Reports

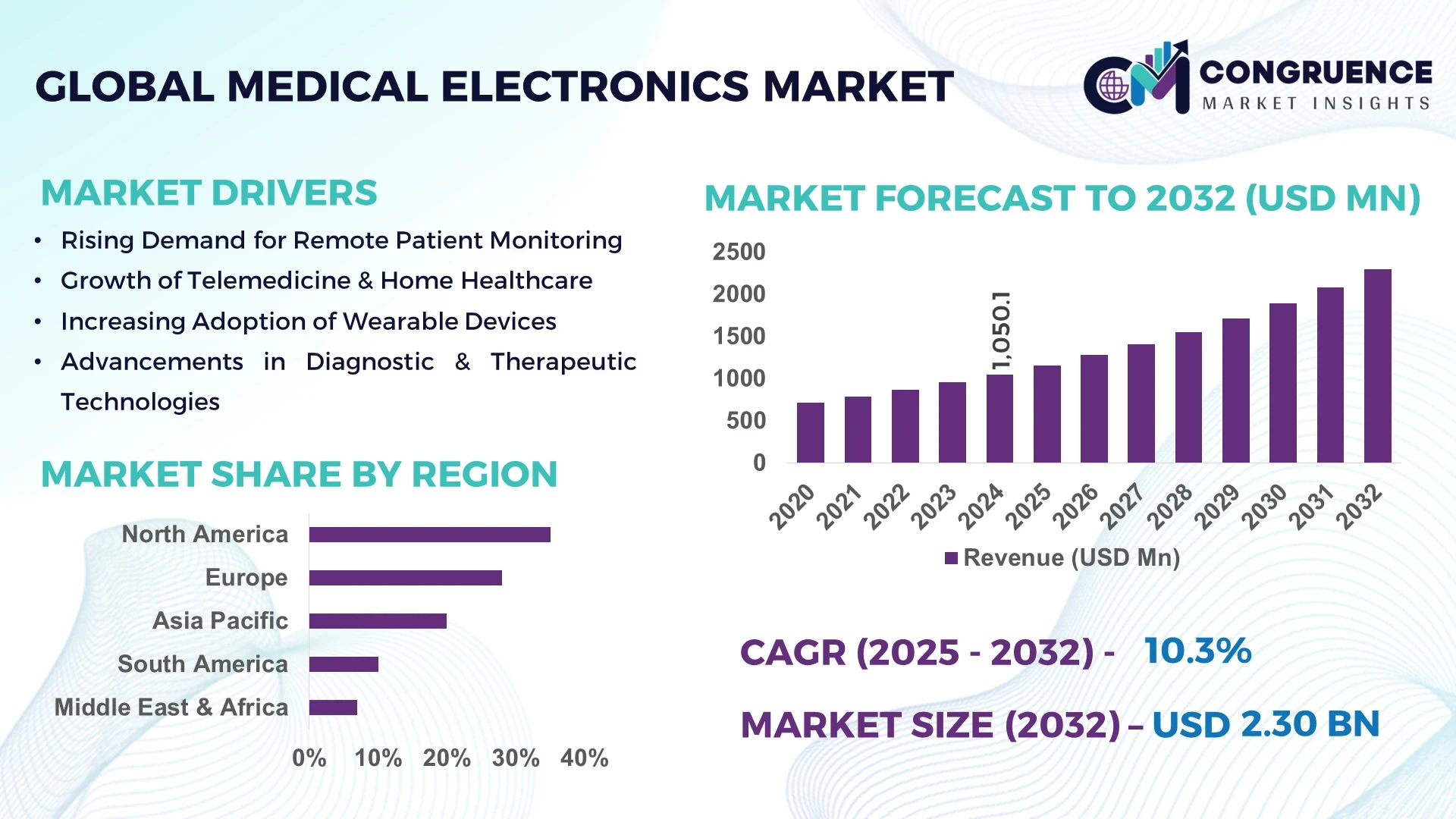

The Global Medical Electronics Market was valued at USD 1,050.1 Million in 2024 and is anticipated to reach a value of USD 2,297.2 Million by 2032 expanding at a CAGR of 10.28% between 2025 and 2032.

In the United States, the dominant country in the Medical Electronics Market, production capacity includes thousands of high-tech manufacturing facilities capable of producing diagnostic, therapeutic, and wearable devices at scale. Investment levels are significant, supported by both private and public funding programs, targeting innovation in AI-assisted diagnostics, patient monitoring, and portable medical electronics. Key industry applications span hospitals, research laboratories, outpatient clinics, and home healthcare, while technological advancements focus on miniaturized sensors, energy-efficient microcontrollers, and integrated IoT-enabled medical solutions.

The broader Medical Electronics Market encompasses multiple sectors, including diagnostic imaging, patient monitoring, surgical instrumentation, wearable electronics, and therapeutic devices. Diagnostics continues to lead in adoption due to its critical role in early disease detection, while therapeutic and monitoring devices are evolving with AI and connectivity integration. Regulatory factors are influencing product design, emphasizing safety, cybersecurity, and compliance. Environmental considerations include energy-efficient devices and sustainable materials. Regional consumption patterns vary, with North America and Europe adopting advanced hospital systems, and Asia-Pacific experiencing rapid growth in wearable and home-based devices. Emerging trends include telemedicine integration, AI-enhanced diagnostics, modular designs, and smart medical devices capable of real-time patient data analysis, shaping the future outlook of the Medical Electronics Market.

Artificial Intelligence is revolutionizing the Medical Electronics Market by enhancing operational efficiency, accuracy, and process optimization across diagnostics, therapeutics, and patient-monitoring systems. In clinical settings, AI-enabled devices improve image analysis, detect anomalies in real-time, and reduce manual intervention. For instance, AI-assisted radiology platforms can analyze thousands of images per hour, improving workflow speed and diagnostic consistency. In manufacturing, AI algorithms optimize production lines for microcontrollers, sensors, and imaging devices, reducing errors and improving output quality. Edge AI integration in wearable and remote-monitoring devices enables local data processing, minimizing latency and supporting immediate clinical decision-making. Supply chains also benefit from AI-driven predictive maintenance, inventory management, and quality control, allowing manufacturers to manage component shortages and logistics efficiently. AI facilitates regulatory compliance by automatically monitoring device performance and detecting deviations, which streamlines certification processes. Collectively, these applications demonstrate that AI not only accelerates innovation in device functionality but also enhances operational performance, security, and patient-centric care delivery within the Medical Electronics Market.

"In late 2024, STMicroelectronics launched its STM32N6 series of edge-AI microcontrollers, enabling on-device processing for wearable and medical monitoring devices. These microcontrollers reduced decision-latency by 35% and decreased energy consumption by 20% in clinical applications."

The Medical Electronics Market is influenced by technological convergence, healthcare infrastructure expansion, and evolving patient care models. Key trends include the rising demand for AI-enabled diagnostics, portable monitoring devices, and wearable electronics for chronic disease management. Supply chain disruptions, component scarcity, and global semiconductor demand affect production planning. Hospitals and outpatient facilities increasingly require interoperable devices capable of seamless integration with electronic health records, emphasizing connectivity and data security. Economic and regulatory factors also shape market strategies, including government support for domestic manufacturing, compliance with safety standards, and energy-efficiency mandates. Market dynamics highlight that manufacturers and decision-makers must focus on innovation, scalability, and adaptability to rapidly evolving technology and healthcare delivery requirements.

The increasing incidence of cardiovascular, respiratory, and metabolic disorders is driving demand for continuous monitoring devices, advanced diagnostics, and therapeutic electronics. Hospitals and clinics are investing in remote patient monitoring and wearable devices that track vital signs and health metrics in real-time. This growing need compels manufacturers to develop reliable, long-lasting devices with enhanced accuracy and user-friendly interfaces. Early intervention facilitated by advanced medical electronics reduces treatment complexity and hospital readmissions. Continuous monitoring also supports preventive care strategies, enabling better management of chronic conditions, which in turn fuels ongoing innovation and expansion in the Medical Electronics Market.

Complex components, such as high-precision sensors, AI processors, imaging modules, and biocompatible materials, create cost challenges for manufacturers and healthcare providers. Rigorous validation and safety compliance testing add to development timelines. Miniaturized imaging modules and AI-driven devices require specialized cleanroom fabrication and highly skilled workforce. Budget constraints in smaller hospitals or emerging markets may limit adoption of premium equipment. Component scarcity, including semiconductors and rare materials, further increases production costs. These factors restrict rapid deployment and innovation across certain segments of the Medical Electronics Market, particularly in regions with limited infrastructure or financial resources.

Embedding AI and edge-computing capabilities in medical devices creates opportunities for real-time data analysis, improved patient care, and device autonomy. Wearable and point-of-care devices now process data locally, enabling immediate alerts for irregular health conditions. Edge intelligence reduces data transmission dependency, enhances privacy, and increases device efficiency. Expansion of home-based healthcare, outpatient monitoring, and telemedicine supports adoption of smart electronics. Manufacturers integrating low-power sensor fusion and AI-based predictive analytics are positioned to gain a competitive advantage while addressing emerging healthcare demands and operational challenges within the Medical Electronics Market.

Medical electronics development faces stringent regulations across multiple regions. Devices incorporating AI or software must comply with safety, efficacy, data security, and interoperability standards. Regulatory bodies require extensive documentation, clinical validation, and post-market surveillance. Meeting diverse regional requirements increases development time, costs, and risk of market delays. Cybersecurity compliance and environmental standards add further complexity. Small and medium manufacturers may face difficulties in obtaining necessary approvals while maintaining product innovation. The challenge of adhering to global regulatory frameworks affects device deployment, scaling, and investment strategies within the Medical Electronics Market.

Modular and Prefabricated Component Adoption: Manufacturers increasingly pre-assemble sensors, power modules, and interfaces off-site to reduce labor requirements and streamline deployment in hospitals and clinics. Precision fabrication allows rapid customization of devices across regions.

Edge-AI Integration in Diagnostics and Monitoring Devices: Microcontrollers with edge-AI capabilities enable local data processing for real-time health monitoring, minimizing latency, improving accuracy, and reducing energy consumption, particularly in wearables and portable diagnostic devices.

Expansion of Wearable and Continuous Monitoring Devices: Devices now track vital signs, cardiovascular metrics, glucose levels, and sleep patterns in real-time. Multi-sensor arrays, wireless connectivity, and extended battery life support outpatient care, home monitoring, and chronic disease management programs.

Cybersecurity, Privacy, and Regulatory Compliance Enhancement: Increased focus on device security includes encrypted communication, secure firmware updates, and risk assessment frameworks. Regulatory requirements mandate verification of cybersecurity protocols before approval, influencing product design and development strategies.

The Medical Electronics Market is structured around multiple layers of segmentation, including product type, application, and end-user categories, each reflecting unique industry needs and consumption patterns. By type, the market encompasses diagnostic devices, therapeutic electronics, patient-monitoring systems, wearable devices, and supporting electronic components such as sensors, controllers, and power modules. Applications span hospital-based care, home healthcare, outpatient and telemedicine solutions, and specialized clinical research environments. End-users include hospitals, diagnostic centers, ambulatory care facilities, home-care providers, and specialized institutions such as research laboratories and rehabilitation centers. Each segment presents specific operational requirements, technological integration needs, and investment priorities. Decision-makers rely on segmentation insights to align product development, service delivery, and strategic investments with the distinct demands of various applications and end-user groups, ensuring maximum operational efficiency and market responsiveness.

The leading product type in the Medical Electronics Market is diagnostic devices, including imaging systems, biosensors, and laboratory analyzers, due to their central role in clinical decision-making and patient assessment. Hospitals and diagnostic centers rely heavily on high-precision diagnostic tools for early detection of diseases, ensuring patient safety and treatment efficacy. The fastest-growing type is wearable devices, driven by rising demand for continuous health monitoring, remote patient management, and preventive care. Advances in miniaturized sensors, wireless connectivity, and energy-efficient electronics are enabling these devices to track vital signs such as heart rate, glucose levels, and oxygen saturation in real time. Therapeutic electronics, including implantable devices and surgical instruments, remain important for specialized interventions and critical care, while patient-monitoring systems such as portable monitors and smart hospital beds provide essential support in both acute and home-care settings. Supporting electronic components—sensors, microcontrollers, and power modules—play a vital niche role, enabling the functionality and reliability of all other device types.

In terms of applications, hospital-based solutions lead the Medical Electronics Market, reflecting the extensive use of diagnostic, therapeutic, and monitoring devices in inpatient care and surgical settings. Hospitals require highly integrated electronics for imaging, patient monitoring, and critical-care operations, making them the primary consumers of medical electronics. The fastest-growing application is home healthcare and remote monitoring, fueled by trends such as aging populations, rising chronic disease prevalence, and increasing adoption of wearable and connected devices. Telemedicine, mobile diagnostics, and outpatient care applications are also expanding, supported by technological innovations that allow real-time data capture and remote analysis. Specialized applications in research laboratories and clinical trials contribute niche yet critical demand, enabling innovation in new diagnostics and therapeutic solutions. Each application area dictates specific device performance, connectivity, and reliability requirements, which in turn guide manufacturers’ R&D and strategic deployment priorities.

Hospitals and large healthcare institutions represent the leading end-user segment in the Medical Electronics Market, reflecting their extensive infrastructure and high demand for sophisticated diagnostic, monitoring, and therapeutic electronics. They require fully integrated systems capable of managing large volumes of patients while ensuring accuracy, safety, and compliance with regulatory standards. The fastest-growing end-user segment is home-care and individual consumers, driven by the rising adoption of wearable devices, remote monitoring solutions, and patient-centric care models that allow real-time health tracking and early intervention. Other end-users contributing to market dynamics include ambulatory care centers, specialized diagnostic labs, and rehabilitation centers, which require specific medical electronics tailored to outpatient services, laboratory testing, and physical therapy monitoring. Each end-user category shapes product design, technological requirements, and service delivery models within the broader Medical Electronics Market.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.28% between 2025 and 2032.

North America continues to lead due to its advanced healthcare infrastructure, high adoption of medical electronics across hospitals and diagnostic centers, and strong technological integration, including AI, IoT, and wearable devices. The region benefits from substantial government investments in healthcare digitization and regulatory frameworks supporting medical device innovation. In contrast, Asia-Pacific is rapidly emerging with expanding healthcare facilities, increasing chronic disease prevalence, and rising investments in domestic manufacturing, which collectively drive higher market adoption. Europe, South America, and the Middle East & Africa also contribute significantly, with Europe showing strong adoption of precision diagnostics, South America focusing on infrastructure expansion, and Middle East & Africa leveraging modernization initiatives across healthcare and energy sectors. Overall, global demand patterns highlight regional diversification and technological transformation shaping the Medical Electronics Market over the next decade.

North America holds approximately 35% of the global Medical Electronics Market in 2024. Key industries driving demand include hospital networks, diagnostic laboratories, and outpatient care facilities, which rely on cutting-edge imaging systems, wearable devices, and patient-monitoring electronics. Regulatory changes such as updated FDA guidelines and government incentives for medical device research and deployment are accelerating adoption. Technological advancements like AI-enabled diagnostics, cloud-integrated patient monitoring, and smart wearable devices are transforming healthcare delivery. Digital transformation initiatives are also prominent, with hospitals and research centers investing heavily in interoperable systems, cybersecurity, and data analytics, ensuring seamless integration of medical electronics into clinical workflows and enhancing patient care efficiency.

Europe accounts for nearly 28% of the Medical Electronics Market, with Germany, the UK, and France being the most significant contributors. Hospitals and diagnostic centers in these countries prioritize high-precision imaging, advanced monitoring systems, and AI-integrated devices. Regulatory bodies, including the European Medicines Agency, enforce stringent compliance and safety standards, while sustainability initiatives promote energy-efficient medical electronics manufacturing. Emerging technologies such as AI-driven diagnostics, wearable monitoring devices, and IoT-enabled hospital systems are widely adopted. European markets also emphasize modular and compact electronics design, which facilitates rapid deployment in both hospital and home-care settings, positioning the region as a hub for innovation and precision medical devices.

Asia-Pacific ranks second in market volume and is witnessing rapid expansion in the Medical Electronics Market. China, India, and Japan are the top consuming countries, with China leading production capacity and India emerging as a major consumer of wearable and home-monitoring devices. The region is characterized by increasing healthcare infrastructure investment, modernization of hospitals, and growth of domestic manufacturing hubs. Technology trends include AI-assisted diagnostics, portable imaging systems, and wireless monitoring devices tailored for outpatient and home healthcare. Innovation centers in Japan and Singapore are developing high-precision sensors, energy-efficient electronics, and integrated telehealth solutions, enhancing the region’s competitive position in the global Medical Electronics Market.

South America represents approximately 10% of the global Medical Electronics Market, with Brazil and Argentina being key contributors. The region’s market growth is supported by hospital modernization, expansion of diagnostic centers, and investments in critical care equipment. Energy-efficient and modular electronics are increasingly adopted to optimize infrastructure capabilities. Government incentives and trade policies are facilitating import of high-tech medical electronics and supporting domestic manufacturing initiatives. Emerging trends include telemedicine solutions, portable monitoring systems, and wearable devices adapted to local healthcare needs, enabling South America to strengthen its presence in the global Medical Electronics Market.

The Middle East & Africa accounts for roughly 7% of the Medical Electronics Market, with UAE and South Africa leading demand. Regional growth is fueled by investments in oil & gas sector healthcare facilities, hospital modernization projects, and adoption of high-tech medical electronics for diagnostics and monitoring. Technological modernization trends include AI-enabled imaging systems, smart hospital solutions, and wireless monitoring devices. Local regulations and trade partnerships support import and deployment of advanced electronics while ensuring compliance with safety and performance standards. Countries are focusing on integrating medical electronics with digital health infrastructure to improve patient care and expand healthcare access across urban and remote areas.

United States – 35% Market Share

Dominates due to advanced healthcare infrastructure, high production capacity, and strong end-user adoption of sophisticated medical electronics.

China – 22% Market Share

Leads because of expansive manufacturing capabilities, growing domestic demand, and government-driven technological initiatives in diagnostics and monitoring devices.

The Medical Electronics Market is highly competitive, with over 150 active global players operating across diagnostics, therapeutic, monitoring, and wearable device segments. Leading firms are strategically investing in research and development to introduce AI-enabled, IoT-integrated, and edge-computing capable devices. Key initiatives include strategic partnerships for technology co-development, targeted acquisitions to expand product portfolios, and frequent product launches emphasizing miniaturization, wireless connectivity, and energy efficiency. Innovation trends shaping competition include integration of AI for predictive diagnostics, development of multi-sensor wearables for continuous monitoring, and modular designs enabling rapid deployment in hospitals and home-care settings. Market positioning is increasingly influenced by the ability to offer end-to-end solutions that combine hardware, software, and digital services. Firms are also focusing on regulatory compliance, cybersecurity measures, and sustainability in design to meet stringent global standards. Decision-makers are observing that companies with strong innovation pipelines, robust manufacturing capabilities, and effective distribution networks are securing leadership positions and shaping competitive dynamics in the Medical Electronics Market.

Medtronic

Philips Healthcare

Siemens Healthineers

GE Healthcare

Abbott Laboratories

Becton Dickinson

Boston Scientific

Johnson & Johnson

Terumo Corporation

Canon Medical Systems

Samsung Medison

Hitachi Medical Corporation

The Medical Electronics Market is experiencing rapid technological evolution driven by integration of AI, IoT, and edge computing into devices. Diagnostic electronics increasingly leverage high-resolution imaging systems, AI-based image analysis, and cloud-enabled interoperability. Wearable devices are now equipped with multi-sensor arrays, low-power processors, and wireless data transmission modules, enabling continuous patient monitoring for vital signs, glucose levels, cardiovascular metrics, and sleep patterns. Therapeutic devices, including implantable and surgical electronics, are adopting precision control mechanisms, miniaturized actuators, and real-time feedback loops for improved patient outcomes. Emerging technologies include smart biosensors, AI-powered predictive analytics, and augmented reality-assisted surgical platforms, which enhance clinical decision-making and procedural efficiency. Digital integration with electronic health records, telemedicine platforms, and mobile health apps is accelerating, allowing remote monitoring and early interventions. Additionally, manufacturers are focusing on energy-efficient designs, reusable or modular components, and robust cybersecurity protocols, ensuring device reliability, safety, and compliance across global healthcare infrastructure. These technological advancements are shaping the future of the Medical Electronics Market by enabling smarter, safer, and more connected healthcare solutions.

In March 2023, GE Healthcare launched the Revolution Apex CT system, featuring ultra-low dose imaging and enhanced AI-assisted image reconstruction, improving diagnostic speed and patient safety.

In July 2023, Medtronic introduced its new AI-integrated insulin pump, capable of real-time glucose monitoring and automated dosage adjustments, reducing hypoglycemic events by 25% in clinical trials.

In November 2023, Philips Healthcare rolled out the IntelliVue Guardian Solution for hospitals, enabling continuous multi-parameter monitoring and automated early warning alerts for at-risk patients.

In June 2024, Abbott launched the FreeStyle Libre 3 wearable glucose monitoring system, providing continuous real-time readings with enhanced sensor accuracy and extended battery life for outpatient care.

The Medical Electronics Market Report provides a comprehensive assessment of global and regional dynamics across device types, applications, and end-user segments. It covers diagnostic electronics, therapeutic devices, patient-monitoring systems, wearable electronics, and component technologies such as sensors, controllers, and microprocessors. The report evaluates hospital-based, home-care, outpatient, and research applications, highlighting adoption patterns, infrastructure requirements, and technology integration levels. Geographically, it examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, focusing on production capacity, consumption trends, and innovation hubs. The study also addresses regulatory and environmental considerations, including compliance frameworks, cybersecurity standards, and sustainability initiatives impacting device development and deployment. Emerging segments, such as AI-enabled wearables, edge-computing diagnostics, and telemedicine-integrated systems, are analyzed for market potential and technological relevance. The report equips decision-makers with actionable insights on strategic initiatives, competitive positioning, product innovation, and future market opportunities, offering a detailed understanding of the breadth, depth, and evolving landscape of the Medical Electronics Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,050.1 Million |

| Market Revenue (2032) | USD 2,297.2 Million |

| CAGR (2025–2032) | 10.28% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Medtronic, Philips Healthcare, Siemens Healthineers, GE Healthcare, Abbott Laboratories, Becton Dickinson, Boston Scientific, Johnson & Johnson, Terumo Corporation, Canon Medical Systems, Samsung Medison, Hitachi Medical Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |