Reports

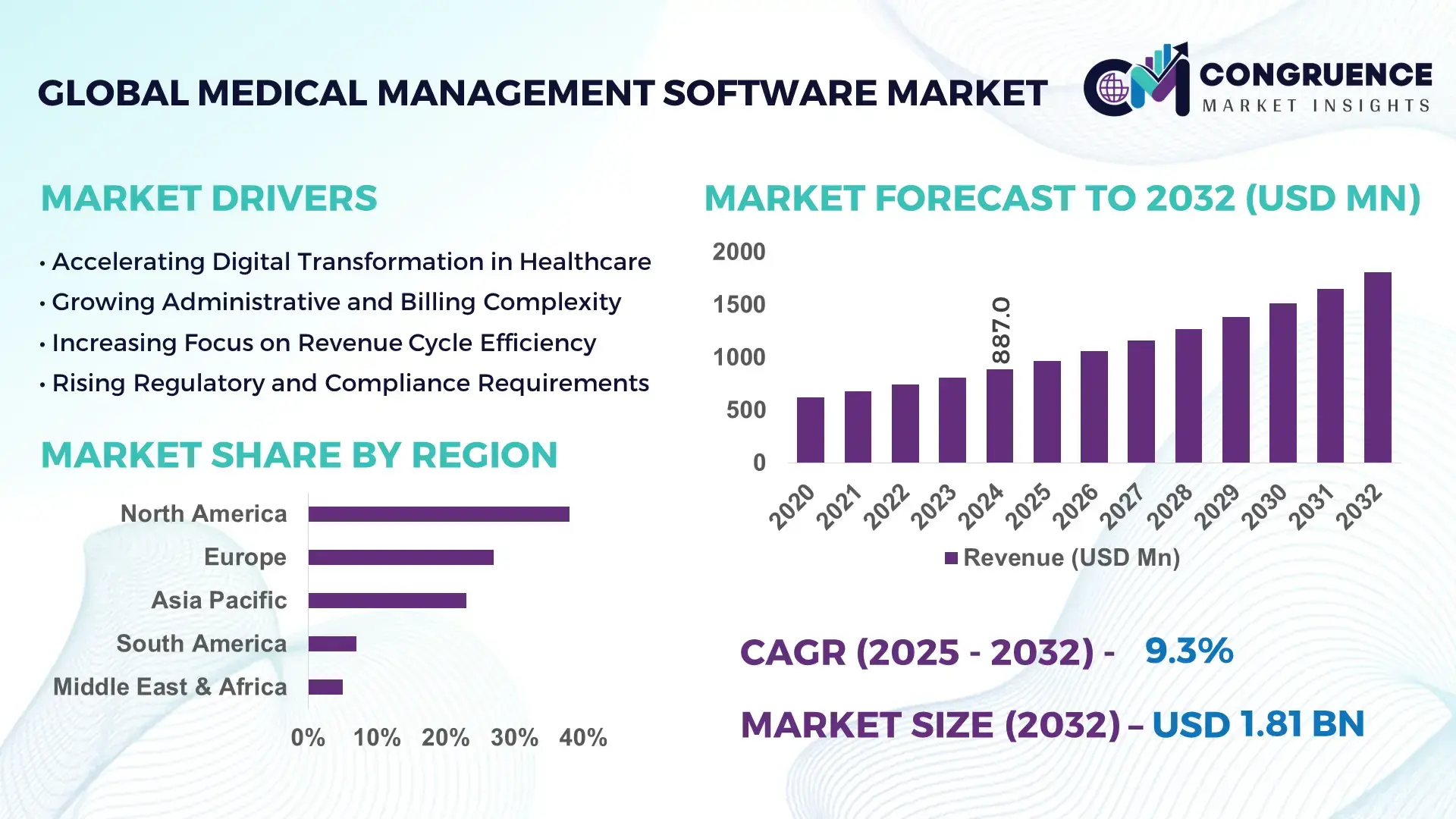

The Global Medical Management Software Market was valued at USD 887.0 Million in 2024 and is anticipated to reach a value of USD 1,806.7 Million by 2032 expanding at a CAGR of 9.3% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by accelerated digitization of healthcare administration workflows and rising demand for interoperable, compliance-ready software platforms across clinical and non-clinical settings.

The United States dominates the Medical Management Software Market in terms of enterprise deployment and technology maturity. The country hosts over 6,100 hospitals and 230,000 physician practices, creating sustained demand for scheduling, billing, claims, and workflow optimization software. Annual healthcare IT spending in the U.S. exceeded USD 75 billion, with software-led solutions accounting for a growing share of hospital capital expenditure. More than 85% of large hospitals use integrated medical management platforms connected with EHR and revenue cycle systems. The U.S. also leads in cloud-based deployment, with over 70% of providers adopting SaaS-based administrative software, supported by advanced AI-driven automation, cybersecurity investments exceeding USD 10 billion annually, and continuous product innovation by domestic vendors focused on scalability and compliance.

Market Size & Growth: Valued at USD 887.0 Million in 2024, projected to reach USD 1,806.7 Million by 2032 at 9.3% CAGR, driven by administrative automation and digital healthcare expansion.

Top Growth Drivers: Cloud adoption at 62%, billing automation improving efficiency by 38%, and AI-assisted scheduling adoption at 41%.

Short-Term Forecast: By 2028, operational cost optimization through software integration is expected to improve administrative efficiency by 32%.

Emerging Technologies: AI-based claims processing, cloud-native SaaS platforms, and API-driven interoperability frameworks.

Regional Leaders: North America projected at USD 720.0 Million by 2032 with advanced integration; Europe at USD 520.0 Million driven by compliance digitization; Asia Pacific at USD 410.0 Million supported by hospital IT expansion.

Consumer/End-User Trends: Hospitals and multi-specialty clinics account for over 60% of deployments, with rising adoption among ambulatory care centers.

Pilot or Case Example: In 2023, a U.S. hospital network pilot reduced claim rejection rates by 27% using AI-enabled management software.

Competitive Landscape: Market leader holds approximately 18% share, followed by Cerner, Epic Systems, Allscripts, McKesson, and Athenahealth.

Regulatory & ESG Impact: Compliance with HIPAA, GDPR, and digital health mandates is accelerating software upgrades and secure data handling adoption.

Investment & Funding Patterns: Over USD 6.5 Billion invested globally in healthcare management software platforms and startups over the past three years.

Innovation & Future Outlook: Integration of predictive analytics, automation, and unified dashboards is reshaping enterprise healthcare management systems.

The Medical Management Software Market serves hospitals, clinics, diagnostic centers, and ambulatory facilities, with hospitals contributing the largest share of deployments. Innovations such as AI-enabled billing, cloud-based workflow orchestration, and interoperability tools are reshaping operations. Regulatory digitization mandates, rising healthcare costs, and regional adoption growth in Asia Pacific are influencing demand, while automation and analytics-driven platforms define the future outlook.

The Medical Management Software Market has become strategically essential as healthcare systems prioritize efficiency, compliance, and data-driven decision-making. Organizations are increasingly aligning administrative software investments with broader digital transformation strategies to control rising operational complexity. AI-driven workflow automation delivers up to 45% faster processing compared to manual administrative systems, while cloud-native platforms enable scalable deployment across multi-location healthcare networks.

From a technology benchmark perspective, AI-enabled claims automation delivers 35% improvement in processing accuracy compared to rule-based billing systems. Regionally, North America dominates in deployment volume, while Europe leads in adoption intensity with over 68% of healthcare enterprises using integrated management software for compliance and reporting. Asia Pacific is emerging as a high-growth region, supported by national digital health programs and hospital infrastructure expansion.

In the short term, by 2027, robotic process automation and AI scheduling tools are expected to reduce administrative turnaround times by 30%, directly impacting patient throughput and cost control. ESG and compliance considerations are also shaping strategy, with firms committing to 40% paperless operations by 2028, reducing waste and improving data traceability.

In 2024, a leading U.S. healthcare network achieved a 29% reduction in administrative overhead through AI-enabled resource management and predictive scheduling initiatives. Looking ahead, the Medical Management Software Market is positioned as a pillar of healthcare resilience, enabling regulatory compliance, operational sustainability, and long-term system-wide efficiency gains.

The Medical Management Software Market is shaped by increasing administrative complexity, regulatory digitization, and the need for real-time operational visibility across healthcare organizations. Healthcare providers are transitioning from fragmented legacy systems to unified software platforms that integrate scheduling, billing, documentation, and analytics. Growing patient volumes, staffing shortages, and reimbursement pressure are accelerating demand for automation. Cloud deployment models are becoming standard, while interoperability with EHR and financial systems is now a core requirement. Data security, system scalability, and compliance readiness remain central to vendor differentiation, influencing procurement decisions across hospitals and outpatient facilities.

Healthcare providers are managing growing patient loads, multi-location operations, and complex reimbursement structures. Administrative staff workloads have increased by over 40% in large hospitals over the past decade. Medical management software enables automation of scheduling, billing, and reporting, reducing manual intervention by up to 35%. Integrated platforms also improve documentation accuracy and workflow coordination, supporting compliance and operational consistency. As healthcare systems expand service offerings, the need for centralized administrative control continues to drive software adoption.

Many healthcare organizations operate on legacy IT infrastructure, limiting seamless integration with modern management software. Nearly 46% of mid-sized hospitals report difficulties integrating new platforms with existing EHR and billing systems. Data migration risks, customization costs, and downtime concerns slow adoption. Additionally, inconsistent data standards across regions increase implementation complexity, restraining full-scale deployment despite strong demand for automation.

Cloud-based medical management software offers scalability, lower upfront infrastructure requirements, and remote accessibility. Over 65% of new deployments are now cloud-native, enabling faster implementation and multi-site coordination. Small and mid-sized clinics increasingly adopt subscription-based platforms, expanding addressable demand. Integration with analytics and AI modules further enhances value, creating opportunities for vendors offering modular, upgradeable solutions tailored to diverse healthcare settings.

Healthcare data breaches have increased by over 30% globally, raising concerns over patient data protection. Medical management software must comply with stringent regulations such as HIPAA and GDPR, increasing development and compliance costs. Providers face challenges in balancing accessibility with security, while vendors must invest heavily in encryption, monitoring, and audit capabilities. These pressures can slow procurement cycles and increase total cost of ownership.

Accelerated Adoption of AI-Driven Administrative Automation: Healthcare organizations report up to 42% reduction in manual billing errors through AI-powered claims and coding tools. AI-assisted scheduling systems have improved appointment utilization rates by 28%, enabling better resource allocation across hospitals and clinics.

Expansion of Cloud-Native and SaaS Platforms: More than 70% of new implementations now use cloud-based medical management software, reducing IT maintenance costs by 34%. SaaS models enable faster upgrades and support multi-location healthcare networks with centralized control.

Integration of Predictive Analytics and Dashboards: Predictive analytics tools embedded in management software help forecast patient volumes with 85% accuracy, supporting staffing and inventory planning. Real-time dashboards improve operational visibility and reduce administrative decision latency by 25%.

Strengthening Focus on Compliance and Cybersecurity: Healthcare organizations increased cybersecurity spending by 22%, integrating compliance monitoring directly into management platforms. Automated audit trails and access controls have reduced compliance-related incidents by 31%, reinforcing trust in digital administrative systems.

The Medical Management Software Market is segmented based on type, application, and end-user, reflecting how healthcare organizations deploy administrative and operational digital tools across varied care settings. By type, the market spans integrated platforms and modular solutions addressing billing, scheduling, documentation, and analytics. Application-based segmentation highlights the dominance of administrative and revenue-related workflows, while clinical-support integration is gaining importance. End-user segmentation shows differentiated adoption patterns among hospitals, clinics, and emerging care delivery models. Decision-makers increasingly evaluate solutions based on scalability, interoperability, and compliance readiness rather than single-function capability. Adoption intensity varies significantly across healthcare facility sizes, with larger systems prioritizing enterprise-wide integration and smaller providers favoring cloud-based, modular deployments. Together, these segments illustrate a market shaped by operational complexity, regulatory oversight, and the need for data-driven healthcare administration.

Medical Management Software is categorized into integrated medical management platforms, billing and revenue cycle management (RCM) software, appointment and scheduling systems, practice workflow management tools, and analytics and reporting modules. Integrated platforms represent the leading type, accounting for approximately 44% of total adoption, as healthcare organizations increasingly prefer unified systems that consolidate scheduling, billing, compliance, and reporting within a single interface. These platforms reduce system fragmentation and improve administrative coordination across departments. Billing and RCM software is the fastest-growing type, expanding at an estimated 11.2% CAGR, driven by rising reimbursement complexity, higher claim volumes, and payer scrutiny. Automation in coding, eligibility verification, and denial management is accelerating adoption. Scheduling and workflow management tools maintain steady relevance, particularly in outpatient and ambulatory settings, supporting patient flow optimization. Analytics and reporting modules, while smaller individually, are increasingly bundled with core systems to support performance monitoring and compliance. Collectively, these remaining types contribute a combined share of nearly 56%, underscoring the market’s multi-functional structure.

By application, the market includes administrative management, billing and claims processing, patient scheduling and coordination, compliance and reporting, and analytics-driven operational optimization. Administrative and billing-related applications dominate, with billing and claims processing accounting for roughly 39% of total usage, due to its direct impact on cash flow accuracy and operational continuity. Healthcare providers prioritize these applications to manage payer interactions and reduce rejection rates. Patient scheduling and coordination is the fastest-growing application, supported by a 10.6% CAGR, as providers aim to maximize resource utilization and reduce wait times. Digital scheduling tools integrated with reminders and analytics are increasingly deployed across outpatient and specialty clinics. Compliance and reporting applications remain essential due to expanding regulatory requirements, while analytics-driven applications support performance benchmarking and capacity planning. These remaining applications together represent a combined share of about 61%. From an adoption perspective, over 41% of healthcare enterprises globally reported piloting advanced scheduling and coordination software in 2024, while approximately 58% of hospitals in the U.S. are testing management applications that integrate administrative data with clinical records to improve throughput.

End-user segmentation includes hospitals, clinics and physician practices, ambulatory surgical centers, diagnostic laboratories, and other healthcare service providers. Hospitals form the leading end-user segment, accounting for nearly 47% of total adoption, driven by their complex administrative needs, multi-department operations, and high patient volumes. Large hospital systems favor enterprise-grade platforms capable of integrating finance, operations, and compliance. Clinics and physician practices represent the fastest-growing end-user group, expanding at an estimated 10.9% CAGR, supported by the shift toward digital-first outpatient care and subscription-based cloud solutions. Ambulatory surgical centers and diagnostic labs contribute steadily, focusing on scheduling precision and billing efficiency. These remaining end-users collectively hold a combined share of approximately 53%, reflecting broad-based adoption beyond hospitals. Adoption trends indicate that over 36% of mid-sized clinics globally adopted cloud-based medical management software in 2024, while around 49% of ambulatory centers reported improved operational visibility after implementation.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.1% between 2025 and 2032.

North America’s dominance is supported by over 6,000 hospitals, more than 230,000 physician practices, and healthcare IT penetration exceeding 85% across large facilities. Europe follows with nearly 27% market share, driven by regulatory digitalization mandates and cross-border healthcare data initiatives. Asia-Pacific currently represents around 23% of global demand, supported by rapid hospital construction, rising healthcare digitization budgets, and over 1.4 billion digitally connected healthcare consumers. South America and the Middle East & Africa together account for approximately 12%, reflecting emerging adoption supported by public-sector modernization programs, expanding private healthcare networks, and rising mobile-first software usage.

The region holds approximately 38% market share, supported by high digital maturity across hospitals, payers, and outpatient networks. Demand is driven primarily by hospitals, multi-specialty clinics, and integrated delivery networks, which together represent over 65% of deployments. Regulatory frameworks such as HIPAA and federal interoperability mandates continue to push upgrades in administrative platforms. Cloud-based deployments exceed 70% of new installations, while AI-assisted billing and scheduling tools are used by more than 45% of large healthcare systems. Local players such as Epic Systems and Athenahealth are expanding AI-enabled workflow automation and predictive scheduling modules. Consumer behavior shows higher enterprise adoption, with over 60% of healthcare organizations prioritizing centralized, enterprise-scale medical management platforms.

Europe accounts for nearly 27% of global market share, with Germany, the UK, and France representing more than 55% of regional demand. Regulatory bodies enforcing GDPR and national eHealth strategies are accelerating adoption of compliant, auditable software systems. Over 68% of hospitals in Western Europe now use digital administrative platforms linked with national health records. Emerging technologies such as AI-driven compliance monitoring and multilingual billing interfaces are increasingly deployed. Local vendors and regional system integrators are focusing on explainable automation and secure data residency. Consumer behavior reflects regulatory pressure, with healthcare providers prioritizing transparency, auditability, and explainable system outputs in procurement decisions.

Asia-Pacific ranks as the fastest-expanding regional market, contributing approximately 23% of global volume. China, India, and Japan collectively account for over 70% of regional deployments. The region has added more than 18,000 new hospitals over the past decade, significantly expanding demand for scalable administrative software. Cloud-first and mobile-enabled platforms dominate, with over 60% of new users accessing management systems via mobile devices. Innovation hubs in India, China, and Singapore are driving AI-enabled scheduling and multilingual billing solutions. Consumer behavior reflects mobile-first adoption, with growth fueled by digital health apps, telemedicine integration, and expanding private healthcare networks.

South America holds roughly 7% of global market share, led by Brazil and Argentina, which together account for more than 60% of regional adoption. Government-led healthcare modernization initiatives and expanding private hospital chains are key demand drivers. Infrastructure digitization efforts have increased hospital IT spending by over 30% in major economies. Local software providers focus on cost-effective, cloud-based platforms tailored for public healthcare systems. Consumer behavior is influenced by localization needs, with strong demand for multilingual interfaces and region-specific billing workflows aligned with national reimbursement systems.

The Middle East & Africa region represents approximately 5% of global demand, with the UAE and South Africa as leading markets. Large-scale hospital construction programs and healthcare diversification strategies are accelerating adoption. Over 40% of new hospitals in the Gulf region are built with integrated digital administration systems. Governments support digital health through national health information exchanges and public-private partnerships. Local and regional vendors are deploying cloud-based platforms optimized for multi-facility management. Consumer behavior varies widely, with higher adoption among private healthcare providers and urban medical hubs prioritizing digital efficiency.

United States – 31% Market Share: Strong enterprise healthcare IT infrastructure, high hospital digitization, and regulatory-driven software upgrades.

Germany – 9% Market Share: Robust hospital networks, strict compliance requirements, and nationwide eHealth digitalization initiatives.

The Medical Management Software Market is characterized by a moderately consolidated yet highly competitive environment with numerous global and regional vendors striving for differentiation through innovation, integrations, and strategic partnerships. Industry analysis indicates 25 + major competitors actively offering practice management, EHR integration, billing automation, and AI-driven clinical support tools. Leading players such as Epic Systems, Cerner (Oracle Health), Allscripts Healthcare, athenahealth, and eClinicalWorks dominate market positioning, supported by extensive deployments in hospitals, clinics, and ambulatory care networks worldwide. Epic Systems alone supports over 305 million patient records globally and is widely regarded as a benchmark in large-scale clinical software implementation.

Competition in this market is driven by strategic initiatives such as product launches, acquisitions, and partnerships. For example, Waystar’s acquisition of Iodine Software in 2025 for approximately $1.25 billion highlights consolidation activity aimed at strengthening AI-driven documentation and claims automation capabilities across provider networks. Similarly, clearlake Capital’s intended majority acquisition of Modernizing Medicine (ModMed) valued around $5.3 billion underscores strong private-equity inflows and valuation expansion in specialized healthcare software solutions.

Innovation trends significantly shape competition, with AI and cloud-native platforms enabling predictive analytics, automated clinical documentation, interoperability, and real-time decision support. Vendors are increasingly integrating machine learning for predictive insights and workflow automation, while cloud deployments continue to enable scalability and faster updates across multi-site practices. Interoperability standards and regulatory compliance (e.g., HIPAA, EU GDPR) further drive differentiation, as solutions capable of seamless data exchange attract larger enterprise clients. Overall, the top 5 companies collectively capture a substantial portion of global installations (estimated 40–50 % combined share), though emerging mid-tier innovators continue to intensify competitive pressure with niche and specialized offerings.

eClinicalWorks LLC

Tebra

CompuGroup Medical SE & Co. KGaA

CareCloud, Inc.

The Medical Management Software Market is undergoing rapid technological evolution driven by AI, cloud computing, interoperability standards, and mobile-first solutions. Cloud-native architectures are now mainstream, with many providers offering software-as-a-service (SaaS) models enabling multi-tenant scalability, real-time updates, and reduced on-premises IT overhead. A significant shift toward cloud-hosted practice management, patient portals, and telehealth integration reflects the priority on seamless remote access and cross-platform availability for providers and patients alike.

Artificial intelligence (AI) and machine learning (ML) have emerged as pivotal technologies reshaping core functionalities. AI-powered modules automate clinical documentation, predictive appointment scheduling, billing reconciliation, and decision support. For instance, analytics engines now leverage vast datasets to generate predictive insights for patient outcomes, optimize physician workflows, and reduce administrative workloads, accelerating clinical throughput without sacrificing accuracy. Real-time natural language processing (NLP) tools are also being embedded into EHR interfaces to convert clinician speech into structured medical notes, significantly cutting documentation times.

Interoperability technologies such as FHIR (Fast Healthcare Interoperability Resources) and APIs are enabling smoother data exchange across disparate systems, improving cross-organization care coordination and compliance with regulatory frameworks. This trend is also enhancing population health analytics, where aggregated patient data can be processed to identify patterns in chronic conditions and guide preventive strategies at scale. Furthermore, mobile health apps and patient engagement tools are integrating with central practice management systems, facilitating appointment management, remote check-ins, and secure messaging, increasing patient satisfaction and retention.

Cybersecurity and privacy technologies remain critical, with advanced encryption, access controls, and secure authentication safeguarding sensitive health information against cyber threats. As digital health ecosystems expand to support IoT devices and wearable integrations, secure data pipelines are essential to maintain compliance and trust.

Overall, the convergence of cloud platforms, AI augmentation, interoperability standards, and mobile-centric experiences is redefining medical management software capabilities, enabling data-driven, efficient, and patient-centric healthcare delivery.

In March 2025, Epic Systems Corporation expanded interoperability capabilities by previewing new developer tools and data-sharing features designed to simplify patient and provider data exchange via APIs, supporting more streamlined clinical workflows and broader integration across health IT ecosystems. Source: www.fiercehealthcare.com

In July 2025, Waystar completed its strategic acquisition of Iodine Software for $1.25 billion in cash and stock, further integrating AI-driven documentation and claims automation tools into its healthcare software suite to enhance administrative efficiency for providers. Source: www.wsj.com

In 2024–2025, athenahealth unveiled enhanced interoperability and payer partnership capabilities at HIMSS 2024, showcasing solutions aimed at delivering next-generation data exchange experiences and AI-informed clinical insights to simplify care delivery and administrative tasks. Source: www.athenahealth.com

In August 2025, MyMichigan Health and Nimkee Memorial Wellness Center launched a collaboration to implement Epic’s Community Connect EMR platform, enabling shared electronic medical records to improve coordination and access to care for patients across multiple sites. Source: www.ourmidland.com

The scope of the Medical Management Software Market Report encompasses a comprehensive examination of product types, application areas, end-user segments, and global geographic footprints. Product coverage includes practice management systems, EHR-integrated management suites, patient scheduling and registration modules, billing and claims processing tools, analytics and reporting platforms, and mobile engagement solutions. Each product category is delineated by functional capabilities, deployment models (cloud-based vs. on-premises), and integration with emerging technologies such as AI and interoperable standards.

Application segments focus on hospitals, clinics, ambulatory care centres, specialty practices, and diagnostic laboratories, with detailed breakdowns highlighting usage patterns, deployment scales, and operational priorities. End-user insights extend to healthcare providers, administrative teams, payers, and patients, outlining how software solutions enhance efficiency, compliance, and experience across diverse organizational structures.

Geographically, the report spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, providing data on technology adoption, regulatory landscapes, and regional trends influencing software uptake. The analysis includes demographic and infrastructure variables that shape regional market dynamics, such as healthcare digitization rates, IT spending levels, and interoperability mandates.

Additionally, the report evaluates emerging and niche market segments such as AI-augmented workflow automation, telehealth integrations, mobile patient engagement, and predictive analytics. It also covers competitive landscapes, strategic initiatives (partnerships, mergers, acquisitions), and innovation trajectories that inform investment and operational decision-making. Insights into cybersecurity priorities, data governance frameworks, and interoperability standards further enrich the market context, offering decision-makers a detailed and actionable understanding of current conditions and future opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 887.0 Million |

| Market Revenue (2032) | USD 1,806.7 Million |

| CAGR (2025–2032) | 9.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Epic Systems Corporation; Cerner (Oracle Health); athenahealth, Inc.; Allscripts Healthcare Solutions; eClinicalWorks LLC; Tebra; CompuGroup Medical; CareCloud, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |