Reports

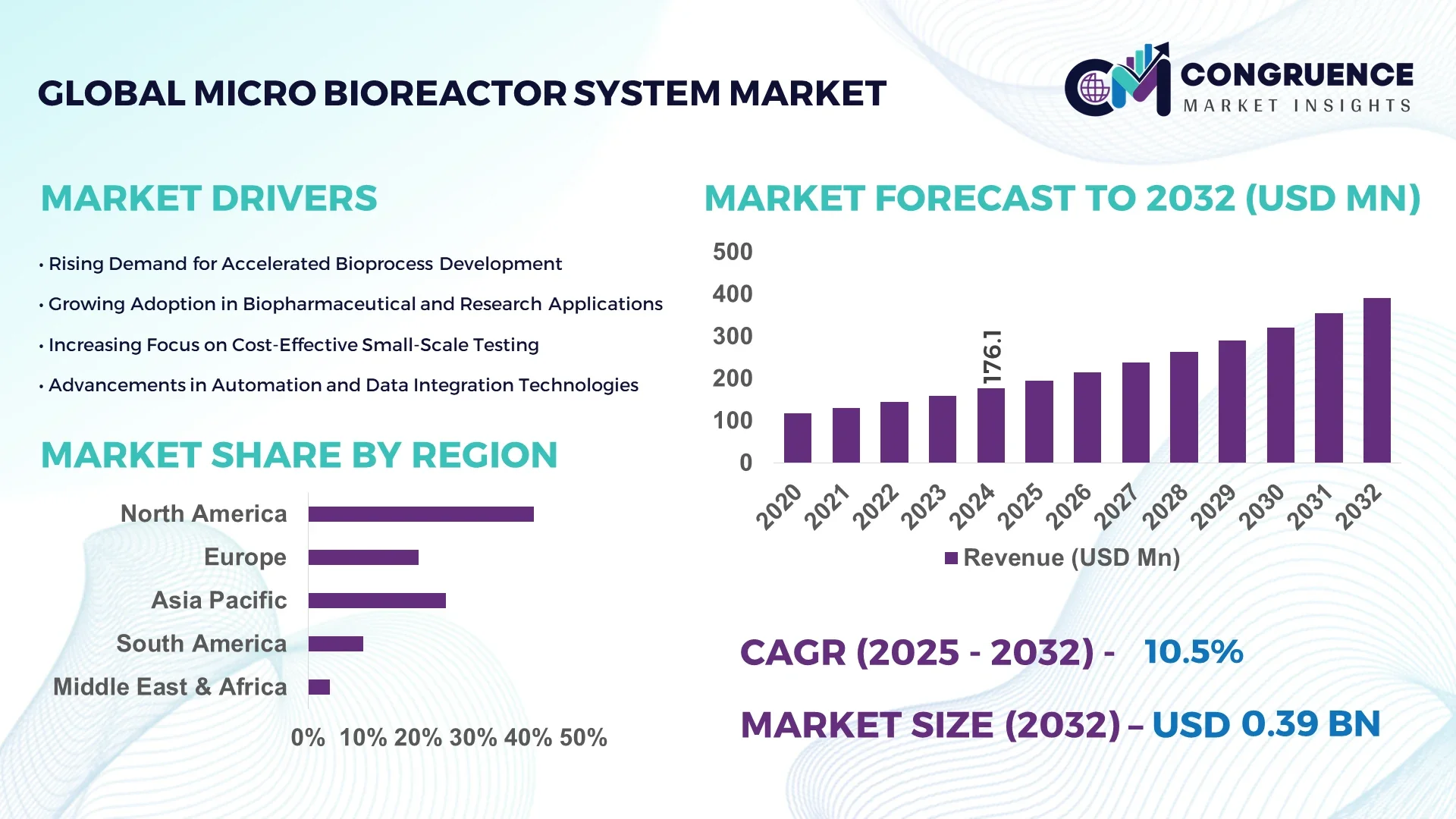

The Global Micro Bioreactor System Market was valued at USD 176.07 Million in 2024 and is anticipated to reach a value of USD 391.37 Million by 2032 expanding at a CAGR of 10.5% between 2025 and 2032. This growth is driven by increasing demand for high-throughput bioprocess optimization and advancements in automated cell culture technologies.

