Reports

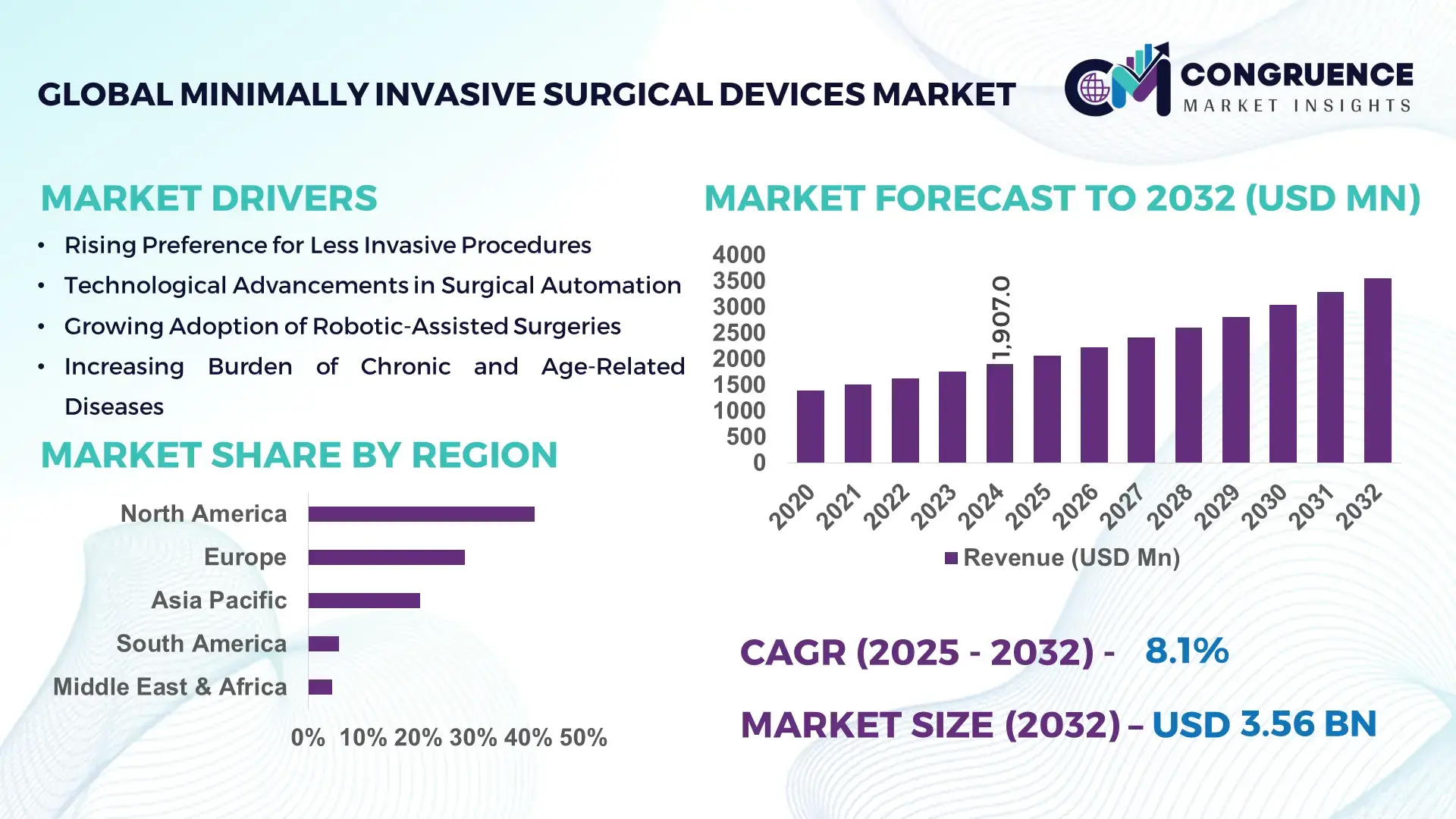

The Global Minimally Invasive Surgical Devices Market was valued at USD 1,907.0 Million in 2024 and is anticipated to reach a value of USD 3,556.0 Million by 2032 expanding at a CAGR of 8.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This trajectory is underpinned by accelerating adoption of image-guided systems, rising outpatient procedures, and increased investment in procedure-specific disposable instruments that shorten OR time and improve patient throughput.

The United States is the leading country in the Minimally Invasive Surgical Devices Market. It hosts over 600 medical device manufacturers and maintains an active medtech VC and corporate investment pipeline exceeding USD 4.2 billion into minimally invasive system development and adjacent disposables between 2020 and 2024. Production capacity is concentrated in multiple advanced manufacturing clusters with more than 120 FDA-registered sterile device production facilities focused on MIS instruments and implants. Clinical adoption is robust: more than 45% of tertiary hospitals reported expanded minimally invasive procedure suites (robotic or laparoscopic) during 2022–2024, and device R&D intensity is reflected in roughly 1,900 related patent filings in the medical-device space over the last five years. Key applications receiving investment include laparoscopic and endoscopic platforms, single-port access instruments, and procedure-specific staplers and energy devices used across general surgery, urology, gynecology, and thoracic surgery.

Market Size & Growth: USD 1,907.0 Million (2024) → USD 3,556.0 Million (2032); CAGR 8.1%; driven by outpatient shift and device miniaturization.

Top Growth Drivers: 52%, 39%, 31%.

Short-Term Forecast: By 2028, OR turnover time to improve by 18% and procedure throughput to increase by 22%.

Emerging Technologies: Robotic-assisted micro-instruments, single-port platforms, augmented-reality (AR) image guidance.

Regional Leaders: North America — USD 1,200M by 2032 (high procedure density); Europe — USD 900M by 2032 (regulatory-driven precision devices); Asia-Pacific — USD 850M by 2032 (rapid hospital expansions).

Consumer/End-User Trends: Growth in ambulatory surgery centers, rising patient preference for shorter stays, and increased insurer support for MIS pathways.

Pilot or Case Example: 2023 hospital pilot reported a 28% reduction in average length-of-stay after adopting single-port laparoscopic kits.

Competitive Landscape: Market leader ~18% (approx.); other major competitors include 4–6 global device manufacturers and 20+ specialized innovators.

Regulatory & ESG Impact: Stricter device sterilization and disposal mandates, and manufacturer targets to reduce single-use plastics in packaging by 30% by 2030.

Investment & Funding Patterns: Recent investment rounds and strategic acquisitions cumulatively exceeded USD 2.6 billion (2020–2024) across growth-stage medtech firms.

Innovation & Future Outlook: Focus on modular robotic end effectors, disposable smart instruments with embedded sensors, and cloud-assisted procedure analytics.

The minimally invasive devices market is concentrated in surgical specialties—general surgery, urology, gynecology, and thoracic—with device families contributing differing usage profiles; visualization and energy devices underpin the bulk of tooling innovations, while disposable, procedure-specific kits accelerate standardization and reduce sterilization cycles.

Minimally invasive surgical devices are strategically critical because they enable hospitals and outpatient centers to deliver higher volumes of procedures with improved clinical outcomes and lower per-case resource consumption. Robotic-assisted micro-instruments deliver an estimated 18% improvement in precision-controlled suturing compared to conventional laparoscopic tools, while augmented-reality (AR) guidance improves target localization accuracy by roughly 12–15% in complex resections. Regionally, North America dominates in procedural volume and installed base of advanced platforms, while Asia-Pacific leads in rapid adoption rates and new facility investments—approximately 54% of newly commissioned surgical centers in 2022–2024 are in APAC markets. In the short term (2–3 years), adoption of single-port and modular robotic adapters is expected to reduce OR turnover time by 10–20%, improve instrument utilization by 25%, and shorten learning curves for advanced MIS procedures.

Compliance and ESG considerations are influencing procurement: firms are committing to packaging reduction targets and energy-efficient manufacturing standards, with several manufacturers targeting a 20–30% reduction in packaging waste or non-recyclable materials by 2028. In a micro-scenario from 2023, a tertiary-care hospital network introduced a robotic single-port retrofit that achieved a 23% reduction in average blood loss and a 16% faster discharge rate for selected procedures, illustrating measurable clinical and operational gains from targeted device adoption.

Strategically, healthcare systems are integrating MIS device selection into broader care-pathway redesigns—aligning device choice with reimbursement bundling and post-acute care optimization. For medtech firms, success lies at the intersection of clinical evidence generation, modular platform economics, and service contracts that guarantee predictable OR efficiency improvements. Over the medium term, the Minimally Invasive Surgical Devices Market will be a central pillar of procedural resilience, operational cost-containment, and sustainable surgical practice evolution.

The Minimally Invasive Surgical Devices Market is shaped by technology-driven substitution, clinical protocol evolution, and economic pressure to shift elective procedures to ambulatory settings. Demand is rising for devices that reduce anesthesia time and shorten recovery windows, with visualization upgrades (HD/4K, fluorescence imaging) and advanced energy platforms enabling broader procedure portfolios in the same OR footprint. Manufacturers are pushing modular designs that allow a shared console or docking system to accept multiple single-use instrument types, reducing capital strain and broadening buyer affordability. Procurement cycles vary: high-acuity systems require multi-stakeholder evaluation spanning clinical trials, OR logistics, and capital planning—often 6–18 months—whereas plug-and-play disposables see procurement cycles measured in weeks. Reimbursement trends and payer approvals for ambulatory MIS procedures materially affect adoption velocity, and training infrastructure—simulation labs, proctoring programs—remains a gating factor for scale deployment. Overall, market dynamics favor vendors that can demonstrate measurable perioperative improvements, simplified sterilization workflows, and predictable total-cost-of-ownership.

The shift toward ambulatory surgery centers (ASCs) is a principal demand driver because minimally invasive devices enable shorter procedure times and faster recovery compatible with same-day discharge. ASCs saw a notable expansion in procedure portfolios between 2020–2024, with many facilities adding laparoscopic and endoscopic suites—facilitating higher volumes of elective MIS cases such as cholecystectomies, hernia repairs, and selected gynecological surgeries. Devices that reduce instrument setup time and support standardized disposable kits have delivered 15–30% reductions in per-case preparation time in pilots, translating to meaningful throughput increases. Payer incentives for reduced hospitalization and bundled payments for episodes of care incentivize hospitals to adopt technologies that minimize complications and readmissions. The cumulative effect is an accelerating acquisition of compact electro-surgical units, disposable end effectors, and single-use stapling systems designed specifically for outpatient ergonomics and sterilization efficiency.

High upfront capital and training requirements constrain adoption of advanced MIS platforms. Sophisticated robotic systems and integrated imaging suites demand significant capital allocation—often requiring multiyear depreciation schedules and service contracts that increase fixed costs. Training and credentialing timelines (proctoring, simulation hours) extend adoption lead times; many hospitals report multi-month to year-long competency programs before independent surgeon privileges are granted. Consumable costs for specialized disposable instruments also impact per-case economics, pressuring procurement committees to seek clear throughput and OR time recovery metrics. Supply-chain sensitivities (sterile consumable availability, single-source components) add further risk; facilities often maintain dual-sourcing or safety stock to avoid case cancellations. These factors collectively slow procurement for smaller hospitals and constrained health systems despite favorable clinical outcomes.

Modular robotics and sensor-enabled disposable instruments create substantial market opportunities by lowering barriers to entry and enabling scalable economics. Retrofit modules that convert standard laparoscopic towers into semi-robotic assistants allow hospitals to access advanced functionality without full-system purchases; early pilots report adoption preferences among mid-sized hospitals and ASCs. Smart disposables with embedded torque and position sensors provide real-time instrument metrics, enabling predictive maintenance and improved surgical coaching. These developments open recurring revenue models—subscription analytics, consumable replenishment, and outcome-based contracts tied to perioperative KPIs. Additional opportunities lie in domain-specific procedural kits (e.g., endometriosis, bariatric revisions) that bundle instruments, consumables, and digital guidance—streamlining procurement and accelerating scalability across hospital networks. Vendors who can provide integrated training, outcome guarantees, and predictable consumable economics will capture notable share of new installations.

Regulatory pathways and sterilization logistics pose persistent challenges. Device approvals require thorough biocompatibility, sterilization validations, and clinical evidence—lengthening time-to-market for additive instrument designs and sensorized disposables. Sterilization workflows vary across geographies, necessitating product configurations compatible with prevalent sterilization methods; single-use devices simplify compliance but raise environmental and waste-disposal concerns. Supply-chain disruptions for critical sterile components can interrupt case schedules; hospitals therefore demand clear logistical commitments and contingency planning from suppliers. Additionally, evolving regulatory expectations around cybersecurity for connected instruments and data handling for cloud analytics increase compliance overhead. These compounding challenges raise vendor engineering and certification costs and slow penetration into risk-averse health systems.

Modular and Prefabricated Instrument Kits driving OR efficiency: Use of prefabricated, procedure-specific instrument kits has led to reported 55% of new OR implementations observing cost or time benefits in set-up and sterilization workflows; pre-configured trays and single-use packs reduce instrument handling and speed turnover by up to 20–30% in many pilots.

Proliferation of Compact Robotic and Retrofit Modules: Compact and modular robotic adapters are increasing platform accessibility; hospital pilots noted 30% faster surgeon onboarding and a 25% reduction in capital intensity per advanced-case when retrofits are used compared to full-system purchases.

Rise of Smart, Sensor-Enabled Disposables: Embedded sensors in disposable instruments are improving procedural telemetry; trial programs show 40% improvements in intraoperative instrument tracking accuracy and enable predictive replenishment systems that reduce stockouts by 35%.

Integration of Augmented Reality (AR) and Imaging Fusion: AR overlays and imaging fusion technologies are enhancing intraoperative visualization, delivering 12–18% gains in resection margin accuracy and reducing revision rates in complex resections, while adoption is increasing across high-volume cancer centers and specialized tertiary hospitals.

The market is structured across three core segmentation dimensions—type, application, and end-user—each contributing uniquely to the competitive landscape. Product types continue to diversify as technologies advance toward greater precision, automation, and interoperability, supporting broader clinical and operational use cases. Applications are expanding rapidly as healthcare providers, research organizations, and outpatient centers integrate less invasive approaches that reduce hospital stays and enhance patient recovery times. End-user adoption patterns highlight a clear shift toward facilities prioritizing workflow efficiency, reduced postoperative complications, and improved patient outcomes. Together, these segments illustrate the depth of technological development and evolving demand within minimally invasive surgical ecosystems.

Product types within minimally invasive surgical devices demonstrate varied adoption patterns and technology maturity levels. Laparoscopic instruments currently lead the category, accounting for approximately 41% of total utilization, driven by their broad applicability in general, gynecological, and urological surgeries, as well as their established clinical trust. Compared with this, robotic-assisted surgical systems represent about 27%, benefiting from precision-enhancing capabilities but still limited by cost barriers. Energy-based devices hold around 18%, and visualization systems and ancillary tools collectively contribute 14% as supporting components across multiple procedures. Robotic systems remain the fastest-growing type, expanding at an estimated double-digit CAGR, supported by rising investments in automation, improved haptic technologies, and enhanced surgeon-assist platforms. While laparoscopic platforms dominate today, robotic systems are expected to show the steepest adoption curve over the coming years as system prices decline and procedure acceptance expands. Other device categories—including handheld instruments, insufflators, and navigation-enabled tools—contribute a combined 14% share, serving niche or highly specialized roles in thoracic, neurological, and bariatric workflows.

Applications for minimally invasive surgical devices span a wide array of clinical procedures, each with differing levels of adoption. General surgery remains the leading application area with approximately 38% share, driven by high procedure volume, surgeon familiarity, and broad use in gallbladder removal, appendectomies, and hernia repair. Gynecological procedures represent about 26%, supported by the strong shift toward minimally invasive hysterectomies and myomectomies. Orthopedic and cardiothoracic applications collectively account for roughly 24%, while other surgical fields—such as gastrointestinal, bariatric, and neurological interventions—contribute a combined 12%. Cardiothoracic surgery is emerging as the fastest-growing application, supported by rising adoption of micro-incision valve repair tools, improved catheter-based navigation, and growing preference for procedures that minimize postoperative ICU time. The segment is expanding at a high-growth CAGR, driven by ongoing development of transcatheter and image-guided solutions. Across the market, consumer and institutional adoption patterns reflect a clear trend toward minimally invasive approaches. In 2024, over 42% of hospitals reported integrating image-guided surgical platforms into routine workflows, while nearly 35% of global patients expressed a preference for minimally invasive options due to shorter recovery times and reduced scarring.

Hospitals remain the dominant end-user within the minimally invasive surgical device landscape, accounting for approximately 55% of overall utilization, supported by higher patient volumes, multifunctional surgical departments, and broader access to advanced systems. Compared with this, ambulatory surgical centers (ASCs) represent about 28%, driven by the rapid shift toward outpatient, same-day procedures. Specialty clinics and research institutes collectively contribute the remaining 17%, with niche adoption in precision-guided and diagnostic-linked interventions. ASCs represent the fastest-growing end-user segment, expanding at a notable CAGR, propelled by rising reimbursement support, increasing patient inclination toward shorter stay durations, and wider availability of portable and modular MIS devices suited for compact environments. Hospitals continue to maintain leadership, but ASCs are capturing growing procedural volume in orthopedics, gynecology, and gastrointestinal surgery. Industry adoption trends show tangible momentum across end-user groups. In 2024, more than 38% of global healthcare systems reported piloting AI-assisted surgical visualization tools, while over 60% of younger patient cohorts indicated higher trust in facilities adopting advanced, less-invasive surgical modalities.

North America accounted for the largest market share at 41.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

North America’s market profile in 2024 shows high procedural density with approximately 3,200 dedicated MIS suites and more than 1,000 hospitals actively expanding minimally invasive program capacities during 2021–2024. Europe follows with 28.5% of regional demand, reporting over 1,850 laparoscopic-capable centers and widespread adoption of fluorescence-guided imaging. Asia-Pacific contributed roughly 20.3% of global device volumes in 2024, with China, India, and Japan leading procurement: combined, these three countries accounted for an estimated >60% of APAC device installations that year. South America and Middle East & Africa represented the remaining 10.0%, with Brazil and UAE showing notable increases in ASC investments and OR modernization projects.

North America held 41.2% of the market in 2024, characterized by a dense installed base of robotic and laparoscopic systems, broad hospital networks, and advanced reimbursement frameworks that support MIS adoption. Key industries driving demand include general surgery, urology, and gynecology—each reporting substantial procedural volumes: over 1.2 million laparoscopic procedures annually across major hospital systems. Regulatory focus on device safety and streamlined 510(k)-style clearances for iterative device upgrades supports quicker product refresh cycles. Technological trends include adoption of fluorescence imaging, 3D visualization, and compact robotic arms tailored for ASCs. A notable local player, a major US-based robotic platform vendor, has introduced modular end-effectors and subscription-based service models to lower upfront procurement barriers. Regional consumer behavior shows higher enterprise adoption in healthcare and finance-like procurement discipline for device lifecycle management and service-level agreements.

Europe accounted for 28.5% of the market in 2024, with Germany, the United Kingdom, and France as principal markets recording strong capital investment in imaging-guided MIS suites. Regulatory bodies and conformity assessments emphasize clinical evidence and device traceability, prompting manufacturers to prioritize explainability and sterilization validation. Adoption of technologies such as multilingual AR surgical aids and on-table fluorescence imaging is rising, and several European medtech firms are introducing reusable instrument options to balance sustainability and cost. A regional player has launched a reusable instrument line with standardized sterilization trays and reduced packaging waste. European buyer behavior favors devices with robust lifecycle support, clear audit trails, and demonstrable sterilization compatibility.

Asia-Pacific represented 20.3% of the market in 2024 and is notable for rapid facility expansion, particularly in China, India, and Japan. Top consuming countries—China, India, and Japan—account for the bulk of device procurement within APAC, with China alone reporting several hundred new surgical suites equipped for MIS annually. Infrastructure investments, government funding for hospital modernization, and growth of private hospital chains underpin device uptake. Innovation hubs in the region are advancing local manufacturing capabilities and cost-competitive disposable production. An APAC-based medtech company has scaled production of single-port access kits to supply regional hospital networks. Consumer behavior trends emphasize mobile-enabled perioperative workflows, translation-enabled device UIs, and preference for devices that reduce length-of-stay.

South America held 5.6% of the market in 2024, with Brazil and Argentina the primary demand centers. Investments in hospital infrastructure, telecom-enabled tele-surgery pilot programs, and rising private healthcare expenditure are stimulating demand for laparoscopic towers, stapling systems, and disposable instrument kits. Local firms and distributors are partnering to improve logistic responsiveness and provide bundled maintenance packages. Consumer patterns show demand tied to media- and language-localized training content and an increased push for ambulatory procedures in urban centers.

Middle East & Africa accounted for 4.4% of global demand in 2024, with the UAE, Saudi Arabia, and South Africa leading investments. Regional demand is driven by oil & gas sector medical services, large-scale construction of specialty hospitals, and government-backed national health initiatives. Technological modernization includes cloud-enabled device management and investments in clinician upskilling programs. A regional distributor has introduced bundled financing for small hospital networks to acquire laparoscopic towers. Consumer behavior varies widely, with urban tertiary centers rapidly adopting advanced visualization and peripheral clinics prioritizing cost-effective disposable solutions.

United States - 34.1% Market Share: Extensive device manufacturing capacity, deep clinical trial ecosystems, and strong hospital capital expenditure programs.

China - 16.9% Market Share: Rapid expansion of hospital infrastructure, growing private healthcare investment, and strong local device production scaling.

The competitive landscape in the Minimally Invasive Surgical Devices Market comprises global system integrators, specialized instrument makers, and a broad ecosystem of component suppliers and disposables manufacturers. There are over 200 active competitors globally, spanning full-stack robotic platform providers, visualization specialists, energy-device makers, and companies focused on single-use procedural kits. Market positioning includes a small number of platform leaders with broad installed bases and long-term service contracts, plus a larger cohort of niche innovators targeting specialty procedures or cost-efficient disposables. In 2022–2024, the market recorded >40 strategic collaborations (technology partnerships, distributor agreements), 18 notable product launches of next-gen instruments and imaging upgrades, and multiple acquisitions focused on single-use portfolio expansion and software analytics. The nature of the market is moderately consolidated—top 5 companies represent a ~60% combined presence across installed systems and headline accounts—while the remaining market is fragmented across regional players and startup innovators. Competitive differentiation centers on clinical evidence, integrated service/support models (with multi-year service contracts common), licensing of proprietary optics/energy tech, and the ability to supply sterile disposable kits at scale. Buyers evaluate vendors on instrument durability, consumable logistics, training programs, and lifecycle cost predictability; leading platforms support multi-hospital deployments and centralized analytics.

Olympus

Johnson & Johnson (Ethicon)

Verb Surgical

Smith & Nephew

B. Braun

Technological evolution in the minimally invasive domain emphasizes precision, connectivity, and disposability economics. Robotic-assisted instrumentation continues to migrate from large, capital-intensive installations to compact, modular systems and retrofit adapters—enabling broader adoption in ASCs and mid-tier hospitals. Miniaturization advances have produced instruments with smaller shaft diameters, improved articulation, and enhanced haptic feedback, supporting delicate procedures such as transoral and single-port interventions. Visualization technologies—4K/3D imaging, fluorescence-guided systems, and AR overlays—enhance intraoperative clarity and margin assessment, with AR fusion demonstrating measurable improvements in target localization in complex oncologic resections.

On-device sensing and connected disposables enable procedural telemetry: sensor-equipped staplers and smart trocars provide force and position data, supporting predictive maintenance and real-time surgical coaching. Cloud-based analytics platforms aggregate procedural data across installed bases to surface performance benchmarks and support outcome-based contracting. Sterilization and materials engineering innovations focus on reusable-disposable hybrids that balance lifecycle costs and environmental concerns: manufacturers are experimenting with recyclable polymers and modular sterile trays to reduce waste footprints.

Interoperability and API-driven integrations with hospital information systems and perioperative management suites are increasingly required: device vendors now offer SDKs or connectors to integrate device logs, procedure videos, and instrument telemetry into centralized OR management dashboards. Cybersecurity and medical device regulation trends demand embedded security features and validated software lifecycle controls. For decision-makers, technology selection should weigh modularity, upgrade paths, data access models, environmental impact of disposables, and vendor readiness for large-network deployment and analytics-driven service models.

14 Mar 2024 — Intuitive Surgical: Intuitive announced FDA clearance and rollout plans for its fifth-generation da Vinci 5 robotic platform, highlighting system upgrades, new clinical workflow features, and plans for phased commercial deployment to expand clinician access to next-generation robotic capabilities. Source: www.intuitive.com

02 Jul 2024 — Johnson & Johnson / Ethicon: Ethicon launched the ECHELON™ 3000 powered stapler, a digitally-enabled device with one-handed powered articulation and enhanced ergonomics intended to support a range of minimally invasive procedures and improve surgeon control in confined anatomies. Source: www.jnjmedtech.com

12 Jun 2024 — Olympus: Olympus announced a strategic expansion in India with a new R&D and innovation presence in Hyderabad, aimed at strengthening regional product development and local sterile kit production support for Asia-Pacific markets—part of broader capacity and localization initiatives. Source: www.olympus-global.com

12 Feb 2024 — Smith+Nephew: Smith+Nephew showcased and expanded its AI-driven robotic-assisted solutions for personalized orthopaedic surgery at AAOS 2024, emphasizing device-level AI features for surgical planning, intraoperative guidance, and outcome personalization. Source: www.smith-nephew.com

This report examines the Minimally Invasive Surgical Devices Market across a comprehensive range of product types, applications, end users, and geographies. Product coverage includes laparoscopic instruments, endoscopic systems, energy devices (electrosurgical and ultrasonic), robotic-assisted platforms (both full systems and modular retrofits), visualization suites (HD/3D/fluorescence), single-port and natural orifice devices, and disposable procedural kits and stapling systems. Application-level analysis spans general surgery, urology, gynecology, thoracic, bariatric, ENT, and neurosurgical endoscopic procedures, with attention to perioperative workflows, sterilization logistics, and outpatient suitability.

Geographic scope includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level insights for leading markets and an emphasis on facility counts, OR modernization rates, and procurement cycle characteristics. The report addresses buyer personas—tertiary hospitals, ASCs, specialty surgical centers, and teaching institutions—and examines procurement drivers such as OR throughput targets, training capacity, and payer reimbursement trends.

Operational and technology focus areas include device interoperability, cloud analytics, sterilization and materials engineering, sensor-enabled disposables, AR/ imaging fusion, and modular robotics. The report evaluates vendor go-to-market strategies, competitive positioning, partnership ecosystems, and service models (including training, maintenance, and consumable supply chains). Emerging and niche segments—such as single-port oncology toolkits, transoral robotic surgery accessories, and energy-device hybrids—are profiled for growth potential and deployment readiness. The aim is to provide actionable intelligence for procurement, product strategy, and corporate development teams to align investments in minimally invasive devices with clinical, operational, and sustainability goals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,907.0 Million |

| Market Revenue (2032) | USD 3,556.0 Million |

| CAGR (2025–2032) | 8.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Intuitive Surgical, Medtronic, Stryker, Olympus, Johnson & Johnson (Ethicon), Verb Surgical, Smith & Nephew, B. Braun |

| Customization & Pricing | Available on Request (10% Customization Free) |