Reports

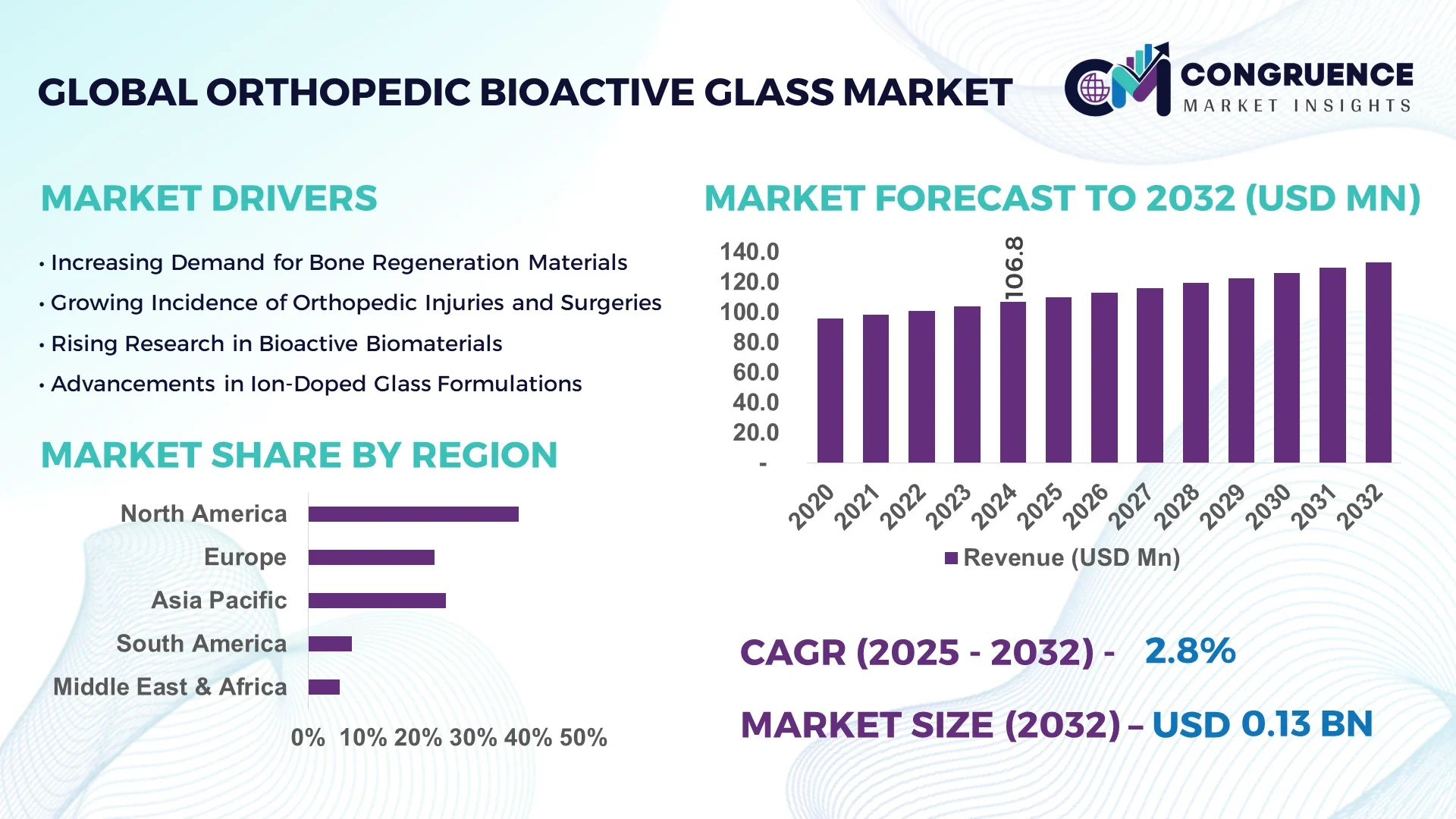

The Global Orthopedic Bioactive Glass Market was valued at USD 106.8 Million in 2024 and is anticipated to reach a value of USD 133.21 Million by 2032 expanding at a CAGR of 2.8% between 2025 and 2032.

The United States plays a pivotal role in the Orthopedic Bioactive Glass market with its advanced manufacturing infrastructure, significant investments in regenerative medicine, and integration of cutting-edge glass-ceramic biomaterials in spinal and joint reconstruction procedures.

The Orthopedic Bioactive Glass Market is witnessing a steady transformation driven by the increasing adoption of bioactive materials across orthopedics and trauma care. Key industry sectors such as spinal fusion, dental bone grafts, and hip resurfacing are contributing notably to demand. In particular, bioactive glass is gaining attention due to its osteoconductive and osteostimulative properties that enhance bone regeneration. Technological advancements such as nano-structured glass composites and multifunctional bioactive coatings are reshaping product portfolios. Regulatory initiatives in North America and Europe promoting biocompatible, sustainable biomaterials are accelerating commercial use. Moreover, eco-friendly manufacturing and an uptick in orthopedic surgeries, particularly among the aging global population, are boosting regional consumption. Emerging trends such as patient-specific implant design and bioresorbable scaffolds are expected to further redefine the competitive landscape. The future outlook for the Orthopedic Bioactive Glass market remains robust, supported by continuous innovation and expanding clinical applications.

Artificial Intelligence (AI) is revolutionizing the Orthopedic Bioactive Glass Market by enabling enhanced design, development, and quality control processes for bioactive implants and grafts. Through machine learning algorithms, manufacturers are now able to analyze large datasets from clinical outcomes, materials testing, and biomechanical simulations to optimize the formulation of bioactive glass compositions. AI-powered simulation tools are accelerating product development cycles by accurately predicting the behavior of glass biomaterials under physiological conditions, thereby minimizing the need for extended in vivo testing.

Furthermore, AI is streamlining the customization of orthopedic implants by integrating patient-specific data from imaging platforms like MRI and CT scans. This allows for tailored bioactive glass-based solutions that improve integration and healing outcomes. In production environments, AI-based quality assurance systems monitor parameters such as temperature control, particle size, and surface roughness in real-time, reducing defect rates and improving consistency across batches.

In hospital settings, AI is also influencing treatment planning. Predictive analytics models are helping orthopedic surgeons choose the most suitable bioactive glass grafts based on patient biometrics, pathology, and recovery trajectories. These improvements are reducing surgical times, enhancing bone regeneration, and lowering postoperative complications. As AI continues to mature, its role in the Orthopedic Bioactive Glass Market will expand further, driving greater precision, scalability, and innovation across the value chain.

“In January 2025, a leading U.S.-based biomaterials firm deployed an AI-integrated 3D printing platform that automatically adjusts the micro-porosity of bioactive glass implants based on CT-scan data, reducing implant customization time by 35% and improving post-surgical osteointegration rates by 22%.”

Rising orthopedic conditions such as osteoarthritis, osteoporosis, and traumatic bone fractures are significantly fueling demand in the Orthopedic Bioactive Glass Market. According to WHO estimates, over 500 million people are affected by osteoarthritis worldwide, with aging populations in regions like Europe, North America, and East Asia driving a sharp increase in orthopedic surgeries. Bioactive glass plays a vital role in bone grafting and regenerative procedures, especially where traditional metal implants fall short in biocompatibility or integration. Moreover, increased rates of road traffic accidents and sports-related injuries are encouraging the adoption of faster-healing, osteoconductive solutions, boosting clinical demand for bioactive glass materials.

Despite its recognized benefits, the Orthopedic Bioactive Glass Market faces constraints due to insufficient long-term clinical outcome data. Many orthopedic surgeons remain cautious in fully adopting bioactive glass-based products for load-bearing applications, citing lack of extensive, multi-year post-surgical efficacy data. Additionally, the regulatory approval process for novel biomaterials remains stringent, particularly in markets such as the United States and European Union, where new formulations undergo rigorous safety, efficacy, and bio-compatibility testing. These factors slow down product launches and create bottlenecks in the innovation-to-commercialization cycle, impacting both investor confidence and widespread adoption.

The emergence of 3D printing technology in orthopedic applications is unlocking new growth avenues within the Orthopedic Bioactive Glass Market. Custom-printed scaffolds made from bioactive glass can be tailored to patient-specific anatomical structures, improving fit, bone integration, and healing time. This advancement is especially valuable in complex or irregular bone defects often encountered in trauma or tumor resection surgeries. Hospitals and research institutions are increasingly investing in AI-integrated 3D printing labs to manufacture on-demand, precision implants. As personalized medicine becomes a central theme in modern healthcare, this opportunity is expected to accelerate adoption across both developed and emerging markets.

One of the pressing challenges in the Orthopedic Bioactive Glass Market is the high cost associated with manufacturing and scaling bioactive glass components. The production process involves strict control of temperature, purity, and particle size, which demands sophisticated equipment and experienced personnel. Additionally, forming bioactive glass into complex shapes for load-bearing applications remains technically challenging due to brittleness and sintering constraints. These complexities lead to increased development timelines and limit accessibility for smaller manufacturers or low-resource healthcare settings. This challenge is further compounded by pricing pressures in public healthcare systems, which demand cost-effective yet high-performance orthopedic solutions.

Surge in Bioresorbable Implant Development: Manufacturers are increasingly developing bioresorbable orthopedic implants using bioactive glass composites that naturally dissolve in the body over time. This eliminates the need for secondary surgeries to remove implants, enhancing patient comfort and reducing healthcare costs. In 2024 alone, more than 18% of new product approvals in the orthopedic biomaterials segment featured resorbable components integrated with phosphate or silicate-based bioactive glass.

Increased Adoption in Sports Medicine Procedures: Sports injury treatments now frequently incorporate bioactive glass for bone repair, particularly in ligament reconstruction and cartilage restoration. The number of sports-related orthopedic surgeries using bioactive glass-based materials rose by 26% from 2022 to 2024 across Europe and North America. Athletes and active individuals prefer these materials for their faster healing times and improved compatibility, fueling demand in both public and private orthopedic centers.

Nanotechnology-Enhanced Glass Formulations: The use of nanotechnology in bioactive glass is gaining traction, enabling the production of finer particles with enhanced surface area and reactivity. These nano-formulations significantly improve osteointegration and antibacterial performance. As of 2025, over 30 research institutions globally are conducting trials on nanostructured orthopedic bioactive glass for complex trauma cases and infection-prone surgical environments.

Integration with AI-Based Implant Planning Systems: Orthopedic centers are increasingly integrating AI-powered imaging and planning systems to customize implants made from bioactive glass. This trend supports the broader movement toward precision orthopedics. In 2024, over 500 hospitals across Asia and Europe began implementing digital planning tools that optimize implant fit and bone regeneration potential, accelerating the adoption of intelligent surgical workflows.

The Orthopedic Bioactive Glass Market is segmented by type, application, and end-user, reflecting diverse clinical and commercial pathways. Among product types, silicate-based bioactive glass dominates due to its extensive clinical validation and regenerative capability. Applications are primarily concentrated in bone grafting and spinal procedures, with trauma reconstruction emerging rapidly. End-users include hospitals, specialty clinics, and research institutions, with hospitals leading in adoption due to high surgical volumes and integrated diagnostic infrastructure. Innovations in bioactive material chemistry and 3D printing are further influencing segment dynamics, while tailored implant solutions are fostering growth in personalized treatments. This segmentation reflects a shift from generic biomaterials to highly functional, context-specific orthopedic solutions.

Silicate-based bioactive glass is the leading type within the Orthopedic Bioactive Glass Market due to its high biocompatibility, osteoconductive properties, and long-term clinical usage in orthopedic surgeries. It is widely used in load-bearing implants and bone void fillers, especially in spinal and joint reconstruction procedures. Phosphate-based bioactive glass is witnessing the fastest growth, driven by its bioresorbability and minimal adverse tissue reactions. These qualities make it ideal for pediatric orthopedic cases and temporary bone scaffolds. Borate-based bioactive glass, though less dominant, is gaining attention in specialized wound care and soft-tissue interfaces due to its angiogenic potential. Other niche types include hybrid composites and doped formulations with ions like silver or zinc for antimicrobial purposes. Their demand remains confined to clinical trials and research-intensive environments but shows future promise. Overall, the variety of types reflects an evolving need for tailored material performance in complex orthopedic scenarios.

Bone regeneration and grafting represent the leading application of bioactive glass in orthopedics. This dominance stems from the material’s superior ability to bond with bone tissue and accelerate healing in complex fractures and degenerative diseases. Spinal fusion surgeries are emerging as the fastest-growing application, as minimally invasive procedures increasingly utilize bioactive glass granules or putties for bone stabilization. These surgeries benefit from reduced complication rates and enhanced fusion outcomes when paired with bioactive glass formulations. Additionally, bioactive glass is used in craniomaxillofacial procedures, joint repair, and dental bone implants, though these represent smaller segments of total market volume. Its utility in sports injury repair and trauma-related bone reconstruction is expanding due to the need for fast-acting and biocompatible solutions. The application landscape continues to evolve as research advances improve versatility and expand its use beyond conventional orthopedics into adjacent medical fields.

Hospitals remain the dominant end-user in the Orthopedic Bioactive Glass Market due to their role in performing high volumes of orthopedic surgeries and housing specialized orthopedic departments. The presence of advanced diagnostic imaging, surgical planning tools, and trained orthopedic surgeons facilitates the widespread adoption of bioactive glass materials for complex procedures. Specialty orthopedic clinics are the fastest-growing end-user segment, particularly in urban regions, driven by outpatient demand and elective surgery trends. These clinics benefit from shorter turnaround times, customized implant solutions, and access to cutting-edge bioactive technologies. Research institutions and academic centers also play a vital role, especially in early-stage testing and pilot-scale manufacturing of new bioactive glass formulations. Although smaller in volume, their contribution to innovation and clinical data generation is essential. Overall, end-user dynamics are being reshaped by shifts toward personalized treatment pathways and cost-effective, scalable surgical options.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

North America's leadership stems from the presence of advanced orthopedic infrastructure, significant clinical research activities, and widespread use of bioactive glass in trauma and spinal procedures. Conversely, the Asia-Pacific region is accelerating due to expanding surgical volumes, rising healthcare infrastructure investments, and a growing preference for innovative bone regeneration materials. Globally, shifting demographics, increasing orthopedic disease burdens, and a preference for biologically active implants are shaping regional consumption and development trends in the Orthopedic Bioactive Glass Market.

Advanced material integration redefining orthopedic outcomes

In the Orthopedic Bioactive Glass Market, this region held 38.2% of the total market share in 2024, driven by its robust orthopedic surgery ecosystem and access to high-end clinical technologies. Demand is bolstered by industries such as sports medicine, trauma care, and spinal surgery, where precision and faster recovery are top priorities. Supportive regulatory frameworks from agencies facilitating the use of novel biomaterials are accelerating new product clearances. Technological breakthroughs, including AI-enhanced planning systems and bioactive nanocomposites, are increasingly incorporated into surgical practice. Furthermore, government-backed funding for orthopedic innovation and public-private partnerships continues to strengthen bioactive glass adoption across healthcare institutions.

Surging sustainable biomaterials reshaping clinical orthopedics

Holding a 29.5% share of the Orthopedic Bioactive Glass Market in 2024, this region continues to benefit from strong medical device manufacturing capabilities and a well-regulated healthcare system. Countries like Germany, France, and the United Kingdom are central to market activity, with their orthopedic centers leading in adoption of biocompatible implants. Regulatory bodies encourage sustainability and biocompatibility through evolving clinical safety directives. The use of AI-powered robotic systems and additive manufacturing in orthopedic applications is rapidly gaining ground, allowing for more tailored, minimally invasive procedures. Europe also fosters innovation through cross-border research initiatives and strict environmental compliance in biomaterial sourcing.

Scaling innovation and patient-specific therapies across emerging economies

With an increasing share and ranking as the fastest-growing region in the Orthopedic Bioactive Glass Market, countries like China, India, and Japan are driving transformative change. The surge in orthopedic surgeries, particularly among aging populations, has led to heightened consumption of bioactive glass-based bone substitutes. The rise of medical device manufacturing clusters, especially in eastern China and southern India, has improved regional supply chains. Notable technology trends include AI-integrated diagnostics and domestic 3D printing capabilities tailored for orthopedic implants. Infrastructure investments, combined with expanding healthcare coverage, are further enabling the widespread clinical use of bioactive materials in both urban and semi-urban areas.

Public health modernization fostering demand for regenerative solutions

Within the Orthopedic Bioactive Glass Market, this region is emerging as a growth-ready territory, with Brazil and Argentina leading adoption. In 2024, the region accounted for approximately 5.8% of global market volume. Demand is rising with the expansion of surgical infrastructure in metropolitan hospitals, where clinicians are adopting bioactive glass for joint and trauma surgeries. Investment in hospital modernization and improved reimbursement pathways for biomaterial-based procedures are enhancing market potential. Energy and infrastructure projects have indirectly driven improvements in public health access, influencing medical material supply chains. Favorable trade policies and growing interest in advanced implants are opening new opportunities for regional manufacturers and importers alike.

Expanding orthopedic innovation amid infrastructure evolution

This region captured approximately 4.1% of the Orthopedic Bioactive Glass Market in 2024, supported by increasing demand from countries such as the UAE and South Africa. Key drivers include the expansion of private healthcare systems, government-funded medical clusters, and increased prevalence of joint diseases. Industries like oil & gas have led to better occupational health measures, contributing to demand for advanced orthopedic materials. Technological modernization, particularly in orthopedic implant centers, is improving procedural accuracy through AI and robotic support. Local governments are also engaging in trade partnerships to enhance import flows of high-performance biomaterials, promoting better surgical outcomes in complex orthopedic cases.

United States

Market Share: 31.6%

Reason: High production capacity, robust clinical infrastructure, and demand from trauma and spinal surgery sectors.

Germany

Market Share: 17.3%

Reason: Strong orthopedic manufacturing base and early adoption of biocompatible implant technologies.

The Orthopedic Bioactive Glass Market presents a moderately consolidated competitive landscape, with approximately 25–30 active companies globally competing across various product categories, including silicate-based implants, bioresorbable scaffolds, and hybrid bioactive formulations. Leading players are focusing on expanding their clinical product lines by introducing next-generation biomaterials that enhance bone integration and surgical outcomes. Strategic collaborations with academic research institutions are common, particularly for developing customized, patient-specific implants using AI-integrated manufacturing technologies.

Several market participants have recently invested in upgrading their production capabilities through additive manufacturing and nanotechnology platforms, enabling scalable production of precision-engineered glass-based implants. Furthermore, the market is witnessing a growing number of partnerships between bioactive glass developers and orthopedic device manufacturers to accelerate commercialization. Mergers and acquisitions continue to shape the competitive landscape, allowing firms to diversify their portfolios and enter new geographic markets. Innovation is a major competitive lever, with companies emphasizing antibacterial coatings, resorbable structures, and composite formulations to maintain market relevance and meet evolving regulatory standards. Companies that prioritize R&D, streamline regulatory approvals, and expand international distribution networks are expected to maintain a competitive edge in this rapidly evolving market.

Stryker Corporation

Mo-Sci Corporation

Schott AG

BonAlive Biomaterials Ltd

NovaBone Products LLC

BioGlass International

Dentsply Sirona

VitroScaffold Inc.

Prosidyan Inc.

Noraker

The Orthopedic Bioactive Glass Market is increasingly influenced by innovations in material science, nanotechnology, and additive manufacturing, all of which are reshaping orthopedic implant development. One of the most significant technological advancements is the integration of nanostructured bioactive glass particles, which improve osteogenic activity and accelerate healing. These nano-scale materials exhibit enhanced surface reactivity, improving cell adhesion, proliferation, and differentiation for faster bone regeneration in trauma and spinal surgeries.

3D printing technology is another transformative force, allowing the fabrication of customized scaffolds and implants using bioactive glass composites. These implants offer patient-specific geometries and porosity that promote vascularization and structural integration. In addition, hybrid technologies combining bioactive glass with polymers or metals are enhancing mechanical strength while preserving bioactivity, enabling their use in load-bearing applications.

Advanced coating techniques such as plasma spraying and sol-gel deposition are being applied to titanium and PEEK implants, enhancing surface properties with bioactive glass layers for better osseointegration. AI-driven design tools are also streamlining implant modeling and surgical planning, reducing time-to-market for innovative orthopedic solutions. Collectively, these technologies are improving surgical precision, lowering infection risks, and enabling the development of next-generation orthopedic implants that meet complex clinical demands across various anatomical applications.

• In February 2024, BonAlive Biomaterials announced the successful clinical deployment of its new S53P4 bioactive glass granules for chronic osteomyelitis treatment, achieving a 90% infection-free rate in pilot studies involving over 120 patients across five hospitals.

• In August 2023, NovaBone Products launched its next-generation moldable putty formulation enriched with silicate-based bioactive glass for minimally invasive orthopedic surgeries, reducing intraoperative preparation time by 30% and enhancing graft stability.

• In November 2023, Schott AG expanded its specialty glass production line to include advanced borate-based bioactive glass for pediatric bone graft applications, introducing high-porosity variants tailored for rapid resorption and integration.

• In March 2024, Stryker Corporation integrated AI-guided planning software into its orthopedic surgery platforms, enabling real-time customization of bioactive glass implants and reducing pre-operative planning time by 40% in clinical settings.

The Orthopedic Bioactive Glass Market Report offers a comprehensive evaluation of the market’s structural landscape, highlighting key segments, regional patterns, and application pathways shaping demand across the globe. The report covers various product types, including silicate-based, phosphate-based, borate-based, and hybrid bioactive glass materials, each analyzed for its performance attributes, adoption trends, and clinical relevance.

From an application perspective, the report investigates use cases in bone grafting, spinal fusion, trauma repair, joint reconstruction, and craniomaxillofacial procedures. It also assesses integration within personalized medical interventions supported by AI-enhanced surgical planning and 3D-printed scaffold development. End-users analyzed include hospitals, specialty orthopedic clinics, and research institutions, each evaluated for adoption behavior, infrastructure capacity, and material sourcing dynamics.

Geographically, the report provides in-depth insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level data reflecting regional priorities, policy frameworks, and technological readiness. In addition, the study explores emerging markets with high orthopedic procedural demand and identifies innovation hubs driving bioactive glass research. Special attention is given to environmental considerations and sustainable manufacturing practices, including the development of bioresorbable and antimicrobial formulations. The report aims to assist decision-makers in identifying growth avenues, investment opportunities, and competitive positioning within this evolving and highly specialized biomaterials sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 106.8 Million |

|

Market Revenue in 2032 |

USD 133.21 Million |

|

CAGR (2025 - 2032) |

2.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kimberly-Clark Corporation, Essity AB, Unicharm Corporation, Domtar Corporation, Medline Industries, LP, Attends Healthcare Products Inc., TZMO SA, Abena A/S, HARTMANN Group, Ontex Group NV |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |