Reports

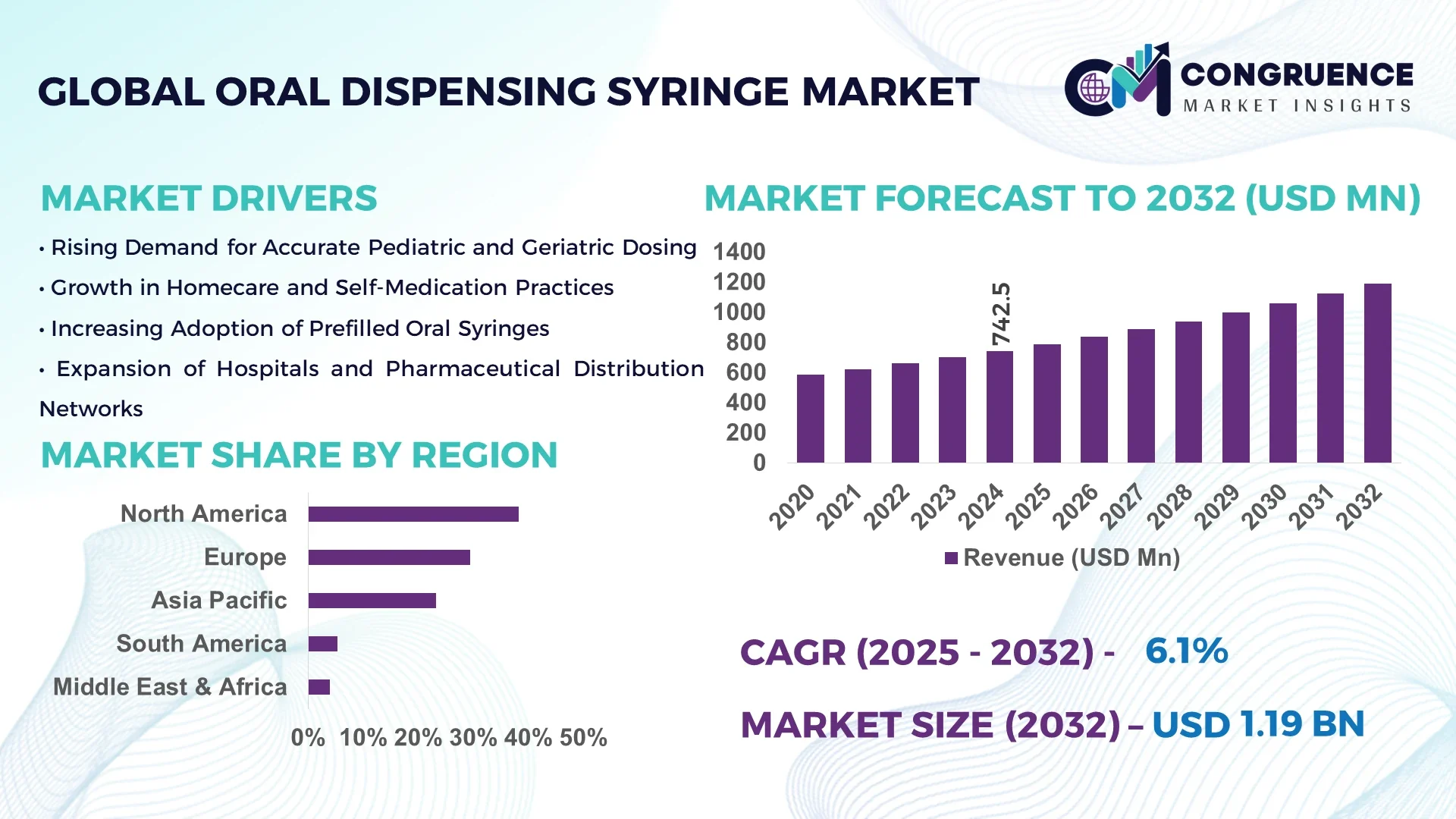

The Global Oral Dispensing Syringe Market was valued at USD 742.5 Million in 2024 and is anticipated to reach a value of USD 1,192.4 Million by 2032, expanding at a CAGR of 6.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is primarily driven by the rising prevalence of pediatric and geriatric patients requiring precise oral dosing, along with increasing hospital and homecare applications.

The United States holds a dominant position in the global oral dispensing syringe market, supported by advanced pharmaceutical manufacturing infrastructure, consistent regulatory approvals, and growing adoption of single-use medical disposables. The country hosts over 1,200 production facilities specializing in oral and parenteral syringe systems, with leading manufacturers investing more than USD 450 million in capacity expansion and automation between 2022 and 2024. Continuous technological upgrades, such as precision-molded polypropylene syringes and child-resistant dosing mechanisms, have accelerated domestic output by approximately 18% annually.

Market Size & Growth: Valued at USD 742.5 Million in 2024, projected to reach USD 1,192.4 Million by 2032, growing at a CAGR of 6.1%. Growth is fueled by rising patient safety standards and increasing demand for accurate medication dosing.

Top Growth Drivers: 38% increase in pediatric dosing applications, 27% improvement in dispensing accuracy, and 31% rise in home-based medical treatments.

Short-Term Forecast: By 2028, automation in syringe manufacturing is expected to improve operational efficiency by 22% and reduce product rejection rates by 18%.

Emerging Technologies: Adoption of smart oral syringes with dose tracking and bio-based polymer syringes with enhanced recyclability.

Regional Leaders: North America (USD 436 Million by 2032) emphasizes digital tracking syringes; Europe (USD 308 Million) focuses on eco-friendly materials; Asia Pacific (USD 292 Million) is driven by rapid healthcare infrastructure expansion.

Consumer/End-User Trends: Hospitals and pediatric clinics dominate demand, with over 65% of usage centered around safe, single-use medication delivery.

Pilot or Case Example: In 2024, a U.S. healthcare consortium achieved a 24% reduction in dosing errors through AI-based syringe calibration systems.

Competitive Landscape: Becton, Dickinson & Company leads with approximately 18% share, followed by Gerresheimer AG, Medline Industries, and Baxter International.

Regulatory & ESG Impact: New sustainability mandates require 40% recyclable plastic use in syringe manufacturing by 2030.

Investment & Funding Patterns: Over USD 520 Million invested globally in syringe automation and cleanroom manufacturing facilities since 2022.

Innovation & Future Outlook: Next-generation oral syringes integrating RFID tracking and precision volume indicators are expected to redefine quality standards and compliance by 2032.

The oral dispensing syringe market is witnessing robust adoption across pharmaceutical, nutraceutical, and homecare sectors. Advanced polymer innovations, patient-centric product designs, and stricter regulatory frameworks are strengthening quality compliance. Regional consumption is rising fastest in Asia Pacific due to improved healthcare infrastructure and local production initiatives, positioning the market for sustained, innovation-led growth.

The Oral Dispensing Syringe Market plays a pivotal strategic role in advancing safe, accurate, and patient-centric medication delivery systems globally. With increased emphasis on precision dosing and regulatory compliance, the market is evolving toward integrated, technology-driven solutions. Smart dispensing syringes equipped with digital dose indicators and tamper-proof seals are transforming clinical and homecare use cases. Comparative benchmarks show that AI-enabled dispensing mechanisms deliver 28% improvement in dosing accuracy compared to traditional manual syringes.

North America dominates in production volume, while Europe leads in adoption, with approximately 62% of hospitals in Western Europe standardizing oral syringe use for pediatric care. By 2028, automation in assembly and calibration processes is projected to reduce manufacturing costs by 17% and enhance traceability by 25%, driven by digital production management tools. Firms are increasingly aligning with ESG goals, committing to a 30% reduction in virgin plastic use by 2030 through material innovation and recycling initiatives.

In 2025, a major pharmaceutical company in Japan achieved a 21% reduction in plastic waste through the adoption of biodegradable oral syringe systems using bio-based polypropylene. The strategic pathways ahead center on sustainable design, digital transformation, and integration into broader pharmaceutical packaging ecosystems. As healthcare personalization accelerates, the Oral Dispensing Syringe Market will remain a cornerstone of compliance, safety, and sustainable healthcare delivery worldwide.

The Oral Dispensing Syringe Market is characterized by steady growth driven by innovations in pharmaceutical packaging, increasing emphasis on dosing accuracy, and evolving global health regulations. Demand is reinforced by pediatric, geriatric, and homecare applications requiring precise oral drug delivery. Technological advancements in low-friction plunger systems and tamper-evident designs are improving usability and patient safety. Additionally, government healthcare investments and expanding distribution networks across emerging markets continue to shape competitive dynamics and production scalability.

Rising pediatric and geriatric populations are significantly influencing the demand for accurate and safe oral drug administration. Over 34% of global hospital medication errors occur in pediatric units, creating urgency for precision dispensing tools. The integration of color-coded, graduated oral syringes ensures dosage accuracy, while hospitals are standardizing syringe-based oral dosing systems to minimize risk. Growth in home-based treatment, supported by smart dosage tracking and improved accessibility, continues to enhance market adoption globally.

Stringent plastic usage regulations and compliance costs are major restraints in the oral dispensing syringe market. Manufacturers face challenges transitioning from conventional polypropylene to recyclable or bio-based materials. The European Union’s directive requiring 25% recycled content by 2028 has increased R&D expenditures and testing cycles. Additionally, maintaining sterility and precision under new materials adds production complexity, raising costs by approximately 11–14% for smaller manufacturers and affecting supply chain efficiency.

The integration of digital and smart technologies presents vast opportunities for innovation in the oral dispensing syringe market. The incorporation of RFID tags, dose-tracking sensors, and cloud-linked data platforms enables enhanced traceability and patient adherence monitoring. Forecasts indicate that by 2027, nearly 45% of high-volume hospitals will adopt smart dispensing solutions. These advancements not only improve treatment accuracy but also open new pathways for pharmaceutical packaging partnerships and automated refill systems.

High capital investment in tooling, precision molding, and sterilization infrastructure remains a key challenge for manufacturers. Advanced cleanroom facilities and medical-grade molds cost 25–30% more than general-purpose setups. Moreover, ensuring microbial safety and regulatory validation under ISO 13485 standards adds additional certification time. This cost-intensive environment discourages smaller firms from entering the market, consolidating production among established players with integrated manufacturing capabilities.

Integration of Smart Dose-Monitoring Syringes: Advanced oral syringes embedded with digital dose-tracking chips have achieved a 29% improvement in dosage accuracy. Hospitals in North America are rapidly implementing these systems, with over 40% of pediatric wards transitioning to smart dispensing models by 2026.

Shift Toward Sustainable Materials: Manufacturers are increasingly adopting bio-based polypropylene and polyethylene materials, reducing carbon emissions by 22% per production cycle. Asia Pacific leads this transition, with 35% of new syringe lines now utilizing eco-friendly polymers.

Expansion of Automated Production Lines: Automation in syringe assembly and sterilization has enhanced production throughput by 31% and reduced labor dependency by 18%. European facilities report improved product consistency and reduced contamination risks due to fully robotic systems.

Rising Homecare and Telehealth Integration: With growing remote healthcare adoption, over 58% of oral syringe use now occurs in homecare settings. Integration with telehealth platforms enables patients to receive precise dosing instructions and monitoring support, contributing to improved medication adherence and reduced clinical revisits.

The Global Oral Dispensing Syringe Market is segmented based on type, application, and end-user categories, reflecting diverse demand patterns across healthcare, pharmaceutical, and homecare sectors. Among these, prefilled and reusable syringe types are gaining traction due to safety and convenience benefits, while hospitals and clinics remain the predominant end-users. Applications span pediatric dosing, geriatric medication administration, and chronic disease management, each emphasizing dosing precision and user safety. Increasing healthcare digitalization, growing patient preference for home-based care, and regulatory emphasis on single-use medical devices continue to define the market segmentation landscape, fostering innovation in design, material, and packaging integration.

Within the type segmentation of the Oral Dispensing Syringe Market, single-use oral syringes currently dominate, accounting for approximately 58% of global adoption. Their leadership is attributed to their sterility, ease of use, and regulatory compliance for one-time dosing in clinical and homecare settings. Multi-use (reusable) syringes represent around 22% of the market, primarily favored in institutional healthcare facilities where controlled cleaning processes ensure safety. However, prefilled oral dispensing syringes are emerging as the fastest-growing type, expanding at an estimated 6.8% CAGR, driven by increasing adoption in pediatric and geriatric medication where ready-to-administer formats reduce dosing errors and enhance compliance. Prefilled formats also support high-throughput pharmaceutical packaging lines and improve shelf-life consistency. Other types, including dose-measurement and safety-lock syringes, collectively account for 20% of total adoption. These variants are increasingly utilized for specialized formulations, including controlled medications and nutraceutical products.

Among applications, pediatric dosing leads the Oral Dispensing Syringe Market, representing approximately 46% of total adoption. This dominance is due to the necessity of accurate liquid dosing for children and the widespread integration of calibrated oral syringes in hospitals and pharmacies. Geriatric care follows with 28% share, supported by increasing chronic medication regimens and demand for simplified administration tools for patients with reduced dexterity. The fastest-growing application segment is home-based medication, expanding at an estimated 7.2% CAGR. Growth is supported by telehealth expansion, digital health monitoring tools, and rising patient preference for self-administered treatments. Other applications, including nutraceuticals and veterinary care, collectively contribute 26% of the overall market, serving specialized dosing and packaging requirements. In 2024, nearly 41% of households in developed economies reported using oral syringes for administering liquid vitamins or antibiotics. Furthermore, over 35% of telehealth service providers globally have integrated dosing verification modules compatible with oral syringe systems.

By end-user, hospitals and clinics are the leading segment, accounting for approximately 52% of the global market, due to standardized medication practices and strict compliance protocols for accurate dosing. Pharmaceutical manufacturers represent around 27%, utilizing oral syringes for pre-packaged liquid medications and patient trial kits. The fastest-growing end-user category is the homecare sector, with an estimated 6.9% CAGR, driven by the aging population, growth in chronic illness management, and digital monitoring tools enabling precise medication delivery at home. Other end-users, including nursing facilities, long-term care centers, and pharmacies, collectively hold 21% share, contributing significantly to retail-level and secondary dispensing applications. In 2024, over 39% of caregivers globally reported preferring oral syringes with safety caps for at-home dosing, while 48% of pharmacies in North America introduced calibrated oral syringes for pediatric antibiotic dispensation.

North America accounted for the largest market share at 38.2% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.6% between 2025 and 2032.

North America’s dominance is driven by the widespread adoption of precision dosing devices across pediatric and geriatric care, strong regulatory compliance, and presence of established pharmaceutical manufacturing infrastructure. Meanwhile, Asia Pacific’s rapid growth is attributed to the surging pharmaceutical production in countries like China and India, increasing adoption of patient-centric drug delivery systems, and rising healthcare access across emerging economies. Europe followed with around 27.4% share, supported by strict safety regulations and the shift toward eco-friendly medical plastics. South America and the Middle East & Africa collectively contributed 9.3%, highlighting untapped potential in expanding local healthcare infrastructure and public health programs.

North America captured approximately 38.2% of the global oral dispensing syringe market in 2024, with strong demand from the pharmaceutical, biotechnology, and home healthcare sectors. The U.S. and Canada are major contributors, supported by the FDA’s stringent patient safety standards and initiatives promoting accurate pediatric dosing. Rapid digital transformation in drug packaging and integration of barcoded syringes enhance traceability and dosage accuracy. Local players such as Becton, Dickinson and Company (BD) are innovating in color-coded and single-use syringe solutions to minimize medication errors. Regional consumer behavior is shaped by higher enterprise adoption across healthcare systems and a preference for convenient, ready-to-use drug delivery formats, particularly in outpatient and homecare settings.

Europe held a 27.4% share of the global market in 2024, with Germany, the United Kingdom, and France as leading contributors. The market is propelled by stringent European Medicines Agency (EMA) standards emphasizing safety, compliance, and environmentally sustainable materials in medical devices. The region has witnessed accelerated adoption of recyclable plastics and bio-based syringe barrels. Companies such as Henke-Sass, Wolf GmbH are investing in advanced polymer technologies to improve product durability and recyclability. Consumer behavior in Europe reflects strong demand for compliance-focused, child-safe designs and transparent dosing mechanisms. Regulatory pressure and the EU’s Green Deal initiatives continue to push manufacturers toward sustainable production and supply chain practices.

Asia-Pacific ranked as the fastest-growing regional market in 2024, accounting for nearly 20.6% of the global market volume. Countries such as China, India, and Japan dominate due to large-scale pharmaceutical manufacturing, rising pediatric healthcare investments, and increasing adoption of affordable oral drug delivery solutions. Growing infrastructure modernization and rapid medical device manufacturing in China and India have created large domestic supply bases. Local players like Nipro Corporation are expanding production capacities to meet escalating export demand. Regional consumer behavior shows strong preference for cost-efficient, disposable syringes supported by e-commerce distribution and government healthcare expansion programs.

South America represented approximately 5.3% of the global market share in 2024, with Brazil and Argentina emerging as primary growth hubs. The region benefits from expanding healthcare coverage, government incentives for localized production, and modernization of hospital infrastructure. Growing focus on pediatric medication safety and demand for standardized oral dosing devices are driving uptake. Local manufacturers are gradually adopting automated assembly lines for syringe production. For instance, Brazilian firms are collaborating with pharmaceutical distributors to meet national self-sufficiency goals. Consumer behavior emphasizes affordability and reliability, with demand tied to language-localized labeling and the need for clear dosage markings in multilingual markets.

The Middle East & Africa accounted for around 3.9% of the total market share in 2024, with UAE, Saudi Arabia, and South Africa leading regional demand. Growth is supported by national health modernization programs, the expansion of pharmaceutical logistics networks, and public investments in pediatric and chronic care infrastructure. Increasing local assembly of medical consumables and import substitution policies are strengthening the regional supply chain. Local players in the UAE are collaborating with hospitals to deploy calibrated dosing syringes in government health centers. Consumer behavior demonstrates rising awareness of precision dosing, supported by digital tracking tools and patient education programs.

United States – 32.8% Market Share: Driven by high pharmaceutical production capacity, strong FDA compliance standards, and widespread adoption in pediatric and geriatric care.

China – 14.6% Market Share: Supported by large-scale domestic syringe manufacturing, cost-efficient exports, and government-led healthcare expansion initiatives.

The Oral Dispensing Syringe market is moderately consolidated, with an estimated 20 – 25 globally active competitors, of which the top five players hold approximately 45% of the total market share. These leading companies have established strong market positioning through vertical integration, global manufacturing networks, and focused investments in precision-dosing technologies. Strategic initiatives include partnerships between device manufacturers and pharmaceutical packaging firms to develop calibrated dosing syringes for pediatric and geriatric use. Several firms have launched new prefilled oral syringe product lines featuring child-resistant safety caps and tamper-evident seals. Mergers and acquisitions have occurred as well—for example, a major player acquiring a specialty plastics division to secure high-precision polymer manufacturing. Innovation trends influencing the competitive environment include development of smart dosing syringes with RFID or Bluetooth dose-tracking, adoption of bio-based polymer materials to reduce environmental impact, and automated production lines to enhance throughput and reduce micro-defects. With the market driven by safety, accuracy, and regulatory compliance, companies that can offer turnkey solutions—combining design, single-use convenience, traceability and sustainability—are positioned to gain competitive advantage. Decision-makers should monitor product launches, alliance announcements, capacity expansions and patent filings as key indicators of competitive momentum.

Baxter International

Henke-Sass

Wolf GmbH

B. Braun Melsungen AG

Technological advancements are reshaping the Oral Dispensing Syringe market by introducing enhanced dosing precision, traceability, and material sustainability. Precision-molded polymer barrels now achieve dimensional tolerances of ±0.1 mm, enabling accurate measured volumes down to 0.1 mL increments. Smart syringes equipped with embedded RFID chips or Bluetooth sensors are enabling digital dose verification and linking to patient management systems—studies show over 30% of high-volume hospitals are piloting these devices for pediatric and chronic care dosing. Bio-based polypropylene and recyclable thermoplastics are increasingly adopted; manufacturers report achieving a 20% reduction in carbon-intensive input materials through new resin formulations. On the production side, fully automated assembly lines using robotics and machine-vision inspection now deliver throughput increases of 25–30% compared to legacy manual lines and reduce defect rates by over 15%. Injection-molding machine cycle times have been reduced by as much as 12% via hot-runner optimization and multi-cavity tooling. Digital manufacturing is gaining ground: closed-loop manufacturing systems integrate sensor data for real-time quality control, and cloud-based analytics track batch variance, enabling predictive maintenance of clean-room equipment. In addition, modular clean-room construction lets firms respond flexibly to regulatory clean-class changes and scale capacity faster in emerging markets. For decision-makers, the imperative is to invest in or partner for technology that offers dosing accuracy, traceability, sustainable materials, and production agility—all of which are becoming critical differentiators in the Oral Dispensing Syringe market.

In March 21, 2024 — BD increases U.S. syringe production. Becton, Dickinson and Company announced ramped domestic manufacturing of syringes at its Nebraska and Connecticut facilities to support U.S. healthcare needs, boosting on-shore capacity and supply continuity after regulatory safety communications. Source: www.bd.com

In 2023–2024 — Nipro expands syringe capacity (Münnerstadt & new building). Nipro PharmaPackaging reported a capacity increase of about 30% at its Münnerstadt prefillable-syringe plant and construction of a ~4,000 sqm building with additional forming and washing lines to increase bulk and sterile production during 2023–2024. Source: www.nipro-group.com

In April 11, 2024 — Baxter launches prefilled Regadenoson syringe in U.S. Baxter added a Regadenoson injection prefilled syringe (0.4 mg/5 mL) to its U.S. pharmaceuticals portfolio, expanding ready-to-use injectable options for pharmacologic stress testing and improving point-of-care preparation efficiency. Source: www.baxter.com

In September 2, 2024 — Gerresheimer introduces silicone-oil-free syringe systems. Gerresheimer announced silicone oil-free syringe systems for sensitive ophthalmic drugs (Gx RTF), enabling precise, reproducible administration of very small volumes and addressing compatibility concerns for advanced biologics. Source: www.gerresheimer.com

This report comprehensively covers the global Oral Dispensing Syringe market, analyzing segmentation by type (e.g., single-use, multi-use, prefilled, safety-lock), by application (pediatric dosing, geriatric administration, home-care medication, nutraceuticals, veterinary use), and by end-user (hospitals/clinics, pharmaceutical manufacturers, home-care providers, nursing/long-term-care facilities). Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights in major markets such as the United States, China, Germany, Brazil and India. The technology focus spans precision dosing systems, smart dosing syringes, bio-based polymer materials, and automated production lines. Industry focus areas include product innovation, regulatory developments, supply-chain dynamics, and sustainability/ESG interventions. Niche segments such as dose-tracking digital integrations, telehealth-compatible oral syringes, and subscription-based home-care dosing kits are also addressed. The scope aims to provide decision-makers with actionable intelligence on competitive strategies, capacity expansions, material innovations, end-user behavior and regional consumption patterns to support market entry, product development and investment planning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 742.5 Million |

| Market Revenue (2032) | USD 1,192.4 Million |

| CAGR (2025 – 2032) | 6.1 % |

| Base Year | 2024 |

| Forecast Period | 2025 – 2032 |

| Historic Period | 2020 – 2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Becton, Dickinson and Company, Gerresheimer AG, Medline Industries, Baxter International, Nipro Corporation, Henke-Sass, Wolf GmbH, B. Braun Melsungen AG |

| Customization & Pricing | Available on Request (10 % Customization Free) |