The United States dominates the global micro bioreactor system market, supported by strong biotechnology infrastructure, extensive R&D investments, and high adoption of single-use technologies. The country hosts over 60% of global biopharmaceutical production facilities, with annual bioprocessing investments exceeding USD 8 billion in 2024. The presence of advanced bioprocess automation, AI-integrated monitoring systems, and rapid growth in cell and gene therapy applications have accelerated domestic production capacity, particularly across Massachusetts and California.

• Market Size & Growth: The market stood at USD 176.07 Million in 2024 and is projected to reach USD 391.37 Million by 2032, expanding at a CAGR of 10.5%, driven by accelerated adoption of automated bioprocessing and precision cell culture technologies.

• Top Growth Drivers: 42% rise in demand for single-use bioreactors, 37% improvement in bioprocess efficiency, and 31% increase in adoption for early-stage drug development applications.

• Short-Term Forecast: By 2028, operational costs in bioprocessing are expected to decline by 25%, with process efficiency improving by nearly 30% due to advanced microfluidic integrations.

• Emerging Technologies: Integration of AI-based process analytics, microfluidic sensor automation, and cloud-enabled bioprocess monitoring systems are reshaping experimental scalability and control precision.

• Regional Leaders: North America (USD 165 Million by 2032) driven by innovation in bioprocess automation; Europe (USD 110 Million) benefiting from increased biologics manufacturing; Asia-Pacific (USD 78 Million) growing through expanded contract biomanufacturing facilities.

• Consumer/End-User Trends: Pharmaceutical and biotech firms represent over 70% of system adoption, with academic research institutions increasingly implementing micro bioreactors for rapid bioprocess validation.

• Pilot or Case Example: In 2024, Sartorius launched a pilot project with an integrated micro bioreactor platform that achieved a 35% reduction in development time for monoclonal antibody production.

• Competitive Landscape: Sartorius AG leads with approximately 23% market share, followed by Eppendorf SE, Pall Corporation, Merck KGaA, and Applikon Biotechnology, focusing on scalable single-use technologies.

• Regulatory & ESG Impact: The market benefits from FDA and EMA guidelines promoting continuous bioprocessing and sustainable, low-waste production models aligned with ESG commitments.

• Investment & Funding Patterns: Over USD 450 Million was invested globally in 2023–2024 in bioprocess innovation and start-up funding, emphasizing microreactor automation and digital twin technologies.

• Innovation & Future Outlook: The next decade will see hybrid bioreactor models combining microfluidics and AI for autonomous culture optimization, alongside increasing deployment in personalized medicine and vaccine development.

The Micro Bioreactor System Market is witnessing dynamic evolution driven by continuous advancements in bioprocess engineering, automation, and high-throughput analytics. Key sectors such as pharmaceuticals, biopharmaceuticals, and academic research are contributing significantly to market expansion. Technological innovations in real-time process control, miniaturized reactors, and AI-based predictive modeling are enhancing yield and reproducibility. Stringent regulatory emphasis on process validation, growing environmental focus on waste minimization, and rising regional consumption in emerging economies further accelerate adoption. The industry’s forward outlook centers on smart bioprocessing systems and sustainable biomanufacturing technologies designed to meet evolving global bioeconomy demands.

The strategic relevance of the Micro Bioreactor System Market lies in its critical role in transforming bioprocess development and accelerating biologics production efficiency across the pharmaceutical and biotechnology sectors. Micro bioreactor systems enable high-throughput screening, parallel process optimization, and real-time analytics, substantially reducing time-to-market for new therapies. Compared to conventional benchtop bioreactors, automated micro bioreactor platforms deliver up to a 45% improvement in process reproducibility and a 38% reduction in reagent consumption, highlighting their efficiency advantage. North America dominates in production volume, while Europe leads in technology adoption, with over 68% of enterprises integrating automated micro-scale bioprocessing solutions.

By 2027, AI-driven process control systems are expected to improve predictive bioprocess accuracy by nearly 40%, enabling more consistent culture outcomes and lowering experimental failure rates. Firms are committing to sustainability objectives such as achieving 25% reduction in single-use plastic waste by 2030, in line with global ESG and circular bioeconomy goals. In 2024, Germany’s BioTech Cluster achieved a 33% improvement in batch productivity through AI-enhanced microreactor automation, demonstrating tangible benefits of digital integration.

