Reports

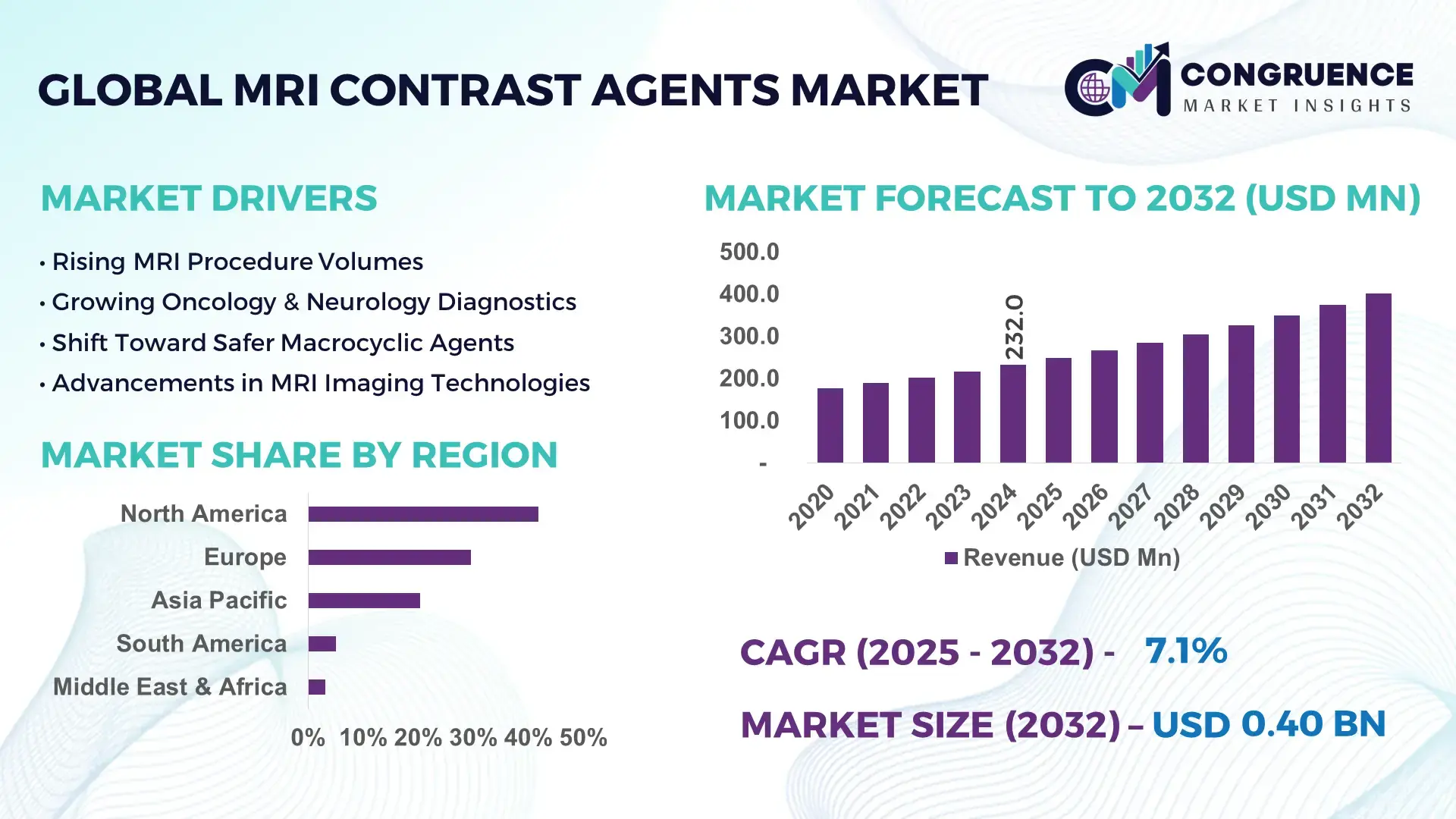

The Global MRI Contrast Agents Market was valued at USD 232.0 Million in 2024 and is anticipated to reach a value of USD 401.6 Million by 2032 expanding at a CAGR of 7.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth trajectory is supported by the rising clinical reliance on high-resolution diagnostic imaging for oncology, neurology, and cardiovascular disease assessment.

The United States represents the dominant country in the global MRI Contrast Agents Market, underpinned by strong domestic production capacity and sustained capital investment in diagnostic imaging infrastructure. The U.S. operates more than 38,000 MRI scanners, accounting for over 40% of global installed MRI systems, driving consistent contrast agent utilization. Annual healthcare R&D spending exceeds USD 200 billion, with a significant share directed toward imaging chemistry, gadolinium alternatives, and AI-optimized contrast dosing. Advanced applications such as functional MRI, perfusion imaging, and oncology-focused contrast protocols are widely adopted across hospitals and outpatient imaging centers. Technological advancements include macrocyclic gadolinium agents with improved stability and the accelerated clinical evaluation of manganese-based and iron-oxide contrast agents, supporting safer, high-frequency imaging workflows.

Market Size & Growth: Valued at USD 232.0 Million in 2024, projected to reach USD 401.6 Million by 2032, growing at a CAGR of 7.1%, driven by expanding MRI procedure volumes and precision diagnostics.

Top Growth Drivers: Oncology imaging adoption (42%), neurological disorder diagnostics (31%), cardiovascular MRI utilization (27%).

Short-Term Forecast: By 2028, AI-assisted contrast dose optimization is expected to reduce agent wastage by 18%.

Emerging Technologies: Macrocyclic gadolinium agents, gadolinium-free contrast chemistries, AI-guided contrast administration.

Regional Leaders: North America (USD 145.0 Million by 2032) with protocol standardization; Europe (USD 112.4 Million by 2032) driven by safety regulations; Asia Pacific (USD 98.1 Million by 2032) led by diagnostic infrastructure expansion.

Consumer/End-User Trends: Hospitals account for nearly 62% of usage, followed by diagnostic imaging centers at 28%.

Pilot or Case Example: In 2023, a U.S. hospital network reduced contrast dosage per scan by 15% using AI-based imaging protocols.

Competitive Landscape: Market leader holds ~24% share, followed by GE HealthCare, Bayer AG, Bracco Imaging, Guerbet, and Lantheus.

Regulatory & ESG Impact: Tighter regulations on gadolinium retention are accelerating adoption of safer macrocyclic agents.

Investment & Funding Patterns: Over USD 1.1 billion invested globally in contrast agent innovation and imaging safety programs.

Innovation & Future Outlook: Integration of AI, safer molecular designs, and personalized imaging protocols will shape next-generation MRI diagnostics.

The MRI Contrast Agents Market is influenced by oncology contributing approximately 38% of total usage, followed by neurology at 29% and cardiology at 18%. Recent innovations include high-relaxivity agents and gadolinium-free compounds improving safety profiles. Regulatory scrutiny on metal deposition, regional consumption growth in Asia Pacific, and rising preventive diagnostics continue to define future market direction.

The MRI Contrast Agents Market holds strategic relevance as healthcare systems increasingly prioritize early, accurate, and non-invasive diagnostics. Advanced contrast agents enhance lesion detectability, tissue characterization, and functional imaging, directly influencing clinical decision-making across oncology, neurology, and cardiology. Macrocyclic gadolinium agents deliver approximately 30% higher molecular stability compared to older linear agents, reducing long-term patient exposure risks and supporting regulatory compliance.

From a technology benchmark perspective, AI-guided contrast dosing delivers nearly 20% improvement in imaging efficiency compared to fixed-dose administration standards. Regionally, North America dominates in volume due to its extensive MRI installed base, while Europe leads in adoption of safety-optimized agents with nearly 58% of imaging centers transitioning to macrocyclic formulations. By 2027, AI-driven imaging workflow optimization is expected to cut scan repetition rates by 22%, improving patient throughput and operational efficiency.

Compliance and ESG considerations are becoming central, with firms committing to reducing gadolinium waste by up to 25% through recyclable packaging and dose-minimization protocols by 2030. In 2024, Germany achieved a 17% reduction in contrast agent consumption per scan by implementing standardized imaging protocols across public hospitals. Looking ahead, the MRI Contrast Agents Market is positioned as a pillar of diagnostic resilience, regulatory alignment, and sustainable growth, supporting value-based healthcare delivery worldwide.

The MRI Contrast Agents Market is shaped by increasing MRI utilization, evolving safety regulations, and technological progress in imaging chemistry. Demand is closely linked to chronic disease prevalence, particularly cancer and neurological disorders, where contrast-enhanced MRI is essential for accurate diagnosis and treatment monitoring. Regulatory oversight on gadolinium deposition has shifted industry focus toward safer molecular structures and alternative metals. Additionally, healthcare providers are optimizing imaging workflows to reduce scan times and improve patient throughput, indirectly influencing contrast agent selection. Regional dynamics vary, with mature markets emphasizing safety and efficiency, while emerging economies focus on expanding diagnostic access.

The increasing reliance on MRI for complex disease evaluation is a primary driver of the MRI Contrast Agents Market. Globally, MRI procedure volumes have grown by over 35% in the last decade, with contrast-enhanced scans accounting for nearly half of all advanced imaging studies. Oncology alone requires contrast use in more than 70% of MRI scans for tumor staging and therapy monitoring. Neurological imaging, including multiple sclerosis and stroke assessment, further accelerates usage. The expansion of outpatient imaging centers has increased scan accessibility, while improvements in scanner resolution necessitate high-performance contrast agents to fully utilize system capabilities.

Heightened awareness of gadolinium retention in human tissues has imposed significant constraints on the MRI Contrast Agents Market. Several health authorities have issued usage restrictions, leading to reduced adoption of certain linear agents. Compliance costs associated with safety testing, labeling updates, and post-market surveillance have increased operational burdens for manufacturers. Hospitals are also implementing stricter contrast usage protocols, lowering average dosage per scan. These factors collectively limit rapid market expansion, particularly in regions with stringent regulatory frameworks.

The development of gadolinium-free contrast agents presents a major growth opportunity for the MRI Contrast Agents Market. Iron-oxide and manganese-based agents are gaining clinical interest due to improved safety profiles. Early trials demonstrate up to 25% enhancement in tissue contrast for specific applications such as liver imaging. Personalized contrast dosing, enabled by AI algorithms, further expands opportunities by aligning safety with diagnostic precision. Emerging markets adopting next-generation MRI systems are likely to favor these innovations.

Cost containment remains a key challenge in the MRI Contrast Agents Market. Contrast agents represent a significant recurring expense for imaging centers, especially high-volume hospitals. Variability in clinical protocols across regions complicates standardization and bulk procurement. Additionally, transitioning to newer agents often requires staff retraining and protocol adjustments, increasing short-term operational costs. These challenges can delay adoption despite clear clinical advantages.

Shift Toward Macrocyclic Contrast Agents: Adoption of macrocyclic agents has increased by over 60% across developed healthcare systems, driven by improved molecular stability and reduced tissue retention. Hospitals report up to 28% lower adverse event monitoring costs after transitioning from linear agents.

AI-Enabled Contrast Dose Optimization: AI-based imaging platforms are enabling 15–20% reductions in contrast volume per scan while maintaining diagnostic accuracy. More than 45% of large imaging centers have integrated automated dosing algorithms into MRI workflows.

Expansion of Outpatient Imaging Networks: Outpatient diagnostic centers now account for approximately 34% of contrast-enhanced MRI procedures globally, reducing inpatient imaging burden and accelerating scan turnaround times by nearly 25%.

Development of Gadolinium-Free Alternatives: Clinical evaluation of non-gadolinium agents has increased by 40% since 2021. Early adoption in liver and vascular imaging has demonstrated contrast efficiency improvements of up to 22%, supporting safer long-term imaging strategies.

The MRI Contrast Agents Market is segmented by type, application, and end-user, reflecting differences in clinical requirements, safety profiles, and imaging workflows. Product segmentation highlights a clear shift toward safer and higher-stability agents as healthcare providers align with stricter regulatory expectations and long-term patient monitoring needs. Application-wise, demand concentration mirrors disease prevalence patterns, with oncology and neurology accounting for the majority of contrast-enhanced MRI procedures due to their reliance on precise tissue differentiation. End-user segmentation is influenced by infrastructure scale, procedure volumes, and reimbursement structures, positioning large hospitals and integrated imaging networks as primary consumers. Across all segments, optimization of diagnostic accuracy, patient safety, and operational efficiency remains the unifying decision driver for procurement and adoption.

The market by type includes macrocyclic gadolinium-based agents, linear gadolinium-based agents, and emerging non-gadolinium contrast agents. Macrocyclic agents currently represent the leading segment, accounting for approximately 54% of total adoption, supported by their higher kinetic stability and lower tissue retention characteristics, which align with evolving safety guidelines. Linear agents hold close to 28% of usage, primarily sustained by cost-sensitive markets and legacy imaging protocols, although their utilization is steadily declining. Non-gadolinium agents, including iron-oxide and manganese-based formulations, represent the fastest-growing type, expanding at an estimated 9.4% CAGR, driven by increasing clinical trials, pediatric imaging needs, and heightened scrutiny of gadolinium deposition. The remaining niche formulations and experimental agents collectively account for around 18% of the market, serving specialized liver, vascular, and functional imaging applications.

By application, oncology imaging leads the MRI Contrast Agents Market, accounting for nearly 38% of total usage, as contrast-enhanced MRI is central to tumor detection, staging, and therapy response monitoring. Neurology applications follow with approximately 27% adoption, driven by routine use in multiple sclerosis, stroke, and neurodegenerative disease assessment. However, cardiovascular MRI represents the fastest-growing application, expanding at an estimated 8.7% CAGR, supported by rising adoption of non-invasive cardiac function and perfusion imaging. Other applications—including musculoskeletal, abdominal, and pediatric imaging—collectively contribute around 35% of demand, serving both acute diagnostics and longitudinal disease monitoring. From an adoption perspective, in 2024, nearly 42% of hospitals in the U.S. reported piloting advanced contrast protocols combining MRI scans with digital patient records to enhance diagnostic confidence. Additionally, over 36% of imaging centers globally indicated increased contrast utilization linked to expanded cancer screening programs.

Hospitals remain the dominant end-user segment, accounting for approximately 62% of total MRI contrast agent consumption, due to high patient volumes, advanced imaging infrastructure, and broad clinical service offerings. Diagnostic imaging centers follow with around 24% adoption, benefiting from increased outpatient imaging demand and faster scan turnaround times. However, specialty clinics and ambulatory care centers are the fastest-growing end-user group, expanding at an estimated 8.9% CAGR, fueled by decentralization of diagnostic services and rising preventive screening initiatives. Other end-users, including academic research institutes and contract research organizations, collectively represent about 14% of the market, supporting clinical trials and imaging innovation. From a usage trend perspective, in 2024, more than 39% of large hospital networks globally reported standardizing macrocyclic agents across all MRI departments, while over 33% of outpatient imaging centers adopted AI-assisted contrast dosing tools to improve efficiency.

North America accounted for the largest market share at 41.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2025 and 2032.

Regional performance in the MRI Contrast Agents Market is strongly correlated with MRI scanner density, healthcare spending intensity, regulatory stringency, and adoption of advanced diagnostic protocols. North America leads due to high MRI utilization rates, with over 120 MRI scans per 1,000 population annually, while Europe follows with a 29.6% share, driven by safety-focused regulatory alignment and standardized imaging protocols. Asia-Pacific currently accounts for approximately 20.4% of global demand, supported by rapid hospital infrastructure expansion and rising diagnostic penetration in China and India. South America and the Middle East & Africa collectively contribute close to 8.2%, reflecting improving access to advanced imaging in urban centers. Variations in contrast agent preference, dosage optimization, and safety compliance further differentiate regional demand patterns.

The region holds an estimated 41.8% share of the global MRI Contrast Agents Market, supported by the world’s highest concentration of MRI scanners and contrast-enhanced procedures. Oncology, neurology, and cardiovascular imaging collectively account for over 70% of contrast utilization across hospitals and outpatient imaging networks. Regulatory actions emphasizing patient safety have accelerated the transition toward macrocyclic agents, with more than 65% of imaging centers standardizing these formulations. Digital transformation trends include AI-assisted contrast dosing and protocol automation, now implemented in approximately 48% of large hospital systems. A leading regional imaging manufacturer has expanded production of high-relaxivity agents to support next-generation MRI platforms. Consumer behavior reflects high acceptance of preventive diagnostics, with contrast-enhanced scans increasingly used for early disease detection and treatment monitoring.

Europe accounts for nearly 29.6% of global market share, with Germany, the UK, and France representing over 60% of regional consumption. Strong oversight by regional regulatory bodies has driven rapid replacement of linear agents, with macrocyclic formulations now used in approximately 68% of contrast-enhanced MRI procedures. Sustainability initiatives emphasize reduced metal exposure and waste minimization, influencing procurement strategies across public healthcare systems. Emerging technologies such as low-dose imaging protocols and AI-supported workflow optimization are adopted in nearly 40% of tertiary hospitals. A prominent European contrast agent manufacturer has focused on reformulating products to meet updated safety thresholds. Consumer behavior shows heightened sensitivity to regulatory compliance, resulting in preference for explainable, safety-validated imaging solutions.

Asia-Pacific ranks as the fastest-growing regional market and currently contributes around 20.4% of global volume. China, Japan, and India together account for more than 75% of regional MRI contrast consumption. Rapid expansion of public hospitals and private diagnostic chains has increased MRI installations by over 30% in the last five years. Manufacturing localization is strengthening, with regional players investing in domestic production of contrast agents to reduce import dependency. Innovation hubs in Japan and South Korea are advancing high-relaxivity and pediatric-safe formulations. Consumer behavior reflects rising awareness of early diagnostics, with urban populations increasingly opting for contrast-enhanced scans as part of preventive health check-ups.

South America represents approximately 5.1% of the global market, led by Brazil and Argentina, which together account for nearly 65% of regional demand. Investments in public healthcare infrastructure and private imaging centers are improving access to advanced MRI services in metropolitan areas. Government initiatives aimed at expanding universal healthcare coverage have increased diagnostic imaging utilization, particularly for oncology and neurological disorders. Regional distributors are partnering with global manufacturers to ensure steady supply of macrocyclic agents. Consumer behavior shows growing reliance on urban diagnostic hubs, with contrast-enhanced imaging adoption rising alongside specialist care availability.

The Middle East & Africa region contributes close to 3.1% of global demand, with the UAE, Saudi Arabia, and South Africa as primary growth countries. Large-scale hospital development programs and medical city projects are expanding MRI capacity, particularly in the Gulf region. Technological modernization includes adoption of high-field MRI systems and digital radiology platforms. Trade partnerships and streamlined import regulations are improving access to advanced contrast agents. A regional healthcare group has expanded its diagnostic network, increasing contrast-enhanced MRI volumes across multiple countries. Consumer behavior varies widely, with higher adoption concentrated in private healthcare settings and urban centers.

United States - 34.2% Market Share: High MRI scanner density, strong clinical adoption, and advanced regulatory frameworks support sustained leadership.

Germany – 9.8% Market Share: Robust healthcare infrastructure, stringent safety regulations, and strong domestic manufacturing presence drive consistent demand.

The MRI Contrast Agents Market competitive landscape exhibits a blend of consolidation among global leaders and active innovation by specialized entities. There are 15+ active competitors with significant market positioning, including multinational firms and regional specialists driving strategic initiatives across product development, partnerships, and capacity expansions. The market shows signs of moderate consolidation, with the top 5 companies collectively accounting for an estimated 60–70% of industry activity due to broad product portfolios, geographic reach, and investment in next-generation offerings.

Key players such as GE Healthcare, Bayer AG, Bracco Imaging S.p.A., Guerbet Group, and Lantheus Medical Imaging are reinforcing competitiveness through strategic product launches, clinical advancements, and collaborative ventures. For example, GE Healthcare completed Phase I clinical development for a macrocyclic manganese-based contrast agent and introduced digital contrast management platforms in 2024, reflecting a shift toward enhanced safety and workflow efficiency. Bracco reported over 1 million examinations using its VUEWAY® (gadopiclenol) agent across 480+ sites by late 2024, demonstrating rapid clinical adoption and competitive strength.

Strategic initiatives such as AI-enhanced contrast injector systems co-developed with Microsoft by Guerbet and digital tracking solutions by GE showcase innovation trends shaping competitive dynamics. Partnerships between major imaging and pharmaceutical firms, alongside expansions of production capacities and regulatory approvals for advanced agents with improved safety profiles, indicate an environment where technological differentiation and strategic alliances are central to maintaining competitive edge. Collectively, this competitive milieu underscores a business landscape where innovation, clinical utility, and network expansion define leadership.

Guerbet Group

Lantheus Medical Imaging

Canon Medical Systems

Siemens Healthineers

Fresenius Kabi

Sanochemia Pharmazeutika

The technological landscape of the MRI Contrast Agents Market is rapidly evolving, driven by advancements that enhance diagnostic precision, optimize patient safety, and streamline clinical workflows. A significant trend is the development of macrocyclic gadolinium-based agents with enhanced relaxivity that require lower dosing while maintaining high imaging quality—a major focus among leading manufacturers. These agents improve lesion visualization across a broad range of clinical indications while addressing concerns about long-term gadolinium retention.

Integration of artificial intelligence (AI) and digital platforms is reshaping how contrast agents are administered and managed. For example, companies like GE Healthcare have introduced integrated contrast management solutions that combine patient monitoring, dosing optimization, and adverse event tracking into unified systems accessible in modern imaging facilities. Similarly, collaborations between contrast agent developers and digital technology partners aim to automate and personalize dosing protocols based on patient characteristics, reducing waste and enhancing imaging consistency.

Emerging non-gadolinium and alternative metal-based agents—including manganese-based chemistries—are progressing through early clinical evaluations, offering potential options for patients with renal concerns or those requiring repeated imaging procedures. Such innovations may expand clinical utility while reducing dependence on traditional gadolinium compounds.

Additionally, technological improvements in supply chain and manufacturing automation are increasing production efficiency and capacity. Major players are expanding fill-finish facilities and optimizing quality control systems to meet global demand, improve reliability, and support scalable deployment of advanced agents. These technological trends underscore the market’s movement toward precision diagnostics, patient-centric solutions, and robust digital workflows, making contrast agents more effective and safer for a wide spectrum of MRI applications.

In October 2024, GE HealthCare announced positive Phase I clinical results for its first-of-its-kind manganese-based macrocyclic MRI contrast agent. The Phase I human trial demonstrated that the investigational agent was well tolerated with no serious adverse events, reinforcing GE HealthCare’s innovation pipeline for alternatives to traditional gadolinium-based agents. Source: www.gehealthcare.com

In April 2023, GE HealthCare expanded its MRI contrast media portfolio with the launch of Pixxoscan (gadobutrol). This macrocyclic, non-ionic gadolinium-based contrast agent was introduced in Europe alongside existing products like Clariscan and Rapiscan, enhancing diagnostic flexibility across a broad range of MRI procedures. Source: www.gehealthcare.com

In November 2024, Bracco Diagnostics Inc. reported that its MRI contrast agent VUEWAY® (gadopiclenol) surpassed one million patient injections. The milestone reflects widespread clinical use across more than 480 customer sites, driven by the agent’s lower gadolinium dose per procedure and strong adoption in routine diagnostic imaging. Source: www.bracco.com

In October 2024, Guerbet’s Gadopiclenol (marketed as Elucirem®) received the JFR 2024 Innovation Award. The recognition in the Jury’s Favorite category at a major radiology event highlighted the agent’s high relaxivity and ability to deliver equivalent image quality with reduced gadolinium dosing. Source: www.guerbet.com

The scope of the MRI Contrast Agents Market Report encompasses a comprehensive examination of global market structures, technological evolution, clinical applications, and geographical distributions. The report outlines detailed segmentation across contrast agent types, such as gadolinium-based, iron oxide-based, and emerging alternative agents, providing insights into differences in chemical composition, relaxivity profiles, and clinical suitability for various imaging scenarios. It further evaluates end-use segments including hospitals, diagnostic imaging centers, and specialized outpatient facilities, reflecting how diverse healthcare infrastructure demands shape product deployment and adoption patterns.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with specific focus on regional consumption patterns, regulatory frameworks, and local production capabilities. This geographical assessment highlights variations in clinical practices, investment levels, and infrastructure readiness, offering decision-makers a nuanced understanding of global dynamics and competitive positioning.

Technological segments within the report analyze advancements in agent formulations, delivery systems, and digital integration—from high-relaxivity macrocyclic agents to AI-enhanced dosing tools and contrast management platforms. It also addresses niche areas such as patient-specific imaging enhancements, safety-optimized chemistries, and evolving regulatory pathways that influence product life cycles and market entry strategies.

Additionally, the report presents strategic profiles of key stakeholders, competitive benchmarking, partnership landscapes, and innovation clusters, aiding business professionals to identify growth opportunities, strategic risks, and investment priorities. The breadth of coverage ensures that decision-makers have visibility into clinical trends, technological disruptions, and regional growth vectors without duplication of previously detailed market data.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 232.0 Million |

| Market Revenue (2032) | USD 401.6 Million |

| CAGR (2025–2032) | 7.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | GE HealthCare; Bayer AG; Bracco Imaging S.p.A.; Guerbet Group; Lantheus Holdings; Canon Medical Systems; Siemens Healthineers; Fresenius Kabi; Sanochemia Pharmazeutika |

| Customization & Pricing | Available on Request (10% Customization Free) |