Reports

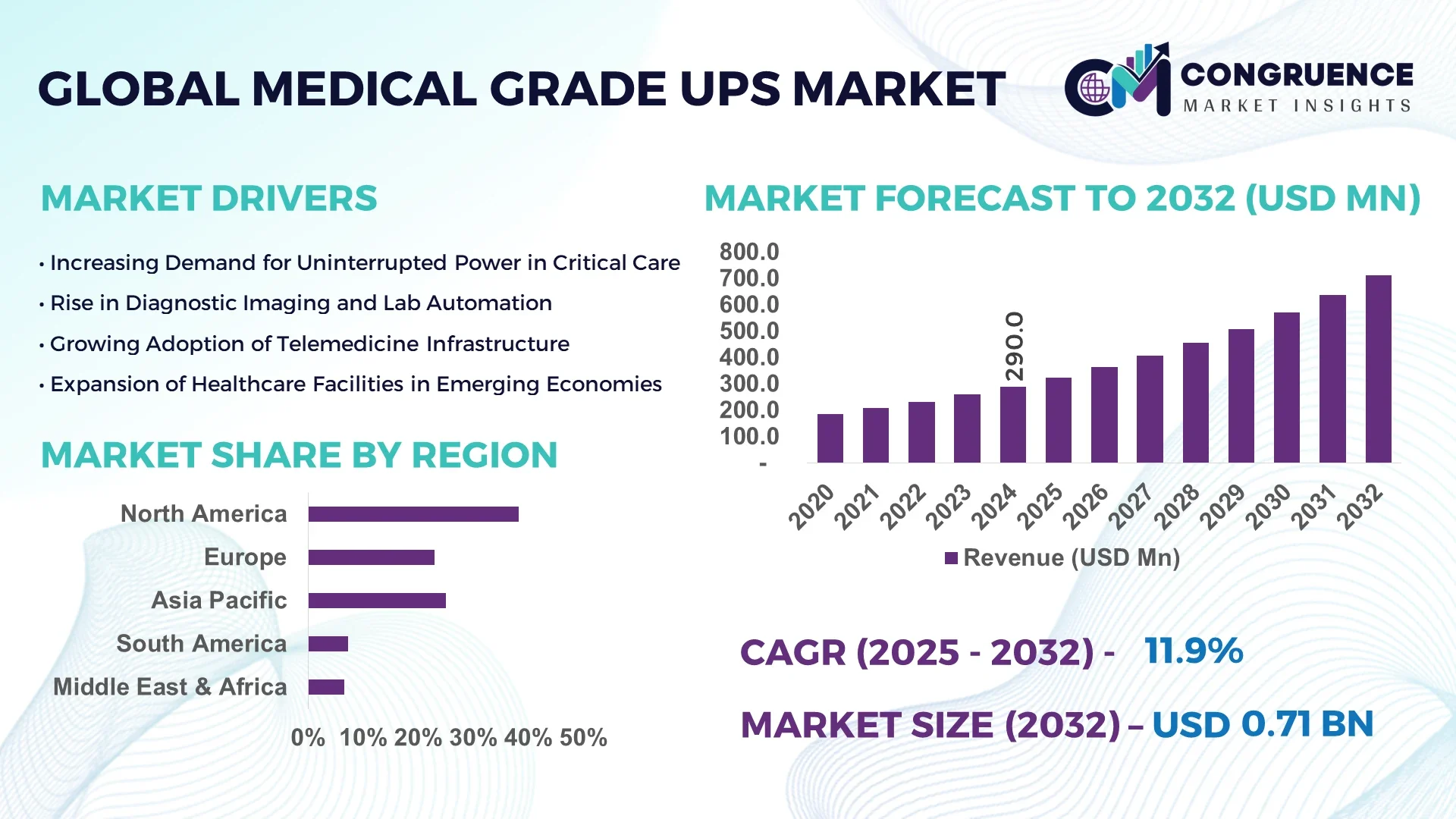

The Global Medical Grade UPS Market was valued at USD 290 Million in 2024 and is anticipated to reach a value of USD 712.9 Million by 2032 expanding at a CAGR of 11.9% between 2025 and 2032.

North America leads global production capacity for medical-grade UPS, with the United States operating several high-output manufacturing plants focused on supplying modular and high-efficiency lithium-ion systems. Continuous multi‑million‑dollar investments in advanced battery integration, hospital-grade certification capabilities, and digital twin testing environments underscore its technological edge. The region’s industrial ecosystem supports large-scale deployment across hospitals, diagnostic labs, imaging centers, and data-centric applications.

The Medical Grade UPS Market spans key industry sectors—hospitals demand high-reliability online UPS systems, clinics prefer compact line-interactive units, and research labs increasingly adopt modular solutions. Recent technological innovation includes intelligent lithium‑ion packs with integrated IoT monitoring, hybrid solar‑UPS systems for off‑grid facilities, and GaN/SiC-based solid-state UPS achieving >99% efficiency. Regulatory and environmental drivers—such as stricter IEC 60601 standards and global sustainability commitments—are prompting manufacturers to optimize energy efficiency and reduce carbon footprints. Economic factors like rising healthcare infrastructure investments in Asia-Pacific and green financing incentives in Europe have shifted consumption patterns, accelerating regional uptake. Emerging trends include AI-powered predictive maintenance platforms, DC microgrid integration for rural clinics, and remote-managed UPS-as-a-Service models. Overall, market outlook indicates robust diversification across product designs, geographies, and service-based offerings.

The infusion of artificial intelligence into the Medical Grade UPS Market is revolutionizing operational resilience and uptime for critical medical environments. AI-driven platforms now play a central role in enhancing system efficiency by continuously analyzing power load fluctuations, battery health parameters, and environmental influences in real time. Leading UPS manufacturers have installed intelligent diagnostics that detect anomalies—such as temperature spikes or battery degradation—well before they escalate into system failures, enabling preventive interventions and minimizing unplanned downtime.

Operational performance is being elevated through dynamic load‑balancing algorithms, which reallocate energy usage across redundant UPS modules to optimize performance under varying equipment demands. Hospitals with multiple operating rooms or intensive care units benefit from AI-enabled load scheduling, which ensures uninterrupted function while extending battery endurance and reducing wear. Moreover, AI analytics identify inefficiencies in energy conversion and heat dispersion, driving finely tuned configuration adjustments that help cut energy losses and improve efficiency by as much as 5–8%.

Process optimization is also receiving a boost. Maintenance workflows are now scheduled based on predictive risk scores generated from tens of thousands of sensor data points, replacing conventional fixed-interval servicing. This extends component lifespan and lowers lifecycle maintenance costs. In addition, remote AI platforms aggregate data from UPS fleets installed across clinics and hospitals, benchmarking performance, and enabling centralized optimization without field visits.

By embedding AI within Medical Grade UPS systems, stakeholders—ranging from hospital CIOs to facility managers—gain unprecedented visibility into power infrastructure health. Real‑time alerts and trend-based risk charts support data‑driven decision-making to uphold compliance with patient safety mandates. The Medical Grade UPS Market is clearly entering a new era of intelligent power management, where AI ensures systems are adaptive, predictable, and aligned with the rigorous uptime demands of medical settings.

“In 2024, a major UPS provider integrated AI-based analytics into its 120 kVA lithium‑ion units, enabling battery health predictions with 90% accuracy and extending replacement intervals by 25%.”

The Medical Grade UPS Market is experiencing dynamic evolution driven by shifting industry standards, technological progress, and changes in infrastructure demands. Trends include the migration from traditional lead‑acid to lithium‑ion and solid‑state battery systems, reflecting needs for higher energy density and reduced maintenance. Regulatory frameworks, such as IEC 60601‑2‑24, now require enhanced output quality and resilience, increasing system complexity. Healthcare providers are favoring modular architectures—which allow capacity scaling and redundancy—reflecting sensitivity to space and investment constraints. Economic pressures, environmental mandates, and infrastructure expansion in emerging markets are collectively reshaping supply chains and procurement strategies, necessitating agile production and adaptive product design. The landscape is thus characterized by converging demands for efficiency, compliance, scalability, and long-term operational reliability.

Remote healthcare services surged during and after the COVID-19 pandemic, driving the need for reliable power backup in decentralized clinical settings and home-health hubs. Medical Grade UPS systems are now essential for telehealth equipment, remote diagnostics, and IoT-enabled patient-monitoring devices. In 2024 alone, over 40% of new outpatient clinics in North America and Europe incorporated dedicated UPS units to support telemedicine terminals, reflecting a structural shift toward distributed care. The result has been improved uptime during unpredictable grid events, maintaining continuity for life-critical consultations and data transmission. By shielding telehealth systems from power interruptions, these UPS installations are also lowering the risk of misinformation, data loss, and patient safety incidents.

The deployment of Medical Grade UPS systems requires sizable upfront capital. Advanced configurations—such as modular lithium-ion or hybrid solar-integrated units—can add 20–30% to initial project budgets compared to basic line-interactive models. This financial burden is amplified when integrating new equipment into legacy hospital infrastructure, which often involves rewiring, harmonic filtering, and regulatory testing. In many mid‑sized clinics, such integration delays installations by 6–12 months, and cost overruns often reach 15% over initial estimates. These factors are causing procurement committees to defer upgrades, particularly in facilities with tight budgets or older infrastructure, despite the long‑term reliability benefits.

Emerging economies, particularly in Southeast Asia and Africa, are rapidly modernizing healthcare systems. However, outright purchase of advanced Medical Grade UPS units remains cost-prohibitive for many facilities. Manufacturers are bridging this gap by offering UPS-as-a-Service contracts and leasing models, allowing hospitals to access high-end equipment and support services without hefty capital costs. In India and Nigeria, pilot programs launched in 2024 saw over 120 hospitals adopt lease-based UPS systems, with monthly costs ranging between USD 300–500—approximately 40% lower than outright purchase financing. These arrangements also include remote monitoring and scheduled maintenance, reducing operational risks and entry barriers for advanced power backup infrastructure.

Medical Grade UPS systems must comply with a web of overlapping standards—IEC 60601‑2‑24 for medical electrical systems, ISO 13485 for device quality management, and HIPAA-related data protections tied to UPS telemetry. Navigating these standards represents a significant hurdle: each UPS unit requires extensive validation and specialized documentation before clinical deployment. In practice, the testing protocols add 3‑4 weeks per certification cycle and cost USD 10,000–15,000 annually per device. Moreover, simultaneous compliance with renewable-energy regulations (e.g., EU Ecodesign) introduces further design complexity. These cumulative burdens slow product rollouts and demand higher in-house quality assurance capabilities from manufacturers and installers.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Medical Grade UPS Market. Pre-fabricated elements for UPS enclosure systems are built off-site with automated precision, reducing on-site labor by 30% and compressing delivery lead times by up to 25%. Hospitals in Europe and North America now favor plug-and-play UPS modules that can be rapidly installed and scaled, making precise automation and robotics-driven factory lines essential for delivering these pre-built solutions.

Integration of DC Microgrid Architectures: More facilities are converting central power systems to DC microgrids, reducing conversion loss by approximately 8–10%. Modern Medical Grade UPS systems now support 380 V DC bus integration alongside AC outputs, enabling direct supply to imaging devices and LED surgical lighting. This shift streamlines energy flow and reduces reliance on multiple conversions—improving grid stability and increasing power efficiency within critical care environments.

Hybrid Solar‑UPS Deployments in Off‑Grid Clinics: Rural clinics, especially in Africa and South Asia, are deploying hybrid UPS systems combining photovoltaic arrays with battery storage. These systems maintain continuous operations during both power outages and night-time hours, enabling UPS uptime of up to 6 hours without grid support. This model has led to a 20% improvement in clinic operational continuity and reduced diesel generator usage by 70%, demonstrating significant environmental benefits.

Smart Remote Monitoring and UPS-as-a-Service Offerings: Vendors are now listing remote monitoring capabilities as standard functionalities within Medical Grade UPS Market offerings. Real-time dashboards, remote firmware updates, and automated service triggers are becoming business-as-usual. In 2024, remote diagnostics were used in over 50% of new UPS installations, allowing predictive alerts and firmware tuning to occur without technician dispatch—cutting average service response time in half across multi-unit installations.

The Medical Grade UPS Market is segmented across three primary dimensions: type, application, and end-user. These segments define the structure of demand and supply in the industry and reveal evolving patterns of product usage, integration preferences, and procurement strategies. In terms of product type, the market is differentiated based on UPS configuration and power range, including line-interactive, online, and standalone units. Applications span from life-support systems to diagnostic imaging and laboratory automation. End-users include hospitals, ambulatory surgical centers, diagnostic labs, and specialty clinics. Each of these segments reflects specific performance needs, regulatory considerations, and operational constraints. Segmentation analysis helps stakeholders align product design and investment focus with real-world deployment environments, facilitating targeted growth strategies and optimizing supply chain efficiency.

Medical Grade UPS systems are categorized primarily into Online/Double-Conversion, Line-Interactive, and Standalone/Battery Backup types. Online UPS systems represent the leading segment due to their ability to provide uninterrupted power without switching delays—an essential feature for surgical suites and critical care units. Their consistent voltage and frequency output also meets stringent regulatory compliance for life-saving equipment.

Line-Interactive UPS systems are the fastest-growing type, driven by their balance of affordability and reliability. These systems are increasingly used in outpatient clinics and remote health centers where space and budgets are constrained but regulated uptime is still critical. Their adaptive voltage regulation and compact design are well-suited for distributed healthcare infrastructure.

Standalone battery-based UPS systems maintain a niche but important presence in laboratories and point-of-care testing environments. These systems offer flexibility and are often integrated into mobile diagnostic units. While they may not support prolonged backup, their portability and ease of deployment make them valuable in certain low-load use cases.

The most dominant application for Medical Grade UPS systems is in surgical and intensive care operations. These settings demand zero power fluctuation and uninterrupted supply for life-critical machines such as ventilators, anesthesia equipment, and monitoring devices. High-frequency power disturbances in such environments can have direct patient safety consequences, which elevates the requirement for robust UPS systems.

The fastest-growing application lies in diagnostic imaging, particularly MRI, CT, and PET scan systems. These machines require continuous power to prevent calibration loss and equipment damage during outages. The shift toward digitized imaging and increasing adoption of AI-powered analytics in radiology have further increased the sensitivity to power quality, fueling demand for high-efficiency UPS units.

Other applications include laboratory automation, remote diagnostics, and electronic health records infrastructure. In these areas, UPS units help maintain system integrity, protect stored data, and ensure uninterrupted operation of processing equipment. Although they represent a smaller portion of the market, they play an integral role in holistic hospital and clinic operations.

Hospitals constitute the leading end-user segment in the Medical Grade UPS Market. Their comprehensive power demand, coupled with regulatory obligations for continuous operation of critical systems, makes UPS integration indispensable. Modern hospitals often deploy multi-tiered UPS systems across departments to ensure redundancy and prioritize power distribution to critical care zones.

Diagnostic laboratories are the fastest-growing end-user category. The rise in high-throughput testing, real-time PCR platforms, and AI-integrated diagnostic devices has increased reliance on stable power infrastructure. Additionally, many labs are now operational around the clock, making uptime a key differentiator in lab performance and reliability.

Ambulatory surgical centers and specialized clinics also contribute to the market, particularly as these facilities expand in number and service complexity. They typically require compact, modular UPS units with remote management capabilities. These end-users benefit from reduced physical footprint requirements and are increasingly adopting scalable systems that grow with operational demands.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.6% between 2025 and 2032.

The dominance of North America is driven by well-established healthcare infrastructure, robust adoption of digital health technologies, and stringent regulatory standards that mandate reliable power backup systems. In contrast, Asia-Pacific is witnessing accelerated healthcare investments, increasing hospital construction, and widespread adoption of lithium-ion and modular UPS systems across emerging economies like India and China. Europe maintains a significant share as well, driven by sustainability initiatives and strong enforcement of healthcare quality standards. Meanwhile, South America and the Middle East & Africa are showing steady progress fueled by infrastructure modernization, public health reforms, and expanding diagnostic lab networks. Region-wise analysis indicates growing diversification in power needs, UPS deployment models, and supply chain adaptations, reinforcing regional strategy importance for manufacturers and investors in the Medical Grade UPS Market.

North America held 38.2% of the global Medical Grade UPS Market in 2024, led primarily by the United States and Canada. The region’s demand is fueled by hospitals, diagnostic labs, and specialty clinics deploying high-performance UPS systems to support critical functions such as ICU power delivery, telehealth platforms, and AI-enabled diagnostics. Regulatory reforms—such as modernization of CMS facility requirements and NFPA 99 power continuity mandates—have intensified adoption of hospital-grade UPS infrastructure. Government funding through infrastructure bills and health tech grants has accelerated installations in both urban and rural networks. Technological advancements, especially the integration of remote monitoring, lithium-ion architecture, and intelligent battery management systems, are standardizing digital transformation in power continuity. This has also led to widespread uptake of predictive maintenance solutions and UPS-as-a-Service models, reducing downtime and extending lifecycle performance across healthcare facilities.

Europe accounted for 28.6% of the global Medical Grade UPS Market share in 2024, with Germany, the UK, and France emerging as the dominant markets. This demand stems from a proactive healthcare modernization strategy and robust compliance with EU medical equipment power standards. Institutions across the region are rapidly phasing out lead-acid UPS systems in favor of energy-efficient lithium-ion and hybrid models aligned with EU Ecodesign directives. National health authorities and regulatory bodies—such as the European Medicines Agency and national building codes—are driving systemic upgrades to emergency backup systems. Adoption of smart UPS units with IoT-based telemetry, battery optimization, and remote failure detection is gaining pace. Additionally, hospitals in Scandinavia and the DACH region are leading pilots for UPS systems with integrated renewable inputs, further pushing Europe toward greener, more efficient power management within clinical environments.

Asia-Pacific is emerging as the fastest-growing region in the Medical Grade UPS Market, with key consumption concentrated in China, India, and Japan. The region ranked second in total market volume in 2024 and is experiencing rapid growth fueled by aggressive healthcare infrastructure expansion and rising medical equipment penetration. China’s public and private hospital projects are demanding high-volume UPS deployments to support operating theatres and imaging centers. India is investing in digital healthcare and remote primary care facilities where compact UPS systems with intelligent monitoring are critical. Japan, with its aging population and tech-forward hospitals, is investing heavily in advanced power systems with modular scalability. Innovation hubs in South Korea and Singapore are developing next-gen UPS solutions incorporating AI-based load prediction and hybrid solar-UPS integration. Collectively, the region’s power management transformation is characterized by demand for scalable, efficient, and low-footprint solutions tailored to densely populated urban and rural applications.

South America, led by Brazil and Argentina, accounted for approximately 6.4% of the Medical Grade UPS Market in 2024. The region is showing steady advancement in demand for mid-tier UPS systems as public healthcare infrastructure undergoes modernization. Brazil’s Ministry of Health initiatives have supported upgrades across public hospitals and diagnostic centers, with a particular focus on uninterrupted power for surgical and laboratory units. Argentina’s energy-efficient hospital campaigns are supporting local UPS deployment, especially in provincial regions prone to frequent blackouts. Infrastructure trends across the region include increased adoption of prefabricated power modules and localized battery assembly units. Government incentives in the form of tax relief and accelerated depreciation on capital medical equipment are further propelling the UPS market forward. Trade relationships with North American and European OEMs have enabled better access to modular UPS technologies tailored to South American grid variability and infrastructure limitations.

The Middle East & Africa Medical Grade UPS Market is gaining traction with growing demand across UAE, Saudi Arabia, and South Africa. In 2024, this region contributed roughly 4.8% to the global market. Strong oil & gas economies like the UAE are reinvesting revenues into world-class healthcare infrastructure, leading to significant UPS system deployments in new mega-hospitals and specialty medical centers. South Africa, facing aging grid infrastructure, has made Medical Grade UPS systems a requirement in many private hospitals and rural clinics. Technological modernization is a key theme, with leading facilities integrating cloud-based UPS monitoring and remote battery diagnostics. Trade partnerships with European UPS vendors and regional initiatives like Vision 2030 in Saudi Arabia are supporting the scaling of smart healthcare technologies. Regulatory frameworks are evolving to support energy resilience, and several nations now include UPS solutions in public tender mandates for critical-care power assurance.

United States – 29.4% Market Share

High production capacity, regulatory-backed healthcare infrastructure, and widespread adoption of AI-integrated UPS solutions support its leadership in the Medical Grade UPS Market.

China – 17.6% Market Share

Strong end-user demand, extensive hospital construction, and rapid integration of modular power systems across urban and rural networks drive its market dominance.

The competitive landscape of the Medical Grade UPS Market is defined by a mix of global power solution providers, medical equipment specialists, and niche UPS manufacturers focusing on healthcare infrastructure. As of 2024, there are more than 45 active companies competing in this space globally, with a concentration of innovation coming from North America, Europe, and East Asia. Companies are prioritizing modular design, lithium-ion integration, and intelligent battery management systems to address the growing demand for flexibility and remote operability in clinical environments.

Strategic initiatives continue to shape market dynamics. In 2023 and 2024, there were several product launches featuring compact UPS systems with IoT-based predictive maintenance and hot-swappable battery modules. Leading players are also entering strategic partnerships with hospital networks and healthcare IT providers to deliver UPS-as-a-Service and smart energy management platforms. Mergers and acquisitions are prevalent, especially among firms seeking to consolidate expertise in battery chemistry and AI integration.

Innovation trends are moving toward AI-enhanced diagnostics, remote firmware updates, and low-carbon footprint UPS solutions. Companies are investing in sustainability certifications and enhancing compliance with international healthcare power standards like IEC 60601. The competition is increasingly defined not only by hardware quality but by the software ecosystem, service contracts, and digital integration capabilities bundled with each UPS system.

Eaton Corporation

Schneider Electric

Vertiv Holdings Co

Tripp Lite (now part of Eaton, but operates as an independent brand)

Delta Electronics Inc.

Socomec Group

Riello UPS

CyberPower Systems, Inc.

ABB Ltd.

Kehua Tech

Hitachi Energy

Fuji Electric Co., Ltd.

AEG Power Solutions

Technological advancements are at the core of transformation in the Medical Grade UPS Market. Modern systems are increasingly built around lithium-ion battery technologies, replacing traditional VRLA (valve-regulated lead-acid) batteries due to their superior cycle life, faster recharge rates, and reduced maintenance requirements. Lithium-ion UPS units now offer up to 60% weight reduction and 50% footprint savings, making them ideal for space-constrained hospital environments.

A significant development is the integration of AI-powered analytics and predictive maintenance. Advanced UPS systems can now track thousands of data points—including ambient temperature, charge cycles, and voltage fluctuations—to optimize performance and alert maintenance teams before failures occur. Real-time monitoring through web dashboards or mobile apps has become standard, reducing service downtimes by up to 40%.

Another notable trend is the rise of modular UPS architecture. These systems allow scalability by adding or removing power modules without service interruption, increasing redundancy and operational flexibility. Hot-swappable modules also enable uninterrupted power in mission-critical areas like intensive care units or surgical wings.

Additionally, UPS-as-a-Service (UPSaaS) is emerging as a digital service model, especially in developing markets. Facilities subscribe to power continuity with full-service packages, including equipment, monitoring, and maintenance. Smart grid compatibility and DC microgrid integration are also on the rise, with next-gen UPS solutions offering hybrid AC/DC outputs to match evolving hospital electrical configurations and reduce conversion losses.

Finally, green innovations like UPS units with biodegradable casings, solar-compatible inputs, and intelligent energy use tracking are gaining traction, aligning with hospital sustainability goals and regional carbon compliance mandates.

• In February 2024, Eaton launched its 9PX lithium-ion UPS system for healthcare applications, delivering over 8 years of expected battery life and reducing maintenance interventions by up to 70%.

• In September 2023, Schneider Electric introduced EcoStruxure™ UPS with AI-based energy analytics for hospital environments, allowing load forecasting and reducing unplanned downtime across multi-unit deployments.

• In March 2024, Delta Electronics announced a new 3-phase modular UPS for medical imaging centers, offering scalable capacity from 20 kVA to 120 kVA with hot-swappable components and 96% energy efficiency.

• In October 2023, Vertiv unveiled its SmartMod™ medical-grade UPS modules in Singapore, which integrate AI diagnostics, lithium-ion batteries, and centralized energy management for mid-sized hospitals.

The scope of the Medical Grade UPS Market Report spans the full spectrum of healthcare power continuity systems, covering product types, application domains, technologies, and regional dynamics. It investigates three major product categories—online/double-conversion UPS, line-interactive systems, and standalone battery backup units—analyzing their usage across diverse healthcare environments.

From an application standpoint, the report focuses on areas such as surgical power support, diagnostic imaging stability, laboratory automation, and telemedicine infrastructure. It offers granular insights into how each application area uniquely shapes demand characteristics, influencing design priorities like redundancy, size constraints, and remote monitoring.

Geographically, the report evaluates the market across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing comparative insights into infrastructure maturity, healthcare investment trends, and power grid reliability. Emphasis is placed on top-consuming countries such as the United States, China, India, Germany, and Brazil.

On the technology front, the report assesses trends in lithium-ion UPS, modular designs, AI-based diagnostics, smart energy management platforms, and hybrid solar-integrated systems. Additionally, it addresses regulatory considerations, lifecycle management strategies, and adoption models like UPS-as-a-Service and DC microgrid-enabled UPS.

The report also highlights emerging segments such as UPS for mobile health clinics, disaster relief setups, and remote diagnostic pods—markets gaining relevance in developing economies and post-pandemic infrastructure strategies. With a structured, insight-driven approach, this report provides decision-makers with actionable intelligence to guide product development, investment, and market entry strategies.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 290.0 Million |

| Market Revenue (2032) | USD 712.9 Million |

| CAGR (2025–2032) | 11.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Eaton Corporation, Schneider Electric, Vertiv Holdings Co, Tripp Lite (now part of Eaton, but operates as an independent brand), Delta Electronics Inc., Socomec Group, Riello UPS, CyberPower Systems, Inc., ABB Ltd., Kehua Tech, Hitachi Energy, Fuji Electric Co., Ltd., AEG Power Solutions |

| Customization & Pricing | Available on Request (10% Customization is Free) |