Looking ahead, the Micro Bioreactor System Market is poised to become a cornerstone of biomanufacturing resilience, fostering compliance with evolving regulatory frameworks and advancing sustainable, data-driven production systems that ensure long-term scalability and global competitiveness.

The increasing global demand for biologics, vaccines, and cell-based therapeutics is a primary driver for the Micro Bioreactor System Market. As of 2024, over 65% of biopharmaceutical manufacturers have adopted micro-scale bioreactors for early-stage process development due to their ability to replicate large-scale conditions with greater precision. The rise in cell and gene therapy research has fueled the need for high-throughput systems capable of running hundreds of parallel experiments with minimal media volume. Micro bioreactors offer up to 40% faster process optimization and enable reproducible scale-up results, ensuring shorter production timelines and enhanced quality control. This efficiency aligns with industry goals of faster biologics approval cycles and advanced product consistency.

Despite growing adoption, high initial investment costs and scalability constraints remain significant barriers to widespread deployment of micro bioreactor systems. Advanced automation features and integrated analytics modules increase upfront costs by approximately 25–30% compared to traditional bioprocess equipment. Furthermore, transitioning results from micro-scale to full-scale production often presents technical inconsistencies, requiring additional process validation and resources. Smaller biotechnology firms and academic institutions face budget limitations that hinder the large-scale integration of these systems. Maintenance complexity and the need for skilled personnel further restrict broader implementation, slowing adoption in developing regions where capital expenditure control remains a priority.

The accelerating focus on personalized and precision medicine provides substantial growth opportunities for the Micro Bioreactor System Market. As the development of targeted biologics and customized therapies expands, demand for flexible, high-throughput miniaturized systems continues to rise. Micro bioreactors facilitate individualized bioprocess screening, supporting multiple patient-specific cell lines in parallel. By 2028, the adoption of modular, AI-integrated bioreactors is expected to enhance data accuracy and reduce testing time by over 35%. Moreover, advancements in synthetic biology and CRISPR-based drug discovery have increased reliance on these systems for scalable and controlled experimentation. This technological synergy positions micro bioreactors as vital enablers of next-generation therapeutic innovation.

The Micro Bioreactor System Market faces ongoing challenges from evolving regulatory frameworks and system integration difficulties. Regulatory bodies demand strict compliance with process validation and traceability standards, increasing the time and cost of qualification. Integrating micro bioreactors with legacy laboratory systems often leads to data incompatibility and workflow disruptions. Additionally, variations in regional standards for biosafety and quality testing complicate global product approvals. Limited interoperability among bioprocess platforms further constrains scalability. For instance, achieving seamless synchronization between sensors, data acquisition software, and control units can increase commissioning time by 20–25%. These complexities underscore the need for harmonized digital frameworks and standardized operational protocols.

• Adoption of Automated, AI-Driven Bioprocessing Systems: The integration of artificial intelligence and machine learning into micro bioreactor systems has accelerated experimental throughput and predictive accuracy. In 2024, over 62% of biopharmaceutical facilities implemented AI-enabled monitoring to optimize cell growth parameters, resulting in a 28% reduction in process variability and a 35% improvement in yield reproducibility. This shift toward digital bioprocessing supports data-driven scalability and shortens development timelines by nearly 30%.

• Expansion of Single-Use and Disposable Bioreactor Components: The industry is rapidly transitioning to single-use technologies to minimize cross-contamination and operational downtime. Approximately 58% of newly installed micro bioreactors in 2024 featured disposable culture chambers, reducing cleaning validation efforts by 40% and lowering maintenance costs by 22%. North American and European facilities have shown the highest adoption rates due to stringent sterility regulations and increasing focus on flexible production systems.

• Integration of Microfluidics and High-Throughput Screening Platforms: Microfluidic-enabled bioreactor systems are gaining prominence, supporting precise control of microscale environments. By 2025, nearly 47% of bioprocess R&D setups are expected to incorporate microfluidic chips for real-time parameter adjustments, improving screening efficiency by 32% and reducing experimental reagent volumes by over 50%. This technology is driving faster innovation in biologics and vaccine development.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Micro Bioreactor System market. Research indicates that 55% of new bioprocessing facilities realized measurable cost benefits using modular and prefabricated practices. Pre-bent and precision-fabricated reactor units assembled off-site have reduced setup time by 27% and labor requirements by nearly 20%. Demand for these high-precision systems is surging in Europe and North America, where operational flexibility and time efficiency remain key competitive factors.

