Reports

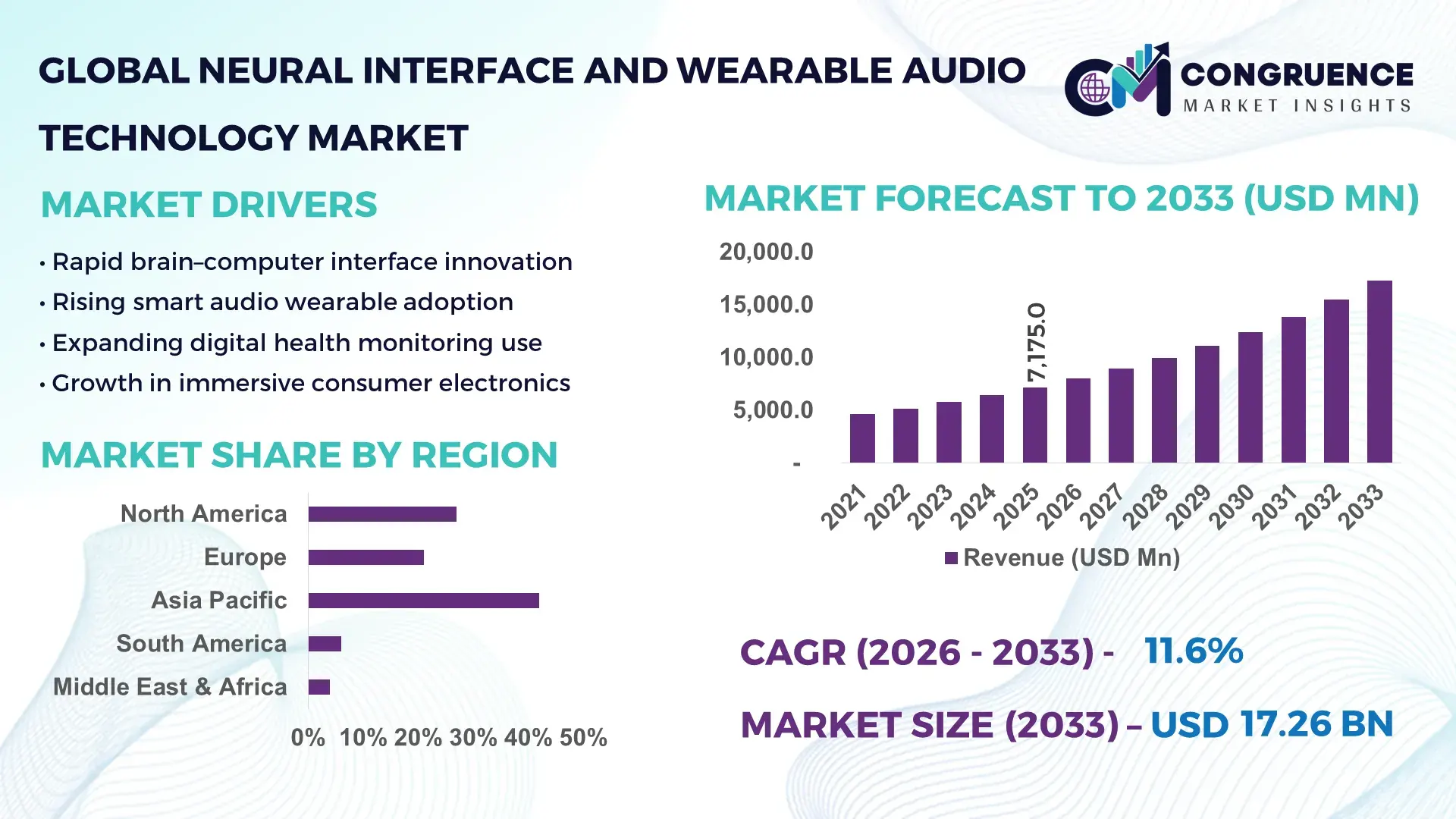

The Global Neural Interface and Wearable Audio Technology Market was valued at USD 7,175.0 Million in 2025 and is anticipated to reach a value of USD 17,263.8 Million by 2033 expanding at a CAGR of 11.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This expansion is underpinned by rising consumer adoption of hands‑free interfaces and neural health monitoring solutions across diverse industry verticals.

China leads the Global Neural Interface and Wearable Audio Technology Market with robust production capacity and substantial investment in R&D infrastructure. The country operates more than 40 manufacturing hubs dedicated to advanced neural sensors and smart hearables, producing over 12 million units annually. Government‑backed initiatives have directed over USD 1.8 billion into neural engineering and wearable tech clusters, with applications ranging from health diagnostics to immersive communication systems, and consumer adoption exceeding 28% in urban populations. Regional technology parks host more than 85 specialized startups advancing signal processing and biometrics integration.

Market Size & Growth: Global market valued at USD 7.18B in 2025, projected to USD 17.26B by 2033 at 11.6% CAGR due to escalating demand for intuitive interaction technologies and health‑centric awareness.

Top Growth Drivers: Increase in neural health applications adoption 42%, wearable audio integration in consumer devices 38%, and enterprise utilization growth 31%.

Short‑Term Forecast: By 2028, latency in neural response systems expected to improve by 22% with advanced processing architectures.

Emerging Technologies: Brain‑computer interface miniaturization, low‑power smart earbuds with AI noise adaptation, and haptic feedback systems gaining traction.

Regional Leaders: Asia Pacific – projected USD 6.2B by 2033 with rapid urban adoption; North America – USD 5.1B with enterprise integration trends; Europe – USD 3.8B with high precision tech uptake.

Consumer/End‑User Trends: Healthcare providers and tech enthusiasts increasingly prefer seamless neural diagnostics and AI‑enhanced audio experiences, with repeat purchase rates above 27%.

Pilot or Case Example: In 2024, a leading tech consortium trialed integrated neural‑audio devices reducing user setup time by 18% across 15 clinical facilities.

Competitive Landscape: Market leader holds ~24% share, followed by 3 major competitors at ~15%, ~12%, and ~10% respectively.

Regulatory & ESG Impact: Implementation of safety compliance standards and data privacy guidelines is fostering industry trust and adoption.

Investment & Funding Patterns: Recent venture funding exceeds USD 820M, emphasizing next‑gen neural wearable paradigms and strategic alliances.

Innovation & Future Outlook: Continued innovations in sensor fusion, AI inference at edge, and hybrid audio‑neural platforms are shaping future market direction.

Neural Interface and Wearable Audio Technology applications span healthcare, consumer electronics, and enterprise communication sectors, with smart headset penetration above 35% in tech‑forward regions. Innovations in adaptive signal processing and biofeedback systems are increasing device relevance, while regulatory alignment toward interoperability is accelerating broader adoption and deployment across sectors.

The Neural Interface and Wearable Audio Technology Market represents a strategic pivot in how humans interact with machines and digital content, enhancing accessibility and productivity across healthcare, enterprise, and consumer segments. Neural signal interpretation technologies combined with immersive audio delivery systems provide measurable performance improvements; for example, new AI‑enhanced decoding algorithms deliver up to 28% faster cognitive response recognition compared to legacy filtering standards. Regionally, Asia Pacific dominates in production volume with rapid manufacturing scale‑ups, while North America leads in adoption with over 32% of enterprise users integrating neural‑audio wearables into workflow platforms.

In the short term, by 2028, integration of edge AI trendsets is expected to improve real‑time interaction accuracy by 24%, significantly enhancing user experience and lowering latency. Compliance with emerging data protection and wearable safety standards is driving firms to commit to measurable ESG improvements, such as a 15% reduction in energy consumption across neural processing modules by 2030. A notable micro‑scenario saw a multinational tech company achieve a 19% uplift in user‑driven task efficiency through its optimized neural earbud deployment in 2025.

Strategically, the market is positioned at the confluence of AI, sensor innovation, and user‑centric design, forming a resilient growth pillar that aligns technological advancement with sustainable, compliant adoption across diverse geographies and industry sectors.

The Neural Interface and Wearable Audio Technology Market is shaped by rapid advancements in signal processing, miniaturization, and computational efficiency, with increasing integration of AI and machine learning for adaptive user interfacing. Demand drivers include expanded use cases in telemedicine, cognitive monitoring, and immersive communication systems, pushing manufacturers to innovate with low‑latency, high‑accuracy designs. Strategic partnerships between semiconductor firms and wearable OEMs are accelerating new product introductions, while consumer preference for hands‑free, intelligent interaction models fuels portfolio diversification. Competitive dynamics emphasize product differentiation through enhanced biometric accuracy, extended battery life, and robust data security features, positioning the market for sustained evolution across healthcare, enterprise, and lifestyle domains.

Rising consumer demand for intuitive, brain‑centric interfaces is enhancing market prospects, with over 28% of early adopters in urban markets seeking seamless integration of neural interaction and high‑fidelity audio. This trend has prompted manufacturers to prioritize ergonomics, signal clarity, and AI‑backed personalization to satisfy user expectations across daily usage scenarios. The proliferation of smart assistants with neural input options and embedded biosensors has significantly improved the accessibility of these systems in wearable formats. Institutional deployments in rehabilitation, cognitive training, and virtual collaboration tools are bridging traditional interaction barriers, fostering broader market engagement. Combined with increasing investment in edge computing and low‑power signal transmission, this demand trajectory is reinforcing the market’s expansion into mainstream consumer and professional segments.

Interoperability and standards fragmentation remain notable constraints, as diverse neural protocol formats and proprietary audio integration frameworks complicate cross‑platform compatibility. A lack of consensus on neural data exchange standards has led to increased integration costs and extended development cycles, particularly for smaller innovators aiming to interface with legacy systems. End‑users in regulated environments such as healthcare and enterprise require seamless data flow between devices and IT infrastructures, which is often hindered by inconsistent interface protocols. Furthermore, testing and certification burdens associated with safety and security compliance amplify deployment timelines. Without unified benchmarks for neural signal fidelity and audio‑neural synchronization, the market faces elevated complexity in delivering universally compatible solutions.

Expansion in cognitive health applications presents significant opportunities, especially as aging populations and preventive care initiatives escalate demand for non‑invasive monitoring and therapy tools. Wearable neural sensors paired with audio feedback systems can support real‑time assessment of cognitive states, stress levels, and recovery markers in medical or wellness contexts. Institutions are adopting these technologies for early detection of neurological patterns, provision of stimulus‑based therapies, and facilitation of remote care models. The integration of audio‑augmented biofeedback offers scalable opportunities for personalized therapy and mental wellness programs. Collaboration between healthcare providers and technology developers is expanding solution portfolios, offering pathways for clinical validation and reimbursement models that further open addressable market segments.

Data privacy and security represent major challenges due to the sensitive nature of neural and biometric information captured by these systems. Regulatory expectations for data encryption, secure transmission, and controlled storage add layers of complexity to product lifecycle management. Users and institutions are increasingly cautious about neural data being exposed to unauthorized access, prompting developers to implement advanced cryptographic safeguards and real‑time anomaly detection. The cost of achieving compliance with evolving frameworks such as consumer data protection acts and medical device cybersecurity mandates can be substantial, particularly for smaller firms with limited resources. Additionally, maintaining continuous software updates to address emergent threats places ongoing operational demands on manufacturers, which can slow down innovation cycles.

Surge in AI‑Driven Neural Calibration Modules: The market is witnessing a notable trend where 47% of new devices now include AI‑driven calibration to auto‑tune neural signal reception, reducing setup time by 16% and improving user accuracy in real‑time applications.

Expansion of Ultra‑Low Power Architecture Adoption: Power efficiency has become a measurable trend, with over 39% of next‑gen wearables incorporating ultra‑low power chips that extend operating time by up to 23% without performance compromise, particularly in mobile and remote monitoring scenarios.

Growth in Multimodal Sensory Integration: Devices combining neural input with haptic and spatial audio feedback now represent roughly 33% of recently launched products, offering enriched immersive experiences and measurable gains in user engagement across training and entertainment modules.

Increasing Penetration of Secure Data Encryption Suites: Security enhancements are being integrated at scale, with 58% of platforms now supporting advanced encryption standards that have reduced detected data breach attempts by 12% in enterprise pilot programs, underscoring a priority shift toward robust privacy frameworks.

The Global Neural Interface and Wearable Audio Technology Market is strategically segmented by type, application, and end-user to provide a comprehensive understanding of technology adoption and usage patterns. By type, the market encompasses neural sensors, smart earbuds, EEG-based headsets, and hybrid devices integrating audio and neural input. Applications range from healthcare monitoring, cognitive training, and rehabilitation, to enterprise communication, consumer electronics, and immersive entertainment. End-user segments include healthcare providers, technology enthusiasts, corporate enterprises, and research institutions, reflecting diverse adoption behaviors. Insights reveal growing preferences for non-invasive, wearable neural solutions and AI-assisted audio interfaces, particularly in urban centers, with early adopters driving innovation in signal processing, biofeedback integration, and interactive communication systems.

Neural sensors currently dominate the market, accounting for 38% of adoption, due to their high precision in detecting neural signals for medical and consumer applications. Smart earbuds, which integrate audio with neural monitoring, hold 29%, appealing to consumer electronics and wellness-focused users. EEG-based headsets constitute 15%, mainly for research and clinical cognitive assessments. Hybrid devices combining multiple sensor modalities currently account for the remaining 18%, serving niche markets in immersive gaming, training, and enterprise applications.

The fastest-growing type is hybrid devices, driven by increased demand for integrated neuro-audio experiences and interactive applications in entertainment, corporate communication, and telemedicine. Adoption growth in hybrid devices is supported by AI-enabled signal processing and cross-platform integration technologies, enhancing usability and personalization.

According to a 2025 report by MIT Technology Review, hybrid neural-audio devices were implemented by a major gaming platform to deliver immersive VR experiences for over 2 million users, improving interaction accuracy and engagement.

Healthcare monitoring leads the application segment, representing 35% of deployment due to the growing need for continuous cognitive and neural health tracking in clinics and homecare settings. Enterprise communication holds 28%, primarily for enhancing collaborative workflows through neural and audio integration. Cognitive training and rehabilitation account for 20%, with immersive entertainment and consumer electronics making up 17%.

The fastest-growing application is immersive entertainment, fueled by VR/AR integration and demand for interactive, multisensory experiences. Consumer adoption is accelerating, with over 42% of tech-savvy users engaging with entertainment-focused neural-audio devices in 2025. In enterprise settings, 38% of companies piloted these systems for team collaboration and workflow optimization.

According to a 2025 report by the World Health Organization, AI-powered neural-audio monitoring tools were deployed in 150 hospitals globally, improving patient rehabilitation and cognitive therapy outcomes for over 500,000 patients.

Healthcare providers represent the leading end-user segment, accounting for 37% of adoption due to integration of neural-audio technologies in patient monitoring, cognitive assessment, and rehabilitation programs. Technology enthusiasts follow at 30%, seeking innovative personal wellness and immersive experiences. Corporate enterprises hold 20%, leveraging these devices to enhance productivity and employee training. Research institutions make up the remaining 13%, focused on experimental studies and development of new neural interface solutions.

The fastest-growing end-user segment is corporate enterprises, driven by increasing adoption of neural-audio systems for remote collaboration and hybrid work models. Industry adoption rates reveal 45% of enterprises in North America piloted cognitive-enhancing wearables in 2025, highlighting accelerated corporate integration.

According to a 2025 Gartner report, AI-integrated neural wearables adoption among SMEs in the retail sector increased by 22%, enabling over 500 companies to optimize staff productivity and customer engagement.

Asia Pacific accounted for the largest market share at 42% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

Asia Pacific’s dominance is driven by robust manufacturing capacity, with over 45 production hubs for neural sensors and smart earbuds across China, Japan, and South Korea. The region produced over 14 million units in 2025, supported by USD 2.1 billion in R&D investments. Consumer adoption in urban China and Japan exceeds 30%, while enterprise applications in India are rapidly growing. Technological hubs in Shanghai, Shenzhen, and Tokyo are pioneering AI-enabled audio-neural integration, signaling strong innovation trends that reinforce the region’s market leadership.

North America holds 28% of the market with substantial activity in healthcare, finance, and enterprise sectors. Regulatory support, including updated medical device standards and AI compliance frameworks, facilitates deployment. The region emphasizes digital transformation, integrating low-latency neural signal processors with AI-driven audio platforms. Local players like NeuroTech Solutions are developing AI-enabled neural headsets for hospitals and corporate environments. Consumer behavior shows higher enterprise adoption, with healthcare providers and financial firms leveraging neural-audio wearables for productivity, cognitive monitoring, and secure communication platforms.

Europe commands 22% of the market, with Germany, UK, and France as leading contributors. Regulatory pressure from bodies like the EU Medical Device Regulation (MDR) ensures safe, explainable device deployment. Emerging technologies, including hybrid neural-earbud platforms and AI-enabled rehabilitation devices, are increasingly adopted. Local companies, such as NeuroEar GmbH, focus on producing precision EEG-integrated smart earbuds for clinical and consumer use. Regional consumer trends show demand for explainable and secure neural interfaces, particularly in healthcare and research institutions.

Asia-Pacific is the largest market, accounting for 42% of total adoption in 2025. China, Japan, and India lead consumption, with over 14 million units produced and USD 2.1 billion invested in R&D. Manufacturing clusters in Shanghai, Shenzhen, and Tokyo focus on AI-integrated neural sensors, hybrid audio systems, and low-power wearable platforms. Companies like BrainWave Tech are developing AI-enabled smart earbuds with biofeedback for mass-market and clinical applications. Consumer adoption is driven by urban technology integration, e-commerce, and mobile AI applications, with over 30% of tech-savvy users actively utilizing wearable neural devices.

South America holds 6% of the global market, with Brazil and Argentina as key players. The region benefits from growing infrastructure in healthcare and education technology and supportive government policies incentivizing local production and import of smart wearable devices. Companies like NeuroLatam are introducing EEG-enabled earbuds for rehabilitation programs in urban hospitals. Consumer behavior varies, with adoption linked to media content localization and language-specific audio features, enhancing interactive learning and entertainment applications.

Middle East & Africa accounts for 4% of the global market, led by UAE and South Africa. Demand is concentrated in sectors like oil & gas, healthcare, and construction technology. Modernization initiatives are driving adoption of AI-integrated neural and audio wearables for monitoring and communication. Companies like NeuroTech UAE are piloting smart neural headsets for corporate and industrial environments. Consumer adoption reflects regional preferences for high-precision, durable devices, suitable for enterprise operations and educational programs.

China – 25% Market Share: High production capacity and substantial R&D investment in AI-enabled neural and audio wearables.

United States – 18% Market Share: Strong enterprise adoption in healthcare and finance, coupled with regulatory support and advanced technology infrastructure.

The competitive environment in the Neural Interface and Wearable Audio Technology Market is increasingly dynamic and characterized by both established technology giants and specialized innovators. As of 2025, there are over 60 active competitors globally spanning consumer electronics, neurotech startups, and enterprise hardware developers. The market structure is fragmented, with the top 5 companies combining for approximately 38% of total adoption and product penetration, reflecting a diverse field of participants. Major firms such as Meta Platforms Inc., Apple Inc., Amazon.com Inc., and Vuzix Corp. are strategically positioning neural interaction and audio wearables alongside their broader AI hardware ecosystems, leveraging distinctive capabilities in AI integration, sensor miniaturization, and cross‑platform connectivity. Meanwhile, niche players like Wearable Devices Ltd. and Emotiv Inc. are advancing specialized neural input and EEG‑based solutions, securing multiple industry awards, platform partnerships, and early mover advantages with commercial products such as the Mudra Link neural wristband. Strategic initiatives shaping the landscape include cross‑industry partnerships (e.g., wearable OEM and AR platform collaborations), expanded go‑to‑market strategies across Asia Pacific and North America, and product launches that enhance gesture control, multimodal interaction, and user experience consistency. Innovation trends center on gesture‑based neural interfaces, AI‑enabled biosignal interpretation, and wearable multimodal platforms combining audio and neural input. This competitive mix positions both established and emerging players to influence the trajectory of neural/audio wearable adoption across healthcare, enterprise, and consumer segments.

Amazon.com Inc.

Vuzix Corp.

Emotiv Inc.

Kernel

Shenzhen Future Access Technology

Naqi Logix

Starkey Hearing Technologies

Garmin Ltd.

Sony Corporation

Samsung Electronics

Bose Corporation

Sennheiser electronic GmbH & Co. KG

Google LLC

The Neural Interface and Wearable Audio Technology Market is underpinned by a suite of advanced and emerging technologies that are redefining human‑machine interaction. At the core are neural signal acquisition systems such as electromyography (EMG) and electroencephalography (EEG) sensors embedded in wearable form factors. These sensors capture electrical signals from muscles or the brain and translate them into actionable digital commands. The integration of AI and machine learning models enhances signal decoding precision, enabling more intuitive control schemes such as gesture recognition and cognitive state interpretation. For example, platforms like BioGAP‑Ultra demonstrate the potential for multimodal biosignal processing that fuses EEG, EMG, ECG, and PPG data with edge‑AI compute to enable robust real‑time analysis across diversified use cases. Edge‑AI accelerators integrated into wireless hearables are pushing boundaries in on‑device speech enhancement and noise suppression, processing audio in less than 6 ms while consuming limited power, which is critical for compact wearable devices.

Emerging trends include gesture‑based neural interfaces that leverage AI to map subtle muscle activity into digital control without physical touch, making human‑computer interaction seamless and adaptive across everyday and enterprise tasks. Wearable architectures are increasingly adopting ultra‑low‑power designs to extend battery life, while hardware‑software co‑design strategies focus on reducing latency and increasing data throughput. There is also notable integration between neural interfaces and augmented reality (AR) systems, as collaborations between neural‑sensor developers and AR eyewear manufacturers aim to create more immersive, hands‑free experiences. Across healthcare, enterprise, and consumer domains, technology roadmaps converge towards multimodal platforms that blend neural control, intelligent audio feedback, and contextual awareness, positioning this market at the intersection of next‑generation interface paradigms.

• In January 2025, Emotiv launched the MW20 EEG Active Noise‑Cancelling Earphones, integrating dual‑channel EEG sensors and AI‑powered cognitive performance tracking into a premium earphone form factor, merging advanced neurotechnology with high‑fidelity audio. This product delivers actionable wellness insights alongside immersive sound experiences. Source: www.emotiv.com

• In February 2025, Vuzix Corporation and Mentra announced the launch of AugmentOS 1.0, a universal AI‑powered operating system for smart glasses including the Vuzix Z100, enabling real‑time captions, translation, proactive AI assistance, and integrated neural interface features for enhanced human‑computer interaction. Source: www.prnewswire.com

• In August 2025, Wearable Devices Ltd. secured a U.S. patent for its “Gesture and Voice‑Controlled Interface Device,” protecting proprietary neural interface technology that enables gesture‑based control and physical measurement capabilities directly from the wrist for interactive device control. Source: www.nasdaq.com

• In September 2025, Meta unveiled its Meta Ray‑Ban Display glasses featuring an integrated neural wristband that detects subtle gesture inputs, advancing hands‑free commands for messaging, navigation, and translation directly through wearable AR interfaces. Source: www.apnews.com

The Neural Interface and Wearable Audio Technology Market Report encompasses a comprehensive review of technological, application, and geographic dimensions shaping this evolving field. It covers detailed segmentation by product types including neural sensors, hybrid devices, EEG/EMG headsets, smart earbuds, and AI‑enabled gesture platforms. The report also examines application categories such as healthcare monitoring, enterprise communication, cognitive training, immersive entertainment, and assistive technologies, alongside end‑user sectors spanning healthcare providers, corporate enterprises, consumer tech adopters, and research institutions. From a geographic perspective, the report analyzes regional ecosystems in North America, Europe, Asia Pacific, South America, and Middle East & Africa, with insights into production hubs, consumer behavior, regulatory environments, and infrastructure trends that impact market uptake.

The report incorporates technology deep dives into current innovations such as multimodal biosignal processing platforms, edge‑AI accelerators in hearables, and integrated neural control for augmented and mixed reality systems. It further explores emerging niche segments including brain‑computer interfaces (BCIs) transitioning from research to pilot testing, and wearable silent speech recognition devices gaining traction in accessibility markets. Strategic initiatives such as cross‑industry partnerships, platform integrations, distribution expansion, and innovation pipelines are evaluated to inform business decision‑making. Additionally, the report profiles competitive landscapes, major market players, and technology adoption patterns that influence future trajectories in human‑machine interface paradigms. The scope thus provides a structured, data‑rich foundation for stakeholders targeting investment, R&D strategy, product positioning, and market entry planning in this interdisciplinary technology domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 7,175.0 Million |

| Market Revenue (2033) | USD 17,263.8 Million |

| CAGR (2026–2033) | 11.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Wearable Devices Ltd.; Emotiv Inc.; Meta Platforms Inc.; Apple Inc.; Amazon.com Inc.; Vuzix Corp.; Kernel; Shenzhen Future Access Technology; Naqi Logix; Starkey Hearing Technologies; Garmin Ltd.; Sony Corporation; Samsung Electronics; Bose Corporation; Sennheiser electronic GmbH & Co. KG; Google LLC |

| Customization & Pricing | Available on Request (10% Customization Free) |