Reports

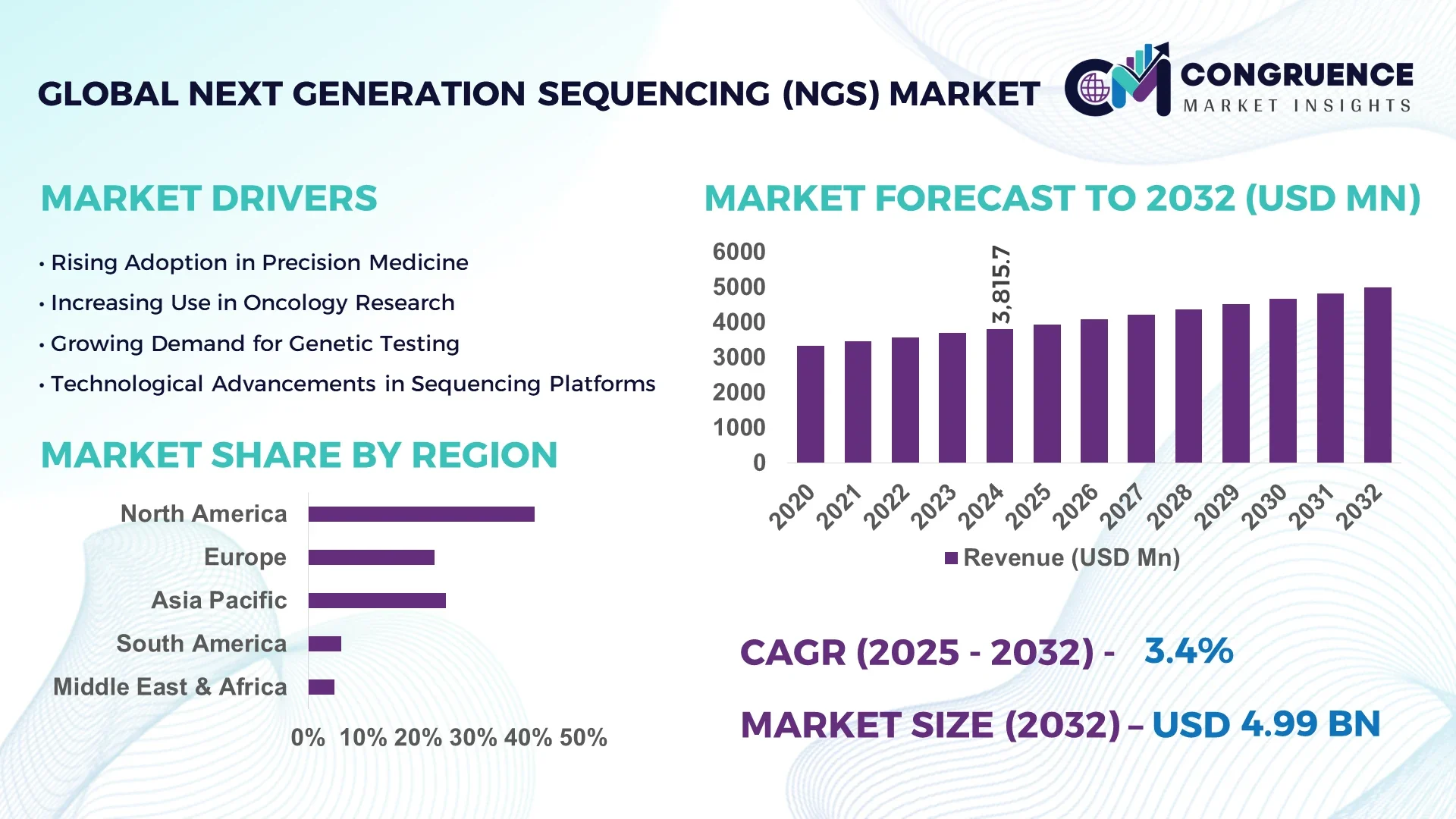

The Global Next Generation Sequencing (NGS) Market was valued at USD 3815.66 Million in 2024 and is anticipated to reach a value of USD 4985.79 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032.

The United States leads the global NGS market with cutting-edge genomics infrastructure, multi-billion-dollar R&D investments, and advanced integration of sequencing technologies into clinical diagnostics, agricultural genomics, and precision medicine platforms.

The Next Generation Sequencing (NGS) market is undergoing a dynamic shift driven by breakthroughs in high-throughput sequencing, miniaturization, and cost reduction of NGS platforms. Prominent demand arises from oncology, genetic disorders, infectious disease diagnostics, and agricultural genomics. Clinical laboratories and biopharmaceutical firms are extensively deploying NGS solutions to improve diagnostic accuracy and therapeutic decision-making. Technological innovations like single-cell sequencing, nanopore sequencing, and long-read sequencing are accelerating the transition to personalized medicine. Increasing regulatory support for genetic testing in Europe and Asia-Pacific is further amplifying market expansion. Meanwhile, Asia-Pacific is witnessing increased adoption of NGS systems due to rising government genomics programs and healthcare infrastructure upgrades. Favorable economic and regulatory frameworks in emerging economies are boosting the regional consumption of NGS solutions. The future outlook of the Next Generation Sequencing (NGS) market indicates a growing convergence of bioinformatics, cloud-based data platforms, and automation, which are expected to enhance operational scalability and analytical capabilities across clinical, research, and agricultural sectors.

Artificial Intelligence is profoundly reshaping the Next Generation Sequencing (NGS) Market by automating and optimizing complex bioinformatics pipelines, accelerating genomic data interpretation, and improving diagnostic workflows. AI-driven algorithms are being integrated into NGS systems to streamline raw data processing, reduce turnaround times, and identify genetic variants with greater precision. Machine learning and deep learning models are also enabling predictive analytics in oncology, aiding in the early detection of genetic mutations and treatment stratification. This has led to enhanced clinical utility and real-time insights into patient genomics.

AI’s impact extends to genomic data management, where natural language processing and neural networks are being utilized to analyze unstructured genomic datasets more effectively. Pharmaceutical companies are using AI-enhanced NGS platforms to fast-track drug discovery, particularly in rare diseases and immunotherapy development. In addition, AI-powered robotic systems are now handling sample preparation, sequencing, and post-sequencing analysis, significantly reducing human error and labor costs. As the volume of sequencing data grows exponentially, AI is becoming indispensable in interpreting large-scale genomic datasets, making the Next Generation Sequencing (NGS) Market more agile and responsive to evolving healthcare needs. These advancements are fostering innovation across multiple verticals including clinical diagnostics, agrigenomics, and environmental genomics, strengthening AI’s position as a critical enabler in the NGS landscape.

“In March 2024, NVIDIA collaborated with DNAnexus to deploy AI-powered models that reduced whole genome sequencing analysis time from 10 hours to under 45 minutes, enabling faster clinical decisions for rare genetic disease diagnostics.”

The Next Generation Sequencing (NGS) market is evolving rapidly, driven by advancements in genomics, precision medicine, and high-throughput sequencing technologies. Increasing demand for rapid and accurate genetic testing in clinical diagnostics, oncology, and infectious disease detection is fueling adoption across healthcare and research institutions. Continuous innovation in sequencing platforms, enhanced data analytics tools, and automation are enabling wider access to NGS applications. Governments and private entities are investing heavily in genomics infrastructure and national sequencing programs, further stimulating market growth. The integration of cloud-based solutions for real-time data analysis and storage is reshaping operational frameworks, while the shift toward personalized medicine is solidifying the NGS market's central role in future healthcare ecosystems.

The expansion of NGS in clinical settings, especially oncology and rare disease diagnostics, is a major driver for market growth. NGS allows for comprehensive tumor profiling, enabling oncologists to identify actionable mutations for targeted therapies and immunotherapies. For example, liquid biopsies powered by NGS are offering non-invasive alternatives for cancer detection and monitoring, which improves patient outcomes and supports early intervention strategies. Additionally, its use in diagnosing rare genetic conditions is accelerating due to its high sensitivity and capability to sequence multiple genes simultaneously. Hospitals and clinical labs are increasingly adopting NGS-based diagnostic kits, with robust pipelines being developed for inherited disorders, prenatal testing, and pharmacogenomics.

Despite the advancements, the high costs associated with acquiring and maintaining NGS platforms act as a significant restraint. Setting up a sequencing facility involves substantial investment in infrastructure, advanced instrumentation, and skilled personnel. Moreover, recurring expenses related to consumables, reagents, software licensing, and equipment calibration further add to the financial burden, particularly for small- and mid-sized laboratories. These cost factors restrict the adoption of NGS technologies in resource-limited settings and developing countries. Even with the declining cost per genome, the total operational expenditure remains a limiting factor for widespread market penetration in non-academic environments.

Government-funded initiatives and national genomic strategies are creating new opportunities within the Next Generation Sequencing (NGS) market. Countries like the UK, China, and India have launched extensive genomics programs aimed at mapping genetic diversity, improving population health, and integrating genomics into routine clinical care. These programs are backed by significant funding and infrastructure support, which in turn encourages the development of local sequencing capabilities, partnerships with biotech firms, and academic collaborations. As governments prioritize precision medicine, NGS is gaining prominence in public healthcare systems, opening doors for broader implementation across population screening, chronic disease prediction, and pharmacogenomic research.

The massive volume of data generated by NGS poses considerable challenges in storage, analysis, and interpretation. Accurate identification of clinically relevant variants requires advanced bioinformatics pipelines, which are often complex and resource-intensive. Many clinical laboratories lack the in-house computational infrastructure or trained personnel to handle NGS data efficiently, resulting in delays or inaccuracies. Moreover, there is a lack of standardized guidelines for variant annotation, filtering, and clinical reporting, which complicates decision-making for healthcare providers. Addressing these bioinformatics hurdles is critical to ensuring the reliability and reproducibility of NGS-based diagnostics and therapeutics.

• Expansion of Portable and Real-Time Sequencing Devices: Handheld and benchtop sequencing devices are becoming increasingly popular due to their flexibility and fast turnaround times. Devices like Oxford Nanopore’s MinION are now widely used in field research and point-of-care diagnostics. These portable systems enable real-time sequencing in remote or clinical settings, allowing for quicker decision-making in infectious disease surveillance, food safety, and outbreak tracking. Their adoption is particularly increasing across Asia-Pacific and Latin America, where infrastructure constraints limit access to central laboratories.

• Integration of NGS with Companion Diagnostics: The combination of NGS with companion diagnostics is transforming treatment personalization. In oncology, NGS-based tests are now guiding targeted therapies by identifying mutations in genes such as EGFR, BRCA, and ALK. The U.S. and European regulatory bodies have approved multiple NGS-based companion diagnostic tools, which are now standard in cancer care. This trend is driving demand for high-throughput and accurate sequencing solutions integrated within therapeutic development pipelines.

• Surge in Single-Cell Sequencing Adoption: Single-cell sequencing has gained traction due to its ability to analyze cellular heterogeneity at unprecedented resolution. This technology is being used extensively in immunology, neuroscience, and developmental biology to identify unique cell populations and track disease progression. Research institutions and biopharma companies are investing in platforms that enable simultaneous transcriptomic, epigenomic, and genomic profiling from individual cells, creating a high-demand segment within the NGS market.

• Growth of AI-Powered NGS Data Interpretation Platforms: AI and machine learning technologies are increasingly being incorporated into NGS data analysis to enhance accuracy and reduce processing time. Platforms equipped with AI algorithms are automating tasks like variant calling, annotation, and clinical interpretation. This trend is accelerating clinical adoption by minimizing manual errors and reducing time from sequencing to actionable insights. Cloud-based AI solutions are also enabling scalable, remote, and collaborative genomics research across multi-institutional settings.

The Next Generation Sequencing (NGS) market is segmented based on type, application, and end-user, each influencing the market’s structure and evolution. Product segmentation includes whole genome sequencing, targeted sequencing, whole exome sequencing, and RNA sequencing, with targeted and whole genome solutions leading in clinical and research settings. Application-based segmentation reveals significant uptake in diagnostics, drug discovery, agriculture, and personalized medicine. Diagnostic applications remain dominant due to the demand for precise genetic testing in oncology and rare disease detection. End-user segmentation shows key demand from academic institutions, hospitals, biotechnology firms, and contract research organizations. While academic research leads in volume usage, clinical and pharmaceutical applications are scaling up faster due to advances in precision medicine and increasing healthcare investments.

Whole genome sequencing (WGS) holds the lead within the product type segment due to its comprehensive data output and widespread usage in both research and clinical applications. WGS allows researchers to analyze complete DNA sequences, making it essential for discovering novel genes and complex mutations. Targeted sequencing is the fastest-growing type, propelled by its cost-efficiency and high sensitivity in identifying known mutations, especially in oncology and hereditary disease panels. Whole exome sequencing also retains a solid share, primarily used in clinical diagnostics and rare disease detection due to its focus on protein-coding regions. RNA sequencing continues to gain traction in gene expression profiling and transcriptome studies, particularly in cancer biology and drug discovery. Each sequencing type serves distinct use cases across varied applications, contributing to a balanced demand profile in the Next Generation Sequencing (NGS) market.

Clinical diagnostics stands as the leading application within the NGS market, driven by growing reliance on genetic sequencing for cancer profiling, rare disease identification, and prenatal testing. Hospitals and diagnostic labs are rapidly integrating NGS into routine clinical workflows, particularly for actionable genetic insights. Drug discovery is emerging as the fastest-growing application, with pharmaceutical companies leveraging NGS to identify drug targets, understand disease mechanisms, and stratify patients during clinical trials. Agricultural genomics, although smaller in comparison, plays a critical role in crop trait selection and livestock improvement. Additionally, microbiome research and environmental sequencing are niche but expanding applications contributing to the broader adoption of NGS technologies across diverse sectors.

Academic and research institutions are the primary end-users in the NGS market due to their historical reliance on sequencing technologies for basic and translational research. These institutions invest heavily in sequencing platforms for genomics, transcriptomics, and evolutionary biology. However, hospitals and clinical diagnostic laboratories represent the fastest-growing end-user category, with increasing utilization of NGS in patient care and disease management. The rise of personalized medicine and regulatory approvals for NGS-based tests are accelerating adoption in healthcare settings. Biotechnology and pharmaceutical companies also play a significant role, especially in research and development of targeted therapies. Contract research organizations are steadily contributing to market dynamics by offering outsourced sequencing services to reduce time and operational costs for smaller biotech firms.

North America accounted for the largest market share at 41.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.9% between 2025 and 2032.

The dominance of North America stems from its extensive deployment of NGS technologies in clinical diagnostics, research genomics, and pharmaceutical applications. Meanwhile, Asia-Pacific's rapid development is fueled by strong government investments in genomics, increasing demand for personalized healthcare, and expanding genomic research infrastructure in China, India, and Japan.

Globally, the Next Generation Sequencing (NGS) market is experiencing technological convergence and cross-sector adoption. Widespread implementation in oncology, microbiology, infectious disease diagnostics, and pharmacogenomics is transforming healthcare systems across regions. Nations are launching large-scale population genomics initiatives, fostering collaborations among biotech firms, academic institutions, and healthcare providers. Additionally, the miniaturization of sequencing platforms and the integration of AI-powered interpretation tools are accelerating the market's expansion into point-of-care and remote diagnostics. Regional consumption is also influenced by regulatory environments, healthcare digitization, and accessibility to cloud-based genomic data services.

Precision Genomics Driving Innovation in Advanced Healthcare Systems

Holding a 41.2% share of the global market in 2024, this region leads due to its highly integrated genomic research ecosystem and expansive clinical adoption. The biotechnology and pharmaceutical industries are the principal demand drivers, utilizing NGS for cancer diagnostics, rare disease detection, and drug development. Regulatory agencies have approved multiple NGS-based tests, accelerating clinical integration. Government-supported projects such as population genomics programs and partnerships with private genomics labs are boosting market maturity. Technological advances include widespread use of AI-powered bioinformatics platforms, robotic sequencing automation, and cloud-based genomic data solutions, enhancing scalability and reducing analysis time in clinical workflows.

Regulatory-Driven Expansion of Clinical Genomics and Research

This region accounted for 27.6% of the global Next Generation Sequencing (NGS) market in 2024, led by Germany, the United Kingdom, and France. The healthcare sector's focus on precision medicine is fueling adoption in hospitals and diagnostic laboratories. The European Medicines Agency and national regulatory bodies are actively supporting NGS-based diagnostic approvals and standardization efforts. Sustainability goals have spurred investment in energy-efficient sequencing platforms and decentralized testing infrastructure. Technological adoption is strong, with next-gen AI-assisted sequencing solutions being used for faster diagnostics and research across major clinical and academic institutions.

Accelerated Genomic Adoption through Government-Backed Infrastructure Programs

Asia-Pacific holds 19.8% of the market volume in 2024, ranking as the fastest-growing region. China, Japan, and India are driving regional consumption through national genome initiatives, growing biotech ecosystems, and investments in healthcare digitization. Local manufacturers are entering the NGS space, boosting affordability and access. Urban research hubs such as Beijing, Bengaluru, and Tokyo are fostering innovation in sequencing technologies and AI-based data analytics. Increased funding for hospital genomics infrastructure and academic research partnerships are reshaping the market landscape, allowing for high-throughput testing, personalized medicine, and real-time infectious disease surveillance.

Genomic Healthcare Expansion Supported by Regional Research Networks

In 2024, this region contributed approximately 6.3% of the global Next Generation Sequencing (NGS) market, led by Brazil and Argentina. Government-backed healthcare modernization initiatives and genomic medicine programs are encouraging NGS adoption. Brazil has become a central hub for research-based sequencing, particularly in cancer genomics and agricultural biotechnology. Infrastructure development in diagnostic centers and regional collaborations with international biotech firms are driving clinical applications. Trade policies that support laboratory equipment imports and favorable regulatory frameworks are supporting the broader integration of NGS across healthcare, environmental, and food safety sectors.

Digital Health Strategies and Genomic Policy Frameworks Fueling Growth

This region contributed 5.1% to the global Next Generation Sequencing (NGS) market in 2024, with the UAE and South Africa as the key growth contributors. National genomics programs are being integrated into broader digital health strategies, especially in population health monitoring and hereditary disease screening. The adoption of NGS is growing in university hospitals and research centers equipped with next-gen sequencing systems. Technological modernization includes AI-assisted variant analysis and integration of cloud-based data repositories. Regional governments are establishing public-private partnerships and entering trade agreements to facilitate access to sequencing platforms and skilled genomic labor.

United States – 39.8% market share

Strong end-user demand from clinical, academic, and pharmaceutical sectors supported by regulatory acceleration and national genomics initiatives.

China – 13.7% market share

High production capacity, expanding hospital adoption, and significant public investment in domestic genomic research and sequencing infrastructure.

The competitive environment in the Next Generation Sequencing (NGS) market is characterized by innovation-driven rivalry, with over 60 active players globally. Key companies are competing across product differentiation, technological integration, scalability, and application-specific solutions. Market leaders are focusing on enhancing sequencing accuracy, speed, and affordability through AI integration, nanopore sequencing, and long-read platforms. The introduction of portable and real-time sequencing devices has intensified competition, especially among players targeting point-of-care and decentralized testing segments.

Strategic partnerships between sequencing technology providers and biopharmaceutical companies are increasing, aimed at co-developing precision medicine and companion diagnostics. Mergers and acquisitions continue to reshape the landscape, with larger firms acquiring niche players to strengthen genomic analytics and bioinformatics capabilities. Companies are also expanding their presence in high-growth regions such as Asia-Pacific and Latin America by establishing local manufacturing and service hubs. Product launch cycles are shortening, with rapid upgrades in software and hardware to meet evolving end-user requirements. Intellectual property protection, software innovation, and regulatory approvals remain critical competitive levers. The focus on end-to-end NGS solutions—ranging from sample preparation to cloud-based data analysis—is redefining leadership and operational advantage within the NGS market.

Illumina Inc.

Thermo Fisher Scientific

Oxford Nanopore Technologies

Pacific Biosciences

Agilent Technologies

BGI Genomics

QIAGEN N.V.

PerkinElmer Inc.

Roche Sequencing

Bio-Rad Laboratories

The Next Generation Sequencing (NGS) market is shaped by rapid technological advancement, with continuous innovation in sequencing platforms, bioinformatics, and automation. Key developments include the adoption of long-read sequencing technologies, such as those used by Pacific Biosciences and Oxford Nanopore, which provide greater accuracy in genome assembly and structural variant detection. These platforms are particularly valuable in applications involving complex genomic regions and rare genetic disorders.

Miniaturized and portable sequencing systems have entered clinical and field environments, expanding real-time and point-of-care genomic capabilities. Devices like nanopore sequencers offer rapid turnaround times and direct RNA sequencing, eliminating the need for amplification and enabling epigenetic analysis. AI integration into bioinformatics pipelines is another major trend, with deep learning models enhancing variant calling, annotation, and genotype-to-phenotype prediction.

Cloud-based sequencing data management platforms now enable scalable, secure, and collaborative analysis environments, significantly reducing the burden on local infrastructure. Furthermore, automated robotic sample preparation and library construction systems are improving reproducibility and throughput, especially in clinical labs and high-volume research centers. There is also increasing adoption of hybrid sequencing methods combining short-read and long-read technologies to optimize both depth and length of coverage. Together, these technological advancements are redefining the efficiency, accessibility, and clinical utility of NGS across global markets.

• In March 2024, Thermo Fisher Scientific launched the Ion Torrent Genexus System for clinical oncology, offering an integrated workflow from sample to report in just 24 hours, significantly reducing diagnostic turnaround time for hospitals and labs.

• In December 2023, Illumina introduced the NovaSeq X Plus system with a capacity of 20 billion reads per run, enabling large-scale population genomics projects with improved efficiency and cost reduction per genome.

• In February 2024, QIAGEN unveiled its new QIAseq Targeted DNA Pro panels, designed to improve coverage uniformity in low-input samples, with applications in cancer diagnostics and hereditary disease testing.

• In August 2023, Oxford Nanopore announced the commercial availability of its PromethION 2 Solo device, a compact sequencer supporting real-time, long-read sequencing with up to 290 Gb of output in a single flow cell.

The Next Generation Sequencing (NGS) Market Report offers a comprehensive evaluation of the global landscape across multiple dimensions, including product types, applications, end-users, and regional markets. It covers all major sequencing types such as whole genome sequencing, whole exome sequencing, targeted sequencing, and RNA sequencing. Applications evaluated span clinical diagnostics, drug discovery, agriculture genomics, infectious disease tracking, and personalized medicine. The report analyzes end-user segments including hospitals, academic and research institutions, biopharmaceutical companies, and contract research organizations. Geographic coverage extends to North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with focused insights into key markets like the United States, China, Germany, and India.

In addition to established segments, the report explores emerging areas such as single-cell sequencing, metagenomics, and epigenetics, which are gaining traction in both research and clinical domains. Technological innovation trends, such as AI-driven bioinformatics, cloud integration, and portable sequencing platforms, are also examined for their impact on competitive dynamics and future opportunities. This detailed report is designed to support strategic planning for industry stakeholders, offering actionable intelligence for decision-makers aiming to invest, expand, or optimize operations within the dynamic NGS ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3815.66 Million |

|

Market Revenue in 2032 |

USD 4985.79 Million |

|

CAGR (2025 - 2032) |

3.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Illumina Inc., Thermo Fisher Scientific, Oxford Nanopore Technologies, Pacific Biosciences, Agilent Technologies, BGI Genomics, QIAGEN N.V., PerkinElmer Inc., Roche Sequencing, Bio-Rad Laboratories |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |