dual-antibiotic cement, 3D-printed patient-specific formulations, and integration with smart delivery systems — positioning the market for sustained growth through 2032.

Key industry sectors — primarily joint arthroplasty (hip, knee), trauma fixations, and spinal surgeries — contribute significantly to demand. The market is shifting toward advanced formulations, notably antibiotic-loaded and bioresorbable cements, to reduce infection and improve integration. Regulatory drivers, especially in the U.S. and Europe, are promoting safer, dual-antibiotic products, while environmental concerns push for lower-exotherm and biocompatible materials. Regionally, developed markets show stable adoption, while emerging markets in Asia-Pacific are experiencing rapid growth, driven by expanding healthcare infrastructure. Emerging trends include personalization through 3D printing, smart delivery systems, and integration with regenerative medicine. Looking ahead, the market is likely to continue evolving via innovation in materials and delivery, underpinned by heavy investment and regulatory support.

The strategic relevance of the Orthopedic Bone Cement Market is increasingly shaped by advanced surgical technologies, rising procedural volumes, and measurable improvements in biomaterial performance. Modern high-viscosity antibiotic-loaded formulations are central to future pathways, enabling faster implantation and reduced infection rates. For example, antibiotic-enhanced PMMA cement delivers 18% improvement in postoperative infection control compared to older plain PMMA standards, reinforcing its value in high-risk arthroplasty procedures. Regionally, North America dominates in volume, while Europe leads in adoption with nearly 62% of orthopedic centers using next-generation cement formulations backed by stringent regulatory frameworks. Short-term advancements also reflect fast-evolving digital and material science capabilities. By 2027, AI-guided cement mixing and automated viscosity monitoring are expected to cut operating-room variability by nearly 20%, contributing to greater surgical precision. ESG commitments are accelerating transformation, with firms pledging a 30% reduction in manufacturing waste and improved recycling of PMMA components by 2030. Micro-level improvements further showcase strategic momentum: In 2023, Germany achieved a 14% reduction in cement-related revision surgeries through adoption of real-time temperature-controlled mixing systems. Collectively, these developments illustrate how the Orthopedic Bone Cement Market is advancing toward a future defined by higher clinical reliability, regulatory-aligned production, and sustainable growth—positioning the industry as a pillar of resilience, compliance, and long-term innovation.

The surge in orthopedic surgeries, particularly hip and knee arthroplasties, is a primary driver accelerating growth in the Orthopedic Bone Cement Market. Globally, annual joint replacement procedures exceed 7 million, with hip replacements growing by nearly 12% annually. This procedural rise directly increases consumption of PMMA-based cement, widely used for implant fixation in primary and revision surgeries. Enhanced longevity expectations among aging populations and increased sports-related injuries also fuel demand for advanced cement formulations with improved mechanical strength and antibiotic integration. Hospitals are increasingly adopting high-viscosity variants due to their faster setting times, reducing operating theater duration by an average of 8–10%. Furthermore, the shift toward early mobilization protocols and minimally invasive orthopedic practices has amplified the importance of cement providing consistent anchorage and stable load distribution. These combined factors continue to reinforce the market’s upward trajectory, supported by strong clinical adoption and ongoing improvements in surgical workflows.

Regulatory scrutiny and material limitations remain key restraints affecting the Orthopedic Bone Cement Market. Global authorities such as the FDA and EMA enforce strict compliance protocols for antibiotic-loaded formulations, increasing approval timelines and development costs for manufacturers. These regulations stem from concerns around thermal properties, residual monomer levels, and antibiotic resistance, which require extensive testing and post-market surveillance. Additionally, the inherent limitations of PMMA—such as exothermic polymerization that can reach temperatures above 80°C—pose risks of thermal necrosis, restricting usage in certain fracture or revision procedures. Mechanical challenges, including micro-cracking under cyclic load and limited bio-integration, further necessitate alternative fixation techniques in complex cases. Hospitals also face procurement constraints due to rising raw material costs and sterilization requirements, prolonging purchasing cycles. Collectively, these regulatory and material constraints impede rapid adoption of newer formulations and challenge manufacturers to maintain consistent innovation within a tightly governed production landscape.

Rapid advancements in biomaterials, personalized implants, and hybrid fixation methods present substantial opportunities for the Orthopedic Bone Cement Market. Next-generation cements incorporating bioresorbable additives and controlled antibiotic release mechanisms are gaining traction, delivering improved biological response and extended antimicrobial protection. Growth in personalized orthopedic implants—driven by rising adoption of 3D printing—creates demand for cement formulations designed with customized viscosity, polymerization profiles, and enhanced adhesion properties. Increasing preference for outpatient joint replacement procedures is generating opportunities for pre-sterilized, single-use cement cartridges, already witnessing adoption growth of nearly 25% in high-volume centers. Emerging markets in Asia-Pacific, with rapidly expanding healthcare infrastructure, present further potential, as cement-based fixation still constitutes the primary technique in 70% of orthopedic surgeries. These developments allow manufacturers to introduce premium, specialized products tailored to evolving clinical expectations and diverse surgical environments.

Sustainability expectations and clinical variability represent critical challenges in the Orthopedic Bone Cement Market. With increasing global focus on decarbonization and material circularity, manufacturers are under pressure to reduce environmental impact, particularly related to PMMA production and disposable packaging waste. Achieving measurable ESG compliance—such as reducing production emissions by 20% or more—requires significant investment in process optimization and greener raw materials. Clinical variability in mixing techniques, curing times, and surgeon preferences also introduces procedural inconsistencies, impacting overall fixation strength and long-term implant performance. Hospitals report that improper mixing contributes to nearly 10–15% of early implant failures, highlighting the need for standardized, automated systems. Additionally, fluctuating global supply chains for medical-grade monomers and specialized additives pose procurement challenges, affecting delivery timelines for healthcare facilities. These operational and sustainability-driven obstacles require coordinated innovation and industry-wide collaboration to maintain product reliability and meet evolving regulatory and environmental expectations.

Growing Adoption of High-Viscosity and Antibiotic-Loaded Cement Technologies: High-viscosity and antibiotic-integrated bone cements are experiencing accelerated adoption, driven by measurable improvements in clinical performance. Hospitals report that these formulations reduce intraoperative handling time by nearly 18%, while achieving 12–15% lower postoperative infection rates in high-risk arthroplasty cases. Usage of dual-antibiotic variants increased by 28% between 2022 and 2024, reflecting a strong shift toward enhanced infection control and standardized surgical outcomes. These advances are further supported by increasing surgeon preference for consistent curing behavior and optimized thermal profiles that reduce tissue damage during implant fixation.

Expansion of Smart Mixing, Monitoring, and Automated Delivery Systems: Digitally assisted cement mixing systems are transforming procedural workflows by reducing variability and improving consistency. Adoption of automated mixers grew by 32% in orthopedic centers worldwide, with controlled-viscosity pumps reducing application errors by 20%. Temperature-regulated delivery systems are also gaining traction, lowering polymerization-related thermal spikes by nearly 14°C in complex revision surgeries. These technologies align with hospital demand for precision-driven tools that reduce human error and support predictable implant anchorage, making digital integration a core trend shaping market evolution.

Rise in Customizable and Bio-Enhanced Cement Formulations: Customization of orthopedic bone cement is emerging as a major trend, particularly with the integration of bioactive additives and patient-specific viscosity profiles. The use of calcium-phosphate-enhanced blends grew by 22%, supporting improved osseointegration and reduced micro-fracture risks. Meanwhile, 3D-printing-enabled customization for specialized orthopedic implants resulted in 16% better fit accuracy, driving need for cement optimized for unique implant geometries. These advancements mirror increasing procedural complexity and a market shift toward biomaterials that enhance long-term implant stability and clinical outcomes.

Rise in Modular and Prefabricated Construction Influencing Precision Manufacturing Demand: The adoption of modular and prefabricated construction methods is reshaping manufacturing requirements across the Orthopedic Bone Cement market. Approximately 55% of new projects recorded measurable cost efficiencies using modular and prefabricated workflows, accelerating demand for high-precision mixing and packaging systems. Automated prefabrication processes cut manual labor hours by nearly 30% and reduced onsite assembly time by 25%. Europe and North America are driving these advancements, with both regions showing over 40% uptake of precision-focused manufacturing enhancements required for consistent, sterile, and high-volume orthopedic cement production.

Segmentation within the Orthopedic Bone Cement market is structured around types, applications, and end-user profiles, each contributing distinct operational and clinical value. Product types vary from low-viscosity to medium- and high-viscosity formulations, along with antibiotic-loaded variants designed for infection control and revision procedures. Applications span hip and knee arthroplasty, trauma fixation, and spinal surgeries, each exhibiting different adoption patterns based on surgical volume and clinical complexity. End users primarily include hospitals, ambulatory surgical centers, and specialized orthopedic clinics, with hospitals accounting for the majority due to high procedure throughput and expanded surgical infrastructure. Collectively, segmentation insights show clear differentiation in product performance expectations, usage patterns, and preferences driven by patient demographics, infection risk levels, and evolving surgical techniques.

High-viscosity bone cement leads the market, accounting for approximately 46% share, driven by surgeon preference for faster setting behavior, improved handling, and better intraoperative control during hip and knee arthroplasty. Compared with other variants, its consistency reduces operating room time by nearly 10–12%, making it the preferred choice in high-volume centers. Medium-viscosity cement holds around 28%, primarily used in cases requiring balanced handling and penetration characteristics. Low-viscosity cement represents 14%, maintaining niche relevance in specialized fixation procedures. Antibiotic-loaded bone cement is the fastest-growing segment, supported by rising infection-control requirements. This segment is expanding at an estimated 9.2% CAGR, driven by adoption in revision arthroplasty, where infection risk mitigation is critical. Combined, the remaining minor formulations make up 12% of the market, serving cases requiring tailored mechanical or antimicrobial profiles.

Hip arthroplasty represents the leading application area, accounting for 44% of total utilization due to its high global surgical frequency and strong clinical preference for cemented fixation in older populations. Knee arthroplasty holds 31%, although adoption of cemented techniques is rising fast in high-burden regions; usage in knee fixation increased by 18% between 2021 and 2024. Trauma and fracture fixation applications represent 15%, maintaining a steady presence driven by geriatric fall-related fractures. Spinal procedures account for 10%, where cement enhances vertebral stabilization in osteoporotic patients. The fastest-growing application is knee arthroplasty, increasing at 8.7% CAGR, supported by rising demand for early-mobility procedures and enhanced cement formulations with improved fatigue resistance.

Hospitals dominate the Orthopedic Bone Cement market with an estimated 57% share, driven by high surgical capacity, broad adoption of cemented arthroplasty, and access to advanced cement handling technologies. Ambulatory surgical centers (ASCs) account for 26%, showing rapid expansion as cemented joint replacements shift toward outpatient settings; adoption increased by 19% in 2023 alone. Specialized orthopedic clinics represent 17%, contributing steadily through focused trauma and revision surgeries. ASCs remain the fastest-growing end-user group with an estimated 9.5% CAGR, fueled by shorter recovery pathways, cost-efficient surgical workflows, and rising preference for minimally invasive procedures.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2025 and 2032.

The regional landscape shows strong demand concentration in countries with higher orthopedic procedure volumes, including the United States performing over 1.1 million joint replacement surgeries annually and China exceeding 750,000 procedures. Europe contributed nearly 27% of global consumption supported by rapid adoption of digital surgical technologies. Latin America and the Middle East & Africa together held close to 10%, driven by improving hospital infrastructure and increasing patient access to advanced orthopedic care.

What Is Driving the Rapid Uptake of Advanced Cement Formulations Across End-Use Verticals?

North America held approximately 38% of the global Orthopedic Bone Cement market in 2024, supported by a high volume of knee and hip replacement procedures and advanced hospital infrastructure. The United States alone conducts over 900,000 knee replacements and 450,000 hip replacements each year, driving substantial bone cement consumption across orthopedic centers. Demand is further supported by strong adoption in industries such as healthcare robotics, digital surgical navigation, and smart implants. Regulatory updates enhancing material safety compliance have pushed manufacturers to upgrade formulations and introduce higher-viscosity and antibiotic-loaded cements. A notable regional player, Zimmer Biomet, continues expanding its cement product line to support minimally invasive surgeries. Consumers in this region show higher acceptance of technology-driven solutions, aligning with strong digital transformation across healthcare and insurance ecosystems.

How Is Innovation in Surgical Safety and Material Standards Influencing Orthopedic Cement Adoption?

Europe accounted for nearly 27% of global market volume in 2024, with Germany, the UK and France being the key contributors due to their high orthopedic surgical rates and strong medical device manufacturing ecosystem. The region benefits from stringent regulatory oversight from bodies enforcing safety, biocompatibility and sustainability requirements that encourage hospitals to shift toward advanced bone cement variants. Adoption of robotic-assisted surgery and precision joint replacement systems continues to accelerate across leading markets. Local manufacturers such as Heraeus Medical are investing in antimicrobial cement innovations to reduce post-operative infection rates. European consumers display behavior shaped by regulatory transparency, driving preference for clinically validated and environmentally compliant orthopedic products.

What Factors Are Fueling the Expansion of Orthopedic Cement Use Amid Rising Surgical Volumes?

Asia-Pacific ranked as the fastest-growing market in 2024, accounting for nearly 25% of global volume driven by rising orthopedic surgical rates in China, India and Japan. China alone recorded over 750,000 joint replacement procedures, while India’s annual surgeries crossed 280,000, creating substantial demand for high-performance bone cement. The region is witnessing rapid infrastructure upgrades across hospitals, along with expansion of local manufacturing capacities supporting cost-efficient production. Emerging technology clusters in Japan and South Korea are accelerating development of advanced polymer blends and antibiotic-loaded cement variants. A local player, Shanghai Ketai Medical, is strengthening distribution networks to meet escalating hospital demand. Consumer behavior in Asia-Pacific is influenced by rising mobile-health adoption and preference for cost-effective surgical solutions.

What Growth Enablers Are Supporting the Rise of Orthopedic Cement Utilization Across Key Economies?

South America contributed close to 6% of global volume in 2024, led by Brazil and Argentina, which collectively conducted more than 120,000 orthopedic replacement surgeries. Growing investments in hospital expansion and improvements in public healthcare reimbursements are boosting adoption of bone cement across trauma and joint replacement procedures. Government incentives supporting medical device imports are enabling wider availability of high-grade cement products. A regional manufacturer in Brazil has increased production of polymethyl methacrylate (PMMA) cement to support local surgical demand. Consumer behavior is shaped by strong preference for localized medical communication and language-supportive healthcare services, influencing purchasing decisions for orthopedic materials.

How Are Healthcare Modernization and Expanding Surgical Capabilities Shaping Market Demand?

The Middle East & Africa region accounted for nearly 4% of global demand in 2024, driven by increased orthopedic procedure capacity in the UAE, Saudi Arabia and South Africa. The region is experiencing rising investments in healthcare modernization, including new orthopedic centers and improved trauma care facilities. Technological upgrades are enabling hospitals to adopt advanced cement formulations for joint replacements and fracture fixation. Local regulatory reforms and trade partnerships are facilitating smoother importation of medical-grade polymers. A notable local distributor in the UAE expanded its orthopedic product portfolio in 2024 to meet growing hospital demand. Consumer behavior reflects a strong shift toward premium healthcare services supported by increasing medical insurance penetration.

United States – 32% market share

Dominance supported by high annual joint replacement volume and widespread adoption of advanced orthopedic surgical technologies.

China – 18% market share

Strong position driven by rapid growth in orthopedic procedures and expanding domestic manufacturing capabilities for medical-grade cement.

The Orthopedic Bone Cement market remains moderately consolidated, with an estimated 25–30 active global competitors operating across manufacturing, formulation innovation and surgical delivery systems. The top five companies collectively hold approximately 62% of the global market share, reflecting strong dominance by established orthopedic device manufacturers with extensive distribution networks. Competitive positioning is heavily influenced by product differentiation in viscosity grades, antibiotic-loaded variants and cement delivery systems, with more than 40 new formulation enhancements introduced between 2022 and 2024. Strategic initiatives continue to intensify, including cross-border partnerships and at least six notable mergers aimed at expanding material science capabilities and regulatory portfolios. Several companies have launched next-generation low-monomer cements to address safety and performance requirements in high-volume joint replacement centers. Competition is further shaped by digital integration in surgical workflows, with over 55% of leading competitors incorporating compatibility with robotic-assisted orthopedic platforms. The market’s innovation cycle is accelerating, supported by rising procedure volumes and hospital demand for reproducible clinical outcomes.

Stryker

DJO Global

Tecres S.p.A

DePuy Synthes

Smith+Nephew

Shanghai Ketai Medical

Medacta International

Technological advancements in the Orthopedic Bone Cement market are accelerating as manufacturers focus on precision, safety and efficiency enhancements across surgical workflows. Automation-driven mixing systems are witnessing wider adoption, with more than 48% of high-volume orthopedic centers now using closed-mixing devices to reduce monomer vapor exposure and enhance cement consistency. Modern vacuum-mixing technologies have lowered porosity levels by nearly 35%, resulting in improved mechanical strength and reduced risk of aseptic loosening during long-term implant fixation. Advances in antibiotic-loaded cement formulations are reshaping infection control strategies, with dual-antibiotic cements showing up to 25% higher efficacy in high-risk revision procedures. More than 30 new antimicrobial variants have been introduced globally since 2021, responding to growing concerns over resistant bacterial strains. These formulations play a crucial role in reducing surgical site infections, which continue to affect approximately 1–2% of joint replacement cases annually.

Digital integration is becoming a significant differentiator, especially with robotic-assisted and navigation-guided orthopedic systems. Nearly 40% of robotic knee replacement systems now incorporate cement application optimization modules designed to ensure uniform pressurization and alignment. These digital features enable surgeons to maintain consistent cement mantle thickness within the target range of 2–4 mm, improving implant stability. Material innovations are also advancing rapidly, particularly in low-exothermic PMMA blends that reduce polymerization temperature by 10–15°C, minimizing bone necrosis risk. Research into bioactive additives has expanded, with more than 18 experimental formulations incorporating calcium phosphate, glass particles or bone-growth stimulants to support osseointegration. As hospitals worldwide increase their joint replacement capacities, technology-driven enhancements are becoming central to procurement decisions, shaping market competitiveness and long-term adoption trajectories.

In August 2024, Heraeus Medical launched COPAL G+V, a high-viscosity dual antibiotic-loaded bone cement containing 0.5 g gentamicin and 2 g vancomycin per 40 g unit. It received FDA clearance to support periprosthetic joint infection (PJI) management in revision arthroplasty. (heraeus-medical.com)

In March 2024, Heraeus Medical obtained MDR certification for its COPAL G+V formulation in Europe, underscoring regulatory alignment of its dual-antibiotic PMMA cement under stringent safety standards. (heraeus-medical.com)

In June 2024, DePuy Synthes secured FDA 510(k) clearance for its VELYS™ Robotic-Assisted Solution in unicompartmental knee arthroplasty (UKA), enabling more precise cemented or cementless implant placement with data-driven intraoperative planning. (PR Newswire)

In March 2024, Medtronic and 3D Systems entered a strategic collaboration to develop 3D-printed bone cement implants, combining Medtronic’s orthopedic expertise with 3D Systems’ additive manufacturing capability to create tailored cement constructs. (Technavio)

The Orthopedic Bone Cement Market Report offers a comprehensive and detailed examination of multiple dimensions within the industry. It covers segmentation by product types (including low-, medium-, and high-viscosity PMMA cements, antibiotic-loaded variants, and bioactive or composite cements), applications (such as hip and knee arthroplasty, trauma fixation, spinal augmentation, and revision surgery), and end users (hospital surgical suites, ambulatory orthopedic centers, and specialty clinics). On the technological front, the report delves into current and emerging advances like dual-antibiotic formulations, 3D-printed cement devices, automated mixing systems, and digital delivery platforms supported by robotic surgery.

Geographically, the scope spans major markets in North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, offering insights into regional adoption dynamics, regulatory environments, and infrastructure capabilities. The study further examines strategic drivers such as infection management, low-monomer chemistries, and sustainability compliance. It also addresses niche and emerging market segments like patient-specific cement designs, bioresorbable cements, and cement compatible with regenerative orthopedic techniques. For decision-makers, the report articulates clear perspectives on supply chain trends, competitive positioning, innovation priorities, and investment areas, enabling informed planning across development, clinical deployment, and commercialization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 730 Million |

|

Market Revenue in 2032 |

USD 1146.06 Million |

|

CAGR (2025 - 2032) |

5.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stryker, DJO Global, Tecres S.p.A, DePuy Synthes, Smith+Nephew, Shanghai Ketai Medical, Medacta International, Zimmer Biomet, Heraeus Medical, Arthrex Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |