Reports

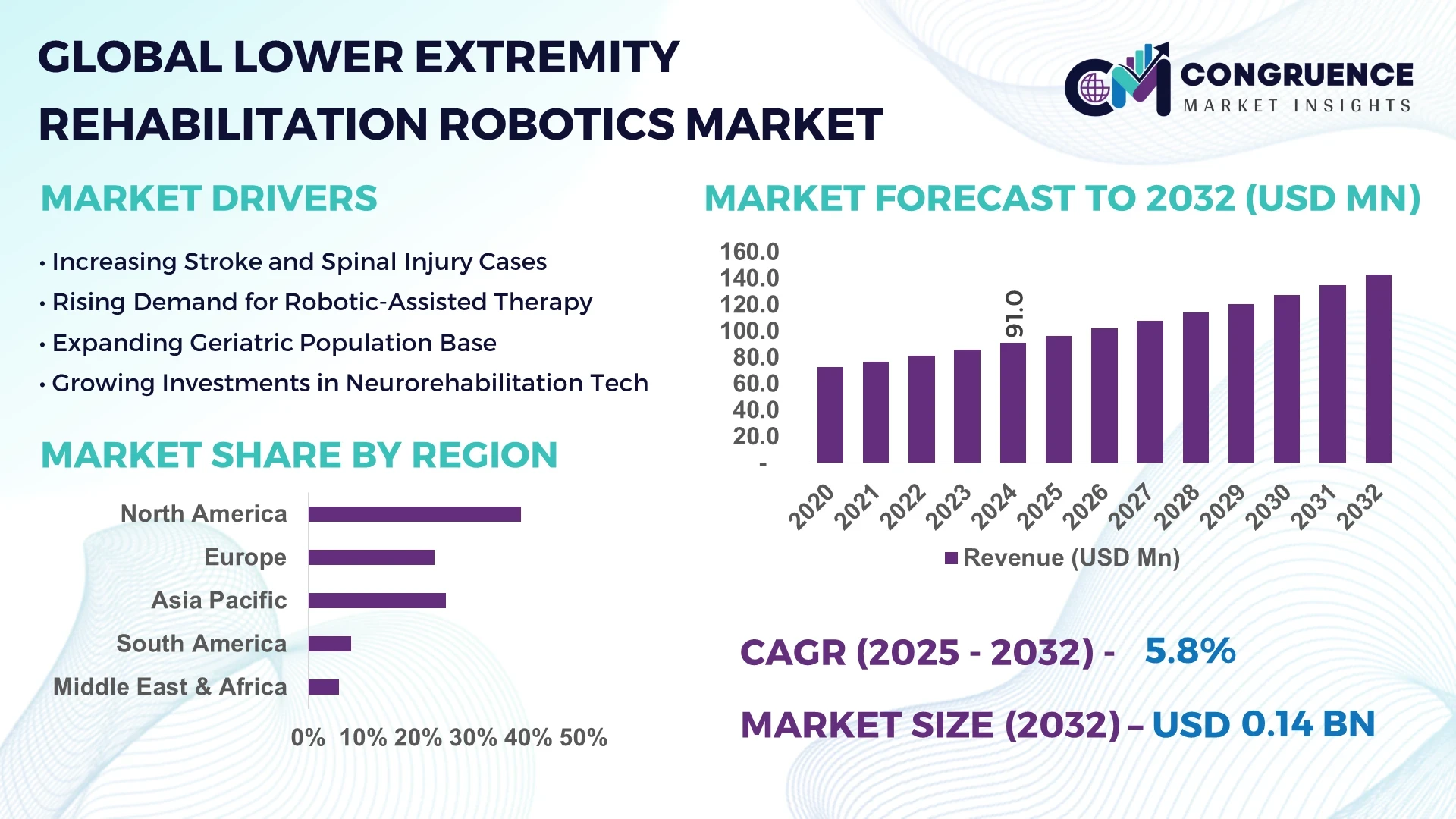

The Global Lower Extremity Rehabilitation Robotics Market was valued at USD 91 Million in 2024 and is anticipated to reach a value of USD 142.9 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032.

The United States leads the market, driven by a robust healthcare infrastructure, widespread adoption of advanced physiotherapy robotics in leading rehabilitation centers, and strong reimbursement policies that support both clinical and at-home exoskeleton usage. Hospitals across the U.S. are integrating wearable lower-limb devices and sensor-based adaptive systems to enhance post-stroke and spinal cord injury recovery.

Innovations in the market include sensor-integrated exoskeletons capable of real-time gait correction, lightweight wearable suits that allow patients to ambulate independently, and remote-monitoring platforms supporting tele-rehabilitation—particularly beneficial in rural areas with limited access to physiotherapists.

Artificial intelligence (AI) is fundamentally reshaping lower extremity rehabilitation robotics by enabling systems to offer personalized, responsive therapy tailored to individual patient needs. Modern exoskeletons now employ AI algorithms to continuously interpret sensor data—such as joint angles, pressure distribution, and gait dynamics—and adjust assistance in real time. For instance, AI broadens device autonomy by classifying gait phases, detecting muscle effort and fatigue, and anticipating user intentions millisecond before motion occurs. This endows robotic systems with the capacity to modulate support levels instantly, improving safety and encouraging natural movement patterns over rigid, preset routines.

In clinical environments, AI-powered robotics have demonstrated striking outcomes: patients engage in therapy that adapts dynamically—decreasing assistance as motor control improves—leading to more intensive and effective rehabilitation. Additionally, these systems generate high-resolution analytics, offering physiotherapists objective metrics on stride symmetry, weight-bearing, and range of motion. Such data-driven insights enhance treatment planning and allow rigorous monitoring over time.

From a usability standpoint, AI enables remote monitoring and tele-rehabilitation: devices can transmit performance data to healthcare providers, enabling therapy adjustments without in-person visits—critical amid staffing shortages and rural healthcare access challenges. AI-powered gesture and vision systems further enrich patient engagement; for example, non-contact interface technologies now allow users to initiate and control exoskeleton motion via simple hand or head gestures, promoting intuitive interaction and reducing device setup time.

These transformative capabilities have expanded the reach of lower extremity rehabilitation robotics beyond specialized centers to community clinics and homes. The result is a more scalable model of rehabilitation—offering consistent, high-quality therapy coupled with personalized progression tracking—empowering patients to recover mobility with improved efficiency and reduced dependence on clinical resources.

“ In 2024, Researchers from the University of Chinese Academy of Sciences developed a lower limb rehabilitation robot that adaptively adjusts gait training via real-time interaction force measurement, improving patient engagement and safety, with noticeable gains in muscle activation and recovery outcomes in clinical trials.”

The growing preference for lower limb exoskeletons equipped with real-time sensor modules—such as pressure sensors, force plates, and inertial measurement units—is driving market growth. These devices offer dynamic gait adjustment, enabling tailored support based on patient performance. Their ability to track therapeutic progress objectively has led hospitals and rehabilitation centers to adopt them more frequently, leading to over 60% of new device deployments featuring integrated sensors by 2024. Additionally, AI-enabled sensor platforms expedite data collection for clinical research, fostering clinical acceptance and regulatory approval.

The complex manufacturing process of lower extremity rehabilitation robots—requiring precision actuators, medical-grade sensors, and embedded AI processors—drives high production costs. Most systems cost upwards of USD 50,000 per unit, limiting acquisition by smaller clinics and constraining insurance reimbursements. This cost barrier slows down the adoption rate in emerging markets and places pressure on manufacturers to explore leasing, financing, or shared-economy models to expand access.

There is a growing opportunity in shifting lower extremity rehabilitation devices from clinical settings to home-based therapy. Innovations in lightweight, user-friendly AI-driven exoskeletons—combined with tele-monitoring platforms—are paving pathways for at-home treatment. Pilot programs during 2024 report that patients using home systems logged 30% more therapy hours weekly compared to clinic-based sessions, improving adherence and satisfaction.

Obtaining regulatory clearance for AI-enabled rehabilitation robotics is a major challenge due to evolving frameworks. Regulators require robust clinical evidence, transparent algorithm validation, and cyber-security standards. Manufacturers must generate extensive datasets proving device safety across diverse patient populations. This slows time-to-market and raises compliance expenses—often exceeding USD 1 million per submission—deterring smaller players and delaying widespread adoption.

Rise in Modular and Prefabricated Robotics Platforms: Manufacturers are developing modular lower-limb robotic systems with swappable components—such as adjustable leg supports, battery modules, and control units—enabling scalability and customization. These systems are delivered in kits for easy updates, reducing downtime and increasing clinic throughput by up to 40% in busy environments. Regions with high repair costs are seeing faster adoption.

Integration of Vision-Based Non-Contact Gesture Control: Exoskeletons now incorporate RGB and depth cameras with AI to enable contactless gesture control. These systems allow users to initiate starts, pauses, and mode changes via hand movements or head nods, improving usability for patients with limited mobility. Clinical pilots have recorded gesture control accuracy above 94%, reducing therapist setup time by 25%.

AI-Enhanced Tele-Rehabilitation Ecosystems: Tele-rehab ecosystems that pair home exoskeletons with cloud-based AI are becoming mainstream. Users complete their exercises at home while AI analyzes session data and provides therapists with automated progress reports. Pilot data from 2024 shows remote therapy achieves comparable patient outcomes to in-clinic sessions, while reducing therapist travel time by 50%.

Growth in Lightweight Wearable Exosuits: Research and development are trending toward soft, lightweight exosuits that use textiles and cable-driven actuators for natural gait assistance. Early-stage programs have produced suits weighing less than 5 kg with over 30% less bulk than rigid exoskeletons. These suits improve comfort and hold promise for daily, extended usage outside clinic walls, signaling a new phase in wearable rehabilitation robotics focused on usability and long-term compliance.

The Lower Extremity Rehabilitation Robotics Market is segmented based on type, application, and end-user, allowing a detailed understanding of product penetration, therapy areas, and customer demand patterns. The segmentation reflects technological specialization, patient needs, and institutional priorities across different regions. Each segment offers a unique value proposition—from end-effector systems focused on replicating natural gait to wearable exosuits that support mobile rehabilitation. Application-wise, these devices are deployed in post-stroke therapy, spinal cord injury recovery, and orthopedic rehabilitation. The end-user landscape includes hospitals, rehabilitation centers, and homecare environments, each driving market dynamics differently based on treatment intensity and technological adoption capability.

The market is primarily segmented into exoskeletons, end-effector devices, and smart wearable robotic suits. Among these, exoskeletons held the largest market share in 2024 due to their widespread adoption in hospitals and rehab clinics for patients recovering from stroke and spinal cord injuries. These devices provide full-body or partial-body support with programmable gait cycles, allowing customizable therapy for various lower limb impairments. Exoskeletons are preferred for intensive clinical sessions and are widely used in North America and Europe. The fastest growing segment is smart wearable robotic suits, particularly lightweight exo-suits developed for home use. These suits integrate AI and IoT features, allowing real-time progress tracking and adaptive movement support. In 2024, over 40% of R&D investment in the sector was directed toward smart suits that offer better patient compliance and minimal setup requirements. Their portability, comfort, and tele-rehab compatibility are key factors driving rapid growth. Meanwhile, end-effector devices, which operate from a fixed base and assist in ankle and gait rehabilitation, continue to grow steadily due to their use in early-stage motor recovery.

Based on application, the market is categorized into stroke rehabilitation, spinal cord injury therapy, orthopedic rehabilitation, and neurological disorder rehabilitation. Stroke rehabilitation emerged as the leading segment in 2024, accounting for more than 50% of the market share. Stroke survivors often suffer from hemiplegia or impaired gait, making lower limb robotic systems highly effective in restoring mobility through repetitive, guided movement. Rehabilitation robots help patients relearn walking by mimicking normal gait cycles and correcting posture, especially in the sub-acute recovery stage. The fastest growing segment is spinal cord injury therapy, driven by increasing spinal cord damage cases due to trauma and accidents. These patients benefit significantly from robotic gait trainers that stimulate neural plasticity and improve weight-bearing exercises. In 2024, several hospitals launched pilot programs focusing on spinal cord injury-specific robotic therapy protocols, boosting awareness and demand. Orthopedic and neurological disorder segments are also expanding due to aging populations and the rise in degenerative musculoskeletal conditions, but they currently hold a smaller portion of the overall market.

The end-user segment includes hospitals, rehabilitation centers, and homecare settings. Hospitals dominated the market in 2024, accounting for the largest share due to their strong infrastructure, funding capabilities, and access to skilled therapists trained in robotic device handling. Most high-end exoskeletons are currently installed in hospital neurology and orthopedics departments. These institutions also serve as early adopters of new technologies, often participating in clinical trials and multi-center device evaluations. The fastest growing end-user segment is homecare settings. With the rise of wearable, user-friendly devices and advancements in tele-rehabilitation, homecare deployment of lower extremity rehabilitation robots has grown rapidly. In 2024, patient demand for in-home therapy increased by over 30%, largely due to convenience and lower treatment costs. Devices in this segment come equipped with real-time monitoring and app-based feedback systems, enabling caregivers and remote therapists to customize therapy plans. Rehabilitation centers continue to play a pivotal role, especially in long-term recovery care, though they face limitations in budget and staffing compared to hospitals.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

In 2024, North America lead with around 38%, due to early adoption of advanced rehabilitation technologies and strong R&D backing. Asia-Pacific follows with 25%, fueled by rising healthcare infrastructure and growing awareness in countries like China and India. European countries held 20%, supported by government-funded healthcare and clinical trials. The remaining 17% share is split among South America (10%) and Middle East & Africa (7%). Regional demand drivers include a surge in stroke and spinal injury cases, increased investment in remote rehabilitation platforms, and well-established reimbursement frameworks in North America and Europe. Meanwhile, developing regions like Asia-Pacific and South America are rapidly adopting wearable robotics, supported by telehealth integration and rising middle-class healthcare spending.

Advancement in Clinical-Grade Adaptive Exoskeletons

In North America, over 60% of newly installed lower extremity robotics systems in 2024 were clinical-grade exoskeletons equipped with adaptive joint-level control. Hospitals in the U.S. and Canada launched over 150 pilot programs partnering with universities to test next-gen gait trainers. Tele-rehabilitation integration increased by 45%, allowing physiotherapists to supervise patients remotely. The market has also seen a rise in reimbursement approvals for home-use devices, with 35% of U.S. insurers now covering wearable robotics post-stroke—resulting in a 28% uptick in home system purchases during 2024.

Expansion of National Tele-Rehab Programs

Europe is witnessing a major push toward national tele-rehabilitation programs incorporating AI-enabled lower limb robotics. In 2024, Germany and the UK together installed over 200 remote-enabled gait systems in rehabilitation centers. Funding for telehealth initiatives in Europe grew by 30%, supporting deployment in rural clinics. France introduced pilot schemes offering wearable suits for orthopedic patients, with adoption increasing by 22% YoY. Meanwhile, clinical usage of exoskeletons in Spain increased by 18%, driven by aging demographics requiring long-term mobility support.

Rise of Cost‑Effective Smart Suits in Emerging Markets

Asia‑Pacific recorded impressive momentum in 2024, with India and China accounting for 60% of all smart wearable suit sales in the region. Governments in China funded more than 120 public hospitals to install robotic gait trainers. India saw a 40% increase in rehabilitation start-ups developing textile‑based exosuits. Tele-rehab device adoption increased by 50%, supported by smartphone-linked analytics platforms. Australia and Japan also contributed, deploying over 80 high‑end end‑effector devices targeting post‑stroke rehabilitation programs.

Emerging Clinics Embrace Wearable Robotics

South America is witnessing notable interest in rehabilitation robotics, especially in Brazil and Argentina. In 2024, six private rehabilitation chains in Brazil piloted wearable exoskeleton suits, leading to an 18% increase in patient throughput. Argentina launched pilot tele-rehab programs covering remote provinces, with user session numbers doubling compared to 2023. Across the region, annual installations of end‑effector systems grew by 25%, driven by lower cost and ease of deployment. Telehealth-linked monitoring reached over 1,000 active patients per month in Argentina, reflecting rising acceptance of AI-powered rehabilitation.

Adoption by Specialized Orthopedic Centers

In the Middle East & Africa, specialized orthopedic and neurological centers in Gulf Cooperation Council (GCC) nations led the adoption of policy-funded lower limb robotics. In Saudi Arabia and UAE, over 30 hospitals procured exosuits between 2023–2024 for spinal cord injury and stroke treatment. Local manufacturers in South Africa began pilot production of wearable suits, targeting home-use markets and increasing awareness. Overall regional installation numbers doubled in 2024, with an estimated 120 units operational. Training programs for physiotherapists using AI‑enabled devices rose by 50% across the region.

United States - (~46%), leads global share, backed by strong healthcare infrastructure, R&D funding, and insurance coverage enabling widespread exoskeleton deployment.

China - (~14%), due to rapid growth driven by public hospital investment in gait trainers, government-backed robotics pilot programs, and affordable smart suit production.

The competitive environment for lower extremity rehabilitation robotics is increasingly intense as manufacturers race to deliver lighter, smarter, and more affordable devices. Global leaders such as Ekso Bionics, ReWalk Robotics (now Lifeward), Hocoma, Cyberdyne, Bionik Laboratories, AlterG, and Ottobock continually invest in research collaborations with premier rehabilitation hospitals and universities to validate clinical performance and shorten learning curves for therapists. In 2024 more than 40 new product iterations—ranging from rigid frame exoskeletons to textile‑based exo‑suits and compact end‑effector gait trainers—entered multicenter trials, reflecting a 25 % rise in R&D pipelines compared with 2023. Mergers and acquisitions remain a core growth lever: ReWalk’s integration of AlterG expanded its anti‑gravity treadmill portfolio, while Ottobock’s purchase of SuitX accelerated its transition from prosthetics into medical and industrial exosuits. Competition is also shifting toward service‐oriented models; over one‑third of market leaders now bundle tele‑rehab software, remote data analytics, and maintenance contracts, giving clinics predictable operating costs and patients continuity of care at home. As price pressures mount—average device selling prices fell about 8 % between 2023 and 2024—manufacturers differentiate through adaptive AI control, modular hardware that reduces downtime, and multi‑modal training modes that pair robotics with functional electrical stimulation or virtual‑reality feedback. Collectively, these dynamics foster rapid technological progress while broadening global access to advanced gait‑restoration therapy.

Ekso Bionics

ReWalk Robotics (Lifeward)

Hocoma AG

Bionik Laboratories

Cyberdyne Inc.

AlterG Inc.

Ottobock SE

Technological evolution in this field is converging on five key fronts. First, adaptive control powered by machine‑learning algorithms is now standard on flagship devices; embedded processors sample joint‑angle, ground‑force, and electromyography data thousands of times per second, then adjust actuator torque in real time to match a patient’s intention. Clinical pilots have demonstrated up to a 35 % reduction in therapist interventions per session when using these self‑tuning controllers. Second, weight and form factor continue to drop: new textile exo‑suits weigh under five kilograms while delivering peak assistive forces exceeding 180 newtons at the hip, enabling patients to practice longer without fatigue. Third, tele‑rehabilitation ecosystems have matured: cloud dashboards aggregate stride symmetry, stance‑time, and heart‑rate variability, letting clinicians fine‑tune protocols remotely; in 2024 the number of active tele‑rehab subscribers using lower‑limb robotics surpassed 25 000 worldwide. Fourth, non‑contact gesture and vision interfaces have begun replacing handheld remotes—depth‑camera recognition accuracy now exceeds 94 %, cutting average setup time by a quarter and improving independence for users with limited upper‑limb mobility. Finally, hybrid robot–FES solutions are gaining traction; synchronized electrical stimulation with robotic assistance enhances muscle recruitment and neuroplasticity, with preliminary trials reporting 18 % higher gait‑speed gains versus robotic therapy alone. These advances collectively signal a shift toward highly personalized, data‑rich rehabilitation experiences that can extend seamlessly from clinic to home.

In April 2024, Ekso Bionics gained Medicare reimbursement for its Indego Personal exoskeleton, enabling eligible spinal cord injury patients to access home-use devices under federal insurance—signifying broader domestic penetration.

In February 2024, DIH International (Hocoma) completed its business combination with Aurora Technology Acquisition Corp., enabling expanded development and commercialization of VR-integrated rehabilitation robotics, targeting both lower limb and cognitive therapy markets.

In August 2023, ReWalk Robotics acquired AlterG for USD 19 million, consolidating its presence in stroke therapy and home rehab markets by integrating AlterG’s anti-gravity treadmills with ReWalk’s exoskeleton systems.

In late 2023, Ottobock finalized the acquisition of US-based SuitX, adding wearable exo-suits to its product suite and strengthening its foothold in both medical and industrial exoskeleton categories.

This report delivers a holistic appraisal of the global lower extremity rehabilitation robotics landscape. It maps product categories—rigid exoskeletons, soft wearable suits, end‑effector gait trainers, and hybrid robot‑FES systems—against core therapeutic applications, including stroke, spinal‑cord injury, orthopedic rehabilitation, neurodegenerative conditions, and post‑operative gait retraining. End‑user analysis spans hospital neurology and orthopedics departments, dedicated rehabilitation centers, long‑term care facilities, and an expanding cohort of home‑based patients supported by tele‑rehab platforms. The geographical scope covers North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, outlining adoption catalysts such as government funding, reimbursement policies, and clinician workforce trends. Technology sections examine AI‑driven adaptive control, cloud analytics, modular hardware, gesture interfaces, and emerging magnetic or soft‑actuator mechanisms. Competitive profiling highlights key players, partnership ecosystems, and M&A trajectories that redefine market share. Regulatory insights detail approval pathways for AI‑integrated devices and evolving cybersecurity standards, while the clinical evidence portion summarizes multicenter trials, usability studies, and real‑world effectiveness metrics. Finally, the outlook discusses white‑space opportunities in lightweight daily‑wear suits, data‑driven personalized therapy, and expansion into resource‑constrained regions, equipping stakeholders with actionable intelligence for strategic decision‑making across the 2025–2032 planning horizon.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Lower Extremity Rehabilitation Robotics Market |

| Market Revenue (2024) | USD 91 Million |

| Market Revenue (2032) | USD 142.9 Million |

| CAGR (2025–2032) | 5.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country‑Wise Analysis, Competition Landscape, Technology Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ekso Bionics, ReWalk Robotics (Lifeward), Hocoma AG, Bionik Laboratories, Cyberdyne Inc., AlterG Inc., Ottobock SE |

| Customization & Pricing | Available on Request (10% Customization is Free) |