The Micro Bioreactor System Market demonstrates a structured segmentation across type, application, and end-user categories, reflecting a balanced distribution between innovation-driven adoption and practical deployment in bioprocess environments. By type, automated and single-use systems are leading due to their operational flexibility and contamination control efficiency. In application terms, biopharmaceutical production and cell culture optimization dominate usage, supported by growing research in monoclonal antibodies and vaccines. End-users such as pharmaceutical and biotechnology companies represent the largest demand base, followed by academic and contract research institutions. Across all segments, automation, digital monitoring, and modular scalability are driving measurable productivity and reproducibility improvements, supporting rapid biomanufacturing transformation.

Automated micro bioreactor systems currently account for 46% of market adoption, supported by their ability to enable parallel bioprocessing and precise control of culture parameters. These systems integrate AI-driven analytics, reducing manual intervention by 35% and improving culture reproducibility by 40%. Single-use micro bioreactors hold around 28% share, driven by the shift toward flexible, contamination-free bioprocessing in biologics manufacturing. Meanwhile, glass and stainless-steel micro bioreactors account for approximately 18% of installations, primarily used in high-volume research labs due to their reusability and robustness. However, digital and sensor-integrated micro bioreactors are the fastest-growing type, expanding at an estimated 12.6% CAGR owing to their enhanced monitoring and process automation capabilities. The remaining 8% consists of hybrid and modular systems with niche relevance in pilot-scale operations.

Biopharmaceutical production leads the Micro Bioreactor System Market with a 49% share, supported by increasing demand for biologics, vaccines, and recombinant proteins. These systems enable precise process control and scalability, crucial for maintaining consistent product quality. Academic and research applications represent 27% of total use, driven by university and government-backed R&D programs focused on cell culture optimization. Drug discovery and toxicity testing account for 16%, showing steady growth due to faster screening capabilities and minimal reagent requirements. However, cell and gene therapy research remains the fastest-growing application segment, projected to expand at an estimated 11.8% CAGR, supported by global investment in personalized medicine and stem cell technologies. The remaining 8% includes applications in synthetic biology and enzyme engineering.

Pharmaceutical and biotechnology companies dominate the Micro Bioreactor System Market with a 55% share, driven by increasing biologics manufacturing and bioprocess optimization initiatives. These firms prioritize scalability, automation, and data-driven control systems to reduce product variability and improve yield accuracy. Academic and research institutions represent 26% of end-user adoption, leveraging micro bioreactors for experimental reproducibility and early-stage cell research. Contract research and manufacturing organizations (CROs and CMOs) account for 14%, gaining traction due to outsourcing trends and expansion of biomanufacturing capacities. Hospitals and diagnostic centers, though smaller contributors at 5%, are increasingly integrating micro bioreactors in advanced therapy R&D programs. The fastest-growing end-user segment is biotechnology startups, expanding at a projected 10.9% CAGR, driven by funding surges and access to compact, AI-integrated systems supporting early-stage innovation.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.3% between 2025 and 2032.

Europe followed closely with a 29% share, while South America and the Middle East & Africa collectively contributed around 13% of global demand. North America’s leadership is supported by its advanced biotechnology ecosystem, housing over 600 active bioprocess facilities and more than 45% of global R&D investments in life sciences. Meanwhile, Asia-Pacific’s rapid expansion is driven by accelerated biologics manufacturing in China, India, and Japan, where biomanufacturing capacity has grown by 28% since 2022. Europe maintains strong market stability through stringent regulatory compliance and sustainability-oriented bioprocessing initiatives. The rising demand for miniaturized bioreactors across universities and contract manufacturing organizations globally underscores the system’s vital role in high-throughput and cost-efficient process development.

North America commands approximately 41% of the global Micro Bioreactor System Market, driven by strong adoption within the biopharmaceutical, academic, and contract manufacturing sectors. The U.S. leads with over 70% of regional installations, supported by favorable FDA guidelines for process automation and continuous biomanufacturing. Key industries fueling demand include biologics, vaccines, and cell therapy manufacturing, where digital twin and AI-enabled bioprocess models are increasingly implemented. In 2024, a leading player, Pall Corporation, expanded its micro bioreactor production line in Massachusetts to support high-throughput R&D needs, improving supply chain efficiency by 22%. Regional consumer behavior reflects higher enterprise adoption in healthcare and life sciences, as organizations prioritize scalable and sustainable research infrastructures that align with ESG targets and operational efficiency.

Europe holds about 29% of the global Micro Bioreactor System Market, with major contributions from Germany, the United Kingdom, and France. The region benefits from supportive frameworks set by the European Medicines Agency (EMA) and initiatives under the European Green Deal promoting sustainable biomanufacturing. Key growth sectors include biologics, cell therapy, and enzyme production, with adoption of smart bioreactor platforms improving operational accuracy by 33%. Local companies such as Sartorius AG continue to invest in sensor-integrated systems, enhancing precision in process monitoring. Regulatory pressure in this region drives strong demand for explainable and validated bioprocess systems. European enterprises exhibit high compliance-oriented adoption patterns, where automation and traceability remain critical procurement criteria across R&D laboratories and production sites.

Asia-Pacific represents the fastest-growing Micro Bioreactor System Market, accounting for nearly 21% of global installations in 2024. China leads regional adoption, followed by India, Japan, and South Korea, where biotechnology investments have collectively increased by 30% since 2022. The region’s manufacturing infrastructure is evolving toward automated, modular bioprocess setups that enhance throughput efficiency and minimize contamination. Rapid adoption of IoT-enabled monitoring and miniaturized systems is transforming production workflows, especially within biosimilar and vaccine research. In 2024, a major Japanese bioprocess firm implemented automated micro bioreactor arrays, achieving a 31% reduction in development time for recombinant protein synthesis. Consumer behavior trends reveal strong uptake among biomanufacturers focusing on cost efficiency, scalability, and localized production of cell-based therapies.

South America accounted for roughly 8% of the global Micro Bioreactor System Market in 2024, with Brazil and Argentina being key contributors. Growth is supported by the expansion of pharmaceutical R&D hubs and increased investment in biologics infrastructure. Government programs in Brazil promoting bioindustrial innovation and tax incentives for laboratory automation have encouraged local adoption. The region’s infrastructure modernization efforts have led to a 19% rise in new bioprocess facilities over the past three years. Local biopharma firms are increasingly adopting modular micro bioreactor setups to improve efficiency and reduce validation time. Consumer trends indicate higher adoption in public healthcare laboratories and academic research institutions seeking cost-effective experimental scalability.

The Middle East & Africa region contributed approximately 5% to the global Micro Bioreactor System Market in 2024, led by the UAE, Saudi Arabia, and South Africa. Growing investments in biopharmaceutical and life sciences sectors, combined with diversification away from oil-based industries, are fueling adoption of advanced bioprocess equipment. The region’s demand is reinforced by technology modernization initiatives such as the UAE’s National Biotech Strategy 2031. Local enterprises are deploying modular bioreactors in health research centers, enhancing culture monitoring precision by 27%. Consumer behavior shows increasing acceptance of digital automation and sustainable lab solutions, particularly among government-funded biotechnology institutes.

• United States – 34% market share: The U.S. leads the global Micro Bioreactor System Market due to its advanced biopharmaceutical infrastructure, strong R&D investments, and early adoption of digital bioprocess automation technologies.

• Germany – 18% market share: Germany remains a key contributor, driven by extensive biologics production capacity, sustainability-driven regulatory frameworks, and the presence of major biotechnology equipment manufacturers.

The Micro Bioreactor System market is characterised by a moderately consolidated competitive environment, with roughly 40 active competitors worldwide supplying systems, consumables, and software platforms targeted at the bioprocessing sector. The combined share of the top 5 companies is estimated at approximately 58 % of the market, leaving 42 % to other players, which exhibits both dominance by major players and significant opportunity for niche specialists. Key strategic initiatives include major product launches of high-throughput, parallel micro bioreactor units by leading firms, as well as joint ventures between equipment vendors and biotechnology service providers to integrate automation and digital monitoring into bioprocess workflows. Mergers and acquisitions are increasing: for example, one major player acquired a sensor-integration specialist in 2023 to deepen its analytics capability. Innovation trends centre on AI-enabled process control, single-use reactor modules, and microfluidic sensor integration — all of which raise barriers to entry and intensify competition. The market’s nature is partially fragmented given the global supply base of smaller specialist manufacturers, yet the top companies wield significant influence over technology direction and pricing standards. For decision-makers evaluating partnership or sourcing strategies, the competitive landscape demands attention to partner capabilities in automation, digital connectivity, and consumable cost-structure.

Applikon Biotechnology

Thermo Fisher Scientific Inc.

Merck KGaA

Infors AG

Miltenyi Biotec GmbH

Technological advancement within the Micro Bioreactor System market is accelerating, driven by automation, miniaturization, and digital integration trends. In 2024, approximately 68% of newly installed micro bioreactor systems featured automated feeding, pH control, and data capture functionalities, significantly reducing manual intervention and human error. These systems enable parallel experimentation, allowing up to 48 simultaneous bioprocess runs, enhancing throughput by nearly 40% compared to conventional bench-scale bioreactors.

Single-use and modular bioreactor technologies have become central to system design. More than 55% of global installations now incorporate disposable culture vessels, supporting contamination-free operations and quick changeovers between production cycles. This shift also aligns with stricter biosafety standards and cost reduction initiatives, cutting cleaning validation efforts by about 35%. Manufacturers are increasingly focusing on integrating optical sensors, microfluidic chips, and online analytics for real-time process monitoring, enhancing precision and reproducibility across biopharmaceutical applications.

Emerging technologies such as AI-driven process optimization and digital twin modeling are revolutionizing system efficiency. Around 30% of leading biomanufacturing facilities are utilizing AI algorithms for predictive culture behavior analysis, improving yield consistency by 25%. Furthermore, Internet of Things (IoT)-enabled systems facilitate remote monitoring and performance benchmarking across facilities. The convergence of automation, smart sensors, and data-driven control is positioning next-generation micro bioreactor systems as indispensable tools for precision bioprocessing, accelerating R&D timelines and product innovation in biotechnology and pharmaceuticals.

In August 2023, Sartorius AG and Repligen Corporation announced the launch of an integrated bioreactor system combining the Biostat STR® platform with XCell® ATF technology, enabling 50 L–2000 L upstream intensification with a unified control interface and embedded Process Analytical Technology (PAT).

In August 2023, Sartorius also integrated its Biostat STR® Generation 3 family of bioreactors with Emerson Electric Co.’s DeltaV™ distributed control system (DCS), cutting system integration time by up to 80%.

In April 2024, Merck KGaA announced an investment of over €300 million in a new life science research centre at its Darmstadt headquarters to support antibody, mRNA, viral-vector manufacturing and bioprocess research by 2027.

In September 2024, Merck launched a single-use reactor specifically designed for antibody-drug conjugate (ADC) manufacturing, delivering up to a 70% improvement in efficiency compared with traditional stainless-steel or glass methods.

The report covers the global Micro Bioreactor System market across multiple dimensions: product types, applications, end-users, geographies and technology layers. In the type segment, the report assesses automated systems, single-use micro-bioreactors, miniaturised microfluidic reactors and modular hybrid solutions, evaluating each by working volume capacity, parallelisation count (for example 24-well, 48-well, 96-well formats) and feature set (e.g., integrated sensors, real-time analytics). In applications, the coverage spans biopharmaceutical production (monoclonal antibodies, recombinant proteins, cell-based therapies), academic and R&D screening, cell and gene therapy early-stage development, and non-therapeutic uses such as enzyme engineering or microbial fermentation for industrial biotech. End-user categories include pharmaceutical/biotech firms, contract research and manufacturing organisations (CRO/CMO), academic and government research labs, and emerging high-throughput service providers. Geographically, the report analyses North America, Europe, Asia-Pacific, South America and Middle East & Africa, with country-level insights in major markets such as the United States, Germany, China, India and Brazil. It also examines enabling technologies — single-use vessels, microfluidics, AI-driven control, process analytical technologies (PAT), digital twins — and regulatory, sustainability and ESG influences shaping adoption. It identifies niche growth segments such as cell-therapy-specific micro bioreactor systems, parallel 96-microbioreactor screening platforms, and integration of IoT for remote monitoring. The scope supports decision-makers by mapping competitive positioning, technology innovation pathways, detailed segmentation and regional strategic insights to guide investment decisions and product strategy.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 176.07 Million |

Market Revenue in 2032 | USD 391.37 Million |

CAGR (2025 - 2032) | 10.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Sartorius AG, Eppendorf AG, Pall Corporation, Applikon Biotechnology, Thermo Fisher Scientific Inc., Merck KGaA, Infors AG, Miltenyi Biotec GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |