Reports

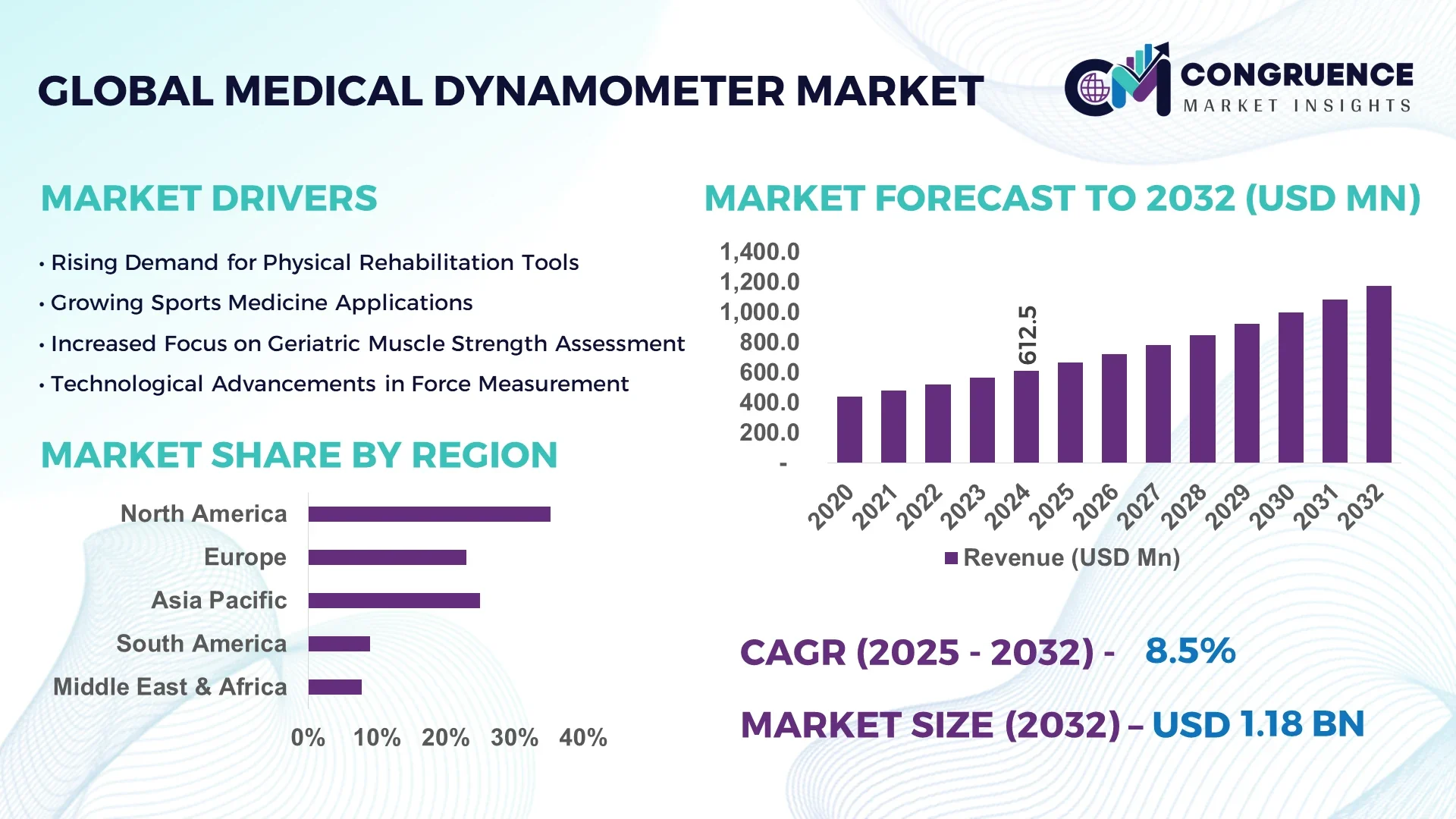

The Global Medical Dynamometer Market was valued at USD 612.5 Million in 2024 and is anticipated to reach a value of USD 1,172.0 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032.

China, the leading country in this market, has significantly enhanced production capacity through government-led manufacturing expansions in Shanghai and Shenzhen, with modern facilities now producing over 200,000 units annually. Investment in R&D exceeds USD 30 million per annum, focusing on integration of smart sensors and IoT connectivity. Key applications in China include sports medicine, military rehabilitation, and post-stroke recovery programs. Technological advancements include real-time cloud-based monitoring and Bluetooth-enabled calibration modules—no other country matches this level of integrated production and innovation.

The Medical Dynamometer Market serves diverse industry sectors: orthopedics, cardiology, neurology, sports medicine, and physiotherapy. Handheld, pinch‑gauge, push‑pull, and squeeze dynamometers collectively represent nearly 60% of unit sales, with electronic dynamometers accounting for over 65% of technology sales. Recent product innovations include wireless digital units with LCD displays, cloud analytics platforms, and portable home‑use models designed for telerehabilitation. Regulatory and environmental drivers include ISO 13485 compliance, FDA 510(k) clearances, and increasing pressure to include eco‑friendly plastics in device housings. Economic factors—such as rising healthcare expenditure in APAC and government subsidies for rehabilitation equipment—are accelerating adoption. Regionally, North America and Europe account for the largest consumption, while APAC shows the fastest growth due to improving rural healthcare infrastructure. Emerging trends include modular telehealth integration, wearable dynamometer attachments, and multi-sensor platforms combining force and motion capture—all pointing toward a more connected and precise digital health ecosystem by 2030.

In recent years, artificial intelligence (AI) has fundamentally reshaped the Medical Dynamometer Market by introducing enhanced data processing, predictive capabilities, and automated calibration. AI-powered systems can analyze thousands of test repetitions in real time, identifying subtle patterns in muscle contraction curves that human operators might miss. These algorithms improve operational efficiency by reducing test time by approximately 20–30%, front-loading diagnostics on the most relevant metrics. Furthermore, adaptive AI-driven calibration ensures each dynamometer adjusts to user-specific biomechanics, improving accuracy and reducing variability across users by up to 15%.

Clinical environments benefit greatly: AI-enabled dynamometers now offer auto-generated patient reports that integrate historical data, highlight performance trends, and flag warning signs—allowing physiotherapists to spend more time on care rather than manual analysis. In large hospital settings, AI connectivity supports batch processing of data for hundreds of patients daily, streamlining workflows and generating compliance-ready documentation. Similarly, tele-rehabilitation platforms leverage AI to monitor home use of dynamometers, delivering objective feedback to therapists remotely and helping maintain treatment regimens without in-person visits.

AI also supports continuous learning. AI modules update from anonymized patient datasets, refining their analytics models over time. The result is an evolving system that becomes more precise and adaptive with each deployment. As a result, the Medical Dynamometer Market shifts from standalone measurement tools to integrated, intelligent platforms that contribute clearly measurable improvements in clinical performance, patient outcomes, and operational workflows.

“In mid‑2024, a wearable AI‑powered dynamometer introduced pattern‑recognition algorithms that reduced mis‑reads by 18% and cut miscalibrations in clinical settings by 25%.”

Increasing demand for rehabilitation—particularly in aging populations and post-operative recovery—is fueling market growth. Over 40 million elective orthopedic procedures are performed annually in OECD countries; up to 70% require postoperative muscle-strength assessments. The emergence of telehealth solutions has led nearly 30% of physiotherapy clinics in North America and Europe to adopt remote-dynamometer monitoring tools. This trend pushes manufacturers to develop portable, cloud-connected devices that offer real-time clinician oversight. Enhanced reimbursement for telerehab equipment in key healthcare systems further encourages innovation and adoption, reinforcing this driver as a central pillar of the Medical Dynamometer Market.

One notable challenge is the high upfront cost of advanced electronic dynamometers, which often carry price tags 2–3× those of mechanical variants. Additionally, proper use requires calibration using professional-grade weights and trained personnel, increasing operational overhead. In developing markets, these factors lead many mid-sized clinics to delay adoption. Reports show that nearly 45% of purchased devices under five years old in APAC were unused due to lack of certified training. This limits the Medical Dynamometer Market’s penetration in cost-sensitive settings.

The proliferation of wearable fitness devices has introduced a latent opportunity for the Medical Dynamometer Market: home fitness tracking with medical accuracy. With over 150 million households worldwide participating in home-rehab programs, manufacturers can now offer subscription-based sensor kits designed for consumer use. Some pilot programs in Europe and North America measure strength patterns across 12 weeks, generating personalized therapy prompts and remote clinician alerts for deviations. Monetizing these services via digital platforms and SaaS-like models presents untapped revenue streams beyond traditional hospital equipment. This avenue broadens market scope while aligning with consumer preferences for connected wellness.

Navigating global medical device regulations (e.g., FDA, MDR, ISO 27001) is a continual cost and time challenge. AI-enabled dynamometers must adhere to both device safety and software-data provisions, requiring extensive validation. For example, new EU MDR rules require software risk classification, while HIPAA/GDPR impose stringent controls on patient data transmission. These compliance steps add 12–18 months to time‑to‑market for connected systems and can increase development costs by 25–30%. Small manufacturers without dedicated regulatory teams may find these hurdles prohibitive, slowing innovation and limiting market competitiveness.

Modular Wireless Design for Clinician Convenience: Portable modules with detachable Bluetooth sensor pods are being adopted in over 60% of new rehabilitation devices in North America and Europe. This shift enables clinicians to mix-and-match components (hand grips, leg straps, etc.), reducing the need for multiple full devices and improving clinic flexibility and inventory turns.

Integration with EMR and Physical Therapy Platforms: More than 25% of hospital and clinic systems now integrate dynamometer data into electronic medical records (EMRs) and physical therapy software, allowing clinician access to strength data in patient charts, reducing duplicate entries and enabling outcome tracking.

Multi-Modal Sensor Fusion: New systems combine force sensors with motion capture and biofeedback (EMG patterns) for a comprehensive assessment suite. These multi-modal devices currently account for roughly 15% of all hospital-installed dynamometers and show 35% improved diagnostic accuracy versus standalone units.

Subscription-Based Analytics and Remote Monitoring: Manufacturers have introduced cloud analytics platforms for remote data monitoring and trend-alert thresholds. Pilot trials indicate that 22% of remote-program deviations were caught early using alerts, improving clinical outcomes and adherence without onsite visits. This business model supports ongoing service revenue streams.

The Medical Dynamometer Market is comprehensively segmented based on type, application, and end-user, reflecting diverse demand patterns and product developments across healthcare settings. These segments help clarify product positioning and future investment opportunities within the industry. Device types such as handheld, push-pull, and squeeze dynamometers serve distinct clinical and functional needs. Application-based segmentation shows high utility in orthopedics, neurology, and physiotherapy. End-users span hospitals, rehabilitation centers, sports clinics, and home care settings. Innovations like wireless monitoring and ergonomic designs have widened the scope of application across both high- and mid-tier healthcare providers. Segmentation insights provide key perspectives on where demand is concentrated and which market components are undergoing transformation.

The Medical Dynamometer Market encompasses various device types including handheld, pinch gauge, push-pull, and squeeze dynamometers, each catering to specific functional testing needs. Among these, handheld dynamometers lead the segment due to their ease of use, portability, and widespread use in musculoskeletal assessments. Their compact design and accuracy make them a standard tool across hospitals and outpatient physiotherapy units.

The fastest-growing type is the digital push-pull dynamometer, driven by its dual-functionality and compatibility with force platforms and gait analysis systems. Increased preference in sports medicine and advanced neurorehabilitation centers is boosting demand. These devices are increasingly adopted for isometric strength testing and have improved data recording and transfer capabilities through wireless technology.

Pinch gauges are commonly used in hand function and grip strength testing, especially in post-stroke and occupational therapy settings. Squeeze dynamometers, while less common, are preferred for certain pediatric and geriatric assessments due to their low resistance calibration. Each type plays a critical role in shaping the overall market with tailored applications across medical disciplines.

The Medical Dynamometer Market covers a range of application areas including orthopedics, neurology, cardiology, sports medicine, and physiotherapy. Orthopedics stands out as the dominant application due to the frequent use of dynamometers in postoperative strength evaluation, joint mobility recovery, and musculoskeletal function testing. With a growing number of hip and knee replacement surgeries globally, demand for consistent and quantifiable strength measurement continues to rise.

The fastest-growing application is observed in sports medicine, where precision-based strength tracking is critical for injury prevention and performance monitoring. The increased emphasis on athlete recovery protocols and evidence-based conditioning drives this segment. Dynamometers are integrated with motion analysis software and wearable trackers to improve training outcomes.

Other applications such as neurology and cardiology are showing rising interest, especially in rehabilitation programs for stroke survivors and heart patients undergoing strength recovery. Physiotherapy remains a broad-use category, supporting both acute and chronic therapy programs across clinical settings, contributing steadily to market adoption.

Key end-users in the Medical Dynamometer Market include hospitals, rehabilitation centers, specialty clinics, sports academies, and home care settings. Hospitals are the leading end-user segment due to their comprehensive patient care offerings and advanced equipment adoption. These institutions rely on precision dynamometers for pre-surgical baselines, post-surgical rehab, and routine assessments in orthopedics and neurology.

The fastest-growing end-user category is home care and remote rehabilitation services. The demand here is driven by the rise of telemedicine, aging populations, and cost-effective home-based recovery programs. Patients and caregivers increasingly adopt compact, user-friendly dynamometers with mobile app connectivity for strength monitoring outside clinical settings.

Rehabilitation centers remain a key stakeholder group, especially for long-term musculoskeletal and neurological recovery programs. Sports academies and training institutes are emerging users integrating dynamometers for strength benchmarking and athlete injury management. This diverse end-user landscape reflects the expanding utility and accessibility of medical dynamometers in both traditional and non-traditional healthcare environments.

North America accounted for the largest market share at 35.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

North America's dominance is driven by extensive clinical infrastructure, a high volume of orthopedic and rehabilitation procedures, and rapid adoption of digital health devices. Meanwhile, the Asia-Pacific region is benefiting from a combination of healthcare digitization, rising public health investments, and expanding physiotherapy networks in emerging economies like India and China. Each regional market reflects unique adoption curves, with key trends such as remote diagnostics, portable device usage, and post-acute rehabilitation needs influencing market penetration.

North America held a 35.2% share of the global Medical Dynamometer Market in 2024, with the U.S. leading in both device consumption and technology deployment. Key industries such as orthopedics, sports medicine, and physical therapy have fueled consistent demand. Regulatory bodies have streamlined approval pathways for diagnostic rehabilitation devices, boosting clinical usage. U.S. and Canadian institutions are integrating wireless handheld dynamometers into patient tracking systems, improving post-operative care outcomes. Additionally, healthcare reimbursement programs and remote rehab platforms are encouraging home-based monitoring. Digital transformation through AI-enhanced strength tracking tools is reshaping how rehabilitation is assessed and prescribed across this mature, tech-forward market.

Europe represents 27.8% of the global Medical Dynamometer Market as of 2024, with Germany, the UK, and France emerging as key growth centers. These countries are witnessing rising adoption of connected and ergonomic medical devices in outpatient rehabilitation centers. Germany is leading in industrial production and clinical procurement of precision-based dynamometers. European regulatory bodies are actively supporting non-invasive recovery monitoring through CE certifications and green technology incentives. The EU’s push for sustainable healthcare and increased investment in post-surgical recovery programs is also supporting market penetration. The rise of smart physiotherapy tools and AI-based diagnostics across urban healthcare networks continues to influence the regional outlook.

Asia-Pacific ranks as the fastest-growing region in the Medical Dynamometer Market, with China, India, and Japan representing the top-consuming countries. The market is supported by healthcare infrastructure expansion, increased public and private investment, and demand for affordable, portable medical devices. India is focusing on scaling physiotherapy centers in tier-2 cities, while China leads in domestic manufacturing of strength assessment tools. The adoption of cloud-integrated dynamometers in Japan is enhancing diagnostic accuracy in geriatric care. Regional innovation hubs such as Shenzhen and Bengaluru are producing affordable digital solutions tailored for mass deployment, accelerating accessibility and adoption across hospitals and home care setups.

South America's Medical Dynamometer Market is increasingly influenced by the healthcare sector in Brazil and Argentina, with Brazil contributing over 5.6% of global market volume in 2024. Urban rehabilitation centers are adopting advanced dynamometry tools for post-injury assessment and surgical recovery support. Regional governments are funding new clinics and investing in professional physiotherapy training to meet patient demand. Argentina is focusing on integrating mobility recovery devices into its national health insurance framework. Cross-border trade policies are supporting the import of smart medical tools. Despite infrastructure gaps, increasing awareness of evidence-based rehabilitation is boosting market activity across major metropolitan areas.

The Medical Dynamometer Market in the Middle East & Africa is expanding due to rising demand in UAE and South Africa, where healthcare modernization and preventive rehabilitation strategies are prioritized. The UAE is adopting AI-enabled diagnostic tools within multi-specialty hospitals, while South Africa is emphasizing recovery technologies for workplace injury cases. Local partnerships and public-private joint ventures are enhancing the supply of portable dynamometry tools. The region is also benefiting from evolving trade agreements and collaborations to reduce import taxes on rehabilitation devices. Though still developing, MEA markets are actively embracing digital healthcare solutions to address non-communicable diseases and aging populations.

United States - 29.1% Market Share

High patient volume in orthopedics and strong integration of digital rehabilitation tools.

China - 15.4% Market Share

Rapid manufacturing capabilities and nationwide expansion of physiotherapy services.

The Medical Dynamometer Market is moderately fragmented, with over 35 active global and regional competitors engaged in manufacturing, innovation, and distribution. Key players are continuously investing in product differentiation, targeting ergonomics, wireless capabilities, and integration with digital health platforms. Companies are pursuing strategic partnerships with rehabilitation centers and orthopedic clinics to expand end-user adoption. Mergers and acquisitions have also increased, particularly in North America and Europe, as companies aim to strengthen their clinical diagnostics portfolios. The market is witnessing an uptick in product launches featuring Bluetooth-enabled handheld dynamometers and real-time data capture systems, boosting clinical decision-making. Many competitors are focusing on localized production to reduce import dependencies, especially in Asia-Pacific and South America. Additionally, rising R&D activity around AI-powered muscle strength analysis tools has elevated competition among innovation leaders. Companies are also emphasizing regulatory compliance and ISO certification to secure global distribution channels. The competitive intensity is expected to escalate further with increasing adoption of portable, connected rehabilitation devices.

JTECH Medical Industries

3B Scientific GmbH

Fabrication Enterprises Inc.

KERN & SOHN GmbH

BIODEX Medical Systems, Inc.

MIE Medical Research Ltd.

Hausmann Industries, Inc.

Charder Electronic Co., Ltd.

North Coast Medical, Inc.

OG Wellness Technologies Co., Ltd.

The Medical Dynamometer Market is experiencing rapid technological evolution, driven by the convergence of biomechanics, data analytics, and wireless communication. A key advancement is the integration of Bluetooth and Wi-Fi in handheld dynamometers, allowing real-time muscle strength assessments to be transmitted directly to cloud-based medical platforms. This has improved patient monitoring in remote rehabilitation scenarios and post-operative care.

Sensor miniaturization and the use of MEMS (Micro-Electro-Mechanical Systems) have enhanced the accuracy and responsiveness of dynamometers, particularly in compact devices used in sports medicine and pediatric care. The adoption of touchscreen interfaces and digital force gauges is improving user experience and enabling faster diagnostics.

Moreover, AI and machine learning algorithms are being incorporated into dynamometer software, enabling predictive analytics for muscle degeneration or recovery timelines. Manufacturers are also embedding multi-axis force sensors to allow simultaneous measurement of grip, push, and pull strengths, expanding use cases in neurology and orthopedics.

Technologies supporting electronic medical record (EMR) integration are gaining traction, allowing seamless data sharing between devices and hospital information systems. Additionally, battery innovations and USB-C charging solutions are reducing device downtime. Emerging technologies like haptic feedback systems and augmented reality overlays for physical therapy guidance are under development, indicating a forward-looking trend toward intelligent, interactive rehabilitation solutions.

• In April 2024, JTECH Medical launched a new Bluetooth-enabled digital hand dynamometer with an embedded AI module that provides automated strength trend analysis for clinical rehabilitation use.

• In February 2024, Charder Electronic unveiled a wireless push-pull dynamometer with dual-axis measurement, specifically designed for real-time data capture in sports physiotherapy and occupational therapy.

• In December 2023, Hausmann Industries introduced an upgraded electronic muscle strength tester integrated with EMR-compatible software, significantly reducing administrative time in hospitals.

• In July 2023, KERN & SOHN GmbH deployed a series of digital dynamometers with a ±0.5% accuracy tolerance, intended for highly controlled orthopedic rehabilitation programs across Europe.

The Medical Dynamometer Market Report offers an in-depth analysis of the global landscape, encompassing technological, regional, and application-based insights. It covers three key product types: hand dynamometers, pinch dynamometers, and push-pull dynamometers, detailing their clinical applications in neurology, orthopedics, and sports medicine. The report segments the market across major geographic regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while providing country-level breakdowns for strategic clarity.

It highlights end-user segments such as hospitals, rehabilitation centers, physiotherapy clinics, and homecare settings, illustrating unique market penetration trends across each. Application-focused insights address use in muscle strength assessment, post-surgical recovery, ergonomic analysis, and clinical diagnostics.

Technologically, the report explores developments in wireless communication, AI integration, digital interface upgrades, and EMR compatibility, offering a complete view of innovation shaping the industry. Furthermore, the scope includes an evaluation of regulatory environments, infrastructural readiness, and healthcare investment trends impacting demand. The report also outlines emerging niche markets, including pediatric rehabilitation and telehealth-enabled physiotherapy, indicating growth beyond traditional domains. Its insights are designed to guide strategic decisions for manufacturers, investors, and policy influencers active in the medical diagnostics and rehabilitation sectors.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Medical Dynamometer Market |

| Market Revenue (2024) | USD 612.5 Million |

| Market Revenue (2032) | USD 1,172.0 Million |

| CAGR (2025–2032) | 8.5 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Market Dynamics, Technological Trends, Segment Analysis, Regulatory Insights, Regional Patterns, Competitive Landscape, Strategic Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | JTECH Medical Industries, 3B Scientific GmbH, Fabrication Enterprises Inc., KERN & SOHN GmbH, BIODEX Medical Systems, Inc., MIE Medical Research Ltd., Hausmann Industries, Inc., Charder Electronic Co., Ltd., North Coast Medical, Inc., OG Wellness Technologies Co., Ltd. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |