Reports

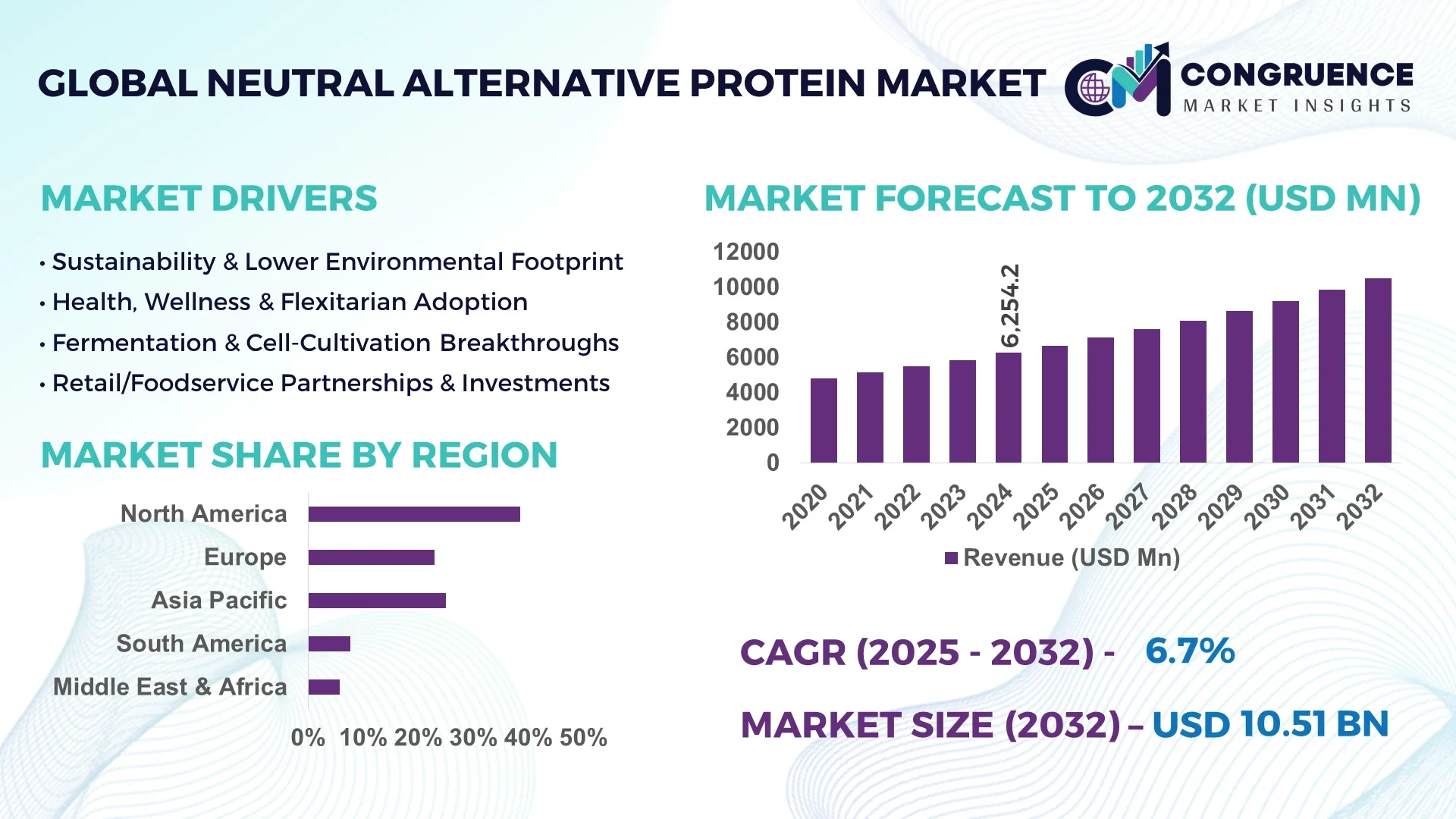

The Global Neutral Alternative Protein Market was valued at USD 6,254.22 Million in 2024 and is anticipated to reach a value of USD 10,507.23 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032.

The United States leads the Neutral Alternative Protein Market with advanced production infrastructure, significant private and public R&D investments, robust downstream processing facilities, and integration into diverse applications such as fortified beverages, dairy alternatives, and functional food formulations.

The Neutral Alternative Protein Market is witnessing expansion driven by the increasing demand from food and beverage manufacturers seeking clean-label ingredients and high-protein, low-flavor profile components for mass-market products. Emerging technological innovations, including precision fermentation and advanced protein extraction techniques, are shaping the development of scalable neutral protein isolates, aligning with evolving consumer preferences for plant-based and fermentation-derived proteins. Regulatory bodies are increasingly supporting novel protein sources, facilitating smoother pathways for market entrants and boosting product innovation. Environmental and economic considerations, including lower greenhouse gas emissions and resource-efficient production, are influencing regional consumption patterns in Europe and Asia-Pacific, contributing to growth in dietary supplements and health-centric ready-to-drink beverages. The future outlook of the Neutral Alternative Protein Market includes expanding use in clinical nutrition, sports nutrition, and specialized dietary products while maintaining taste neutrality and functional versatility for food processors.

Artificial intelligence is transforming the Neutral Alternative Protein Market by enhancing operational efficiencies, precision formulation, and advanced fermentation control within manufacturing processes. Machine learning models are now deployed to optimize protein extraction yield and purity while maintaining the desired neutral taste profile, significantly reducing manual intervention during production. AI-enabled predictive analytics are facilitating better supply chain management by forecasting raw material demand based on market consumption patterns, reducing wastage and improving inventory planning for producers in the Neutral Alternative Protein Market. Advanced computer vision systems integrated into quality control are enabling real-time monitoring of protein particle sizes and functional property consistency, ensuring uniformity across production batches. In product innovation, AI-driven molecular modeling aids in identifying protein structures with enhanced solubility and functionality without altering flavor neutrality, supporting the development of next-generation protein ingredients for the Neutral Alternative Protein Market. These improvements are fostering faster prototyping and testing of neutral protein-based product formulations, including protein beverages, supplements, and fortified dairy alternatives, driving consistent quality and efficiency within production pipelines while meeting stringent food safety standards. Moreover, the Neutral Alternative Protein Market benefits from AI-led market intelligence tools that analyze consumer feedback and trend data to align product development with evolving health and wellness trends without compromising processing efficiency.

“In April 2025, a leading U.S.-based food technology firm deployed an AI-powered real-time fermentation monitoring system in its Neutral Alternative Protein production line, reducing processing cycle times by 18% and improving protein purity levels by 12%, enabling consistent scalability of neutral protein isolates for ready-to-drink nutrition beverages.”

The Neutral Alternative Protein Market is evolving rapidly due to shifting consumer dietary preferences, increasing adoption of clean-label and functional ingredients, and technological advances in protein extraction and fermentation processes. Market dynamics are influenced by the growing need for neutral-tasting, high-protein ingredients in ready-to-drink nutrition beverages, dairy alternatives, and performance nutrition products. Rising health awareness is driving demand for neutral alternative proteins with high bioavailability while supporting sustainability goals due to lower carbon emissions and water usage during production. Manufacturers are leveraging advanced process optimization to maintain cost efficiency while ensuring high purity and taste neutrality. Regional growth dynamics reveal expanding production capacities across Asia-Pacific and North America, supported by government-backed investments in plant-based and microbial protein infrastructure. The increasing emphasis on traceability, quality control, and product standardization within the Neutral Alternative Protein Market is creating a favorable environment for strategic collaborations and new product development while supporting market stability.

The expansion of plant-based and microbial fermentation facilities is driving significant momentum within the Neutral Alternative Protein Market. Producers are investing in advanced bioreactors and continuous fermentation lines to manufacture neutral protein isolates with high functionality while retaining taste neutrality, essential for seamless integration into sports nutrition products, fortified dairy alternatives, and medical nutrition formulations. For instance, large-scale fermentation systems are being utilized to produce proteins with a 90%+ purity level, reducing dependency on traditional extraction methods that often compromise flavor profiles. Additionally, the establishment of specialized downstream processing units is helping manufacturers scale operations while achieving consistent product quality and cost optimization, enhancing supply to food and beverage sectors. As consumer demand rises for allergen-free, sustainable, and neutral-flavored protein ingredients, the availability of expanded facilities is ensuring timely production to meet formulation needs while maintaining functional integrity.

The Neutral Alternative Protein Market faces limitations due to the restricted scalability of precision fermentation technologies currently used for producing high-quality neutral protein isolates. While precision fermentation enables manufacturers to produce proteins with targeted functionality and taste neutrality, the high operational costs associated with bioreactor maintenance, feedstock preparation, and contamination control limit large-scale deployments. Many smaller and mid-sized manufacturers encounter technical challenges, including variability in fermentation yields and maintaining consistent taste profiles during scale-up, which can disrupt supply chains and affect formulation timelines for end-use sectors. Additionally, stringent regulatory compliance for food-grade fermentation facilities, requiring specific equipment, contamination control systems, and waste management infrastructure, increases production complexity and delays capacity expansion plans. These constraints slow down the broader adoption of precision fermentation in the Neutral Alternative Protein Market despite its potential to deliver highly functional and neutral-tasting proteins.

The Neutral Alternative Protein Market is witnessing emerging opportunities due to its growing application in clinical and sports nutrition products requiring high-quality, neutral-tasting protein ingredients. Clinical nutrition products often demand proteins with high digestibility and bioavailability while maintaining taste neutrality for patients with dietary restrictions, creating demand for neutral alternative proteins in meal replacements, enteral nutrition, and therapeutic dietary formulations. Similarly, sports nutrition sectors are increasingly incorporating neutral protein isolates into ready-to-drink protein beverages and recovery shakes that require flavor flexibility while delivering high protein concentrations per serving. This expanding application landscape enables manufacturers to develop tailored protein ingredients for specialized nutrition markets, aligning with rising consumer interest in health-focused, high-protein, allergen-free products. As regulatory frameworks across developed markets support the inclusion of neutral alternative proteins in medical and sports nutrition, manufacturers have an opportunity to diversify their product portfolios and enter premium application segments.

The Neutral Alternative Protein Market faces challenges arising from complex supply chain structures and the need for consistent, high-quality sourcing of raw materials for neutral protein production. Producing neutral alternative proteins with uniform taste neutrality and functionality requires high-purity input materials, specialized processing equipment, and stringent quality controls at each stage, increasing operational complexity. Supply disruptions, especially in sourcing high-quality legumes or feedstocks for fermentation, can impact production timelines and consistency, directly affecting the delivery of neutral protein isolates to food and beverage sectors. Additionally, fluctuations in agricultural input prices and transport disruptions contribute to volatility in raw material availability, increasing overall production costs and impacting profitability for manufacturers. Maintaining robust traceability and adhering to quality standards while operating within a dynamic supply chain environment presents continuous challenges for producers in the Neutral Alternative Protein Market striving to ensure product uniformity while scaling up operations.

• Integration of AI-Driven Fermentation Control Systems: Advanced AI-based fermentation control systems are being deployed within the Neutral Alternative Protein market to optimize process stability and enhance protein purity. Real-time monitoring using machine learning algorithms has resulted in up to 15% improvements in yield while maintaining taste neutrality, supporting higher production scalability. This trend is particularly evident among leading manufacturers seeking to reduce energy consumption and operational downtime in continuous fermentation lines, aligning production with consistent quality and efficiency targets.

• Expansion of Precision Fermentation Facilities in Asia-Pacific: Countries including Singapore and South Korea are rapidly expanding precision fermentation facilities specifically for neutral protein production. These facilities utilize modular bioreactor designs to increase batch flexibility, achieving higher throughput rates while maintaining uniformity in particle size and functional quality. Over 30 new fermentation lines dedicated to neutral protein isolate production were commissioned across Asia-Pacific in the last 18 months, demonstrating regional commitment to alternative protein technology and food security.

• Development of Protein Blends with Enhanced Solubility: Manufacturers are actively developing neutral alternative protein blends with improved solubility for ready-to-drink beverages and clear protein applications. Utilizing enzymatic hydrolysis and advanced filtration, these blends achieve over 98% solubility without impacting flavor, enabling smoother integration into beverages and high-protein dairy alternatives. This trend addresses the increasing consumer preference for functional beverages with clean taste profiles while maintaining high protein density.

• Regulatory Support for Novel Protein Sources: Regulatory agencies in North America and Europe have accelerated approval processes for neutral alternative proteins derived from novel sources, including microbial and algal proteins. This has led to a measurable increase in product launches using these ingredients in nutritional supplements and clinical nutrition products. Companies are leveraging these approvals to diversify product portfolios while ensuring compliance with stringent food safety and quality standards, expanding the market landscape for neutral alternative proteins globally.

The Neutral Alternative Protein market segmentation is defined by type, application, and end-user sectors, reflecting the operational diversity within the industry. By type, the market includes plant-based isolates, microbial-derived proteins, and blended formulations, each catering to different formulation and processing needs while ensuring taste neutrality. Applications span ready-to-drink nutrition beverages, dairy alternatives, clinical nutrition, and sports nutrition products, where taste neutrality and high protein content are critical. End-user sectors include large-scale food manufacturers, dietary supplement producers, and clinical nutrition product developers actively incorporating neutral alternative proteins to meet the rising consumer demand for functional, allergen-free protein sources. Each segment plays a role in shaping supply chain priorities and technological advancements within the Neutral Alternative Protein market.

Plant-based neutral protein isolates remain the leading type within the Neutral Alternative Protein market due to their established production infrastructure and integration into large-scale food and beverage manufacturing. These isolates are preferred for their high protein concentration and neutral taste profile, making them suitable for fortified beverages and dairy alternatives. Microbial-derived proteins are emerging as the fastest-growing type, driven by increasing investments in precision fermentation technology that enables scalable production with consistent quality while reducing environmental impact. These proteins offer improved functional properties, including solubility and emulsification, supporting their application in advanced nutritional formulations. Blended protein formulations, which combine plant-based and microbial-derived proteins, are gaining traction for specialized dietary applications where specific amino acid profiles and taste neutrality are required, catering to clinical nutrition and high-performance sports products while expanding the market landscape for functional neutral protein ingredients.

Ready-to-drink nutrition beverages represent the leading application within the Neutral Alternative Protein market, driven by consumer demand for convenient, high-protein functional drinks that align with health and wellness trends while maintaining clean taste profiles. The fastest-growing application is within clinical nutrition products, supported by rising healthcare needs for high-protein, allergen-free, and easily digestible formulations used in medical and therapeutic dietary programs. Dairy alternatives, including neutral protein-enriched yogurts and milks, are also contributing significantly, providing consumers with lactose-free, high-protein options without compromising taste. Sports nutrition applications continue to grow steadily as manufacturers incorporate neutral alternative proteins into recovery shakes and performance nutrition products, benefiting from their high bioavailability and ease of integration into flavored products while ensuring consistent quality and nutritional profiles.

Large-scale food and beverage manufacturers represent the leading end-user segment within the Neutral Alternative Protein market, using neutral protein ingredients to fortify mainstream consumer products, including beverages and dairy alternatives, with high protein content without altering taste profiles. The fastest-growing end-user segment is clinical nutrition product developers, as healthcare providers and specialized nutrition companies increasingly incorporate neutral alternative proteins into therapeutic formulations for patients requiring targeted dietary interventions. Dietary supplement producers also play a significant role, using neutral protein isolates in powdered supplements and functional nutrition bars where flavor flexibility and high protein density are essential. These diverse end-user segments collectively contribute to shaping demand, driving advancements in processing and formulation technologies while expanding the operational landscape of the Neutral Alternative Protein market.

North America accounted for the largest market share at 38.5% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

The Neutral Alternative Protein Market is observing robust expansion due to the increasing integration of neutral protein isolates in high-protein beverages, dairy alternatives, and clinical nutrition products across key regions. North America remains strong due to advanced processing infrastructure and high consumer adoption of functional, clean-label products. In Asia-Pacific, countries such as China, India, and Japan are investing heavily in precision fermentation and modular production lines to scale neutral protein manufacturing while addressing sustainability goals. Europe continues to push the adoption of neutral alternative proteins through stringent sustainability policies and innovation in functional food manufacturing, while South America and the Middle East & Africa regions are emerging with focused government incentives and evolving consumer dietary patterns, expanding the operational landscape for the Neutral Alternative Protein Market globally.

Driving Adoption Through Functional Nutrition Innovation

North America holds a commanding 38.5% share in the Neutral Alternative Protein Market, driven by extensive adoption across the functional beverage and sports nutrition industries. High demand from the United States and Canada for neutral protein isolates in fortified ready-to-drink beverages and dairy alternatives contributes significantly to market volume. The FDA’s continued support for innovative protein ingredients and GRAS approvals has streamlined product launches while ensuring compliance and safety in formulations. Technological advancements, including the use of AI in fermentation monitoring and advanced filtration systems, are enhancing production efficiency and consistency. Digital transformation across supply chains, particularly predictive analytics for ingredient demand forecasting, is further strengthening the operational capabilities of manufacturers, helping North American producers maintain leadership within the Neutral Alternative Protein Market.

Pioneering Sustainable Solutions in Functional Ingredients

Europe accounts for 26.3% of the Neutral Alternative Protein Market, with Germany, France, and the UK being key markets driving demand for neutral protein isolates in clean-label, high-protein foods. The region’s strict sustainability frameworks and the European Food Safety Authority’s structured pathways for novel proteins are accelerating the introduction of neutral protein-based ingredients across functional foods and nutritional supplements. Adoption of advanced processing technologies, including enzymatic hydrolysis and membrane filtration, is enhancing the functional quality of neutral proteins. Collaborative R&D initiatives between food manufacturers and technology providers are fueling product innovation while supporting Europe’s sustainability targets. The region’s strong focus on reducing carbon footprints across food processing aligns with increasing consumer demand for low-impact, neutral-tasting protein ingredients, supporting consistent market growth.

Scaling Neutral Protein Production to Meet Functional Demand

Asia-Pacific is the fastest-expanding region in the Neutral Alternative Protein Market, driven by rising demand across China, India, Japan, and South Korea, which collectively contribute to over 30% of the global volume. Rapid infrastructure development in modular fermentation facilities and advanced downstream processing is positioning the region to meet high-volume demand for neutral protein isolates in functional beverages and clinical nutrition products. China and India are investing heavily in food technology parks and bio-manufacturing hubs, facilitating innovation and scale-up of neutral alternative proteins. Regional tech trends, including AI-driven process monitoring and continuous fermentation advancements, are reducing operational inefficiencies while ensuring consistency in taste neutrality and functional properties. These developments align with shifting consumer preferences toward health-focused, high-protein diets, expanding the Neutral Alternative Protein Market across Asia-Pacific.

Emerging Hubs Driving Functional Ingredient Expansion

South America, led by Brazil and Argentina, is emerging in the Neutral Alternative Protein Market with a growing focus on producing neutral protein isolates for fortified beverages and nutritional supplements. The region currently holds around 5.7% of the market share, with Brazil’s large-scale agricultural infrastructure supporting cost-effective sourcing of plant-based raw materials for protein extraction. Energy-efficient production systems and strategic investments in food processing infrastructure are facilitating the entry of neutral alternative proteins into mainstream product formulations. Government trade policies and participation in sustainability-focused initiatives are supporting manufacturers seeking to export neutral protein ingredients to North America and Europe. Brazil’s innovation hubs are increasingly exploring enzymatic processing methods to enhance the solubility and functionality of neutral proteins, aligning with evolving dietary preferences in the region.

Leveraging Technology to Advance Functional Nutrition

The Middle East & Africa region is gradually expanding in the Neutral Alternative Protein Market, driven by increasing demand from the UAE, Saudi Arabia, and South Africa for neutral protein ingredients in functional foods and clinical nutrition products. The region contributes approximately 4.2% of the global market volume, with growth supported by government-backed food security initiatives and investment in local food processing infrastructure. Technological modernization, including the adoption of continuous fermentation systems and advanced filtration units, is enabling manufacturers to maintain taste neutrality and functional quality during production. Local regulations facilitating the entry of innovative protein ingredients into the functional foods sector are supporting market expansion. Trade partnerships with European and Asian manufacturers are strengthening the region’s supply chain capabilities, allowing for a stable supply of high-quality neutral alternative proteins to address rising consumer health awareness.

United States – 34.2% market share

Strong end-user demand and advanced production capacity drive the United States’ dominance in the Neutral Alternative Protein Market.

China – 15.8% market share

High production capacity combined with rapid scaling of modular fermentation facilities positions China as a key leader in the Neutral Alternative Protein Market.

The Neutral Alternative Protein market features a highly competitive landscape with over 150 active global and regional players competing across plant-based, microbial-derived, and blended neutral protein segments. Key competitors are focusing on functional product differentiation, emphasizing taste neutrality and enhanced solubility to strengthen market positioning within ready-to-drink nutrition beverages, dairy alternatives, and clinical nutrition products. Strategic initiatives such as partnerships for technology sharing, joint ventures for precision fermentation facilities, and cross-border product launches are shaping competition in the Neutral Alternative Protein market. Recent trends include the deployment of AI-driven fermentation optimization and advanced filtration technologies to improve protein purity and production consistency. Several players are also pursuing vertical integration strategies to secure high-quality raw materials, ensuring stable supply chain operations in an evolving regulatory landscape. Mergers and acquisitions within the protein ingredients and fermentation technology sectors are being used to enhance technological capabilities and expand geographic reach. The increasing emphasis on sustainability and allergen-free, clean-label product formulations is influencing innovation pipelines, leading to rapid prototyping and commercial launches in the Neutral Alternative Protein market to capture emerging demand in functional and clinical nutrition sectors globally.

ADM

Cargill

Roquette Frères

Ingredion Incorporated

Kerry Group

Burcon NutraScience Corporation

Glanbia Nutritionals

DuPont Nutrition & Health

Puris

Royal DSM

The Neutral Alternative Protein market is witnessing accelerated technological advancements focused on enhancing process efficiency, purity levels, and functional flexibility of neutral protein isolates for diverse applications. Precision fermentation has become central in microbial-derived protein production, utilizing modular bioreactor systems with advanced control algorithms to maintain consistent environmental conditions and yield uniform, neutral-tasting proteins with over 90% purity. Enzymatic hydrolysis is increasingly used in plant-based protein extraction, improving solubility to over 98% for ready-to-drink applications while preserving clean taste profiles critical for clinical and sports nutrition formulations. Membrane filtration and cross-flow microfiltration technologies are being employed to reduce particulate content, refine molecular weight distribution, and enhance functional properties such as emulsification and water-binding capacity. AI and machine learning models are now integrated within production monitoring systems to predict fermentation endpoints, optimize raw material utilization, and reduce batch variability, ensuring cost-effective, scalable production aligned with sustainability goals. 3D food printing technology is under exploration to create customized, neutral-tasting protein-based products tailored for patient-centric nutrition and high-performance sports dietary needs. Blockchain and digital traceability tools are also being piloted to secure sourcing transparency, essential for meeting regulatory and consumer expectations within the Neutral Alternative Protein market as demand continues to rise across functional and therapeutic nutrition sectors.

• In February 2023, Puris inaugurated a new pea protein facility in Minnesota with a processing capacity of 20,000 metric tons annually, significantly increasing supply of neutral-tasting protein isolates for ready-to-drink beverages and clean-label dairy alternatives.

• In July 2023, ADM partnered with a European biotech startup to implement precision fermentation for neutral alternative protein production, achieving a 15% reduction in water usage and a 12% improvement in protein purity in pilot-scale batches.

• In March 2024, Roquette launched a new neutral pea protein isolate designed for clinical nutrition and elderly care formulations, featuring over 92% purity and enhanced solubility to support easy integration into therapeutic ready-to-drink nutritional products.

• In May 2024, DSM opened a food technology hub in Singapore focusing on the development of neutral alternative proteins using AI-assisted fermentation, targeting high-protein beverages and fortified dairy products with improved taste neutrality and functional versatility.

The Neutral Alternative Protein Market Report provides comprehensive insights into the evolving landscape of neutral protein isolates across plant-based, microbial-derived, and blended segments, covering advanced extraction, fermentation, and downstream processing technologies shaping market development. The report analyzes applications spanning functional beverages, dairy alternatives, clinical nutrition, and sports nutrition products, where demand for high-purity, taste-neutral proteins is driving innovation and production scaling globally. Regional assessments include North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing infrastructure readiness, manufacturing capabilities, and regulatory frameworks influencing adoption. The report highlights the impact of digital transformation within production processes, including the integration of AI, predictive analytics, and real-time monitoring systems that improve operational efficiency and product consistency. It also explores emerging segments such as 3D-printed nutrition and customized clinical nutrition formulations, providing a forward-looking view for stakeholders considering entry or expansion in this dynamic market. Attention is given to the evolving competitive landscape, showcasing the strategic initiatives of key players while addressing technological advancements, supply chain developments, and consumer trends influencing the Neutral Alternative Protein Market’s operational and growth pathways.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6254.22 Million |

|

Market Revenue in 2032 |

USD 10507.23 Million |

|

CAGR (2025 - 2032) |

6.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ADM, Cargill, Roquette Frères, Ingredion Incorporated, Kerry Group, Burcon NutraScience Corporation, Glanbia Nutritionals, DuPont Nutrition & Health, Puris, Royal DSM |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |