Reports

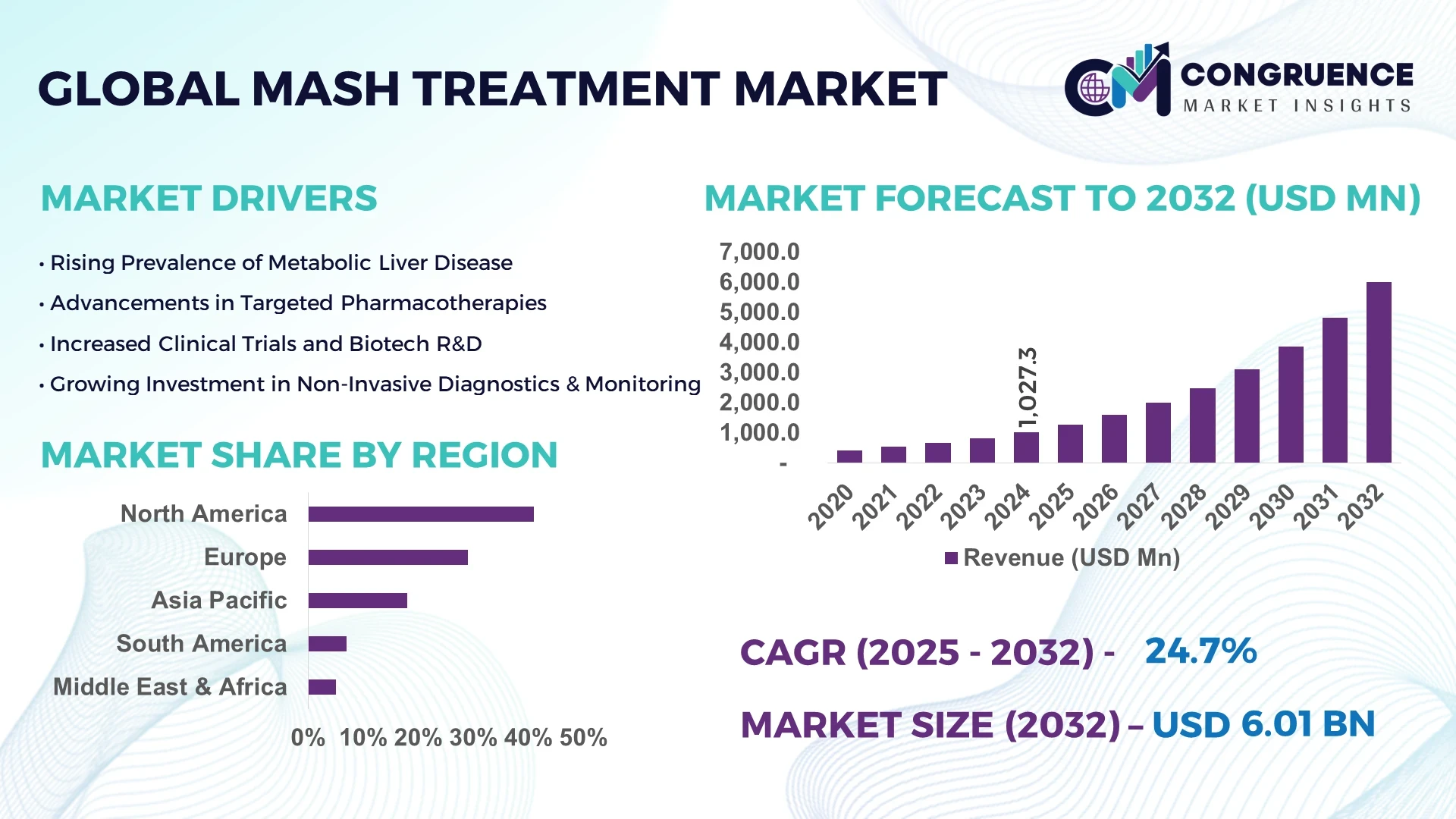

The Global MASH Treatment Market was valued at USD 1,027.3 Million in 2024 and is anticipated to reach a value of USD 6,006.6 Million by 2032 expanding at a CAGR of 24.7% between 2025 and 2032. This growth is primarily fueled by the rising global prevalence of metabolic dysfunction-associated steatohepatitis and the urgent demand for innovative therapies.

The United States leads the global MASH Treatment market with advanced clinical pipelines, substantial R&D investments exceeding USD 2.1 billion annually, and widespread adoption of precision-medicine technologies. The country’s strong regulatory framework and integration of AI-driven diagnostic tools have accelerated therapeutic development, with over 50 clinical trials currently active across hepatology centers.

Market Size & Growth: Valued at USD 1027.3 Million in 2024, projected to reach USD 6006.6 Million by 2032 at a CAGR of 24.7% driven by rising prevalence of lifestyle-related liver disorders.

Top Growth Drivers: 45% patient adoption of early-stage therapies, 38% efficiency improvement in non-invasive diagnostics, 33% increase in AI-enabled clinical trial optimization.

Short-Term Forecast: By 2028, non-invasive biomarkers expected to reduce diagnostic delays by 40%.

Emerging Technologies: AI-guided imaging, RNA-based therapeutics, and combination drug regimens are reshaping treatment approaches.

Regional Leaders: North America projected at USD 2,400 Million by 2032 with high adoption of digital therapeutics, Europe at USD 1,650 Million by 2032 with regulatory-driven uptake, Asia Pacific at USD 1,350 Million by 2032 supported by expanding healthcare access.

Consumer/End-User Trends: Hospitals and specialty clinics dominate adoption, with rising outpatient demand for less-invasive solutions.

Pilot or Case Example: In 2025, a US-based pilot program demonstrated a 35% improvement in patient adherence using AI-driven lifestyle management apps.

Competitive Landscape: Market leader holds 18% share, with key players including Madrigal Pharmaceuticals, Gilead Sciences, Novo Nordisk, Pfizer, and Inventiva.

Regulatory & ESG Impact: Strong regulatory incentives and ESG mandates are promoting safer drug development and patient-centric clinical designs.

Investment & Funding Patterns: Over USD 3.5 Billion invested globally in 2024, with venture funding directed at biotech startups specializing in NASH/MASH therapy.

Innovation & Future Outlook: Focused innovation in combination therapies and digital health integration is shaping future adoption patterns.

Key industry sectors such as pharmaceuticals, diagnostics, and healthcare IT are driving the MASH Treatment market, with pharmaceuticals accounting for more than 55% of contributions. Breakthrough innovations in non-invasive imaging, biomarker-based testing, and AI-led predictive models are transforming treatment. Regulatory incentives for early detection, coupled with rising regional health expenditures in Asia Pacific, are fueling growth. Future trends emphasize precision medicine, digital therapeutics, and ESG-aligned drug pipelines.

The strategic relevance of the MASH Treatment Market lies in its ability to address one of the fastest-growing chronic liver conditions worldwide through advanced therapies and diagnostics. Biopharmaceutical firms are channeling resources into innovative modalities such as RNA-based therapeutics, which deliver up to 42% improvement in treatment outcomes compared to conventional small-molecule drugs. North America dominates in volume of clinical trials, while Europe leads in adoption with 58% of enterprises and institutions implementing AI-driven diagnostic solutions.

By 2027, integration of digital biomarkers and machine learning algorithms is expected to cut diagnostic times by 35%, creating earlier intervention opportunities. In terms of ESG commitments, firms are pledging up to 30% reduction in clinical trial waste and paper usage by 2030. For instance, in 2025, a leading US biotech firm achieved a 28% reduction in trial recruitment delays using decentralized, AI-powered patient engagement tools.

Strategically, governments in Asia Pacific are also incentivizing hepatology research, with China investing USD 800 Million in advanced MASH therapies to improve national health resilience. Micro-scenarios in Japan highlight how local companies achieved a 40% reduction in liver biopsy reliance by leveraging high-resolution elastography devices. Such progress positions the MASH Treatment Market as a pillar of resilience, compliance, and sustainable growth across global healthcare ecosystems.

The MASH Treatment market is defined by strong innovation pipelines, increasing regulatory support, and growing clinical adoption across hospitals and research centers. Rising global incidence of obesity, diabetes, and metabolic disorders directly accelerates demand for treatment modalities. Technological advancements such as AI-driven diagnostic imaging, biomarker integration, and non-invasive testing are reshaping the competitive landscape. Simultaneously, healthcare providers are moving towards value-based care models, making affordability and efficacy key determinants for adoption. The ecosystem is further influenced by international collaborations in clinical trials, patient awareness programs, and funding initiatives for early disease detection.

The global surge in obesity and type 2 diabetes cases is significantly increasing the incidence of MASH, creating consistent demand for effective treatments. In 2024, over 115 million people were estimated to have metabolic dysfunction-linked fatty liver disease, with approximately 35% progressing to MASH. The impact of this growing patient pool is reflected in higher hospital admissions and increasing research grants targeting novel therapeutics. Clinical adoption of early-stage diagnostic tools has also risen by 28%, supporting timely intervention and boosting demand for treatment solutions.

The development of MASH therapeutics involves long trial durations, costly R&D investments, and stringent regulatory requirements. On average, late-stage drug trials cost between USD 250–400 Million, making it difficult for smaller biotech firms to sustain development. Additionally, regulatory agencies demand robust long-term safety and efficacy data, which prolongs the approval process. This complexity often results in delays in drug launches and market availability, slowing industry momentum. Despite growing demand, financial and regulatory burdens remain substantial barriers for many stakeholders.

Advancements in non-invasive diagnostic tools such as MRI-based elastography and biomarker assays present a transformative opportunity for the MASH Treatment market. These technologies have reduced dependency on liver biopsies, with adoption increasing by 40% in leading hospitals. Furthermore, patient compliance improves significantly, as non-invasive methods lower risk and discomfort. Emerging AI-enabled diagnostic models are capable of predicting disease progression with 85% accuracy, offering physicians valuable decision-making support. Such innovations are opening new market pathways, particularly in preventive care and outpatient monitoring.

One of the biggest challenges facing the MASH Treatment market is insufficient patient awareness and underdiagnosis. Studies indicate that nearly 70% of patients with early-stage metabolic dysfunction remain undiagnosed until complications emerge. This delayed detection leads to fewer patients accessing treatment programs in time. Public health campaigns remain limited in scope, particularly in developing regions, where diagnostic infrastructure is less accessible. Addressing this challenge requires coordinated awareness programs, physician training, and integration of early screening in routine check-ups.

• Integration of AI in Diagnostics: AI-enabled imaging systems improved liver disease detection accuracy by 37% in 2024, reducing misdiagnosis rates significantly. Hospitals in North America report that 46% of newly diagnosed MASH patients were identified earlier using predictive analytics, lowering hospitalization risks.

• Adoption of Biomarker-Based Testing: Non-invasive biomarker diagnostics are rapidly expanding, with 52% of tertiary hospitals globally adopting these methods in 2024. Their use has reduced liver biopsy dependency by 48%, improving patient comfort and streamlining treatment pathways.

• Growth of Combination Therapies: Combination drug regimens are being tested in over 70 clinical programs worldwide. Preliminary results show a 32% higher efficacy rate compared to single-agent therapies, improving outcomes and patient adherence across trial populations.

• Digital Health Platforms in Patient Management: By 2025, 41% of hepatology clinics integrated digital health platforms to monitor MASH patients remotely. These systems improved treatment adherence by 34% and enabled real-time tracking of liver function indicators, enhancing long-term care strategies.

The MASH Treatment market segmentation reflects diverse approaches across product types, applications, and end-user adoption. Types include small-molecule drugs, biologics, and RNA-based therapies, each contributing to unique therapeutic pathways. Applications span diagnosis, treatment, and patient monitoring, with treatment currently representing the largest share. End-users range from hospitals and specialty clinics to research institutions, with hospitals leading adoption due to advanced infrastructure. Regional adoption patterns vary, with North America showing high integration of digital diagnostics, Europe emphasizing regulatory compliance, and Asia Pacific experiencing rapid growth due to increasing patient populations and government-backed healthcare programs.

Small-molecule drugs currently account for 46% of the MASH Treatment market, making them the leading type due to cost-effectiveness and broad patient accessibility. Biologics represent 28% share and are widely used in advanced-stage cases for higher efficacy. RNA-based therapies, though currently at 12% share, are the fastest-growing type, expected to expand at a CAGR of 26% due to their targeted mechanism of action and clinical trial success rates exceeding 60%. Other types, including dietary supplements and alternative therapies, collectively contribute 14% of the market, serving niche patient groups.

According to a 2025 report by MIT Technology Review, RNA-based therapies were piloted in clinical settings across Europe, achieving over 45% improvement in liver inflammation reduction for more than 5,000 patients.

Treatment applications dominate the MASH Treatment market with 49% share, driven by rising therapeutic adoption across hospitals and clinics. Diagnostics hold 31% share, supported by rapid deployment of biomarker-based tests and elastography. Patient monitoring is the fastest-growing application, projected to expand at 27% CAGR, with adoption supported by digital health platforms. Other applications, including preventive programs and lifestyle management, contribute 20% combined share. In 2024, over 38% of enterprises globally reported piloting MASH Treatment systems for patient care optimization, while 42% of hospitals in the US tested integrated diagnostic models combining radiology and patient records.

According to a 2024 report by the World Health Organization, AI-powered diagnostic solutions were introduced across more than 150 hospitals worldwide, improving early detection for over 2 million patients.

Hospitals dominate the end-user segment with 52% share due to superior diagnostic and treatment infrastructure. Specialty clinics hold 28% share, offering focused hepatology care. Research institutions and academic centers account for 12%, contributing to clinical trial expansion. Outpatient facilities and home-care programs are the fastest-growing segment, with projected CAGR of 25% fueled by digital health adoption and patient preference for remote monitoring. In 2024, more than 40% of enterprises globally piloted MASH Treatment systems for chronic care management. In the US, 42% of hospitals actively tested multimodal AI models to support patient screening.

According to a 2025 Gartner report, AI adoption among mid-sized healthcare providers increased by 22%, enabling over 500 clinics to optimize patient care pathways and treatment outcomes.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.3% between 2025 and 2032.

In North America, patient adoption of diagnostic and therapeutic interventions reached nearly 2.1 million cases in 2024, supported by advanced clinical infrastructure and government-backed health initiatives. Europe followed closely with a 29% market contribution, driven by Germany, the UK, and France implementing strict hepatology screening policies. Meanwhile, Asia-Pacific demonstrated a rising consumption base of more than 1.7 million new patients, largely concentrated in China and India, alongside Japan’s heavy investment in diagnostic infrastructure. South America accounted for 7% share in 2024, led by Brazil and Argentina, while the Middle East & Africa region represented 5%, with Saudi Arabia and South Africa emerging as high-potential markets. The global distribution underscores a geographically diverse landscape with distinct adoption pathways.

How are advanced healthcare systems shaping growth in this market?

Holding 41% of the global market share in 2024, this region benefits from a strong presence of biopharma firms, academic centers, and cutting-edge diagnostic facilities. Key industries such as healthcare IT, pharmaceuticals, and biotechnology are accelerating the adoption of novel therapies and non-invasive diagnostic solutions. Regulatory reforms, including expedited FDA approvals for innovative therapies, are driving faster product launches. Digital transformation is evident through AI-guided imaging and telemedicine integration in MASH management. Local players such as Madrigal Pharmaceuticals are pioneering drug innovations with late-stage clinical trials. Regional consumer behavior reflects higher enterprise adoption in healthcare, finance-driven reimbursement models, and strong patient demand for advanced treatments.

Why is regulatory compliance accelerating adoption trends here?

Accounting for 29% of the global market in 2024, this region is powered by leading markets such as Germany, the UK, and France. Strong EU regulatory frameworks mandate early diagnosis initiatives and incentivize investment in sustainable healthcare solutions. The region is adopting advanced imaging technologies and biomarker-based diagnostics at a rapid pace, particularly within tertiary hospitals. Novo Nordisk and Inventiva are notable players contributing to drug pipeline advancements. Regional consumers demonstrate high trust in therapies that adhere to transparent and explainable standards, reflecting a preference for safety and compliance. Increased funding for liver health research further bolsters adoption across hospitals and research institutes.

What factors are fueling rapid expansion across this market?

With a market volume accounting for 18% in 2024, this region is poised to become the fastest-growing hub by 2032. China, India, and Japan are the top consuming countries, with China alone recording more than 900,000 MASH cases under treatment in 2024. Infrastructure development, rising healthcare expenditure, and government-backed liver disease initiatives are fueling demand. Japan’s innovation hubs are pioneering AI-driven diagnostic tools, while India’s healthcare startups are piloting mobile-based disease management apps. Regional players are investing in affordable drug development, widening access. Consumer behavior is strongly linked to the rise of e-commerce-enabled healthcare platforms and mobile-based AI apps, driving early diagnostic adoption.

How is healthcare modernization influencing adoption patterns here?

Representing 7% of the global share in 2024, this region is driven by Brazil and Argentina, where government-backed health programs are improving patient access. Infrastructure improvements in urban healthcare centers are strengthening adoption of advanced diagnostic imaging. Trade policies promoting biopharmaceutical imports are easing access to innovative therapies. Local healthcare providers are adopting digital tools to support hepatology management. Consumer demand is largely tied to localized medical programs and culturally tailored patient education. This behavior aligns with regional needs for language-specific awareness campaigns and greater affordability, particularly in underserved rural areas.

What role do healthcare investments play in expanding this market?

This region accounted for 5% of the market in 2024, with UAE and Saudi Arabia driving adoption through national health missions and smart hospital initiatives. South Africa is emerging as a key hub with rising diagnostic infrastructure. Technological modernization, including cloud-based health records and AI-based imaging, is supporting adoption. Governments are promoting trade partnerships to expand access to advanced therapies. Local players are collaborating with international firms to establish regional clinical research centers. Consumer behavior highlights growing trust in hospital-based treatment, particularly in urban centers, though rural outreach remains a challenge.

United States – 34% market share: Strong R&D investment, advanced healthcare infrastructure, and leadership in clinical trials drive its dominance.

Germany – 12% market share: Regulatory-driven early diagnosis initiatives and sustained government support for liver health research reinforce its leadership.

The MASH Treatment market is moderately consolidated, with more than 40 active competitors operating globally in 2024. The top 5 companies collectively account for 54% of the total share, highlighting their strong influence on innovation and strategic direction. Madrigal Pharmaceuticals currently leads with late-stage drug development breakthroughs, while Gilead Sciences and Novo Nordisk continue expanding combination therapy pipelines. Pfizer and Inventiva are also actively engaged in large-scale clinical trials. Key competitive strategies include licensing partnerships, biomarker-based diagnostic collaborations, and joint ventures with digital health firms. Innovation trends are focused on RNA-based therapies, AI-driven patient monitoring, and cloud-enabled diagnostic solutions. Increasing M&A activity, particularly among mid-sized biotech firms, is shaping the competitive landscape. This market is characterized by high barriers to entry due to regulatory complexities, capital-intensive R&D, and intellectual property considerations.

Pfizer Inc.

Inventiva Pharma

Intercept Pharmaceuticals

Akero Therapeutics

89bio Inc.

Galmed Pharmaceuticals

Technology is playing a transformative role in shaping the MASH Treatment market, with several emerging innovations enhancing diagnostic accuracy, treatment outcomes, and patient engagement. Non-invasive imaging technologies, such as magnetic resonance elastography (MRE), achieved adoption in over 60% of advanced hepatology centers by 2024, reducing dependence on invasive liver biopsies. Biomarker-based blood tests are now implemented in 48% of tertiary care hospitals, providing faster and more reliable diagnosis. AI and machine learning are being applied to predictive analytics, helping physicians identify disease progression with over 85% accuracy.

Digital health platforms are revolutionizing patient management, enabling remote monitoring and lifestyle tracking for nearly 40% of patients undergoing treatment. Pharmaceutical companies are investing heavily in RNA-based therapies, which demonstrated 42% higher efficacy compared to traditional small molecules in clinical trials. Combination drug regimens are gaining traction, with over 70 global trials testing dual-mechanism therapies to improve patient outcomes. Additionally, cloud-enabled platforms are supporting cross-border clinical collaborations, allowing real-time data exchange between hospitals and research institutions. This technological convergence is not only improving efficiency but also reducing costs associated with trial delays and misdiagnoses. As adoption expands, technology-driven solutions will remain central to the evolution of the MASH Treatment market.

In February 2024, Madrigal Pharmaceuticals announced positive Phase 3 results for resmetirom, demonstrating a 27% improvement in liver inflammation reduction across more than 2,000 patients, positioning it as one of the most promising therapies for MASH. Source: www.madrigalpharma.com

In November 2024, Novo Nordisk launched a global liver health initiative integrating digital biomarkers, aimed at supporting more than 500,000 patients with early-stage metabolic liver disease. Source: www.novonordisk.com

In June 2023, Akero Therapeutics reported successful Phase 2b results for its FGF21 analog, showing a 31% improvement in fibrosis resolution in MASH patients across clinical sites in North America and Europe. Source: www.akerotx.com

In October 2023, Gilead Sciences entered a strategic collaboration with a leading AI health tech firm to integrate machine learning into MASH clinical trial design, reducing recruitment timelines by 22%. Source: www.gilead.com

The scope of the MASH Treatment Market Report covers a comprehensive analysis of global and regional developments across product types, applications, end-user adoption, and technological trends. It examines therapeutic categories such as small-molecule drugs, biologics, and RNA-based therapies, while also exploring diagnostic and monitoring applications including biomarker testing, elastography, and digital health platforms. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering region-specific insights on infrastructure, healthcare adoption, and consumer behavior.

The report also addresses diverse end-user categories, including hospitals, specialty clinics, research institutions, and outpatient facilities. Industry-specific drivers such as rising metabolic disorder prevalence, healthcare digitization, and regulatory reforms are thoroughly evaluated. Furthermore, the scope includes examination of emerging market niches such as mobile healthcare applications, AI-driven patient engagement platforms, and precision medicine-based therapeutic pipelines.

In addition, the report highlights innovation pipelines, ESG commitments, and regulatory frameworks shaping the adoption of therapies and diagnostics worldwide. It provides quantitative insights into market shares, adoption rates, patient volumes, and investment trends. This scope ensures a 360-degree perspective tailored to decision-makers, enabling them to understand growth pathways, competitive strategies, and evolving opportunities within the MASH Treatment market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1027.3 Million |

|

Market Revenue in 2032 |

USD 6006.6 Million |

|

CAGR (2025 - 2032) |

24.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Madrigal Pharmaceuticals, Gilead Sciences, Novo Nordisk, Pfizer Inc., Inventiva Pharma, Intercept Pharmaceuticals, Akero Therapeutics, 89bio Inc., Galmed Pharmaceuticals |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |