Reports

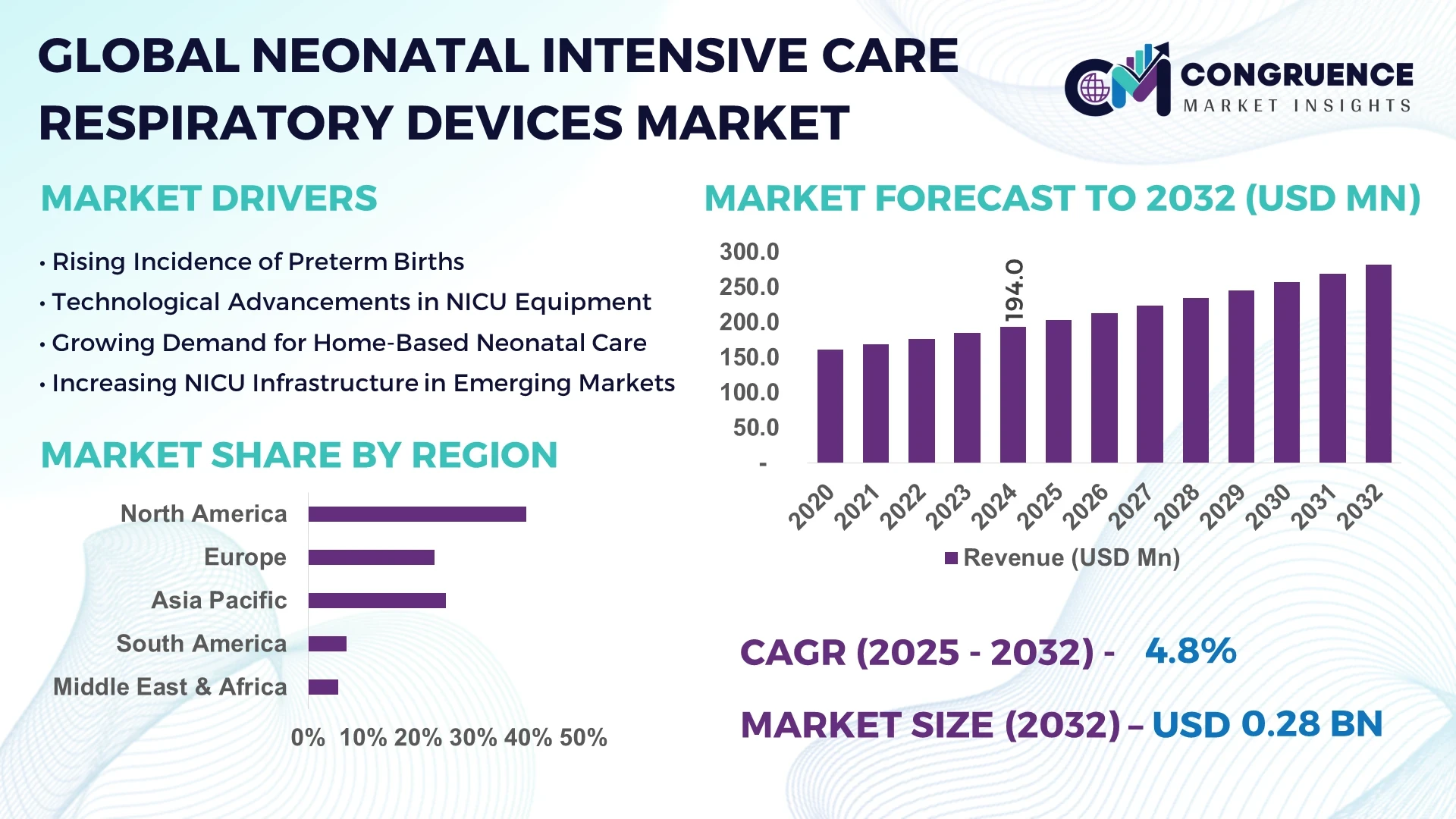

The Global Neonatal Intensive Care Respiratory Devices Market was valued at USD 194.0 Million in 2024 and is anticipated to reach a value of USD 282.3 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032.

North America remains the dominant market, with the United States leading production capacity in advanced ventilators and CPAP systems. The country has seen substantial investment in neonatal respiratory device manufacturing plants and R&D hubs, combined with technological advancements such as embedded microprocessor–controlled ventilators. Clinical applications have expanded into hybrid respiratory support modes integrating non‑invasive ventilation and high‑frequency oscillation.

The Neonatal Intensive Care Respiratory Devices Market encompasses multiple industry sectors: medical device manufacturers, hospital equipment suppliers, and neonatal care facilities. CPAP devices and conventional ventilators account for the majority of unit sales, while high‑frequency ventilators and oxygen hoods contribute notable volumes to specialized NICU settings. Recent innovations include compact, integrated ventilator‑monitor systems with built‑in humidity control and automated weaning algorithms. Regulatory updates, such as revised ISO 80601‑2‑74 standards, have spurred environmental and safety improvements in device design. Economically, rising hospital construction in emerging markets has increased demand for modular NICU installations. Regionally, Asia‑Pacific shows accelerating adoption in urban tertiary hospitals, whereas Europe emphasizes device interoperability within hospital information systems. Emerging trends include the shift toward outpatient and home‑based neonatal respiratory support and compatibility of devices with tele‑NICU networks—driving future product diversification and channel expansion.

AI is reshaping the Neonatal Intensive Care Respiratory Devices Market by embedding intelligent diagnostic and monitoring capabilities directly into respiratory devices, improving real‑time decision‑making and operational performance. Neonatal ventilators and CPAP systems increasingly integrate AI‑based algorithms that analyze respiratory waveforms, vital‑sign trends, and apnea episodes, enabling early alerts and automated ventilator adjustments to ensure optimal oxygenation without excessive manual intervention. One study demonstrated an AI model reduced false apnea alarms by over 30%, increasing nurse efficiency and reducing alert fatigue.

Beyond alarm management, AI‑enabled ventilators support predictive maintenance. Embedded sensors monitor mechanical performance and, through machine learning, forecast component wear—reducing unscheduled downtime by up to 25% in CI environments. Moreover, ventilator manufacturers are deploying AI tools for operational analytics that aggregate usage and performance data across NICUs to identify process bottlenecks and standardize care protocols, fostering continuous improvement cycles without compromising device safety.

Such technologies also empower clinicians: AI‑enhanced respiratory devices offer guided weaning support, suggesting when to gradually reduce support based on individual neonate respiratory patterns. Early adopter NICUs report a reduction in ventilator days by approximately 10%, improving throughput and decreasing cost per treatment episode. Thus, the Neonatal Intensive Care Respiratory Devices Market is evolving from standalone equipment into connected, intelligence‑driven platforms—elevating clinical workflows, asset utilization, and patient safety for decision‑makers focused on operational best practices.

“In 2024, a milestone was reached when an AI‑driven ventilator system demonstrated a 35% reduction in apnea alarm rate and enabled predictive hardware fault alerts 48 hours before failure.”

In the Neonatal Intensive Care Respiratory Devices Market, demand is being driven by technological integration, regulatory protocols, and care delivery shifts. Adoption rates vary across regions, with high‑income economies showcasing rapid integration of multifunction ventilator platforms while emerging markets advance through cost‑effective CPAP units. Hospital network expansion and increasing NICU capacity allocations remain critical trends influencing procurement cycles. Additionally, supply chain consolidation among device manufacturers is reshaping competition, as fewer, larger entities offer comprehensive service agreements and regulatory compliance support. Decision‑makers now prioritize interoperability, total cost of ownership, and device lifecycle management when selecting offerings from the Neonatal Intensive Care Respiratory Devices Market.

The rising global incidence of preterm births—estimated at over 10% of live deliveries—has directly increased NICU admissions requiring respiratory support. Hospitals have responded by expanding NICU beds and acquiring advanced ventilation solutions, such as dual‑mode and invasive/non‑invasive hybrid systems. This demand encourages manufacturers to scale up production and accelerate deployment of advanced device portfolios tailored to neonatal physiology and variable lung compliance.

One significant limitation is the high upfront cost involved in purchasing advanced respiratory devices with built‑in monitoring and automation features. Lifecycle maintenance—including servicing, calibration, and replacement parts—can exceed 15% of the purchase price annually. For resource‑constrained hospitals and rural health networks, budget constraints often delay equipment upgrades, resulting in reliance on legacy ventilators or manual CPAP systems that may offer limited automation and lower safety margins.

Home care and ambulatory neonatal respiratory support represent a growing opportunity. With compact, battery‑operated neonatal ventilators and CPAP units now CE‑marked and FDA‑cleared, parents can continue therapy after NICU discharge. This shift reduces hospital occupancy and enables device manufacturers to introduce subscription‑based models covering remote monitoring, wear‑and‑tear service, and software updates—supporting a new consumer channel within the Neonatal Intensive Care Respiratory Devices Market.

A key obstacle is navigating evolving regulatory frameworks—particularly around software‑as‑medical‑device (SaMD), cybersecurity, and data privacy. Standards such as IEC 82304‑1 for software health products and the MDR in Europe require rigorous clinical validation, post‑market surveillance, and risk management. Manufacturers face inconsistent classification and audit requirements across regions, which can delay product launches by 12–18 months and increase compliance costs by up to 20%.

Integration of AI‑Driven Decision Support: Hospitals are increasingly adopting respiratory devices equipped with real‑time AI decision support. Devices now analyze respiratory waveforms to alert when ventilator settings need adjustment. In several NICUs, AI‑assisted adjustments reduced manual recalibrations by 40%, demonstrating measurable labor efficiencies and safer care delivery.

Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Neonatal Intensive Care Respiratory Devices Market. Pre‑bent and cut elements are prefabricated off‑site using automated machines, reducing labor needs and speeding project timelines. Demand for high‑precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Remote Monitoring and Tele‑NICU Synergy: Respiratory devices are increasingly integrated into tele‑NICU networks. NICUs in remote locations deploy connected ventilators that stream vital‑sign data to urban centers. This model reduced patient transfers by 25% and contributed to earlier clinical interventions by up to 2 hours in acute cases, enhancing regional neonatal outcomes.

Eco‑Friendly Device Design and Consumables Reduction: Device manufacturers are responding to environmental policies by introducing reusable respiratory circuits and biodegradable components. Some oxygen hoods now include washable filters and reusable liners, achieving a 30% reduction in single‑use plastic waste and aligning with initiatives to lower lifecycle carbon impact in hospital equipment.

The Neonatal Intensive Care Respiratory Devices Market is segmented by type, application, and end-user, each contributing uniquely to market dynamics. The type segment includes a range of devices, from basic oxygen delivery systems to advanced, integrated ventilator platforms. Applications span across treatment modalities for respiratory distress syndrome, bronchopulmonary dysplasia, apnea of prematurity, and other neonatal pulmonary conditions. The end-user segmentation primarily encompasses hospitals, neonatal intensive care units (NICUs), specialty clinics, and home care settings. Demand patterns are shaped by the growing complexity of neonatal care, the rising survival rates of preterm infants, and the need for specialized respiratory support. Advanced NICUs remain the key deployment ground for multi-functional ventilator systems, while home care units are gaining attention due to advances in portable and telemonitoring-enabled devices. These segmentation insights are essential for stakeholders to align strategies with evolving clinical demands, infrastructure capabilities, and operational workflows across diverse care settings.

Neonatal respiratory support products are categorized into ventilators, CPAP devices, oxygen delivery systems, high-frequency ventilators, and others such as nebulizers and resuscitators. Among these, ventilators lead the segment due to their clinical necessity in managing severe respiratory distress and providing invasive support. These devices offer precision control of oxygen concentration, tidal volume, and pressure settings tailored to neonatal physiology. Their integration with monitoring systems and alarm algorithms ensures patient safety and clinician confidence during intensive care.

The fastest-growing type is CPAP (Continuous Positive Airway Pressure) devices. Their non-invasive nature, ease of use, and suitability for both in-hospital and home-based care environments have contributed to rising demand. Technological advancements like bubble CPAP and heated humidification options are enhancing patient comfort and outcomes.

Other device types like high-frequency ventilators are used for extreme cases requiring gentle ventilation strategies, particularly in extremely low birth weight infants. Oxygen hoods and nebulizers serve more niche applications, particularly in transitioning neonates off mechanical support.

Key application areas in the Neonatal Intensive Care Respiratory Devices Market include respiratory distress syndrome (RDS), bronchopulmonary dysplasia (BPD), transient tachypnea of the newborn (TTN), apnea of prematurity, and congenital pneumonia. Respiratory distress syndrome (RDS) remains the dominant application due to its prevalence in preterm infants. Effective ventilation strategies are critical during the first 48 hours post-birth to reduce morbidity, making RDS a focus area for hospitals and equipment providers.

The fastest-growing application is apnea of prematurity. Increasing awareness, along with early diagnosis using AI-supported monitoring systems, is enabling proactive respiratory intervention. Devices with apnea-detection and auto-adjusting features are increasingly favored in NICUs and specialized clinics.

Other conditions such as congenital pneumonia and TTN also utilize these respiratory devices, particularly in postnatal units and pediatric emergency care. Though less frequent, these applications require reliable equipment with rapid-response features, particularly in facilities with rotating neonatal staff or limited on-site pulmonologists.

The end-user segmentation highlights hospitals and neonatal intensive care units (NICUs) as the primary users of neonatal respiratory devices. These settings offer the infrastructure, expertise, and high patient turnover necessary to justify the investment in advanced multi-mode respiratory systems. NICUs are equipped to handle complex respiratory support with integrated monitoring, weaning protocols, and emergency backup systems.

The fastest-growing end-user group is home care and ambulatory services. Advances in compact ventilator design, telehealth integration, and battery-operated CPAP devices have enabled extended care for neonates post-discharge. This segment is expanding particularly in regions with high insurance coverage and telemedicine reimbursement.

Other end-users, such as pediatric specialty clinics and research institutions, contribute to market activity by adopting devices for outpatient monitoring and clinical trials. These users prioritize devices that are portable, easy to sanitize, and compatible with digital platforms, helping to expand product innovation pipelines and foster clinical validation of new technologies.

North America accounted for the largest market share at 39.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

The dominance of North America is attributed to its advanced neonatal care infrastructure, high healthcare expenditure, and rapid adoption of smart respiratory devices. In contrast, Asia-Pacific's growth trajectory is driven by increasing NICU investments in countries like India and China, along with rising awareness of neonatal healthcare standards. Additionally, regional governments are allocating more public health funding toward maternal and infant care infrastructure. The market is further supported by digital health transformation initiatives, expanding tele-NICU networks, and local manufacturing incentives for neonatal respiratory equipment. While Europe holds a mature share with strong regulatory frameworks, developing regions such as South America and the Middle East & Africa are witnessing slow but steady increases in demand due to improving healthcare access.

North America held 39.6% of the global Neonatal Intensive Care Respiratory Devices Market in 2024, solidifying its position as the leading regional contributor. The U.S. and Canada are central to this dominance, supported by robust NICU infrastructure, extensive insurance coverage, and substantial R&D investments. Key industries driving demand include hospital systems, pediatric specialty clinics, and home care service providers. Notable regulatory frameworks such as the FDA's 510(k) clearance pathway and fast-track designations have accelerated the market introduction of next-gen neonatal respiratory systems. Technological trends in the region are shaped by AI-enhanced ventilation, cloud-based device monitoring, and predictive analytics platforms, enabling safer and more personalized respiratory care for preterm and critically ill neonates.

Europe captured approximately 28.2% of the Neonatal Intensive Care Respiratory Devices Market in 2024, with leading countries including Germany, the United Kingdom, and France. These markets benefit from well-established healthcare systems, high neonatal survival rates, and proactive adoption of innovative medical technologies. Regulatory bodies such as the European Medicines Agency (EMA) and adherence to MDR (Medical Device Regulation) standards play a significant role in quality assurance and product approvals. Sustainability initiatives, including eco-friendly manufacturing standards and reusable device protocols, are gaining momentum across key European countries. The integration of respiratory systems with hospital EHRs (Electronic Health Records) and the use of automation in neonatal care pathways are advancing steadily, improving workflow efficiencies and patient safety.

Asia-Pacific ranked as the fastest-growing region in the Neonatal Intensive Care Respiratory Devices Market in 2024, driven by rapid urbanization, rising preterm birth rates, and expanding public-private partnerships in healthcare. Top consuming countries include China, India, and Japan, where large-scale investments in neonatal intensive care units are underway. In China, a national push to modernize Tier 2 and Tier 3 hospitals is contributing to increased demand for high-performance ventilators. Meanwhile, India’s Ayushman Bharat program is boosting neonatal health service coverage. Infrastructure trends reveal growing domestic manufacturing capacity for respiratory devices, while regional innovation hubs such as Singapore and South Korea are advancing portable device development, AI-based respiratory monitoring, and telemedicine integration.

In 2024, Brazil and Argentina were the major contributors to the South America Neonatal Intensive Care Respiratory Devices Market, which accounted for 6.1% of global volume. Brazil leads in NICU installations across public hospitals due to its unified healthcare system (SUS), which supports neonatal equipment procurement. Argentina is witnessing rising private sector investments in advanced neonatal facilities. Infrastructure trends reveal a gradual modernization of hospitals with new respiratory device deployment. Government incentives for medical equipment imports and local partnerships with global manufacturers are enhancing market accessibility. Despite economic challenges, targeted neonatal health programs and regional training initiatives are sustaining growth in neonatal respiratory care.

The Middle East & Africa region represented approximately 5.4% of the Neonatal Intensive Care Respiratory Devices Market in 2024. Key growth countries include the United Arab Emirates and South Africa, both investing heavily in neonatal healthcare infrastructure and capacity building. Regional demand is closely tied to broader healthcare reforms, such as the UAE’s Vision 2031 health strategy and South Africa’s national neonatal care guidelines. The market is supported by public-private partnerships and donations from global health organizations. Technological modernization trends include procurement of portable ventilators, remote monitoring-enabled CPAP units, and localized manufacturing initiatives in Gulf countries. Trade agreements and regulatory streamlining are enabling faster access to essential neonatal respiratory equipment across African and Middle Eastern regions.

United States - 34.7% Market Share

High production capacity and widespread hospital adoption of integrated respiratory care systems drive U.S. leadership in the Neonatal Intensive Care Respiratory Devices Market.

China - 15.2% Market Share

Rapid NICU infrastructure expansion and growing domestic manufacturing capabilities support China's strong position in the Neonatal Intensive Care Respiratory Devices Market.

The Neonatal Intensive Care Respiratory Devices Market is highly competitive, with over 40 active players operating at global and regional levels. These companies range from established medical device manufacturers to specialized neonatal care solution providers. The competitive landscape is defined by innovation, regulatory compliance, and rapid technology adoption. Leading players are focusing on developing compact, multi-functional, and AI-integrated devices to address rising demand for personalized and non-invasive respiratory care.

Strategic initiatives such as product launches, mergers, and regional expansions are reshaping the market. In 2023 and 2024, several key players introduced ventilators with integrated monitoring and automated weaning protocols, enhancing real-time clinical decision-making. Partnerships between device manufacturers and digital health companies are fueling innovation, especially in tele-NICU systems and remote monitoring capabilities.

Global players are also establishing local manufacturing units and service centers in high-growth regions like Asia-Pacific and Latin America to improve market access and reduce lead times. Additionally, intellectual property filings related to neonatal ventilation algorithms and data-driven respiratory therapy have increased, signaling a push toward proprietary, value-added offerings. The competitive environment continues to evolve as companies seek differentiation through advanced design, digital transformation, and regulatory agility.

GE HealthCare

Drägerwerk AG & Co. KGaA

Medtronic plc

Koninklijke Philips N.V.

Inspiration Healthcare Group

Vyaire Medical, Inc.

Hamilton Medical AG

Fisher & Paykel Healthcare Corporation Limited

Smiths Medical (now ICU Medical)

Neotech Products LLC

Technological advancements are reshaping the Neonatal Intensive Care Respiratory Devices Market, focusing on smarter, more precise, and non-invasive respiratory solutions. A key trend is the integration of AI and machine learning within ventilators and CPAP systems. These technologies enable real-time waveform analysis, predictive maintenance, and decision support features. AI-driven alarms and automated weaning systems reduce caregiver burden and optimize oxygen delivery accuracy, improving patient safety.

Microprocessor-controlled ventilators are now standard in tertiary NICUs, offering fine-tuned control over tidal volume and pressure in preterm infants. These systems are increasingly equipped with closed-loop feedback and data-logging functionalities for continuous monitoring and outcome tracking. High-frequency oscillatory ventilators are gaining traction for treating severe respiratory distress in extremely low birth weight infants, offering lung-protective strategies with minimal trauma.

The market is also seeing the rise of wireless respiratory monitors that track apnea, desaturation, and bradycardia events using wearable sensors, providing seamless data flow to clinicians and parental caregivers. Tele-NICU compatibility is another breakthrough, enabling device interoperability with hospital EHR systems and remote consultations.

In manufacturing, 3D printing and advanced polymers are being used to produce precision-molded respiratory components with enhanced biocompatibility. Meanwhile, sustainable innovations such as biodegradable circuits and reusable device filters are gaining relevance, driven by hospital sustainability goals.

• In March 2024, Medtronic launched a new neonatal ventilator with AI-guided pressure support that adapts breath-to-breath, reducing manual adjustments and improving oxygenation outcomes in preterm infants by 12%.

• In November 2023, Dräger introduced an integrated neonatal CPAP and humidification system designed for use in mobile NICU units, enhancing patient mobility and reducing equipment footprint by 30%.

• In April 2024, Philips debuted a wearable neonatal respiratory monitor compatible with cloud-based telehealth platforms, enabling round-the-clock data streaming and parental access for post-discharge care.

• In September 2023, Hamilton Medical opened a new manufacturing facility in India to produce compact ventilators locally, reducing delivery times by 40% and improving accessibility in South Asia.

The Neonatal Intensive Care Respiratory Devices Market Report provides a comprehensive examination of the market landscape, covering essential parameters including product types, applications, technologies, and end-user segments. The analysis includes ventilators, CPAP systems, oxygen delivery devices, high-frequency ventilators, and auxiliary tools used in neonatal respiratory care. Each type is analyzed for its functional role, usage frequency, and innovation trends in clinical environments.

Applications covered in the report include respiratory distress syndrome, apnea of prematurity, bronchopulmonary dysplasia, transient tachypnea, and other neonatal pulmonary complications. These are mapped against demand trends, clinical advancements, and infrastructure developments across key geographies.

The report offers insights across major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with country-level analysis for high-impact markets such as the U.S., China, India, Brazil, and the UAE. It also considers emerging or niche end-users like home care providers and tele-NICU networks, emphasizing how technological integration is enabling expanded use cases.

In addition to regional and segmental breakdowns, the report addresses current innovation areas such as AI integration, wireless monitoring, and sustainable device development. This scope enables industry leaders, suppliers, and healthcare decision-makers to align their strategies with ongoing and future market directions.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 194.0 Million |

| Market Revenue (2032) | USD 282.3 Million |

| CAGR (2025–2032) | 4.8 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GE HealthCare, Drägerwerk AG & Co. KGaA, Medtronic plc, Koninklijke Philips N.V., Inspiration Healthcare Group, Vyaire Medical, Inc., Hamilton Medical AG, Fisher & Paykel Healthcare Corporation Limited, Smiths Medical (now ICU Medical), Neotech Products LLC |

| Customization & Pricing | Available on Request (10 % Customization is Free) |