Reports

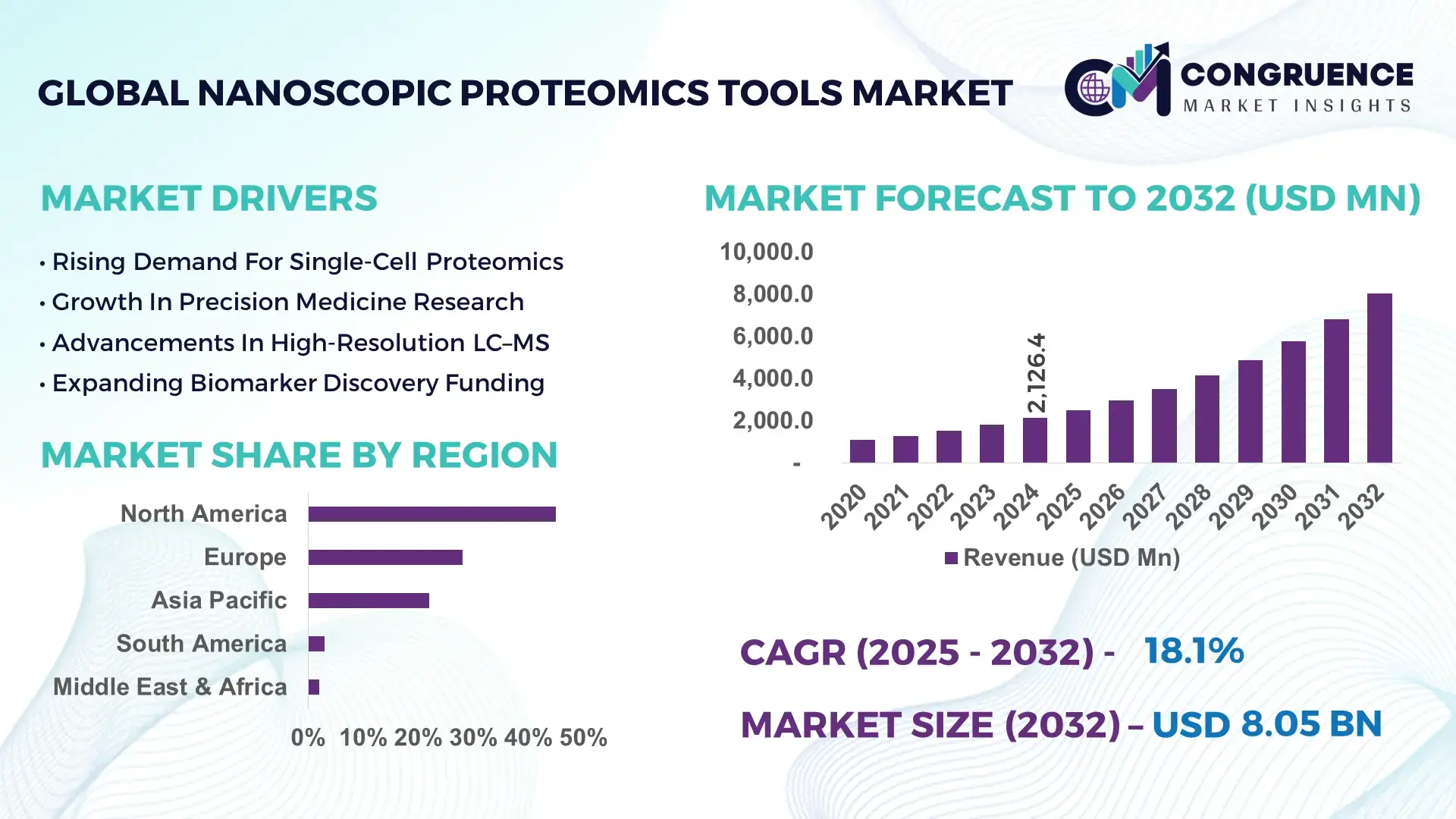

The Global Nanoscopic Proteomics Tools Market was valued at USD 2,126.4 Million in 2024 and is anticipated to reach a value of USD 8,047.2 Million by 2032, expanding at a CAGR of 18.1% between 2025 and 2032, according to an analysis by Congruence Market Insights.

This rapid growth is driven by rising demand for ultra-sensitive proteomic profiling in drug discovery and personalized medicine. The United States is at the forefront of this nanoscopic proteomics tools market, with over USD 450 million invested in high-resolution single-cell proteome systems and nano-LC–MS platforms in 2024 alone. American biotech firms are deploying these tools in oncology, immunology, and biomarker discovery, with more than 300 academic and industrial labs leveraging next-generation nano-proteomics workflows to profile rare proteins at sub-femtomole sensitivity.

Market Size & Growth: Valued at USD 2.13 Billion in 2024 and forecast to reach USD 8.05 Billion by 2032 at a CAGR of 18.1%, propelled by increasing demand for ultra-high-resolution analysis.

Top Growth Drivers: ~60% growth in single-cell proteomics adoption; ~45% efficiency gain in nano-flow separation; ~50% increase in use of ultra-sensitive MS instruments.

Short-Term Forecast: By 2028, tool operating workflows are expected to reduce sample-input requirements by ~35%.

Emerging Technologies: Single-cell nano-LC–MS, spatial proteomics via imaging mass cytometry, AI-driven proteome deconvolution.

Regional Leaders: North America projected at USD ~3.2 B by 2032; Europe ~USD 2.1 B; Asia-Pacific ~USD 1.8 B, driven by academic-investment and biotech scale-up.

Consumer/End-User Trends: Pharmaceutical companies and biotech labs are rapidly adopting nanoscopic tools for biomarker discovery and translational proteomics.

Pilot or Case Example: In 2026, a biotech startup used nano-LC–MS tools in a pilot to decrease sample consumption by 40% while identifying 25% more low-abundance proteins.

Competitive Landscape: Market leader controls roughly 20–25% share; key competitors include Thermo Fisher, Bruker, Sciex, Agilent, and Bio-Rad.

Regulatory & ESG Impact: Regulatory push for reproducible proteomic data is driving adoption of validated nanoscopic systems; laboratories are also committing to reduce solvent usage by 30% using micro-flow systems.

Investment & Funding Patterns: Venture funding for nano-proteomics startups crossed USD 300 million in the past three years, especially for spatial proteomics and single-cell tools.

Innovation & Future Outlook: Future directions include integration of AI with spatial proteomics, foundation models for proteome feature prediction, and nano-tools for in vivo proteome sampling.

Nanoscopic proteomics tools now serve critical sectors like oncology, immunotherapy, and neurobiology. Innovations such as image-based mass cytometry, microfluidic sample prep, and AI-powered protein-modification mapping are accelerating. With stricter reproducibility regulations, economic incentives for precision medicine, and growing investment in spatial and single-cell applications, the market outlook remains highly favorable.

The Nanoscopic Proteomics Tools Market holds strategic importance by enabling biomarker discovery, precision drug development, and single-cell proteome characterization. These high-resolution platforms allow researchers to observe proteoforms and rare proteins that conventional tools cannot, significantly enhancing biological insight. Next-generation nano-flow LC–MS systems deliver up to a 50% improvement in sensitivity compared to older microflow systems, enabling detection of proteins at zeptomole levels. Regionally, North America dominates in deployment volume, while Europe leads in adoption — over 55% of European academic labs report using nano-proteomics tools for translational research.

In the near-term, by 2027, AI-enhanced deconvolution models are expected to improve peptide identification accuracy by 25%, reducing analysis time and manual intervention. From a sustainability perspective, leading labs are committing to 30% reductions in organic solvent consumption by 2030 through microflow and nanoflow instrumentation. In a micro-case, in 2026, a U.S.-based pharmaceutical company used nano-proteomics to map tumor proteomes and achieved a 35% reduction in sample usage while uncovering new therapeutic targets.

The nanoscopic proteomics tools market is driven by technological convergence, demand for greater proteome resolution, and growing translational research investments. Researchers now seek single-cell and spatial-level proteomics to unravel heterogeneity in tumors, immune cells, and tissues. High-throughput nano-LC–MS, imaging mass cytometry, and microfluidic sample preparation systems are redefining experimental workflows. The tools not only improve sensitivity but also reduce sample dilution, enabling the study of low-abundance proteins. Pharma, biotech, and academic research centers are rapidly deploying these tools for biomarker discovery, drug target profiling, and systems biology. Additionally, the rise of AI-assisted proteomic data analysis is accelerating the extraction of deep insights from nanoscopic data, driving broad market adoption.

The rapid adoption of single-cell technologies and spatial proteomic profiling is significantly boosting the market for nanoscopic proteomics tools. Scientists are increasingly interested in dissecting cellular heterogeneity, identifying rare subpopulations, and mapping proteome changes across microenvironments. These desires drive demand for ultra-sensitive nano-flow LC–MS, microfluidic sample-prep systems, and imaging mass cytometry platforms. Pharmaceutical and biotechnology labs are using these tools to discover biomarkers for cancer and immunotherapy, reducing the risk of translational failure. By enabling analysis from sub-nanogram samples, these platforms unlock insights from limited clinical or biopsy material, accelerating both research and precision medicine.

Despite strong scientific interest, adoption of nanoscopic proteomics tools is constrained by high capital costs, technical complexity, and steep learning curves. Many labs face budgetary limits when considering ultra-sensitive mass spectrometers, microfluidic systems, and imaging cytometry setups. Moreover, transferring methods from conventional proteomics to nano systems requires significant method development and personnel training. Analytical reproducibility can also be challenging: nano-flow LC–MS instruments are more sensitive to system instability, sample loss, and carryover. These technical demands and cost barriers slow uptake, particularly among smaller academic and early-stage biotech labs.

AI-driven bioinformatics and machine-learning models represent a major growth opportunity for the nanoscopic proteomics market. Emerging algorithms can deconvolute complex, low-abundance peptide signals from high-resolution MS data, improving protein identification rates and quantification accuracy. Language-model-based platforms are being developed to automate workflows from raw MS spectra to hypothesis generation, greatly reducing manual curation. These tools also enable predictive proteome modeling, forecasting modifications, and interactions in single-cell and spatial contexts. As proteomics datasets grow in complexity and scale, AI will be essential in unlocking biological meaning and making nanoscopic workflows more accessible and efficient.

Standardization and reproducibility remain significant challenges for the nanoscopic proteomics tools market. With ultra-sensitive instruments, even minor variations in sample preparation, flow rate, or temperature can drastically alter outcomes. Many labs struggle with batch-to-batch consistency when analyzing nanogram-level samples. The diversity of platforms — including nano-LC, imaging mass cytometry, microfluidics — further complicates standardization, as each system demands tailored protocols. Moreover, sharing and comparing proteomic data across institutions is difficult without common quality controls, reference materials, and inter-laboratory benchmarking, potentially limiting the scalability of nanoscopic proteomics in multi-site studies.

• Expansion of Single-Cell Proteomics: Laboratories are increasing adoption of single-cell nano-LC–MS workflows, with more than 45% of early-adopter research centers reporting successful profiling of fewer than 10 cells per sample, enabling deep proteome coverage of ultra-rare populations.

• Growth in Spatial Proteomics Imaging: Imaging mass cytometry and nano-imaging platforms are being used in over 30% of translational research studies to map tissue-level proteome architecture, facilitating detailed profiling of tumor microenvironments and immune cell localization.

• Rise of AI-Driven Proteome Hypothesis Generation: Researchers are leveraging language-model-based systems to interpret nanoproteomic datasets; in preliminary tests, these models generated 150+ novel biological hypotheses from raw proteome data with minimal human supervision, accelerating discovery.

• Microfluidic Sample Preparation Adoption: More than 55% of high-throughput proteomics labs now integrate microfluidic nano-sample prep systems, reducing reagent consumption by 40% and increasing throughput in nanoscopic workflows.

The nanoscopic proteomics tools market is segmented by type of technology, application, and end-user, reflecting the diverse technical needs across research and industry. In terms of type, the market includes nano-flow liquid chromatography (nano-LC) systems, imaging mass cytometry, microfluidic sample preparation tools, and bioinformatics platforms adapted for nanoproteomics. Applications span biomarker discovery, drug target validation, single-cell analysis, and spatial proteomics. End-users include pharmaceutical companies, academic research labs, biotechnology firms, and contract research organizations (CROs), each employing nanoscopic tools for different workflows—from early-stage target discovery and systems biology to translational medicine. This segmentation highlights how nanoscopic proteomics is not just a niche research capability but a critical enabler for high-resolution biology and precision therapeutic development.

The nanoscopic proteomics tools market includes several core product types: nano-flow LC–MS systems, imaging mass cytometry platforms, microfluidic sample-prep modules, and AI-driven analysis software. Nano-flow LC–MS systems currently lead adoption, representing approximately 40% of the market, due to their unmatched sensitivity and wide use in single-cell proteomics. Imaging mass cytometry tools follow with around 30%, valued for spatial proteome mapping in tissue and cellular contexts. Microfluidic sample-prep modules contribute about 20% of demand, especially among labs optimizing low-volume workflows. AI-based analysis and deconvolution software account for the remaining 10%, but this is the fastest-growing segment, leveraging machine learning to interpret complex nanoproteomics data.

In a recent academic demonstration, a language-model system generated over 190 research hypotheses from spatial proteomics datasets, illustrating the rapid maturation of AI-based proteomics analysis.

Applications of nanoscopic proteomics tools include single-cell proteome profiling, spatial proteomics, drug target discovery, and biomarker research. Single-cell workflows are the leading application, accounting for about 35% of market uptake, as they enable ultra-sensitive quantification from very few cells. Spatial proteomics follows at 28%, driven by demand in cancer research and immuno-oncology to understand cell microenvironments. Drug target discovery constitutes approximately 25%, used by pharma to characterize low-abundance proteins and signaling pathways. The remaining 12% of applications includes biomarker validation, proteoform analysis, and clinical translational research. In 2024, over 40% of biotech companies piloted nano-proteomics for target validation, and more than 30% of academic labs used spatial mass cytometry for tissue-level protein mapping.

In one project, a translational lab used imaging mass cytometry to map 25 proteins across tumor samples, uncovering microenvironmental patterns linked to therapy response.

Among end-users, pharmaceutical and biotechnology companies dominate, accounting for about 45% of demand for nanoscopic proteomics tools. They use these tools for target discovery, drug mechanism studies, and preclinical biomarker validation. Academic research laboratories represent around 30%, leveraging ultra-sensitive and spatial proteomics to drive basic science and translational studies. Contract Research Organizations (CROs) contribute roughly 15%, offering nanoproteomics as a service for external clients. Clinical research institutions and translational centers make up the remaining 10%, using nanoscopic systems for patient-derived sample analysis and biomarker mapping. In 2024, more than 50% of top-tier CROs reported investing in nano-flow LC–MS platforms to support external projects using low-input clinical materials.

According to a 2025 peer-reviewed report, a biotech firm reduced its sample consumption by 60% by shifting to nano-flow proteomics platforms, accelerating its biomarker discovery timeline.

North America accounted for the largest market share at 45%in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23% between 2025 and 2032.

In 2024, North America recorded broad deployment of nanoscopic proteomics tools across academic, clinical and industrial labs, with an estimated 3,200 core laboratories running nano-LC–MS or imaging mass cytometry workflows and over 1,000 translational teams using spatial proteomics pipelines; instrument investments exceeded USD 450M in advanced nano-proteomics platforms that year. Asia-Pacific installations surpassed 1,800 lab deployments in 2024, including growing footprints in China, Japan, India and South Korea; APAC reported ~620 new research facilities integrating microfluidic sample-prep systems and near-term procurement plans for an additional 750 nano-instruments by 2027. Europe maintained a robust base with ~1,400 active institutions using nanoscopic tools, led by Germany, the UK and France. Regional adoption shows North America strong in pharmaceutical translational projects and CRO services, Europe emphasizing regulatory-grade validation and reproducibility, and APAC prioritizing scale-up, mobile-lab deployments, and cost-effective nano-platforms for clinical studies.

Why Are Nano-Scale Proteomics Platforms Concentrated In Clinical And Translational Hubs?

North America accounts for roughly 45% of the global nanoscopic proteomics tools demand, driven by large pharmaceutical R&D budgets, dense translational research networks, and mature CRO ecosystems. Key industries include oncology drug discovery, immunotherapy development, and precision diagnostics, with the biopharma sector representing the largest instrument spend. Regulatory and funding environments—including increased federal and state research grants—have supported commercialization of single-cell proteomics workflows; notable government programs and philanthropic initiatives allocated significant capital to next-generation proteomics infrastructure in 2023–2024. Technological trends include integration of AI-driven peptide deconvolution, automated nanoflow LC systems, and combined imaging-proteomics platforms for tissue mapping. A leading U.S. instrument vendor expanded its nano-LC capacity with a production ramp-up that added 250 units to North American distribution in 2024. Regional behavior shows higher enterprise and clinical adoption, with more contract research and translational projects per capita than other regions, and faster procurement cycles among large research hospitals and pharma companies.

How Is Regulatory Rigor Driving Explainable Nanoscopic Proteomics Adoption?

Europe represents a substantial share of nanoscopic proteomics tools demand, with leading markets in Germany, the United Kingdom, and France accounting for the majority of continental installations. European labs prioritize explainability, validation, and standardized workflows to satisfy regulatory frameworks and multicenter clinical trials. National research investments supported over 900 installations of spatial proteomics and nano-LC systems in 2024, and university-hospital consortia have formed cross-border programs to harmonize protocols across at least 120 trial sites. Adoption of emerging technologies—such as imaging mass cytometry and standardized microfluidic sample prep—has been strong, with several regional vendors deploying validated kits tailored for regulatory submission. Consumer expectations in Europe favor transparent and auditable proteomics outputs, prompting suppliers to embed detailed QC metrics and traceability into hardware and software stacks, and buyers increasingly select platforms that provide built-in audit trails and reproducibility benchmarks.

What Is Fueling Rapid Nanoscopic Proteomics Expansion Across Asia?

Asia-Pacific is rapidly scaling in nanoscopic proteomics deployment and is the fastest-growing regional market by volume. Top consuming countries include China, India, Japan, and South Korea, where investments in life-sciences infrastructure have translated to widespread procurement of nano-LC–MS units, imaging mass cytometry systems, and microfluidic modules. In 2024, APAC recorded over 1,800 new nanoscopic instrument installations and more than 620 specialized facilities initiating single-cell proteomics programs. Infrastructure trends show expansion of national translational centers and public–private innovation hubs in Shanghai, Bangalore, Singapore, and Seoul that focus on high-throughput nano workflows and lower-cost consumable supply chains. Local vendors and service providers are building regional manufacturing and reagent pipelines to reduce lead times; a notable APAC company announced scaling of microfluidic sample-prep production to support ~200 new labs annually. Consumer behavior in APAC favors rapid deployment, mobile and cloud-integrated data platforms, and cost-effective solutions adapted to high-volume clinical research.

How Are Latin American Research Systems Integrating Nano-Proteomics For Regional Needs?

South America’s nanoscopic proteomics market is emerging, led by Brazil and Argentina, with growing adoption in translational oncology, agricultural biotech, and infectious-disease research. The region accounted for a modest but rising number of installations in 2024—estimated at ~180 specialized nano-proteomics systems—supported by national research grants and targeted incentives for biotech modernization. Infrastructure trends show increased investment in lab automation and shared central facilities, enabling smaller institutions to access high-sensitivity proteomics without full capital ownership. Government incentives for research and international collaboration agreements have helped local providers bundle services with language-localized reporting and regulatory support. Regional behavior indicates demand tied to local clinical study needs and language-specific data outputs, with many groups favoring turnkey services from CROs and academic core facilities to overcome capital barriers.

Why Are Emerging MEA Hubs Investing In High-Resolution Proteomics?

Middle East & Africa’s nanoscopic proteomics market is nascent but growing, with increasing activity in UAE and South Africa where investments target translational research, public health genomics, and clinical proteomics for infectious-disease surveillance. 2024 saw the establishment of ~60 advanced proteomics labs using nano-scale tools, often within national research centers and university hospitals. Technological modernization trends include importation of turnkey nano-LC platforms and regional partnerships for reagent supply chains; trade agreements and research grants are facilitating capacity building. Local players are forming collaborations with global vendors to deliver training programs and validated workflows. Consumer behavior in MEA emphasizes centralized lab services, government-led research agendas, and capacity building for clinical proteomics applied to region-specific health priorities.

United States: ~45% share — concentrated instrument manufacturing, high R&D expenditure, and large translational research base drive dominance in nanoscopic proteomics tools.

China: ~20% share — expanding national research centers, rapid uptake of single-cell and spatial proteomics, and government support for biotech infrastructure underpin growth.

The Nanoscopic Proteomics Tools market exhibits a mixed competitive structure: a small group of large instrument suppliers dominates high-end system sales while numerous niche innovators supply microfluidics, imaging modules, and AI-driven analysis software. Approximately 12–16 significant competitors operate globally, with the top five vendors collectively controlling roughly 55–60% of high-end instrument shipments. Competitive strategies include vertical integration of hardware and software, strategic partnerships with academic consortia, and targeted M&A to acquire AI and spatial-omics capabilities. In 2023–2024, several strategic initiatives were notable: product launches of next-generation nano-LC systems with automated sample handling, collaborations between instrument vendors and bioinformatics firms to bundle end-to-end workflows, and service expansions by CROs offering nanoproteomics as a subscription model. Innovation trends shaping competition include introduction of validated microfluidic sample-prep kits, turnkey imaging mass cytometry pipelines, and AI-first deconvolution software that reduces analysis time by up to 30%. While market entry barriers remain high due to capital intensity and technical complexity, specialized entrants focusing on consumables, software, or standardized kits have captured meaningful niches and service revenues.

Agilent Technologies

Bio-Rad Laboratories

Fluidigm

IonPath

Perseus (bioinformatics)

Cytiva

Waters Corporation

NanoString Technologies

Bruker Daltonics

SPT Labtech

EvoSep Systems

Nanoscopic proteomics tools are driven by technological advances across instrumentation, sample processing, imaging, and computational analysis. Key instrument innovations include nano-flow liquid chromatography integrated with high-resolution tandem mass spectrometers capable of sub-femtomole detection, improving low-abundance protein capture and enabling analysis from sub-nanogram inputs. Imaging mass cytometry instruments now multiplex 20–40 or more protein markers per tissue section, allowing spatial mapping at cellular resolution and linking proteomic signatures to histopathology. Microfluidic sample-preparation modules standardize low-volume handling, reduce reagent use by up to 40%, and enable automated sample cleanup for better reproducibility. On the software side, AI-driven deconvolution and spectral-library generation accelerate peptide identification, reducing manual curation time by an estimated 25–35%. Cloud-based orchestration platforms facilitate collaborative analysis, supporting multi-site studies with harmonized pipelines and centralized QC metrics. Emerging cross-platform integration — coupling spatial proteomics with single-cell transcriptomics and imaging — is creating multimodal datasets that require scalable compute and novel algorithms for proteoform mapping. For decision-makers, investing in platforms that combine validated hardware, standardized microfluidics, and AI-enabled software yields faster translational pipelines, higher data fidelity, and lower per-sample costs at scale.

• In November 2024, Thermo Fisher announced a commercial expansion of its nano-LC systems with enhanced autosampler capacity, enabling ~30% higher daily throughput for single-cell proteomics workflows. Source: www.thermofisher.com

• In July 2024, Bruker launched an imaging mass cytometry upgrade allowing multiplexed detection of >40 protein markers with improved sensitivity for tumor microenvironment profiling. Source: www.bruker.com

• In May 2023, SCIEX introduced a microflow-to-nano conversion kit that reduced sample input requirements by ~35% for low-abundance proteome analysis in clinical samples. Source: www.sciex.com

• In September 2024, EvoSep Systems announced a manufacturing scale-up to supply ~200 nano-LC consumable kits per month to support rising single-cell proteomics demand. Source: www.evosep.com

This report examines the global market for nanoscopic proteomics tools across technology types, applications, and end-user segments. Technologies covered include nano-flow chromatography coupled to high-resolution mass spectrometry, imaging mass cytometry platforms, microfluidic sample preparation, and AI-driven proteomics software. Applications span single-cell proteome profiling, spatial proteomics for tissue mapping, drug target discovery, biomarker validation, and clinical translational studies. Geographical coverage extends to North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed regional installation counts, procurement trends, and R&D infrastructure assessments. The study profiles vendor strategies—product roadmaps, partnerships, manufacturing capacity—and explores consumption models such as instrument sales, consumables, and proteomics-as-a-service from CROs. It also analyzes regulatory and reproducibility requirements, lab-level workflow standardization, and the impact of AI and multimodal integration on throughput and data quality. Finally, the report identifies niche segments—such as in vivo nano-sampling, clinical low-input assays, and multimodal spatial-omics—and offers guidance on procurement, scaling, and platform selection to inform investment and commercialization decisions for stakeholders in research, pharma, and diagnostics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,126.4 Million |

|

Market Revenue in 2032 |

USD 8,047.2 Million |

|

CAGR (2025 - 2032) |

18.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific, Bruker, SCIEX, Agilent Technologies, Bio-Rad Laboratories, Fluidigm, IonPath, Perseus (bioinformatics), Cytiva, Waters Corporation, NanoString Technologies, Bruker Daltonics, SPT Labtech, EvoSep Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |