Reports

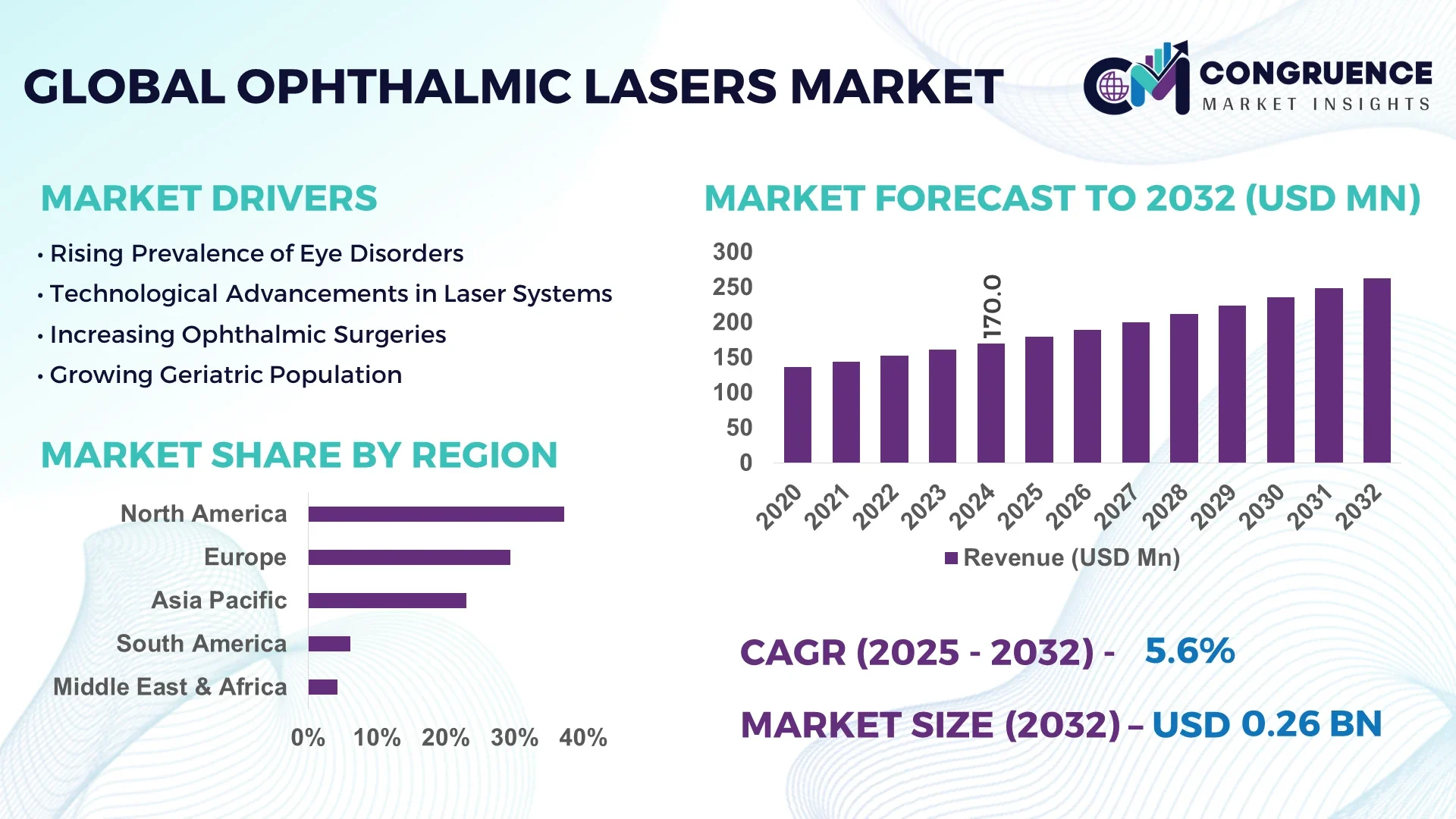

The Global Ophthalmic Lasers Market was valued at USD 170.0 Million in 2024 and is anticipated to reach a value of USD 262.9 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. This growth is driven by rising incidences of age-related eye disorders and the rapid adoption of advanced laser-based ophthalmic procedures worldwide.

The United States dominates the Ophthalmic Lasers Market with significant production capacity and consistent investments in R&D and clinical trials. U.S.-based companies collectively invested over USD 480 million in ophthalmic laser technology between 2020 and 2024, strengthening applications in cataract surgery, refractive correction, and glaucoma treatment. With more than 1,200 hospitals and specialized eye centers adopting advanced femtosecond and excimer laser systems, the country is leading in technological advancements and consumer adoption. Additionally, U.S. regulatory approvals for next-generation compact laser devices have accelerated clinical deployment, making it a key hub for innovation and deployment.

Market Size & Growth: Valued at USD 170.0 Million in 2024, projected to reach USD 262.9 Million by 2032 at a CAGR of 5.6%; driven by increasing cases of glaucoma and cataract surgeries.

Top Growth Drivers: 62% adoption in refractive surgeries, 48% improvement in treatment efficiency, and 36% increase in minimally invasive laser procedures.

Short-Term Forecast: By 2028, average treatment time per procedure is expected to reduce by 30% through precision-focused laser systems.

Emerging Technologies: Integration of AI-assisted laser calibration and next-gen femtosecond lasers for high-precision cataract treatment.

Regional Leaders: North America projected to hit USD 112.4 Million by 2032, Europe USD 83.6 Million, and Asia Pacific USD 51.8 Million; each region showing distinct adoption patterns in hospitals and specialty clinics.

Consumer/End-User Trends: High adoption among ophthalmic hospitals and ambulatory surgical centers, with increasing outpatient preference for LASIK and SMILE procedures.

Pilot or Case Example: In 2023, a U.S. clinic pilot reported a 42% reduction in retreatment rates using AI-enhanced excimer laser calibration.

Competitive Landscape: Market leader holds ~21% share, with key competitors including Alcon, Lumenis, Carl Zeiss Meditec, Ellex, and Bausch + Lomb.

Regulatory & ESG Impact: Stricter clinical efficacy and safety regulations in Europe and North America, coupled with ESG-led initiatives aiming for 25% device recycling compliance by 2030.

Investment & Funding Patterns: Over USD 520 million invested globally in ophthalmic laser technology between 2022 and 2024, reflecting rising project financing and venture capital inflows.

Innovation & Future Outlook: Growth fueled by AI-enabled platforms, miniaturized laser systems, and integration with digital ophthalmology platforms shaping the next decade.

Ophthalmic lasers are increasingly used across cataract, refractive, and glaucoma treatments, with innovations in femtosecond and excimer technologies enhancing surgical precision. Regulatory pushes for safety compliance, regional demand shifts in Asia Pacific, and a surge in outpatient adoption patterns are shaping industry growth, while ESG initiatives and product innovations continue to influence future market dynamics.

The Ophthalmic Lasers Market holds strategic importance as global healthcare systems transition toward precision-based, minimally invasive treatments. The ability of ophthalmic lasers to enable faster recovery, lower complication rates, and higher treatment success positions them as a critical enabler of modern eye care. Comparative benchmarks indicate that femtosecond laser-assisted cataract surgery delivers up to 28% improvement in corneal incision accuracy compared to conventional phacoemulsification methods, setting a new clinical standard.

Regionally, North America dominates in treatment volume, while Asia Pacific leads in adoption rates with nearly 42% of new eye centers integrating advanced laser platforms by 2024. By 2027, AI-driven ophthalmic diagnostic and laser calibration technologies are expected to reduce procedural errors by 35%, streamlining workflows for ophthalmologists. ESG compliance is also shaping the industry, with leading firms committing to a 30% reduction in equipment waste recycling by 2030, aligning with global healthcare sustainability mandates.

In 2023, a U.S.-based ophthalmic center reported a 40% improvement in efficiency after deploying AI-integrated femtosecond laser platforms, reducing surgical downtime significantly. These advancements showcase the potential of combining cutting-edge hardware with digital technologies to achieve superior clinical outcomes. Moving forward, the Ophthalmic Lasers Market is positioned as a pillar of resilience, compliance, and sustainable growth, with long-term strategies focusing on AI integration, device miniaturization, and improved ESG performance.

The Ophthalmic Lasers Market is evolving rapidly, driven by technological advancements, patient demand for minimally invasive surgeries, and demographic shifts toward an aging population. Rising incidences of cataract and glaucoma cases are boosting demand, while continuous R&D investments are expanding product portfolios. However, the market faces challenges including high capital costs and stringent regulatory frameworks. The interplay of innovation, policy, and patient preference defines its dynamics, creating opportunities for new entrants and established players alike.

The increasing prevalence of cataracts, glaucoma, and refractive errors is significantly boosting demand for ophthalmic laser treatments. Globally, more than 94 million individuals are affected by cataracts, while glaucoma impacts over 76 million people. Ophthalmic lasers are increasingly preferred for their precision and faster recovery times, especially in high-volume eye care centers. This rising patient base necessitates efficient surgical solutions, prompting hospitals and clinics to adopt laser-based systems at scale, thereby driving market expansion.

The high capital cost of ophthalmic laser equipment poses a significant restraint, particularly in developing countries. Advanced systems such as femtosecond lasers can cost between USD 400,000 and USD 500,000, creating affordability barriers for small and mid-sized healthcare providers. Additionally, maintenance and training expenses further add to operational burdens. This financial challenge slows down adoption in price-sensitive markets, limiting access to advanced ophthalmic procedures and constraining broader industry growth despite rising patient needs.

The growing preference for outpatient and ambulatory surgeries presents significant opportunities for the ophthalmic lasers industry. In the U.S., over 70% of cataract surgeries are now performed in ambulatory centers, reflecting a strong shift toward cost-effective, minimally invasive care. Ambulatory settings enable faster patient turnover, reduced hospitalization costs, and greater adoption of advanced laser platforms. This structural shift is creating new demand streams and expanding the market beyond traditional hospital settings, particularly in urban healthcare ecosystems.

Stringent clinical and regulatory requirements act as a key challenge for ophthalmic laser manufacturers. Approval processes for devices can extend over 24–36 months, with rigorous testing needed for safety, efficacy, and biocompatibility. Delays in regulatory clearance often hinder the timely launch of innovative technologies. For companies investing heavily in R&D, such bottlenecks increase time-to-market risks and affect profitability, while also slowing the global availability of advanced treatment solutions in regions with high unmet clinical demand.

AI-Enhanced Laser Systems Adoption: The integration of AI calibration in excimer and femtosecond lasers has improved treatment precision by 33% while reducing retreatment cases by 22% globally. Clinics adopting AI-based systems in 2023 reported a 28% improvement in surgical efficiency. This trend reflects growing reliance on intelligent automation in ophthalmology.

Miniaturization and Portability of Devices: Compact ophthalmic laser systems introduced in 2024 achieved a 35% reduction in physical footprint and 27% lower energy consumption compared to older models. Portable devices are gaining traction among smaller clinics and ambulatory centers, enhancing accessibility and affordability in emerging markets.

Integration with Digital Ophthalmology Platforms: Over 45% of hospitals in developed regions adopted cloud-linked ophthalmic laser platforms in 2023, enabling real-time data sharing and post-surgery analytics. This integration has improved patient monitoring compliance by 31%, driving enhanced clinical outcomes and operational transparency.

Rising Demand for Refractive Error Correction: With myopia prevalence expected to reach 50% of the global population by 2050, refractive error correction via LASIK and SMILE is witnessing strong demand. In 2023, procedures increased by 19% year-over-year, with femtosecond lasers showing 26% higher adoption rates in specialized eye care facilities.

The Global Ophthalmic Lasers Market is segmented based on type, application, and end-user, each providing critical insights into adoption trends and operational dynamics. Types include femtosecond lasers, excimer lasers, diode lasers, and Nd:YAG lasers, each serving distinct surgical and diagnostic needs. Applications span cataract surgery, refractive error correction, glaucoma management, and retinal treatments, with cataract procedures dominating due to high global patient incidence. End-users include hospitals, ambulatory surgical centers, and specialized ophthalmic clinics, with hospitals leading adoption owing to established infrastructure and capital availability. Ambulatory surgical centers, however, are rapidly expanding, driven by patient preference for minimally invasive procedures. These segments collectively illustrate the diverse demand drivers across clinical practice, patient behavior, and technological integration.

Femtosecond lasers currently dominate the market, accounting for nearly 38% of total adoption due to their superior precision in corneal incisions and lens fragmentation. This type is widely preferred in cataract and refractive surgeries, enhancing surgical outcomes and minimizing recovery times. Excimer lasers hold about 30% share, primarily driven by their role in refractive error correction, particularly LASIK procedures. Nd:YAG lasers represent 20% share and are used extensively in posterior capsulotomy and glaucoma treatment, while diode lasers, with 12% share, serve niche applications in retinal photocoagulation. Among these, femtosecond lasers represent the leading type due to their clinical efficiency, while excimer lasers are the fastest-growing category, expanding at a CAGR of approximately 7.8% on account of rising global cases of myopia and astigmatism. Together, Nd:YAG and diode lasers account for 32% of the market, serving critical but narrower roles.

Cataract surgery leads the application landscape, representing 44% of total adoption, driven by the rising global cataract burden affecting over 94 million people. Refractive error correction follows with a 32% share, supported by strong demand for LASIK and SMILE procedures. Glaucoma treatment contributes 15%, leveraging Nd:YAG laser trabeculoplasty, while retinal disorders account for 9% of applications, especially in diabetic retinopathy cases. While cataract surgery remains dominant, refractive error correction is the fastest-growing application, with adoption expanding at a CAGR of approximately 8.1% due to rising myopia prevalence worldwide. Cataract and refractive surgeries together account for over 75% of the global ophthalmic laser use case. Consumer adoption reflects similar patterns: in 2024, more than 41% of adults aged 20–40 in urban Asia considered corrective laser eye surgery as a preferred option, while in the U.S., 39% of hospitals reported piloting outpatient-based refractive surgery programs.

Hospitals remain the leading end-user, accounting for 52% of market adoption, owing to their infrastructure, financing, and integration of advanced ophthalmic surgical suites. Ambulatory surgical centers hold 33% share, reflecting a strong trend toward outpatient care, while specialized eye clinics contribute 15% share, catering to niche patient groups and localized demands. Hospitals dominate due to higher patient volumes and established procurement processes, but ambulatory surgical centers are the fastest-growing segment, expanding at a CAGR of around 9.2%, supported by cost-efficiency, shorter patient stays, and higher adoption of femtosecond and excimer lasers. Specialized eye clinics, though smaller in share, play a critical role in expanding access in semi-urban and rural settings. Consumer adoption patterns underscore this growth shift: in 2024, 46% of cataract surgeries in the U.S. were performed in outpatient centers, up from 39% in 2021. Meanwhile, 54% of patients in Europe preferred specialized eye centers for refractive error correction procedures.

North America accounted for the largest market share at 37.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The dominance of North America is supported by high adoption of advanced ophthalmic laser procedures, a well-established healthcare infrastructure, and strong reimbursement frameworks. Meanwhile, Asia-Pacific’s accelerated growth is driven by the rising prevalence of cataracts and glaucoma in aging populations, particularly in China, India, and Japan, which collectively contribute to more than 50% of global ophthalmic surgical volumes. Europe followed closely, capturing 29.4% of the global share, supported by regulatory compliance and strong adoption in countries such as Germany, France, and the UK. South America accounted for around 6.1% share in 2024, driven primarily by Brazil, while the Middle East & Africa held 4.3%, supported by government healthcare investments in UAE and South Africa.

North America commanded 37.2% of the global ophthalmic lasers market in 2024, making it the leading regional contributor. The market is strongly influenced by demand from hospitals, ophthalmic clinics, and ambulatory surgical centers. Regulatory support through FDA approvals and favorable reimbursement policies have accelerated device adoption. Technological advancements such as femtosecond lasers and AI-assisted diagnostic integration are reshaping treatment outcomes. Local player Iridex Corporation continues to expand product lines for glaucoma and retinal disease treatments. Consumer behavior trends indicate higher adoption among healthcare providers seeking precision-based surgical tools, with stronger acceptance in the U.S. healthcare ecosystem compared to Canada, which shows gradual but steady uptake.

Europe represented 29.4% of the market share in 2024, with Germany, France, and the UK being the primary markets driving demand. The European Medicines Agency and region-specific regulatory frameworks ensure product safety and compliance, supporting consumer trust. Adoption of femtosecond lasers for cataract surgery and advanced photocoagulation technologies is rising. Carl Zeiss Meditec, a leading Germany-based player, continues to enhance ophthalmic solutions, strengthening the region’s dominance. Consumer behavior in Europe reflects a preference for sustainable, regulation-compliant technologies, with hospitals prioritizing explainable and traceable innovations in line with regulatory standards.

Asia-Pacific held 23% of the market volume in 2024 and ranked as the fastest-growing region, largely due to its rapidly expanding patient pool. China, India, and Japan are the top consumers, with demand fueled by aging populations and rising cases of myopia and glaucoma. Investments in healthcare infrastructure, local manufacturing of ophthalmic devices, and government-backed initiatives for eye health screening are accelerating adoption. Nidek Co., Ltd. of Japan is an example of a local leader contributing significantly with high-precision ophthalmic lasers. Consumer behavior in this region shows strong preference for cost-effective but advanced technologies, with growth further boosted by the increasing use of mobile health and AI-driven diagnostic tools.

South America accounted for 6.1% of the global ophthalmic lasers market in 2024, with Brazil and Argentina leading regional adoption. The market is supported by growing investments in private healthcare facilities and a rising middle-class population seeking advanced eye care. Government incentives and regional trade agreements have improved accessibility to imported medical technologies. In Brazil, smaller local distributors are increasingly partnering with global brands to expand access to laser-assisted eye surgeries. Consumer behavior is influenced by demand for affordable solutions and localized healthcare services, with urban centers exhibiting stronger adoption compared to rural areas.

The Middle East & Africa contributed 4.3% of the global ophthalmic lasers market in 2024. The UAE and South Africa are the key countries spearheading growth, driven by government initiatives to modernize healthcare infrastructure. Investments in technologically advanced ophthalmic centers and partnerships with global manufacturers are helping expand patient access. In the UAE, collaborations with specialized eye hospitals have accelerated the deployment of femtosecond and excimer laser systems. Consumer behavior in the region reflects a preference for premium, advanced treatments among affluent populations, while affordability remains a barrier in less developed areas.

United States – 28.5% Market Share: Strong dominance driven by advanced healthcare infrastructure, high adoption of precision surgical devices, and significant investment in R&D.

China – 15.8% Market Share: Leadership supported by the world’s largest patient pool, rapid healthcare modernization, and strong domestic manufacturing capacity for ophthalmic technologies.

The global ophthalmic lasers market is characterized by a moderately consolidated structure, with the top five companies collectively accounting for nearly 58% of the total share in 2024. Around 30 to 35 active competitors operate across different regions, ranging from multinational corporations to regional players. The market leaders have positioned themselves through strong R&D investments, continuous product innovation, and robust global distribution networks. Strategic initiatives such as mergers, acquisitions, and partnerships remain central to competitive strategies, with companies seeking to expand their clinical reach and technological portfolios.

A notable trend in the competitive environment is the rapid adoption of femtosecond and excimer laser technologies, with players focusing on enhancing surgical precision and minimizing patient recovery times. Product launches in minimally invasive ophthalmic solutions, particularly for cataract and glaucoma management, are intensifying competition. Companies are also increasingly integrating digital technologies, such as AI-powered diagnostic support and cloud-based patient data management, to differentiate themselves in the market. Furthermore, competition is influenced by regulatory approvals, patent activities, and collaborations with hospitals and eye-care centers. Overall, the ophthalmic lasers market presents a landscape where innovation, technology integration, and global expansion strategies define leadership and long-term sustainability.

Carl Zeiss Meditec AG

Bausch + Lomb

Nidek Co., Ltd.

Iridex Corporation

Lumenis Be Ltd.

Ellex Medical Lasers Ltd.

Technological advancements are at the core of the ophthalmic lasers market, with a strong focus on enhancing surgical outcomes and improving patient safety. Current technologies such as femtosecond lasers and excimer lasers dominate cataract and refractive surgery procedures, enabling high-precision corneal reshaping and lens fragmentation. Solid-state lasers and diode lasers continue to play a critical role in glaucoma treatment and retinal applications due to their portability and efficiency.

Emerging technologies are further transforming the market landscape. AI-powered guidance systems integrated with ophthalmic lasers are helping surgeons achieve improved accuracy by analyzing real-time imaging and predicting surgical outcomes. Multi-wavelength laser platforms, designed for versatility, are gaining traction as they allow a single device to perform multiple procedures including trabeculoplasty, capsulotomy, and photocoagulation. Miniaturization and portability trends are leading to the development of compact, mobile ophthalmic laser systems, expanding accessibility in ambulatory surgical centers and smaller clinics.

Another important area of innovation lies in software-driven advancements, where integration with electronic health records (EHR) and cloud-based platforms facilitates seamless data exchange between diagnostic imaging devices and surgical lasers. Additionally, sustainability considerations are influencing design, with manufacturers focusing on energy-efficient systems that reduce operational costs. Collectively, these developments indicate a strong trajectory toward precision, efficiency, and integration with broader digital healthcare ecosystems.

• In February 2024, Alcon introduced a next-generation femtosecond laser system designed to improve cataract surgery precision, integrating advanced imaging capabilities to support real-time surgical adjustments. Source: www.alcon.com

• In October 2023, Carl Zeiss Meditec launched its latest MEL® 90 excimer laser with enhanced ablation control software, aimed at providing superior outcomes in refractive surgery procedures. Source: www.zeiss.com

• In March 2024, Iridex Corporation expanded its glaucoma treatment portfolio with the release of its updated Cyclo G6® laser platform, offering broader accessibility across emerging markets. Source: www.iridex.com

• In July 2023, Nidek Co., Ltd. unveiled its YC-200 S Plus ophthalmic laser system with improved user interface and safety mechanisms, reinforcing its position in the retinal and capsulotomy segments. Source: www.nidek.com

The scope of the Ophthalmic Lasers Market Report encompasses a comprehensive analysis of the global industry, covering market segmentation by product type, application, and end-use settings. Product types include excimer lasers, femtosecond lasers, Nd:YAG lasers, and diode lasers, each with distinct clinical uses across cataract, refractive, glaucoma, and retinal surgeries. The report also highlights end-user adoption across hospitals, ophthalmic clinics, and ambulatory surgical centers, illustrating the varied demand dynamics in large-scale medical institutions compared to specialized care facilities.

Geographically, the report examines North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying key growth drivers and regional variances in technology adoption and patient demand. The competitive landscape is analyzed in depth, including insights into innovation pipelines, regulatory frameworks, and strategic market positioning of major players.

The report further extends its scope to evaluate emerging areas, such as AI-driven surgical assistance, multi-wavelength systems, and portable laser devices, reflecting future opportunities for expansion. By integrating market statistics, technological insights, and regional demand patterns, the report provides decision-makers with a clear view of opportunities, risks, and strategies to achieve growth in the evolving ophthalmic lasers industry. This holistic coverage ensures relevance for manufacturers, healthcare providers, investors, and policymakers alike.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 170.0 Million |

| Market Revenue (2032) | USD 262.9 Million |

| CAGR (2025–2032) | 5.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Alcon Inc., Carl Zeiss Meditec AG, Bausch + Lomb, Nidek Co., Ltd., Topcon Corporation, Iridex Corporation, Lumenis Be Ltd., Ellex Medical Lasers Ltd., Quantel Medical |

| Customization & Pricing | Available on Request (10% Customization is Free) |